Surprisingly, I didn’t cover all our houses in posts last year. I was going to say, “let’s finish this up,” but we’ve since purchased #14! This is a long post. I tried to separate the stories, but since they were part of the same purchase, it was too convoluted to decide which story went with which house.

We spent the summer of 2019 living in Lexington, KY. Mr. ODA took a temporary job for 3 months, and we spent our summer looking for more rental properties to try another market. The housing costs in central Kentucky were less than central Virginia, but the rental rates were also lower.

We drove around with our Realtor for quite some time. We were hoping to find a multi-door complex. However, 4-8 door units have just not been well taken care of. We take care of our houses, and I didn’t want to inherit all the deferred maintenance of a poor landlord. Many of the places had long-term tenants, so there wouldn’t be a vacancy to ease getting work done either. Additionally, there were several that we saw where the tenant was home, smoking and telling us all that was wrong with the property. It was abysmal.

So after searching through many other options, we settled on two houses at the same time.

FIRST OFFER

Mr. ODA actually made an offer on a house in Winchester that I hadn’t seen. It was a large house that had been converted into 2 units. Mr. ODA and our Realtor went after work one day, and it wasn’t worth me packing up the baby and driving a half hour to meet them for one house. However, I did get to see some of it because I took on the home inspection appointment. Since I had never walked through the house, it was easy for me to objectively see the information on the inspection and convince Mr. ODA to walk away. There was just too many big-ticket items (e.g., not enough head room for stairs, water damage not properly cleaned up in multiple rooms, several code violations) and deferred maintenance that it wasn’t worth us putting the money into it. The tenants were sitting on the porch smoking during the inspection, and I didn’t love the idea of inherited tenants that were allowed to smoke in the house.

SECOND OFFER

I can’t tell the history of these purchases without this gem of a story. Mr. ODA found a house that was in a decent shape in Winchester.

Aside: We focused on Winchester because while the rent income was low, the housing cost was also low. Whereas in Lexington, the rent was low, but the housing prices were higher.

We made an offer on the house. In the offer, it lists the seller’s name. It was a State Senator! When we sent over the offer, the seller’s agent agreed to our details, but asked for a pre-approval letter before he’d sign. The amount of weight the people in Kentucky put on a pre-approval letter is absurd, in my opinion. We went through the effort to get the letter and send it over. About that same time, the seller’s agent said someone else came in with a better offer, so we could either submit our highest and best offer, or lose the deal. The sketchiness of the action floored us.

The house had been on the market for a month. We had a verbal agreement (that had even been put in writing, but not yet signed). What are the odds that someone came in at the same time as us with an offer over asking for a house on the market a month? We called his bluff, and we were wrong.

THIRD AND FORTH OFFERS – UNDER CONTRACT

In August 2019, we went under contract on two houses in Winchester, KY.

Property12 had been owner occupied and flipped to sell. The owner had lived there long enough that she wouldn’t Docusign the contract, and we had to wait for her to initial, sign, and date all the pages by hand. The house had been listed for 36 days when we made the offer. It was listed at $115,000, and we went under contract at $112,000 with $2,000 in seller subsidy (closing costs) on 8/7. It’s a 3 bed, 2 bath ranch at 1120 sf.

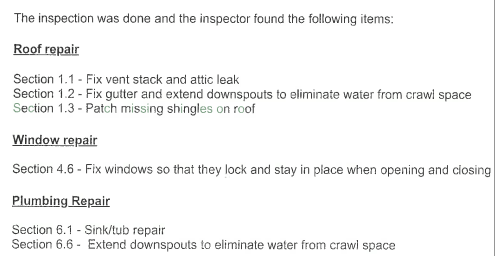

We received the home inspection on 8/14. We asked for the items below to be addressed, or to take $1000 off the purchase price. They agreed to fix the issues.

Property13 had been listed for nearly 3 months before we made an offer. It had been most recently listed at $105,500. Our offer was for $102,000 with $2,000 seller subsidy. We also included the following requirement in the contract: Seller agrees to remediate the water and mold in the crawl space, fix the down spout next to the crawl space door so that it channels the water away from the home, replace the missing gutter on the front of the house, and repair the rotted facia and sheathing on the front of the house.

Additionally, we had a home inspection on the house and identified the following items for them to repair.

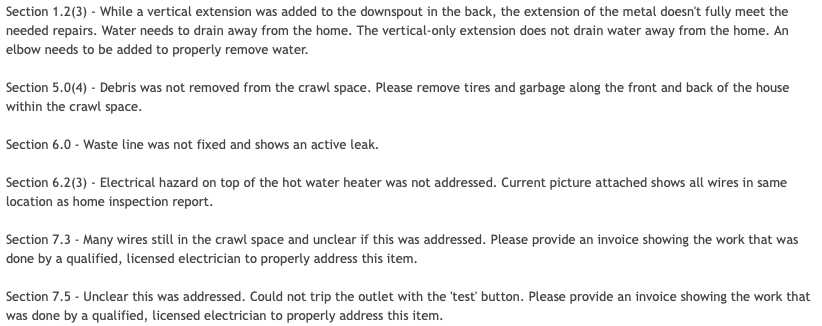

Getting the sellers to identify that these items were done before closing was not an easy task. We checked the day that closing was originally schedule for and noted that several things were not complete.

Then, at 7:30 pm the night before closing (which had already been delayed a week), we received one receipt identifying a couple of things were done. Eventually we received documentation that it was taken care of.

LOAN DETAILS

The options we typically ask for when considering the direction of our loan are as follows.

We chose the 25% down – 30 yr fixed option for both properties. Our goal is to not pay points, so that led us to the 25% down options. Since there was no incentive to take a shorter term (thereby increasing your monthly mortgage payments and decreasing your cash flow), we chose the 30 year option.

These loans were originated in September 2019. We processed multiple cash-out-refinances on some of our properties in December 2021; we used it to pay off about $66k on Property12 and about $74k on Property13.

LOAN PROCESSING & DELAYED CLOSING

We had a lender that we loved in Virginia. She couldn’t cover loans in Kentucky, but the company itself had a branch that could do it. She referred us to someone in Kentucky. It was the worst experience I’ve had in closings. Our closings are always annoyingly stressful in that last week, but this was bad throughout the month and then bad enough that our closing was delayed a week – completely due to the loan officer’s inability to manage the loan.

We had multiple issues over the course of the week we initiated our relationship just accessing the disclosures. They kept telling us to sign things we didn’t receive, or they’d tell us our access code and then when I say it doesn’t work, act like they never told us different information and give new information.

On August 16, I had to tell the loan officer that one of the addresses was wrong. THE ADDRESS. On August 26, we received conditional approval of our loan from underwriting. On August 27, we received our appraisal with no issues noted. But at that point, our August 30 closing was delayed a week already.

That’s where the problem was – our appraisal was ordered late, had to be rushed, and still didn’t make it in time for them to develop the Closing Disclosure (CD) and get us to a closing on August 30. The loan officer never once acknowledged that he ordered the appraisals late, causing this delay. It took asking for timelines from his supervisor, and piecing together emails we had on hand, to show that it was his fault.

On August 29, I finally made contact with the loan officer’s supervisor and was rerouted to someone else to get the job done. I had to repeat all of our issues and the errors that were found on the CDs.

On September 3, I was given disclosures that were still wrong. The new loan officer claimed that what she put in the system was correct, so she wasn’t sure what was wrong, causing me to once again outline all the errors.

On September 4, I was asked for more documentation that wasn’t caught during underwriting. I was furious.

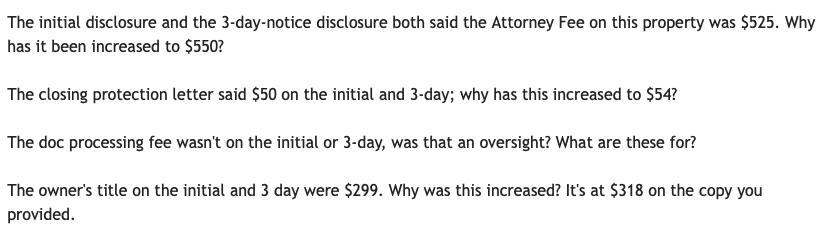

On September 5, I gave up talking to our lender about issues on the CD and spoke directly to the Title Attorney’s office, who was much more knowledgable and responsive. Here’s an example of what I’m questioning when I look over a CD. Some of these seem small (e.g., $4 difference, $25 difference), but you can see how these add up, both on a single transaction and when we’re processing several homes in one year. Not to mention – why pay more for something than you were quoted or you’re supposed to?

Another surprise that came our way was a “Seller Agent Fee” for $149 per transaction. At no point in time was an additional fee disclosed to us by our Realtor. A typical transaction has 6% commission paid by the seller, which is traditionally split 3% and 3% for the buyer and seller representation. Being that these were Rentals #12 and 13, in addition to 2 personal residences we had purchased, imagine the surprise when we, as buyers, were being charged for representation. We questioned why this wasn’t disclosed to us up front as a Re/Max requirement, and it was taken off our CD.

CLOSING DAY

I had planned to leave town the Friday after the original closing date because that was the last date that we had our apartment. I didn’t want to move me and the baby into my in-laws house and continue the poor sleep we had been dealing with by not being at home. So even though closing was delayed, I left. Mr. ODA had to be my power of attorney. He had to sign his name, write a blurb, and then sign my name on ALL those papers that are part of a closing….. times two. Eek. I didn’t know that at the time (but baby went back to sleeping perfectly once we were home, so it was worth my sanity 🙂 ).

At 11:30 am on closing day, the lender claimed that the power of attorney documents (from the lawyer…) were not complete enough to be counted as filed on their end. I appreciated the snip from the attorney when questioned.

I always wondered why tv shows always showed both at the closing table with a ceremonious passing of the key. We’ve had our share of weird closings (in a closet, in a parking lot, at our dining room table), but we never sat at the table with the seller in Virginia. We were so confused about how specific the closing attorney was being about the closing time options, and then we found out that the seller and buyer are at the table together in Kentucky. The seller for Property12 was so rude to Mr. ODA through the transaction! She kept grilling him on whether he addressed the utilities. The seller shouldn’t be allowed to talk to the buyer! We’ve since been able to process 3 transactions in Kentucky and avoid the seller at the table, but I’d like to advocate that Kentucky move away from this buyer/seller meeting process!

RENTAL HISTORIES

Property12 was listed at $895 on 10/2. Based on my birds-eye-view of the area, I thought $1000 was going to be easy to rent it at. Based on the 1% Rule that we had followed in Virginia, we should have a goal of $1,100 per month. However, we were trying for a Fall lease, which is more difficult than a Spring lease, so I thought listing at $995 would get quick movement instead of letting it sit for too long. Our property manager disagreed. She also said we were limited our pool of candidates by not allowing smokers; but, the whole house is carpeted and I was not budging on that.

We found a tenant on October 16 and allowed her to move in right away, but not start paying rent until November 1 if she agreed to an 18 month lease (we really wanted to be on a Spring renewal going forward). That was an unfortunate blow to our expectations – nearly two whole months without rental income on a house we didn’t need to do any work to.

We increased rent to $950 as of 6/1/2022 after no previous increases.

Property13 was listed for rent at $995 with no movement. We dropped to $875 and offered free October rent for however long was remaining in the month. A lease was established on 10/18/2019. Our property manager was supposed to establish an 18 month lease and didn’t. Luckily, the tenant agreed to a 6 month extension.

Property13 renewal came in April 2022. She had balked about the state of our economy in 2021, and we backed off the proposed increase at that time. Well, all the jurisdictions finally jumped on the increased assessments, and we saw a drastic increase in our costs. We told her that the new offer for a year lease is $950, which is higher than we’d typically increase in one year ($75 instead of $50). But we told her that we were willing to let her walk if she didn’t agree to it since she originally negotiated a lower cost and argued an increase at the 18 month mark, which we let go. She tried to fight it, but our property manager told her to check the rental options in the area to see that she’s still getting a deal. She agreed to the increase.

MAINTENANCE HISTORIES

Property12 requires a new heat pump in June 2021. We paid $3900 for a whole new system, which is a funnily low number just a year later.

The tenant there complained of high water bills. I asked to see a history of the water bills to know how much was considered higher than their average usage. The property manager agreed that the toilet was running and causing higher bills, but also admitted that they attempted to fix the toilet twice over a 3 week period, with multiple days between receiving a maintenance request and taking action. While I agreed that we could compensate her for the issue, I couldn’t quite pinpoint why this was my financial burden and neither the tenant’s nor the property manager’s. I followed up with more information from the property manager with questions like: Why did it take the tenant from 9/20 until 10/11 to identify the issue still remained and that there was a waste of water? They indicated that they believe they made a good faith effort to address the issues as reported. I eventually settled on a $25 concession on one month’s rent.

Property13 had several issues with the hot water installation that were eventually resolved, which was frustrating after we tried to manage issues with the hot water heater through the home inspection process and received documentation as if it was complete. The tenant requested pest control in July 2020 claiming that a vacant house next door caused an increase in pests. I was frustrated because that’s not how it works. I approved treatment at that time, and then she came back with another request in October. Luckily, I haven’t heard about pests since then. In my Virginia leases, we’ll handle some pest control requests, but if there are roach issues once a tenant has been there for some time, we don’t typically pay for that type of treatment.

SUMMARY

All in all, these tenants have been pretty quiet. They ask for random maintenance things here and there, but they’re not usually big-ticket items (except that HVAC replacement!). Our property manager has been more difficult than the tenants.

Being that we were used to the 1% Rule when we purchased these houses, it’s unfortunate that even at 3 years in, we’re not renting it at 1% of our purchase prices. Our cash-on-cash isn’t completely accurate right now because I won’t see our taxes for this year for another month or two. Being that jurisdictions kept the tax amount steady through the pandemic, I’m expecting to see an increase in assessments for this year. I’ve also seen big increases in our home insurance policies, so that will probably eat into our cash flow as well. Our cash-on-cash analysis on Property12 is about 6.5%, and it’s about 7.5% on Property13. These numbers are only slightly lower than our expectation/desire, with our average being about 8%.

In the upcoming year, we’re going to look to get rid of our property manager, so these houses may begin needing more attention from us. It’s been hard to take on more when paying a property manager has been a sunk cost at this point. However, the frustration of managing their management (e.g., making sure charges are correct, not getting a full picture of what work is being done, and then paying them a significant amount of management money and leasing money only for them to claim that checking on the property requires additional fees) has led to us wanting to take it on since we’re in town now. The current lease terms are up in April and May, so if we’re going to take on management, it should be before the possibility of paying them half a month’s rent for leasing it (not to mention they’re notoriously 4-6 weeks out in every leasing attempt they’ve done for us, whereas I’ve never had an issue getting a property leased within a week).