Hopefully you read my previous post trying to dispel some incorrect understandings of how marginal tax brackets work. This will build off of that, including showing how the marginal tax brackets for annual income affect the “per paycheck” payroll withholdings your employer processes before paying you.

Let’s take another common misconception, the payroll tax withholding.

When you start a new job, your employer likely hands you a W-4 to fill out. This tells them how you want your federal taxes to be withheld from your paycheck. This depends on your filing status, the number of dependents you have, the way some of your personal activities throughout the year may affect any tax credits or deductions you’ll claim, etc. The W-4 is used to approximate your federal tax liability for the year, divided by the number of paychecks you’ll get in the year.

I’m going to look in my crystal ball and know that my federal tax liability for 2019 will be $13,000. I want to fill out my W-4 so that my employer knows to take out $500 of my paycheck every two weeks to pay the tax man on my behalf.

This is easier said than done, and most employers will allow an employee to adjust their withholdings throughout the year (I can do it for every paycheck if I needed or wanted to).

When you file your taxes in the winter/spring of the following year, this process analyzes your tax liability (what you owe based on deductions, credits, income, etc) and compares it to how much your employer paid on your behalf throughout the year. If your employer withheld too much, you get a refund. If your employer didn’t withhold enough, you have to pay. There are differing opinions on how to strategize this situation, but a general rule of thumb should be to match as well as possible your withholdings to your projected liability.

- If you get a refund, you’ve given Uncle Sam an interest free loan on your money for several months or the whole year. However, this can be a forced saving tool that people use who are scared they’d spend that money if they received it in their paycheck. Others see this as a cash windfall they receive in the spring and use it to splurge on a big purchase.

- If you owe money, sometimes there are fines for owing too much, and it can hurt to have to shell out a big sum of money at the beginning of every year, if you weren’t saving for it and didn’t expect it.

Where things get tricky, and people start to misunderstand, is if people get a bonus at work, or work some overtime, and get a higher paycheck than normal.

Payroll processors use a chart similar to the tax brackets, where they know your filing status and the number of exemptions you requested on your W-4, and use your income for that pay period to determine how much federal tax to withhold.

If every paycheck you get in the year is for working the same amount with the same salary, your withholding amount will not change and your taxes will be easy to follow and understand.

When it changes, payroll processors do not look at your yearly salary or previous pay periods. They only look at the dollar amount that you earned for that paycheck.

Let’s say you earn $2,000 per bi-weekly pay period in 2019. You file single with 1 exemption. Each exemption (withholding allowance) is worth a deduction of $161.50, so you can deduct $161.50 from your taxable wages for every paycheck for the purposes of reading the payroll withholding charts. (This dollar amount comes from the IRS, as part of their math for how withholdings are estimated to determine tax liability.) Now, you can say you “earned” $1,838.50.

More information on this can be found here, on pages 22 and 44 specifically.

From the chart, you owe (will have withheld) $174.70 plus 22% of the amount over $1,664, which is a balance of $174.50. Times this amount by 22% = $38 (rounded). This totals $213 deducted from your paycheck.

Let’s say that happens 24 out of the 26 paycheck you get this year, but in one, you get a $2,000 bonus, and in another you work $500 worth of overtime extra.

For the check with a bonus, your payroll processor knows you earned $4,000 that pay period, independent of what has happened the rest of the year. Using the same table, your tax withholding will be $553.32 plus 24% of what you earned above $3,385 (don’t forget to subtract your exemptions). That’s $109 more dollars. So you’ll have $662 deducted. That’s a big difference from your $178! Makes the bonus come with a tad bit of bad news, right?

The overtime paycheck works similarly, but because it’s only a little bit more money that paycheck relative to the norm, your tax withholding that check is $323.

Let’s add up your whole year.

24 paychecks of $2,000 income = $48,000 with ($213 times 24) $5,112 taxes withheld

One paycheck of $4,000 with $662 withheld.

One paycheck of $2,500 with $323 withheld.

$54,500 in earnings and $6,097 withheld.

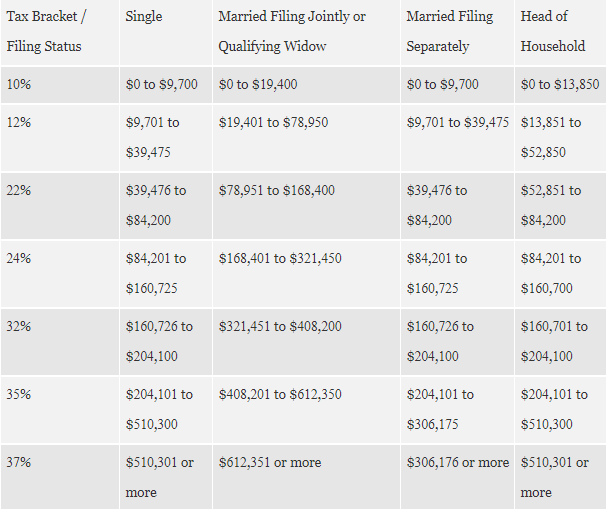

Federal Income tax liability is 10% of $9,700, then 12% from $9,701 to $39,475, then 22% for the rest; this comes to $7,848. However, our system includes a standard deduction of $12,000. This means that you can take $12,000 off the top of your earnings and it won’t be taxed. We’re going to calculate as if you earned $42,500 for the year.

Your tax liability for the year is $5,208. With $6,097 withheld by your employer, this means you should expect an $889 refund!

A couple things were in play here. You claimed one exemption. You could’ve easily claimed a second exemption for some or all of the year to have less deducted from each paycheck to more closely match your eventual full year liability.

Secondly, those two paychecks where the payroll processor charged you extra tax, your paycheck was proportionally smaller, which means your refund at the end of the year was higher. You weren’t ACTUALLY taxed more for that bonus check, you simply had more withheld, a majority of which you’ll get back when you file in the winter/spring of the following year. The bonus check had an even more profound difference because the marginal bracket it fell into that period was the 24% bracket!

If your employer allows as many withholding/exemptions adjustments as you want, you can track your tax withholdings and projected liability changes throughout the year to strategize and minimize your potential difference between the two numbers.

In summary, your total annual income is the only thing that affects the tax liability when you file income taxes at the beginning of the following year. It does not matter if your paychecks were consistent, all over the place, front loaded, back loaded, or any other weird scenario that might happen with bonuses, overtime, raises, job changes, etc. Those variables do affect a single particular paycheck and how much cash you bring home in net that week, but the effects of that can be mitigated by shifting withholding amounts with your payroll processor and planning ahead by tracking your numbers.

Reminder, do not confuse payroll tax withholdings from your tax liability. Withholdings are an estimate, meant to match your projected liability. Filing your income tax at the end of the year simply remediates the difference between the two total amounts. If you had too much withheld, you get a refund. If you didn’t have enough withheld, you’ll owe the tax man.

HAPPY TAX SEASON!