Recent national media, Facebook, and personal interactions served as the catalyst for these posts on taxes. There is a lot of misinformation and misunderstanding of the way things work, which create opinions and divisiveness not necessarily based on fact.

First, let’s talk about tax brackets and the key word for the American tax system: marginal tax brackets.

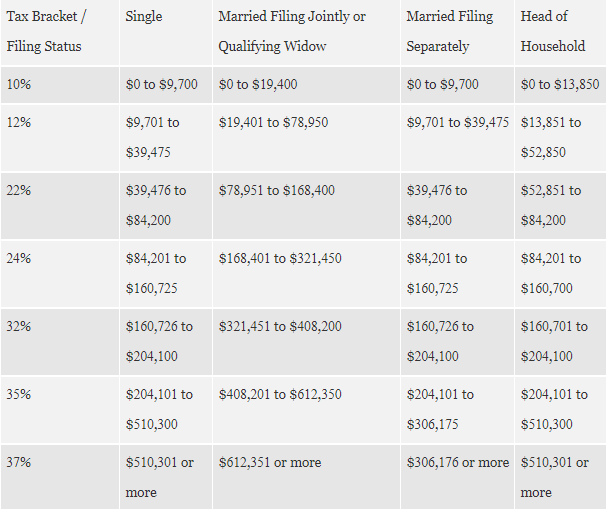

In 2019 there are 7 tax brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Each of these brackets has varying dollar thresholds for the 4 filing statuses: single, married filing separately, married filing jointly, and head of household. Once you establish under what status you are filing, you know where each dollar you earn will fall in the brackets on the chart.

What I’ve heard many times before, and still see implications of misunderstanding in the media, are folks that think that the last, or highest, dollar you earn is what dictates what tax bracket you fall in. This is incorrect.

In 2019, single filers get taxed on 10% of their income up to $9,700. That means that the first dollars they earn are taxed at 10%, but the $9,701st dollar they earn is taxed in the next bracket, or 12%. The 12% bracket goes to $39,475. Similarly, the $39,476th dollar they earn will be taxed at 22%, and so on.

Individuals that say they do not want that raise, or to make more money, because it would put them in a higher tax bracket are sorely mistaken. Yes, the higher dollars they earn would be taxed more, but those dollars do not suddenly make all the lower amount of dollars be taxed at the high rate too. Those lower amounts stay in the marginal brackets they already were being placed in, based on the way the charts work.

Another single filer example (simplified for easier illustration). You make $80,000, which is the 22% bracket. Taxes for the year are figured as follows.

10% for $9,700 = $970

12% for $9,701 to $39,475 = $3,573

22% for $39,476 to $80,000 = $8,915

For a total tax liability of $970 + $3,573 + $8,915 = $13,458

If you make $80,000 and have to pay $13,458 in taxes, that is 16.8% of your income, not the 22% that the “tax bracket you fall in” might create the perception of.

Say you get a $10,000 raise to $90,000.

We know an $80,000 salary pays $13,458. Let’s add the taxes for the final $10,000.

$4,200 of that is still in the 22% tax brackets, so we can multiply = $924

$90,000 minus $84,200 = $5,800 in the 24% bracket = $1,392

So total taxes are $13,458 + $924 + $1,392 = $15,774.

That represents 17.5% of your income of $90,000 being paid to taxes, not the whole 24% bracket.

If we did not have marginal tax brackets and that raise really did bump all of your dollars up, or if it was calculated in a manner that many Americans think it is, then $90,000 times 24% = $21,600. It would look like your $10,000 raise caused you to pay $8,142 more taxes.

Good thing it doesn’t work that way!

2 thoughts on “TAXES! Part 1 – What are Marginal Tax Brackets?”