Whew, we’ve been busy. Son turned 4. Lots of traveling. Kids started school. Managing two houses. Managing the rentals. Being 7 months pregnant.

We’ve been working on our old house to get a lot of the things moved to the new house, while keeping enough there to live. A slow move sounded great in concept, but dragging this out for 3 months now, with another 6-8 weeks to go probably, has been rough. We unload the car, put it in the new house dining room, and then I need to unpack all that and find it a home. Then we come with another dump of things right after I clear that out. It’s been exhausting. Meanwhile, I’ve been painting almost all of the new house, changing out light fixtures, changing out some electrical switches/outlets that were dated, etc. Mr. ODA has started working on the rebuild part of the bathroom renovation, so we happily have gotten all the electrical work that we wanted to do done (we need to hire an electrician to run a line for the dryer), and then got the shower framed. He’s also been working on the yard and landscaping, which is a big project because the original owner of the house put in a lot of landscaping, and then the people who owned the house for about a year before us didn’t maintain any of it.

We’re listing the house this week, and we’re hoping for a reasonable offer ASAP and a closing at the beginning of November. That closing will pay off our mortgage (~$265k) and our HELOC (~$82k).

RENTAL PROPERTIES

October brings a lot of rental bills. KY’s property taxes are due in October and November, and none of the houses we have here are escrowed, so I need to plan on about $6,500 outlay. Right now, we have a HELOC on our last primary residence, so I have that to fall back on. Typically, I project out 2 months of expenses, and I know how much I have “left over.” The “left over” usually is paid towards a mortgage or, currently, our HELOC balance; in the Fall, I plan to have that “left over” go towards the taxes. Luckily, our houses in Virginia that aren’t escrowed have the tax payments due half in December and half in June.

While our credit card balances are high (we’re carrying a large balance on one that’s 0% interest), we didn’t have a lot of expenses this past month. Mr. ODA’s work trip hotels and restaurants are on the credit cards that will get paid this week, and we’ve had higher gas expenses because of my driving to/from NY and then capitalizing on Kroger incentives so filled up one car. Other than that, we’ve only eaten at restaurants sporadically and have been focused on getting projects done, so haven’t gone out much.

This is the first month of the newly executed lease with a tenant who paid late every month. Their rent total increased for the convenience of paying twice a month (although the total owed now is still less than their rent and late fee they had been paying). They paid the first half on time, and they haven’t paid the second half, which if it’s not paid by the end of today will incur a late fee. Rent was $1450, so they were paying $1595 every month. Rent is now $750 twice a month. If they pay on time, it’s $1500 per month. If they pay half late, then it’s now $1575 per month.

I submitted the security deposit charges to the tenant that moved out. She asked a question about the charges on the list, but then didn’t acknowledge by the deadline. We need to have our property manager file the charges in court. Somehow it’s the 19th of the month, and we haven’t pursued that yet because we’ve been so busy.

Other than that, we didn’t have any service calls on any of the houses, and everyone else has paid their rent.

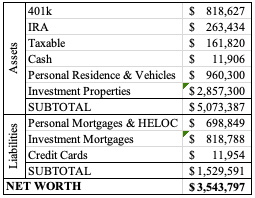

NET WORTH

We have a busy October planned. I hope we’ll finish the projects at the new house and be close to closing the chapter of our last house. Our investments have declined significantly (almost $91k!) from last month. Our cash is higher than usual because of the cycle timing for this update compared to the bill due dates. And finally, the credit cards are higher than usual, and they’re higher than last month, but that’s because we’re purposely carrying a balance on a 0% interest card. So while our overall net worth has decreased over $33k since last month, the stock market issues have been offset by paying down mortgages and increased property values.

Welp, I haven’t posted in a month. We have been so busy and exhausted.

We bought a house on June 15. That process was not smooth in the week before closing, even through the day of. Our attorney had to come to our house the next day to have us sign other papers. Our lender was great, great, great, until they weren’t at the 11th hour. As always, everything went through, and we have ownership of the house. And that week will be a distant memory soon. But why does the mortgage industry get away with operating this way? I feel like there hasn’t been a single transaction we’ve done where there wasn’t a “where’s my paperwork????” or “why’s this wrong the day before closing???” moment (or my favorite, when we begged for the HUD-1 to review it before closing, and a traveling notary showed up at our house, only for the HUD-1 to be different than the closing disclosure and the numbers to be wrong on both documents).

We used our HELOC on our current house to pay the downpayment and closing costs on the new house, so that was a quick debt addition. We started with a balance of about 86k and have paid it down to 75k. We didn’t necessarily need to take the whole amount from the HELOC, but it was easier to get one cashiers check from the HELOC and immediately pay towards it than to transfer some from the HELOC and do a wire from our checking account.

This new house will be our personal residence, but it requires work. We’ve gutted the master bathroom, and I’ve been painting nearly all my free waking moments. I have the first floor mostly done (including making a ceiling go from navy to white.. ugh) and the kids’ bathroom done.

We opened two new credit cards in the last month, but I’ll get into that in the next post. Just note that our credit card balances are higher than our usual, and will remain that way.

We had opened a checking account for rewards a while back, and the account required $500 of direct deposits each month. It was one more account to manage, and it was no longer serving a purpose, so we finally closed that. Now we just manage two checking accounts.

RENTAL HOUSES

We have a vacant rental house as of June 30th, which I’ll also get into in a future post. The good news is that one of our houses that’s a repeat offender of not paying rent is now out of the picture. We still have one house that never pays on time, but I’ve at least got them paying half the rent by the 5th so that we aren’t constantly floating their mortgage and bills until the last Friday of every month.

We had two rental increases go into effect this month. One was for $20 (good tenants, long term, told us in advance they wanted to renew, but we also needed to cover our cost increases) and another was for $50.

Our property manager in KY hasn’t been easy. We’ve had to do a lot of managing the manager. All of our paperwork says not to charge the 10% fee on contractors. The document that they put in our file says it, and that’s the same document they put the charge on. I keep having to ask for all the documentation. Once I ask, they note the 10%, but it’s not until I ask.

We paid a plumber to fix a shower handle in one of our houses. On June 1st, she texted that it was loose. She didn’t really explain the situation, and I asked her to tighten the screw and let me know. She texted me on July 8th that it didn’t work. Where have you been for a month?! Then she said “let me know when the plumber is coming so I can wake my husband.” Um, you waited 5 weeks to tell me that it’s still broken, I’m not rushing a plumber out there today.

One of our insurance companies dropped us once they found out we don’t live within a certain radius of the houses. We have a property manager, so this rule doesn’t make sense to me. They let us finish out our policies, but they wouldn’t renew. Our agent quoted one company that doubled the cost we had been paying because the roof “may have been last replaced in 2000” (and we couldn’t prove otherwise). I said nope, and I asked another agent to give a quote. Their increased our cost by about $100, but it was better than $300. I executed that at the beginning of this month.

We had an HVAC go out, but luckily it was able to be fixed (for 225) than replaced.

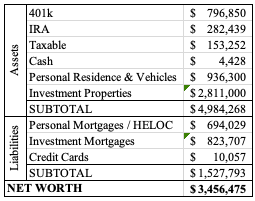

NET WORTH

Well, even though our investments are declining and we took on a lot more debt, our net worth increased by 75k from last month. Truly, I’ve focused on the work we’ve had to do over the last month, and not necessarily on the spending or the market. At some point I’ll need to get through all our expenses and identify how our spending has changed, but perhaps that’s a job for another season while we continue to work on a new house and work towards moving our family in the coming months.

Every once in a while, I like to share what I’ve been doing to manage the properties. There was a lot of activity needed over the last two months.

RENT INCOME

One of our usual suspects for late rent payments was late again. We seem to only have a one-month streak for on-time payments with them. She at least communicates with us that they’ll be late and gives a projection on when we’ll see it. She ended up paying rent on the 14th, and said she needed to pay the late fee on the 21st.

Two other houses haven’t paid rent, but they’ve applied for rental assistance.

RENT RELIEF PROGRAM

House2 applied for rent assistance in September, and we still haven’t received that from the State. I did finally get a tracking number on the 19th that it’s on its way. She paid $400 worth of January’s rent on a Friday and said she’d have the rest on Monday. Well, as she has a history of not communicating and not upholding her word, I wasn’t taking a chance with her. I served her the default notice on Saturday to indicate that she didn’t pay rent in full and had 14 days to remedy that. She remedied that by applying for rental assistance again. She said that she only applied for January assistance, so hopefully we’ll have February rent on time. I wish I could dig into her finances and find out how she didn’t have to pay any rent for September, October, or November, only had to pay $600 towards December because she had a credit from a payment plan previously in place, and then can’t pay January rent in full.

House3 had to apply for rent assistance. They’re great tenants and have been with us since we purchased the house. In November, she applied for December, January, and February assistance. The application expires 45 days after it’s sent, as a means to protect the landlord from floating the expenses on the property indefinitely. This tenant ended up paying December’s rent, but hasn’t paid anything towards January. Luckily, we did receive approval for their application on January 11. Hopefully we’ll receive that money in less than 3 months time like the last time this program was involved. What she paid in December will be counted as March’s rent (2021 income for tax purposes, but she won’t pay March rent because she has that credit now).

REFINANCES & MORTGAGES

We had to provide several post-closing documents on the refinances. It was horrendous. They asked for new types of documentation. Clearly, whoever is purchasing our loans didn’t like the lack of due diligence done pre-closing. Except for the new request, everything else they requested could have been ascertained by looking at the documentation already on hand, so we didn’t appreciate that. Then the new request was to explain how we paid off a mortgage, which was paid off 4 months prior to us establishing a relationship with this company to refinance the other loans. I had to provide proof that it was paid off, and then I had to provide the funds used to pay it off. The balance was $3,100. Paying a $3k bill hardly touches our finances. I want to become an underwriter so I can understand how they need so much detail and are sticklers for the type of detail, but they don’t need to know how to read the details they request.

We had an escrow analysis done on House7. It said that our mortgage was going to increase by $183 each month, but the increase should have been just about $60. I’ll explain details in another post, but that took some time. Mr. ODA called and walked the representative through the error. He said it took a while for her to get there, and we’re awaiting an update.

Since our refinances occurred at the end of the year, and all our city tax payments are due in January, I was nervous about the right amounts getting paid. The initial closing disclosures had the old tax payment amounts on it, but every one had increased. I was able to catch it and request that they be updated before our closing, but it was a day or two before closing. I was afraid it wouldn’t catch correctly. I had to stay on top of the payments and make sure they were all paid in full, and I had to pay the property taxes for those that aren’t escrowed. I was most worried about the three properties that were being refinanced, but then the issue ended up being one of our other houses. The escrow check was sent on 12/21, and it still hadn’t processed as of the tax due date of 1/14. I sent an email to the finance office hopefully showing that I had done my due diligence timely. Luckily, when I checked on 1/20, the taxes were processed by then.

LEASE MANAGEMENT

We require action from the tenant no later than 60 days from the end of their lease. There are 3 properties that have an April 30 lease term expiration. One tenant already reached out and asked to renew their lease. They’ve already been there for two years, and their rent has remained steady at $1300. We have precedent of increasing long-term tenant rent every 2 years by $50 (but we also have precedent of not actively managing houses and not increasing the rent at all.. oops). I explained to this tenant how there have been several increases in our expenses over the last two years. They’re really great tenants, and they hardly ever ask for anything from us. I felt guilty, but we’re trying to run a business, so we need to take care of that side too. Plus, if we didn’t increase slightly this coming year, it’ll be hard to manage future increases. It’s a lot harder to keep a good tenant if you don’t raise their rent and then hit them with $100-$200 increase down the road, so it’s best to keep with inflation. I did the cash-on-cash analysis for this property and discovered that the $50 increase falls slightly short of our expenses and keeping our rate of return the same.

I have to work with two other houses (via a property manager on those) to determine their new rent amount. One house negotiated a lower rent for a longer lease term at their lease initiation, which was October 1, 2019. This property in particular has had the highest jump in taxes. We grieved them to no avail. They’re claiming our neighborhood is part of a more affluent neighborhood and refuse to see how their district lines aren’t accurate for the type of house and street it’s on. I plan to push for an increase of $75 on that one, since their original lease amount is based on a discounted rate. One the other house, the tenants wield a lot of power to our property manager. We tried to increase rent last year, and the tenant flipped out on us about it. We’re already below what we thought market value was on the house, so 2.5 years without an increase is insult to injury. I’m going to request an increase from $875 to $950 on the house and see what the property manager says. If she agrees to a $50 increase, that’d be acceptable, but it’d be nice to recoup some of the other expenses too.

EXPENSES

We have a tenant in one of our houses that is amazing. He treats the house as if he’s the owner. He’s quick to take care of problems, and only seems to let us know when it gets to be a certain level of problem. This house has always had a mice problem. One tenant, who we evicted, created a really big problem that involved several mice making this house their home. She refused to do her part in cleaning up food messes, be it old food sitting on the counter or in the sink, grease splattered all over, or just general mess left behind. We got it under control, but the occasional mouse still rears its head. He sent us an email saying he’s been having an issue, and he’s tried really hard to address each individual mouse appearance. He said it has gotten to the point where he wants to do something more drastic, but wanted our permission. I said that it was absolutely at the point where it’s our issue to deal with, not his, but we thank him for his efforts. I called our pest control company, and we’ll see if that helps. One or two mice is one thing, but for him to say he’s caught 9 in a year, that’s a bit much. The pest control was $165.

One of our KY houses has a bunch of little and weird expenses pop up. This month’s explanation on my report from the property manager simply said “Repaired door by adjusting door to fit opening and resetting stuck plates.” I don’t know what door or how the plates got stuck, but I threw in the towel on that $60.

We were also informed that a toilet at another property stopped flushing. When asked for more detail, we were told that she presses the handle and nothing happens. My response? “Please don’t tell me I’m going to have to spend $125 for someone to reconnect a chain.” Our property manager’s husband said he’ll go look at it, for $80. That’s a downside to not living near the property and being able to check on the issue yourself. We got a text later saying that he talked the tenant through the issue, and it turned out that the flapper was just stuck. So luckily it’s nothing at the moment, but it could be an expense down the road.

SUMMARY

So that was a lot for one month. Luckily, our expenses themselves were low (225), even though we’re missing some rental income ($1,900 and $145 worth of a late fee) and we had to do more management than usual. By having 12 properties, late rent payments or non-existent payments don’t create a strain on our finances. For example, if we only had House2, who paid $1550 worth of 5 months of rent because of the rent relief assistance program, then we’d be floating those mortgages each month. By having more houses, those other rents are covering the expenses on the one house.

In 4 weeks time, a ‘full time job’ would be 160 hours of work. I estimate that all the action that I took this month (and the phone call Mr. ODA had to make to our bank on the escrow issue) comes out to about 6 hours. There’s the perspective. Even when it seems like a lot, because it’s more than nothing, it’s still hardly anything.

Spring is a time for lease renewals or preparing to re-rent a house.

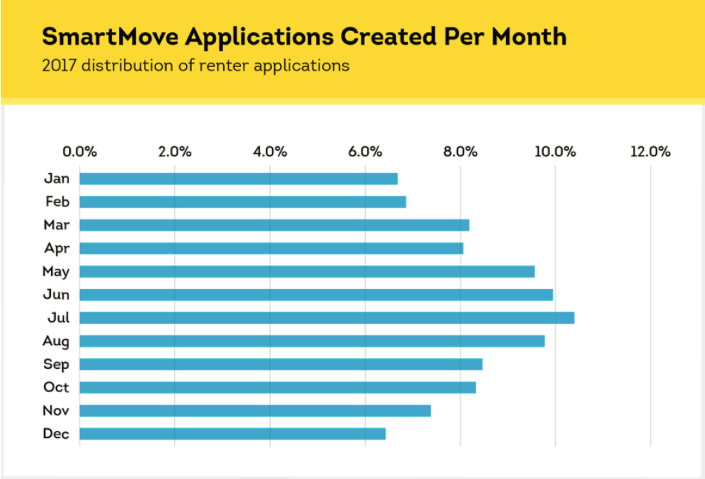

Spring and Summer are times when people are most active in the real estate market. It’s the best time to be listing your house for sale and for rent, which may yield you a better sale/rent amount because of greater competition. This timeframe is likely most active because of the better weather for moving and the school year – if a family is looking to move, they’re more likely to do it when they don’t have to transfer their kids to a different school district mid-school-year. Personally, when I was in college, nearly all the rentals were available in May or June. I remember being frustrated that I couldn’t get an August lease and had to pay for the summer months even though I’d be back living at my parents’ house. Now that I’m older and have more experience, it all makes sense. Below, you can see the increase in applications processed by SmartMove (the way we process tenant applications) that occur during the summer months, which indicates the most active time in the market.

We have seen this reflected in our days-on-the-market and rent prices. When we can list a house in the Spring months, we’re able to get it rented with very few days vacant. Houses that we’ve closed on at the end of the Summer (when school starts) and in the Fall have taken us more time to find a tenant, and we’ve had to reduce our asking monthly rent amount.

For those houses that we had purchased in a less-opportune time of year, we’ve worked to get them back to a Spring-time market for renewal.

We purchased two in September 2019 that we weren’t able to get rented until November 1st that year; we offered those tenants an 18 month lease so that their lease expiration would become May 31st.

We did similar with a house that we purchased in August. After that first year, a prospective tenant tried negotiating the list price for rent, and we said we were willing to reduce the rent a bit for an 18 month lease; they agreed, and we got our rental on a Spring renewal.

We recently had a tenant break their lease (with our concurrence), so that house has a lease expiration of October 31st now. We intend to offer a 6 month lease term to that tenant when the time comes.

With that said, we have lots of activity at this time of year.

We have 9 houses in Virginia and 3 in Kentucky. These markets are so different for us. We do our best to work with our tenants to encourage them to continue renting with us. I wrote about this in detail in my Tenant Satisfaction post.

Here’s a break down of how we handled all the leases that are expiring at this time of year.

In Kentucky, one lease was set to expire at the end of April and another at the end of May. These two properties are under a property manager. She attempted to increase the rent for a new lease term, but the tenants pushed back. Landlords don’t have a lot of leverage in a pandemic. Since the property manager is the one who handled the communication, I don’ t know what the details were. We believe both these houses are rented for less than market value, so that’s unfortunate. But, we’re grateful that both tenants renewed their lease for a year, so we don’t have to work to turnover the houses. Within reason, we’d always rather rent for a few bucks under market value than to handle turnover and lost rent (vacancy) by trying to maximize monthly cash flow.

In Virginia, we have an array of situations. Richmond was quick to acknowledge the property value increases that have occurred over the last year or so. This means that they increased our assessments, which effectively increases our property taxes.

We have the first two properties that we bought in that market, which are next door to each other and both have long term tenants (one since we before we purchased it, and the other is the second tenant who moved in a year after we purchased). We inherited their rent at $1,050, and then we increased it to $1,100 two years ago. With the property assessment increases, it was time to raise their rent again for this July. I initiated a letter to each of them stating the rent will increase as of July 1, which gave two options: they could leave the property by June 30th in accordance with their lease, or they could sign on for another year at the increased rent rate. Both chose to stay in the property, and they signed another year at $1,150. This is still below market value for the houses, but we’re happy with the lack of maintenance needs in these houses over the last 5 years. We’re in the middle of replacing the flooring in one of the houses. That house has a family of 5 and a dog living in it, so it’s not surprising that it’s worn out faster than the identical one next door with one person in it.

We have a 2 bed, 1 bath house that rents at $795. She’s been in the house since July 2018, which means that her lease ends June 30th of this year. Based on the 1% Rule (i.e., we’re looking for the monthly rent to be 1% of the original purchase price) for this house, our rent goal is $635. Since we’ve exceeded that goal for the life of our ownership, and the house hasn’t cost us much in maintenance, we chose to not increase her rent if she wanted to renew for another year, which she did. She has also spent some of her own money to spruce up the house and make it her home, and we recognize the value to us that her efforts also bring.

Another house reached out to us and asked if we were willing to renew her lease for another year. She’s been there since we purchased the house in 2017, and we’ve never increased her rent. She usually pays rent early and doesn’t ask for anything. The 1% Rule puts us at $660, and we’ve been collecting $850. Since we’ve been lenient on rent increases, I thought it a good idea to re-evaluate her terms. I plugged all the numbers into Mr. ODA’s calculation sheet to see how we were doing since the taxes increased so much on this house. Our cash-on-cash return (which we aim to be at 8-10%) came back at 19.8%. A rent increase for the sake of increasing rent isn’t worth it for such a good tenant, so we agreed to renew her lease for another year at the same rent. She wrote back: “omg thanks so much for the good news!” Happy tenants = good tenants, remember?

As for the others that I haven’t mentioned:

Two of our houses were put under a two year lease last year, so they didn’t require any action from us this year.

We have another house in KY that has a lease ending 7/31 and is under a property manager. We’ll offer a renewal option for them (i.e., we’re not interested in asking them to leave), but we haven’t worked out those details yet. Since we’re very hands off for our KY houses, we don’t know the satisfaction level of those tenants to gauge. Historically, we’ve had trouble renting this unit, costing us long vacancy times, so if we can renew their lease for even the same rent, we’re happy. Plus, having a 7/31 end date starts pushing us closer to the Fall for any future year-long rental agreements.

One of the houses that we have with a partner has a difficult tenant. I mention the tenants almost every month in the financial updates because they don’t pay their rent on time, and getting information out of them is like pulling teeth. They’ve rented there long before we owned the property, and their rent has always been $1,300, which is well below market value. We plan on offering them a drastic rent increase and a new lease term (we’re still managing under the previous owner’s lease agreement) in July for their September 30th expiration term.

While we don’t have any houses to turn over, we’re going to get into each house this summer. Since so many of our houses don’t typically have turnover, we don’t get into them as often as we should to make sure things are running correctly (i.e., don’t want small issues to go unnoticed and cost us in the long run). Specifically, we need to make sure that the HVAC filters have all been changed and verify there aren’t any red flags. I plan to give the tenants at least a month’s notice before we enter, so that if there are any maintenance activities they should have been performing, they have time to get it situated. I’ll walk through with our typical move in/out inspection form and note any concerns or areas of interest. I also understand that by being visible, I’m opening myself up to being asked for things that a tenant may not necessarily ask for via email or text, but I’ll cross that bridge when I come to it. For now, we’re just grateful that we have no houses to turn over and no expected loss of rental income for the year thus far!

House 1 was purchased from a family member because we saw an opportunity when they were getting ready to sell their townhome. House 2 was purchased because we were looking for a way to make our profit from the sale of our first home to get to work for us. While in the process of purchasing House 2, the seller said he was interested in liquidating the house next door, which was a mirror image of House 2, and so that became House 3. Both House 2 and House 3 came with tenants, which was a big advantage, but delayed a few lessons in rentals for us.

After we sold our house outside of DC, we moved just outside of Richmond, VA. We spent a few months looking at the neighborhoods and analyzed the markets available in Richmond. I was more interested in the college area, where it’s a market I knew well, having been a college kid who rented in an old house that was sectioned into apartments. Mr. ODA was more ambitious (in my opinion), looking into neighborhoods that families would rent in. Many investors are looking to rent in areas of Richmond that fit the quintessential Richmond mold (e.g., walkability to restaurants and shops, bike routes). However, these houses don’t come close to hitting the 1% Rule.

We’ve purchased several houses on the east side of town, and they’ve worked out very well and most don’t have turnover. The value of House 2 since we purchased it has increased by about $70k as the neighborhoods in the area continue to decrease crime and increase value. Both houses are about 13 years old, 1200 square feet, and have 3 bedrooms and 2 baths. All of the rooms except bathrooms and kitchen are carpeted, which is something we’ve since tried to stay away from.

THE EXCLUSIVITY AGREEMENT

After we saw House 2 and wanted to make an offer, our Realtor relationship went downhill. We had a Realtor for our home purchase when we moved to the area, and we continued the relationship to have access to the MLS. After we purchased our home and started looking for rentals, we soon learned that our Realtor 1) had an agenda to get the most commission, regardless of the best deal or our interests, and 2) kept pushing areas she knew versus areas we were interested in. We had made it known that we wanted to buy several properties, and I believe by the time we wanted to make an offer on a house, she realized we weren’t looking to further this relationship after this deal. Since she had shown us a few houses, we expected to see this deal through with her. That’s when the straw broke the camel’s back. We received the offer to review, and it came with an exclusivity agreement.

An exclusivity agreement is a contract established by the Realtor to protect their interests. If the client signs it, then it means that the client is committed to that agent for the terms in the agreement (e.g., a single purchase, a period of time). We hadn’t needed one in Fairfax, and the one we had for our personal home contract covered a month’s time. When we received the contract for House 2, the exclusivity terms were until October 4, 2016, from the date of the contract, which was May 4, 2016. We requested the date be changed to match the “close no later than” terms in the contract, which was June 17. That’s when the bs-ing commenced. I’m sure the average buyer wouldn’t have noticed nor cared. We saw right through it, and she kept digging in deeper with holes in her story and guilt.

First, she claimed that she made it 6 months (although it was 5 months) so that it gets through closing and we didn’t have to sign again. We countered with three pieces of logic: 1) the field can accept an address, so change it to the house’s address to cover us for the entire time it took us to get to closing, whenever that may be; 2) the exclusivity period on our personal residence’s contract expired long before we actually closed (because it was a new build, and the contract was signed before construction began), but we never had to re-sign an agreement; and 3) we never experienced a 6-month closing on a routine purchase.

Instead of addressing that the field could accept the house’s details rather than a period of time, she said: I’m committed to helping you guys look for houses and make offers, are you committed to working with me? Red flag. When we said we wanted it changed to the house address, and that we didn’t mind signing on for each property we made an offer on, she furthered the guilt with: We have know each other for almost a year and I honestly didn’t think it would be such an issue. If you are not willing to sign it I am not going to be able to work with you. If it’s not supposed to be a big deal for us, why is it a big deal for you/your broker?

One of the first things we learned in the real estate market was to not sign an exclusivity agreement. It eliminates your rights as a buyer and ties you unnecessarily to an agent. On the Realtor’s side, I understand that a lot of time and effort goes into working with clients, and there is a possibility that one Realtor shows a client a house, but that client uses a different Realtor to sign the contract, which causes the agent who showed the property to lose the commission. However, I believe that if there’s a good relationship with the Realtor and client, it shouldn’t need to be in writing that they’re committed to each other. I also don’t believe that it’s routine that a Realtor shows several houses to a client, and then that client finds someone else to make an offer. I was also surprised that it’s at the contract stage in the process, and not at the showings stage.

When she wouldn’t write the offer without us signing an unnecessarily long exclusivity agreement (again, we were willing to sign it as associated with this offer/property), we called our old Realtor and asked if she could write the offer for us even though she didn’t cover that area. (An Agent’s license covers the whole state, but typically their access to the MLS is confined to local metro areas unless they want to pay for other regions.) She wrote the offer for us. She also introduced us to a loan officer who we have used for every property purchase since then, and recommended to others.

EXPENSES

This house is relatively new, so we haven’t had any major expenses. We had a couple of HVAC service calls, one was a legitimate concern and one was a misunderstanding by the tenant on how it works in extreme temperatures. What we haven’t paid for in physical house repairs, we’ve made up with in learning new things about tenants.

TENANTS

We had a tenant move in right before we closed on the house. She had gone through a divorce and was living on her own. At the end of the year, she got back together with her ex-husband and moved out. We touched up the paint, cleaned the carpet, cleaned the kitchen and bathrooms, and then listed the house for rent. We chose two ladies, one of which had a criminal record for forgery a few years prior. Other than that, they were the best qualified financially.

Our only issue in the first year was that they had a ‘friend’ look at our HVAC unit. We told them that it’s not their property, and had anything been wrong, it would have been on them to fix because we didn’t authorize tinkering with our very-expensive property. The issue was that it was 100 degrees outside, they had the thermostat set at 60, and it wasn’t getting to that temperature. That’s not surprising. Our technician went out, checked the unit, and explained to them that when it’s that hot, you can’t expect it to get to such a different temperature in the house. He suggested using fans.

They moved in June 1, 2017 and one of the ladies is still there.

At the end of their second year, we increased their rent by $50/month to $1100. This is still under market value for the house, but not having to turnover the unit was more important than a drastic increase in rental income.

In February 2020, we learned a new aspect of the law – domestic disputes. One of the ladies reached out to us and requested to be released from the lease because she had a restraining order filed on her roommate. We researched the requirements associated with restraining orders (because the two she gave us were expired) and then her rights as it related to being a tenant. She had paid her portion of the rent each month, so we weren’t aware of issues. We released her from any responsibility immediately and notified the roommate. Per Virginia Code, the remaining tenant is responsible for the entirety of the lease from then-on. We gave her the opportunity to vacate the property within 30 days if she could not pay the full lease amount going forward, but she chose to stay on the property.

The world shut down a month later. Other than an issue here and there with our other properties, this one has been the most affected. She doesn’t communicate up front anymore when she won’t be able to have rent on time. We received a letter from her stating that she had been furloughed, but things in the letter didn’t look professional and piqued my interest (recall the forgery charge). I called her employer who informed me that her hours were cut, but she was not furloughed; the woman who answered the phone sounded exasperated and indicated she had explained this to our tenant several times. I informed the tenant that I had done an employment verification and that we could be flexible, but rent was still expected. Then a few months later, after she didn’t pay rent or tell us what was happening, she claimed she couldn’t pay rent because of an issue with a check showing up. We requested her employment information again, and I verified she was fully employed. When I asked her what was going on, she stated that she wasn’t required to tell me where her rent was coming from and whether she was employed didn’t mean she could pay rent. Fun.

Then, a few months later again, I received an email from the Commonwealth of Virginia asking me for my tax identification number and other information because our tenant had applied for rent assistance. I was confused because the rent assistance program was for unpaid rent balances, and she was fully paid. I watched the rent assistance program training and attempted an application myself so that I could see how the process works before I questioned anything more. I verified that the program was indeed for past due rents and couldn’t be requested for future rent. I contacted the State office to gather more information, and the tenant had submitted that she didn’t pay January 2021’s rent, which she had. The State made a note in her file. I informed the tenant that the program was for past due rents, which she had none, and that she was not qualified for such a program, but we were willing to work with her if she had any problems paying rent timely in the future.

Each time she’s not paid full rent by the 5th of the month, she has paid rent in full before the end of the month. After she took full responsibility of the property’s rent and lease, we had her sign a new lease with just her name. That lease ends on June 30 this year, and we’re currently decided whether we’ll offer her another year at an increased rate (last increase was 2 years ago) or we’ll request her to vacate the property.