Spring is a time for lease renewals or preparing to re-rent a house.

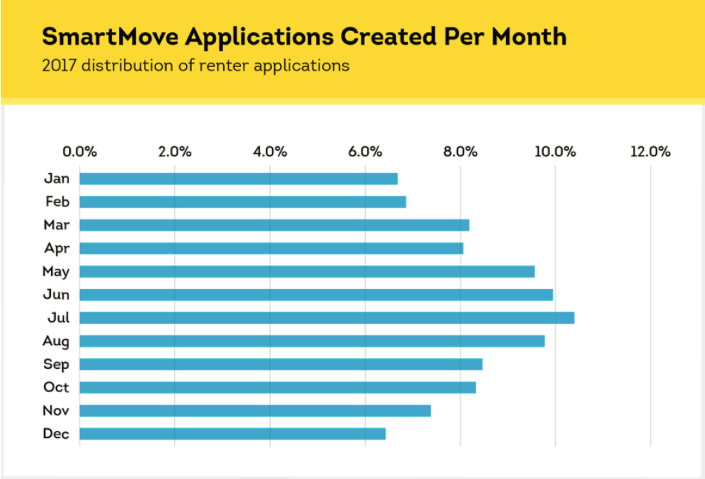

Spring and Summer are times when people are most active in the real estate market. It’s the best time to be listing your house for sale and for rent, which may yield you a better sale/rent amount because of greater competition. This timeframe is likely most active because of the better weather for moving and the school year – if a family is looking to move, they’re more likely to do it when they don’t have to transfer their kids to a different school district mid-school-year. Personally, when I was in college, nearly all the rentals were available in May or June. I remember being frustrated that I couldn’t get an August lease and had to pay for the summer months even though I’d be back living at my parents’ house. Now that I’m older and have more experience, it all makes sense. Below, you can see the increase in applications processed by SmartMove (the way we process tenant applications) that occur during the summer months, which indicates the most active time in the market.

We have seen this reflected in our days-on-the-market and rent prices. When we can list a house in the Spring months, we’re able to get it rented with very few days vacant. Houses that we’ve closed on at the end of the Summer (when school starts) and in the Fall have taken us more time to find a tenant, and we’ve had to reduce our asking monthly rent amount.

For those houses that we had purchased in a less-opportune time of year, we’ve worked to get them back to a Spring-time market for renewal.

- We purchased two in September 2019 that we weren’t able to get rented until November 1st that year; we offered those tenants an 18 month lease so that their lease expiration would become May 31st.

- We did similar with a house that we purchased in August. After that first year, a prospective tenant tried negotiating the list price for rent, and we said we were willing to reduce the rent a bit for an 18 month lease; they agreed, and we got our rental on a Spring renewal.

- We recently had a tenant break their lease (with our concurrence), so that house has a lease expiration of October 31st now. We intend to offer a 6 month lease term to that tenant when the time comes.

With that said, we have lots of activity at this time of year.

We have 9 houses in Virginia and 3 in Kentucky. These markets are so different for us. We do our best to work with our tenants to encourage them to continue renting with us. I wrote about this in detail in my Tenant Satisfaction post.

Here’s a break down of how we handled all the leases that are expiring at this time of year.

In Kentucky, one lease was set to expire at the end of April and another at the end of May. These two properties are under a property manager. She attempted to increase the rent for a new lease term, but the tenants pushed back. Landlords don’t have a lot of leverage in a pandemic. Since the property manager is the one who handled the communication, I don’ t know what the details were. We believe both these houses are rented for less than market value, so that’s unfortunate. But, we’re grateful that both tenants renewed their lease for a year, so we don’t have to work to turnover the houses. Within reason, we’d always rather rent for a few bucks under market value than to handle turnover and lost rent (vacancy) by trying to maximize monthly cash flow.

In Virginia, we have an array of situations. Richmond was quick to acknowledge the property value increases that have occurred over the last year or so. This means that they increased our assessments, which effectively increases our property taxes.

We have the first two properties that we bought in that market, which are next door to each other and both have long term tenants (one since we before we purchased it, and the other is the second tenant who moved in a year after we purchased). We inherited their rent at $1,050, and then we increased it to $1,100 two years ago. With the property assessment increases, it was time to raise their rent again for this July. I initiated a letter to each of them stating the rent will increase as of July 1, which gave two options: they could leave the property by June 30th in accordance with their lease, or they could sign on for another year at the increased rent rate. Both chose to stay in the property, and they signed another year at $1,150. This is still below market value for the houses, but we’re happy with the lack of maintenance needs in these houses over the last 5 years. We’re in the middle of replacing the flooring in one of the houses. That house has a family of 5 and a dog living in it, so it’s not surprising that it’s worn out faster than the identical one next door with one person in it.

We have a 2 bed, 1 bath house that rents at $795. She’s been in the house since July 2018, which means that her lease ends June 30th of this year. Based on the 1% Rule (i.e., we’re looking for the monthly rent to be 1% of the original purchase price) for this house, our rent goal is $635. Since we’ve exceeded that goal for the life of our ownership, and the house hasn’t cost us much in maintenance, we chose to not increase her rent if she wanted to renew for another year, which she did. She has also spent some of her own money to spruce up the house and make it her home, and we recognize the value to us that her efforts also bring.

Another house reached out to us and asked if we were willing to renew her lease for another year. She’s been there since we purchased the house in 2017, and we’ve never increased her rent. She usually pays rent early and doesn’t ask for anything. The 1% Rule puts us at $660, and we’ve been collecting $850. Since we’ve been lenient on rent increases, I thought it a good idea to re-evaluate her terms. I plugged all the numbers into Mr. ODA’s calculation sheet to see how we were doing since the taxes increased so much on this house. Our cash-on-cash return (which we aim to be at 8-10%) came back at 19.8%. A rent increase for the sake of increasing rent isn’t worth it for such a good tenant, so we agreed to renew her lease for another year at the same rent. She wrote back: “omg thanks so much for the good news!” Happy tenants = good tenants, remember?

As for the others that I haven’t mentioned:

- Two of our houses were put under a two year lease last year, so they didn’t require any action from us this year.

- We have another house in KY that has a lease ending 7/31 and is under a property manager. We’ll offer a renewal option for them (i.e., we’re not interested in asking them to leave), but we haven’t worked out those details yet. Since we’re very hands off for our KY houses, we don’t know the satisfaction level of those tenants to gauge. Historically, we’ve had trouble renting this unit, costing us long vacancy times, so if we can renew their lease for even the same rent, we’re happy. Plus, having a 7/31 end date starts pushing us closer to the Fall for any future year-long rental agreements.

- One of the houses that we have with a partner has a difficult tenant. I mention the tenants almost every month in the financial updates because they don’t pay their rent on time, and getting information out of them is like pulling teeth. They’ve rented there long before we owned the property, and their rent has always been $1,300, which is well below market value. We plan on offering them a drastic rent increase and a new lease term (we’re still managing under the previous owner’s lease agreement) in July for their September 30th expiration term.

While we don’t have any houses to turn over, we’re going to get into each house this summer. Since so many of our houses don’t typically have turnover, we don’t get into them as often as we should to make sure things are running correctly (i.e., don’t want small issues to go unnoticed and cost us in the long run). Specifically, we need to make sure that the HVAC filters have all been changed and verify there aren’t any red flags. I plan to give the tenants at least a month’s notice before we enter, so that if there are any maintenance activities they should have been performing, they have time to get it situated. I’ll walk through with our typical move in/out inspection form and note any concerns or areas of interest. I also understand that by being visible, I’m opening myself up to being asked for things that a tenant may not necessarily ask for via email or text, but I’ll cross that bridge when I come to it. For now, we’re just grateful that we have no houses to turn over and no expected loss of rental income for the year thus far!