We ramped up our travel this month, which has actually led to us canceling a few trips that were planned for this next month. I went to visit my family for my sister’s baby shower, we went on a family trip for a long weekend, and then Mr. ODA was gone all week for work. We’ve done a few local activities, but several of our plans have been cancelled or postponed due to the current gas prices, which are about $4.75. Even Sam’s Club and Costco, which were holding strong in the low 4s, are both at $4.69 right now.

We’re working towards closing on a new house next Wednesday, so that’s been the stressor right now. We had a month and a half for closing, which is literally the longest we’ve ever had, and then yesterday I got asked for tax information. Seriously, what have you been doing for the last month since I signed off on the initial disclosures? We went with an online bank, so that’s been an extra factor in uncertainty through this process.

RENTALS

I served a notice of non-renewal to one of my tenants. Her lease ends on 6/30, and we want her out. It’s the first time in 6 years that we’re so fed up with a tenant that we actually said it’s time to leave. We’ve had issues with tenants in the past, but we’ve just increased their rent as a means of giving them the option to leave, or compensating us for our frustrations associated with them living there. She, of course, didn’t pay rent by the 5th. When I asked her where rent was, along with the balance of outstanding late fees and the current late fee, she said she was trying to secure a place to live, so she wouldn’t be able to “pay towards that” until the 17th. Pay your rent timely OR communicate a need for more time without the landlord having to hunt you down. That will keep a roof over your head so you don’t have to move when you don’t want to, and it’ll also put you in a position where your current landlord can actually provide a referral at a new place.

My other usual suspect, who I told needed to start getting their act together and pay rent before the last Friday of every month, paid half of rent on the 3rd and sent an email saying we won’t get the rest until the last Friday of the month. Progress, I guess.

We had a massive issue with our property manager in Kentucky. The accountant felt he had a little too much power and ran with it. Mr. ODA went to meet with them, where the accountant had to admit his mistake in charging us $900 in front of the owner. As a means of making amends, the owner credited us the management fee they took out of our security deposit. While I understand their thought process that our contract says “10% of income,” and a security deposit gets counted as income for tax purposes, I disagree with them taking a commission out of it. If that’s the case, our security deposits under them should be 10% higher than a month’s worth of rent. A security deposit’s purpose is to reimburse us for our costs to fix a unit that has been unreasonable mangled by a tenant before their departure. In this case, we have $4000 worth of costs. The security deposit was $895. Them taking $89.50 was insult to injury in this case, especially after they took 18 days before taking any action to confirm the place was abandoned. Moving on.

That house that was abandoned ended up getting rented for June 1st. We’re netting about $250 more per month with the higher rent there.

One of our mortgages was going to be paid off in May, which I mentioned last month. I scrambled to find out how to pay the taxes, which wasn’t easy (it’s a different jurisdiction than most of our houses… being in the county instead of the city). I finally got that figured out and paid the taxes at the beginning of the month.

PERSONAL FINANCES

This month we actually had a few “receivables” to expect. We learned that our lender wasn’t requiring an appraisal (we don’t get it), so they were going to refund us the appraisal fee of $525. We had a major issue with Home Depot and getting an appliance delivered, which ended with us going to the store, buying the appliance, putting it in our car, and driving it to the rental. We had to wait for the terrible delivery company to “scan” the not-delivered appliance back into their warehouse, and then we got $600 back. When I registered my kids for preschool, the system glitched and charged an extra $100, so we got that back. I had already registered my oldest at the same school as this year before we learned we’d be moving, and they were kind enough to return my registration fees, so that was $300.

All that to say, stay on top of your finances. Know what you owe so that you know when you’re overcharged. When someone says you’re owed a refund, pay attention that you receive it; we had to follow up on the refund, and it turned out she hadn’t processed it. Don’t be afraid to ask if there’s an option for a refund in some cases. Just those transactions are $1525 worth of money back in our pockets in a month’s time.

SUMMARY

We have work on a rental that’s still outstanding. I don’t expect her to actually be out on June 30th at 5 pm like she’s been instructed. I have our property manager handling the move out (even though she doesn’t manage that property). This way, if she’s not out on the 30th, I haven’t driven 8 hours to find out I can’t do any work on the property.

We plan on doing a lot of work on our new house after close next week. That’ll take up a lot of our free time over the next few months.

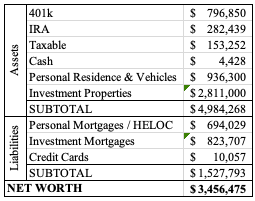

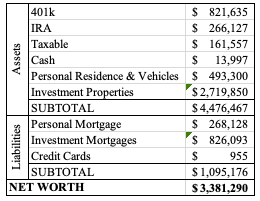

The stock market has somewhat rebounded. It’s not back to levels it was once at, but it’s nice to see balances go up instead of down. Our credit cards are down significantly because I am purposely keeping a low balance right before we close on a house (down by paying it off, not down by not spending…). Our funds for closing are coming from our HELOC, so it hasn’t been a stressor to keep a cash balance to go towards our cash-to-close.