We turned over a rental in April, bought a new house that requires work in June, and turned over another rental in July. Those activities have a lot of expenses associated with it. While we could have strategically spent the money and paid off credit cards, it’s nice to have a cushion. When we’re faced with a lot of large expenses, Mr. ODA searches for a new credit card.

Why do we open a new credit card for big expenses? Because it’s a free short term loan for us. We’re looking for a card that provides an introductory 0% interest period, as well as some other bonus(es). Carrying a balance on a credit card and paying up to 25% interest is a non-starter in our financial portfolio.

Mr. ODA had searched for a new credit card back in the April timeframe, but we had multiple credit hits around that time, and I didn’t want to risk it. We paid off the expenses for the first rental turnover through our regular credit cards. Once we bought our new house and we knew that turning over another rental was looming (with big expenses like carpet replacement), Mr. ODA found a credit card he wanted.

At the last second, Mr. ODA switched which card he wanted. The card gave an introductory offer of $200 back after you spent $1000 within 120 days, up to 5% cash back on two categories you choose, 2% cash back on one everyday category, and 1% on all other purchases. It had 15 months of 0% APR and no annual fee. He received a credit limit of $500. Seriously. He called to get a credit increase and find out why it was so low, but they said they required another credit report pull to talk to him about anything. Nope. So we have this random $500 limit credit card in our portfolio. We’ve spent our $1000 and will get our $200 cash back (unless they find a loophole, which I would expect based on how this company’s relationship has been so far), and then this card will just sit unused until they close it years from now due to inactivity.

Since that was a bust, Mr. ODA opened a different credit card in my name (spread the wealth on credit inquiries). I was granted a $9,000 credit limit, and we got straight to work spending that. There’s no annual fee; it has a 15 month 0% introductory period; and earn 5% cash back on purchases in your top spending category (automatically, without choosing a category) up to the first $500 spent and 1% cash back after that. It gave us $200 cash back after we spent $750 in the first 3 months.

Two of our first few expenses were a vanity for our new master bathroom and 1,000 sf worth of vinyl plank flooring for a rental. Our balance within the first week was over $5,000. As much as I can’t stand to see that balance sitting there, it has helped us move money around. Usually we focus our spending in the categories that each credit card offers with higher rewards, but for these bigger expenses, we’re focused on being able to float them for several months.

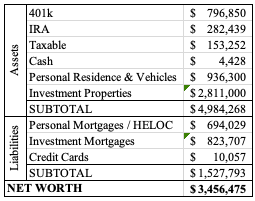

We used a Home Equity Line of Credit (HELOC) for the down payment on the new house. Originally, we had been paying down the principal on that, and put $14k towards that over the last month. We then decided we should focus more into buying the dip of the stock the market instead of paying down that account with 4% interest rate (although that’s variable). That’s what we’re currently focusing on, knowing that when we sell our current house, proceeds will pay off the HELOC in a short few months. We currently have about a $1500 cash cushion because we know that we have the HELOC to fall back on. For instance, we’re replacing the driveway and walkways at our new house, and we’ll pull cash out of the HELOC to pay for that (they don’t take credit).

If your credit is in favorable standing and you have large expenses looming (without a need for a new loan/mortgage in the near future), then look for a new credit card. Don’t open any random one. You’re looking for 0% interest for 12-15 months, no annual fee, and the possibility of a reward system (whether it’s an introductory offer related to spending, a cash back incentive for spending, or some form of both).