There’s a company in Virginia that advertises no-closing-cost-refinances. If it’s your personal residence, then this holds true. For investment properties, there are some closing costs, but it’s cheaper than the usual refinance. We used them for two other loans – one at the beginning of the pandemic when we signed the paperwork in a tent in the parking lot, and another where we signed the paperwork at our kitchen table in Kentucky with a traveling notary (that’s a thing!).

There was a threshold requirement in order to qualify for this refinance, and that was the new loan had to be at least $100,000. Only 2 of our houses had a loan originated for over $100k originally, so that limited our abilities.

Mr. ODA came to me and said he wanted to do a cash-out-refinance. This company had changed their policy, and they’d allow a cash-out-refinance to get us to the 100k threshold. The first two Virginia houses we purchased (2016) had balances of about 70k and 60k. We had enough equity in these houses that we could take a substantial amount out in the refinance, but Mr. ODA chose $50k each.

Here’s a run through of the thought process on how to do this and why it’s a benefit. I personally like seeing the details behind other’s decisions, so hopefully this will help someone or help make the concept click and open up an opportunity. This process was only just initiated, so I’ll do an update after we execute the plan to see how it changed.

The original goal was to use that money to pay off another loan. We’ve made our decision on which loan to pay off based on the highest interest rate. Right now, our highest interest rate is a loan with our partner at 5.1%, but this is also the loan that we’re actively paying off (leaving a balance right now of 26k, which we’re responsible for half). Since we need to time our principal payments to be matched with our partner, we can’t just dump money into this loan without really complicating things. So our second-highest interest rate is 4.625%. This loan originally was $89k in 2017 and has a balance of $62k. If we paid this off, that would leave about $35k in cash (based on the other two loan refinances that we’d take $50k out of each) that we could use to pay towards another loan or earmark for another purchase. As this discussion happened, Mr. ODA pivoted.

This company is only available to refinance loans in Virginia. Instead of paying off that $62k loan for a Virginia property, what if we also refinanced that loan and paid off one of two loans remaining on our Kentucky houses? I’m a visual person and needed to see how this would actually play out.

The terms were that if we picked a 15 year loan, that brings the interest rate down to 2.5%. With a 30 year loan, it’s 3.125%. I compared the current amortization schedule to the proposed amortization schedule, and here they are. Note that the interest isn’t a one-to-one comparison because we’ve already paid 4-5 years of interest on these loans.

HOUSE 2

The original loan terms were a 20 year at 3.875%.

The new terms would create a new 15 year loan, reduce the rate to 2.5%, and increase the loan to about $123k (pay off old loan, fees for closing, and $50k cashed out). This decreases our monthly cash flow, on this property, by $294.38.

HOUSE 3

The original loan terms were a 15 year at 3.25%.

The new terms would create a new 15 year loan, reduce the rate to 2.5%, and increase the loan to about $113k (pay off old loan, fees for closing, and $50k cashed out). This decreases our monthly cash flow, on this property, by $155.89.

HOUSE 8

The original loan terms were a 30 year at 4.625%.

The new terms would create a new 30 year loan, reduce the rate to 3.125%, and increase the loan to about $ (pay off old loan, fees for closing, and $35k cashed out). This is slightly off because the new loan isn’t showing at exactly $100k, but for all these the final numbers will be slightly different. This decreases our monthly cash flow, on this property, by $84.87.

In these projections, we’ll receive $135,000 cash in hand. With that, we’ll pay off the higher loan in Kentucky, which has a balance of about $81k. That mortgage has a monthly payment of $615.34. These three loans have increased their monthly mortgage payments by $535.14 in total. Since we’ve eliminated a monthly mortgage with the cash from these new loans, our total monthly cash flow actually has a net increase of $80.20. In addition to this net positive cash flow, we also have over $53k in cash in our account.

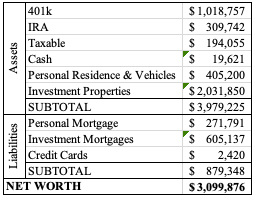

Now, if you know us, cash in our account isn’t a preference by any means. In my last monthly update, you can see that we have almost 20k in cash and that’s abnormal. Add $53 to that, and that’s just too much money sitting in a checking account. At this point, the goal is to buy another house. With the way the market is, we’re probably not going to hit the 1% Rule we strive for (the expected monthly rent will be at least 1% of the purchase price – $1000 rent for $100,000 purchase), and we’re not going to see the margins that we’re used to. It’s going to take a lot of effort to get our psychology right for this next purchase. We’ll have to hold strong in knowing that our other houses have great margins, and at least it won’t be negative cash flow.

At this point, we’ve started the refinance process by signing our initial disclosures and providing all the many, many documents needed to originate a loan.