This month was unbelievably painful financially. And yet, I appreciate that we’ve set ourselves up that we can handle these things without stress, even though the balances on credit cards made me feel like I was drowning. At one point, we had over $30k on credit cards. I’m still juggling life as a mom, financial consultant, part time worker, and volunteer on the HOA board. Oh, and managing two vacant rental turnovers, throw in 2 trips away from home, and school starting.

RENTALS

We had one house pay late, with little notice and communication (if you’ve been here, you know this is a pet peeve of mine). They paid the late fee at least. I had another house pay partial on the 3rd and then true up on the 6th. Again, no communication, and she beat me to asking what the deal is. I also had a tenant who already pays twice per month be late on both of this month’s payments, so that also brought in late fees.

In a story for another time, we have two vacant rentals. 11 of 13 houses renewed. Two houses each actually moved out of state, and unfortunately, my kind heart scheduled both of them to end their leases on July 31st. We’ve been spending all our time at these two houses. The one had smokers in it (against the lease) and we’re struggling with that. We’ve replaced the carpet and painted all the walls (except 2 closets and a powder bathroom) and it still smells funky when you walk in. Then there’s just the routine type turnover things like scrubbing and wiping dirty hand marks off the door frames. All of these things will be detailed in separate posts. The other vacant one was quite the story, so that’ll be multiple posts. Our attention isn’t as heavily on that one because we’re going to likely sell it instead of re-rent it.

We replaced a roof ($5500), replaced an HVAC ($8300, but split with a partner), evicted bats ($1480), and made decisions on flooring replacement in another house with extensive termite damage. Seriously. Financially painful. Coming this next month, we will also be paying for termite repairs at another house where we tore out carpet and laid LVP.

HEALTH COSTS

I tend to focus heavily on this topic in this blog. It’s surprising because it’s not really the niche of making money, but insurance and doctor bill processing seem to be wrong more than they’re right. Therefore, it falls more into “protect your money” than anything else.

This is a longer story for another post yet again, but the gist is that the insurance company took 6 months to process a claim. They sent me the bill in June. I called 3 weeks after the bill arrived to find out they had sent my balance to collections because their system flagged it as a January overdue balance…even though this was my first invoice on the matter. Love it.

The end result here is that we needed to add $1600 to the credit card.

PERSONAL

I don’t know that there’s much personal life happening with all those other things we’re managing. We took 2 trips. One didn’t cost us much because the grandparents take care of a lot of the cost, another one cost us more than usual because I put a lot of effort into food that we usually don’t do when we travel there. Overall, the trips were fairly inexpensive financially, but they took a toll on me due to the time commitment and what we had to give up by doing these trips.

Otherwise, we’ve just been wrapping up summer and starting school. We’re about to get back into baseball season with lots of practices.

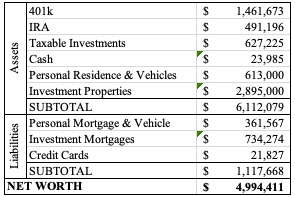

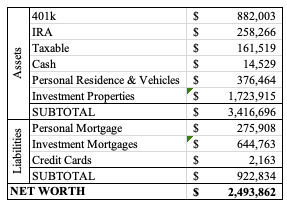

NET WORTH

The market had a big jump last week and my update of financials occurred Thursday morning. Unfortunately, life put a blog post on the back burner while we were turning over a rental, so I’m only getting around to posting this now. The market is in a fairly similar spot as of yesterday’s close, and I’m thinking we’d even be over $5 million if I were to fully update our financial status right now. We’ll just hope for the best for next month.

In October, we’ll pay off our $15k credit card that we’re carrying, so that will be a big swing in our credit card balance two months from now. We need new windows at our house (the seal keeping in the gas between the panes is going on quite a few windows (or went years ago), and it creates this streaky dirty look to them), but I think I’ll appreciate not carrying this large credit card balance month to month while we utilize the $0 interest for a while.

Every year, I like to look back at ways we earned income outside of a W-2 or our rental properties. These things include interest earned, dividends paid, and bonuses received on credit cards.

CREDIT CARDS

We opened a new credit card to give ourselves a 0% interest loan when we purchased the hot tub. I’m a broken record on this, but I’ll keep pointing out the availability of this option. Yes, we made this purchase because we could pay for the item outright, but it would be nice to pay for the hot tub over time while letting our money earn more money in other accounts. A sign-on bonus for that credit card and the immediate high purchase led us to $489 earned for doing nothing expect spending money and opening that new card.

Outside of that credit card reward, we deposited almost $1,200 worth of rewards from other cards into our checking accounts. Then we have some cards that earn points instead of cash. These are kept in that credit card’s “bank” of points because they can be worth more if they’re used within the rewards portal (e.g., booking a hotel). Essentially, 100 points equates to a dollar, but it’s not always that because of the bonuses available. With that said: we earned 18,683 points between 3 cards and $73 on another card.

INTEREST & INVESTMENTS

We have two accounts that pay out dividends in December of each year. This year that totaled over $4k. Between two savings accounts, we earned $2,500 of interest payments.

Mr. ODA invests in Treasury bonds. Instead of withdrawing the money after each 4-6 week period, he rolls it over and the interest earned gets deposited into our account. That’s paid us $2k this year.

ODD JOBS & RANDOM INCOME

On top of the things I can project like interest earned and rewards, I also do a few odd jobs throughout the year. Between a part time substitute teacher position, doing surveys, and selling kids clothing and toys to second hand shops, I brought in another $1600. I use this concept as an ‘offset’ in my mind to cover gift giving throughout the year. Mr. ODA brought in nearly $1,000 doing mystery shopper activities for restaurants. Betting on games and doing fantasy football brought in another $700.

SUMMARY

So with minimal effort, we brought in about an additional $14,000 in the past year! That more than pays for our hot tub purchase. It more than pays for our Christmas gifts, and even birthday gifts paid for through the year.

When I consign, it takes several hours to prepare. But I do those items that way because I can earn more money with less stress. For consignment, I’m preparing my items, logging them, printing labels, and then dropping off. Once I drop off, all I do is watch my sales. If I try to sell these items on mom-to-mom type forums, then I have to manage each individual item, follow up on people who need to pay/pick up, and then set out my items and wait for them to actually follow through. It’s just a lot more mental energy even if it may be less physical hours of work.

Outside of the consignment effort and my very part-time job, everything else was fairly passive. We earned a lot of money just by buying other things. We earned a lot of money by just having a savings account with a decent yield. We earned a lot by Mr. ODA investing in Treasury bonds, which takes a few clicks every few months.

The first step should be to ensure your money that’s not in use is in a saving account and earning interest. After that, a credit card with rewards earned should be used. Teach yourself discipline to count your credit card swipes the same as swiping that debit card in your checking account. You’d be amazed at how much those small bits add up.

A few years ago, I set out on this journey. I wanted to talk about money so that people would start talking about money. Talking about money is taboo. Someone will act funny talking about what they bought their house for, yet it’s public record that can be found in 2 seconds. People act like it’s “cool” to say they’re broke, as if it’s a badge of honor. I want people to talk about their spending and find ways to move forward so that money isn’t controlling their life.

In addition to that general goal, I’m also sharing lessons learned as we navigate owning rental properties. I hope that information helps both landlords (including potential ones) and tenants. I want tenants to understand the work that goes into owning the house and renting it to someone, and how the statement, “I can own a house for less than rent” doesn’t get you very far because you’re not the one maintaining the rental.

At the end of 2022, I was in the process of moving to a new home, renovating the new home, and was very pregnant with two toddlers nipping at my heels. My posts were just the monthly financial updates (and I didn’t even get to a December post because our baby was a sick little one). It was always in the back of my mind to make a post, but I didn’t have the bandwidth. It took until the last day of June for me to get my feet under me and start posting again. A few years ago, I tried to post twice per week. This year, my goal was once per week, with a schedule of Thursdays. I posted 31 times in 2023. I posted every week from June 30th until December 31st, except for Thanksgiving day.

MONEY

We used to make much bigger moves in our finances – buy a house, sell a house, pay off mortgages. This year, we did things differently. Mr. ODA discovered Treasury Direct. He invests in these short term savings bonds. They’re available from 4 weeks to 52 weeks, but we’ve only held them for 4 or 8 week periods. We had three different insurance claims over the last year or so, leaving high savings balances for a few months. Treasury Direct was a way to get our money to work for us, earning at a faster rate than a regular savings account.

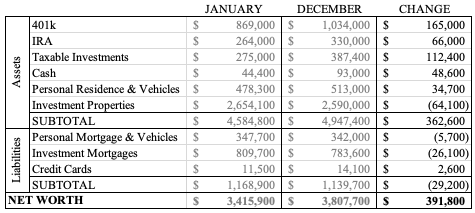

Our net worth increased by almost $400k, which is impressive since there wasn’t a large swing with a new house purchase. In January, home values were still high. However, the higher interest rates over this year cooled the market some, leaving our values $64k lower than January.

The goal all along has been for both of us to quit working. I quit in 2019, but have been doing odd jobs here and there. Mr. ODA’s quit date continues to be pushed back for a variety of reasons, but it’s something we’ve been planning towards. One step towards that goal was that we opened a new checking account. Nearly all of his pay check goes into that account, and we don’t touch it. While I could manually track our money as if we don’t have his income, it was a big step to helping us visualize him not working and how our finances would play out. I’m happy to report that I haven’t felt the strain of not having his paycheck coming into the account.

We opened one new credit card this year. We open new credit cards when we have a large purchase coming up. It started with our IVF journey, and we’ve continued that concept. It’s a “free loan” for us. We could either pay the total sum immediately (typically over $10k) from savings, or we could get an interest free credit card, allow our money to earn interest in savings, and then pay the balance by the end of the interest-free introductory period. That’s the path we choose. We replaced the carpet in our new home – the living room and entire second floor except bathrooms – for over $10,000. That’s sitting on an interest-free credit card right now, and I make $500 payments each month, until I need to pay the full balance at the end of the introductory period.

INCOME

Since I quit working my full-time-Federal-career in 2019, I’ve done several odd jobs. I’ve wanted the small break from being in the house, the small opportunity to have conversations with other adults, and a small feeling of contributing to the household’s finances. 2023 was the first year that I didn’t contribute more significantly. I worked 1 day as a substitute teacher in a preschool; $47 was deposited into our checking account. Comical. Even though in the literal “job” sense, I didn’t contribute much, I did work.

Besides the fact that I had to care for a newborn baby and keep three kids and a dog alive for the whole year….. 😉

I manage our rental properties. This year required a lot of management. I’m managing the work that needs to be done at each property. I’m recording expenses per property. I’m tracking income each month to ensure that we’ve been paid rent from everyone (and one property made this a very frustratingly daunting task).

On top of that, I also have worked to declutter and organize our house. As our last baby grows, we don’t need all the baby accessories that take up space. By selling these, it’s providing the ability to buy things that the kids need now. I brought in nearly $1,000 through that process.

Mr. ODA signed up to be a secret shopper. He goes into restaurants, follows the instructions he’s given, and is essentially reimbursed for the meal. He “made” about $750 doing that. It’s important to note that we’re spending money to get that money though. If he spends $15 on a meal at an assigned restaurant, he may be getting only $15 back from the company. Sometimes they offer a premium if they can’t get people to select the “shop,” but it’s just a few dollars.

CREDIT CARD REWARDS & INTEREST EARNED

Every year I love to tout this category. This year, the interest earned section far outperformed any recent years. I typically make a post where I go into the details of how our credit cards are earned, so this is just an overview. For the sake of this conversation, this is based on rewards redeemed as cash. Citi makes it easy to see how much has been earned/redeemed, but Chase has a portal where things are different. Chase allows for your points to go further if you redeem through their travel portal. That makes it hard to manage “earned” versus “redeemed” for a total each year, because the amount earned is inevitably less than it’ll be redeemed for.

Between all our credit card redemptions for cash and interest earned on checking and savings account, we brought in $4,000.

GOALS

I want to track our expenses more often throughout the year. I want to be able to get a handle on trends we’re making with our expenses and whether there’s an opportunity to cut costs. When I do this review once per year, it’s not giving me a lot to work with.

Mr. ODA is discussing leaving his job this year. It’s something that’s been on the table for several years now, but there’s never been a real reason to leave his flexible job where he has a bunch of leave and benefits.

Mr. ODA is working towards a financial advisor certification though. It’s a big deal, and I’m excited about it. He loves to talk about money and help other people with their finances, so I’m hoping this is a springboard for him to doing more of what he enjoys.

I’d like to work more. The few temporary jobs I’ve had have been more time consuming over a short period of time, whereas this substitute teacher position right now is so sporadic that I’m only working 1 day per pay period. While I appreciate the availability I have, I’m looking for something with a little more consistency (granted, for the Fall semester, I would basically be available everyday of the week, so maybe that will help).

We’d like our deck and patio to be replaced, which will then lead to more home improvement expenses. We plan to build a privacy feature wall under the deck, so that we can add a hot tub on the patio. There’s also an old hookup for a tv, which means some sort of tv set up is planned for out there, which may be further expenses. We have two more bathrooms in this house that haven’t been touched yet, and I plan to do a few upgrades.

A lofty goal will be that we keep our tenants in place and don’t have any insurance claims this year. The last year has definitely been more taxing on us than previous years.

I think the big goal is that Mr. ODA wants to hit $4 million in net worth. Mr. ODA was 30 when we hit $1 million, 34 at $3 million, and hopefully 37 for $4 million (I don’t know when $2 million occurred because we weren’t updating regularly). Being that we’re at $3.98 million now, and that we grew by nearly $400k this year without any drastic moves (buying/selling a house), I think it can happen!

NET WORTH

This “net worth” graph isn’t the best since I didn’t update our net worth from February through June, but I kept those months in there so you can see the trajectory. I’m sad that life got in the way of my updating those data points. If I just post the first and last month, you can see there’s an increase. But that doesn’t show you that there are dips along the way, and everything is based on a single snapshot in time, even though balances are changing daily. I hope that I’m able to track each data point this year and in future years so I can see these trends.

As an intro for newbies: I write a monthly finance post. These posts started out as a way to manage our dollars spent per category. It evolved to show insight into my monthly money management and thought process. It’s also meant as a way to remind people that they should be looking at their money regularly.

Every month, I’m looking back at my spending, looking at trends on the higher level (e.g., why is my credit card higher than I expected), and sharing the rental property expenses and activities that I’ve accomplished.

I typically post on Thursdays. Unfortunately, life got in the way. I had 98% of this written, but I hadn’t updated our accounts until 10 pm, so this is now posting off-schedule, on Friday morning. Sorry about that!

RENTALS

I suppose with 13 houses, it’s inevitable that I’ll have to keep track of one.. or a few.. to collect their rent. One tenant is set up to pay twice per month (they pay a premium for this). They paid both parts of December late, and the first part of January late. They pay a late fee with that. I had two other tenants pay late by a few days, but they communicated this up front, and I didn’t collect late fees.

I’ve been sharing that I have a tenant who has been behind on rent since October 1 and has communicated very poorly. By the end of December, she was caught up with rent due, but no late fees. We’re now 11 days into January without any payment. My frustration with her was that she didn’t communicate at all for the first two months, and didn’t keep her word on anything that she said she was going to do, but didn’t tell us that something would change. I always say that I’m willing to help and work with you, but you have to talk to me. If I have to beg you to tell me what the plan is, I can’t help.

I paid a carpet cleaner $250 and paid a painter $2000 for a house that we’re turning over. The carpet was new before the last tenant, but they were there for over 3 years, so it had to be done. They didn’t damage the walls, but my property manager said that all the walls looked like different colors, and I didn’t trust “touching up” 4 year old paint. The paint looks amazing, so I’m happy I went for the whole house.

I paid just over $1000 as a deposit on 3 new windows for a house, which are scheduled to be replaced on Monday (a couple of weeks for new windows far exceeded my expectations!). We had replaced the majority of windows when we bought the house. However, at the time, the kitchen and bathroom windows were considered an irregular size, and we were told they were going to be $2000 just themselves, when we were paying $2000 for all the other windows. I don’t know what pricing scheme changed in 5 years, but now all sizes are the same price, and the 3 of them are $2000 now.

We had a tenant ask to be released from his lease, which we concurred to. We had terms associated with that, which I’ll share in a separate post. We were able to get a couple into that house with no loss of rent, which has been appreciated.

We’re under contract with our handyman to do work on a house, so that’s over $5,000 of cost that is waiting to rear its head out there.

PERSONAL

This was a month of spending in activities. I signed up for a 5k in August with “early bird” pricing, our daughter’s acro class had semester tuition due, and the kids’ monthly school tuition was paid as usual. Mr. ODA bought a new battery for his car and installed that. On somewhat of a whim, we replaced our back door, which was over $1100 added to Mr. ODA’s credit card.

Just before Christmas, we took a trip. It was just to Cincinnati, which we regularly do as a day-trip. However, we wanted to accomplish a few things this time around. We went to Top Golf for 90 minutes and lunch, let the baby nap at the AirBnB, went to Zoo Lights, spent the night, and then went skiing the next morning (the kids’ first time!). We already purchased season passes (and equipment) for skiing for 4 of us, and had already purchased the zoo annual membership. Without the cost of those two things, our trip cost $330 for Top Golf, lodging, parking (we stayed in the city), a ski lesson for our 5 year old, and food. Our lodging for 1 night was nearly $200 and was significantly more than we’d typically spend on lodging. However, we’re still in a phase of life where the baby needs the be in a space by himself so he sleeps for a nap and through the night. That means we look for a place with at least 2 bedrooms and 2 bathrooms, or 3 bedrooms and 1 bathroom (bonus points for master-sized closets or an extra bathroom with no windows for me to black out). We then made 2 day trips since then, and the kids are doing awesome on skis.

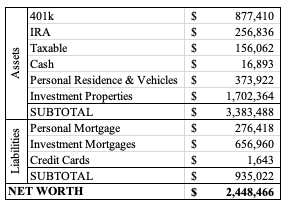

NET WORTH

Our cash has decreased, but that was offset to taxable investments because of our Treasury Direct accounts. Even with our extra spending, our credit card balances are comparable to last month’s. The increase in net worth from last month is mostly due to increases in our investment accounts.

This year’s goal is to hit $4 million net worth. Mr. ODA said that to our financial advisor via Instagram, and he didn’t share that publicly because it wasn’t relatable. The point in sharing here is that, well it’s January and people set goals, and to note that even if this goal specifically isn’t attainable to you in the short term, know that we also once had an account balance well below where we’re currently at. Consistent investing in the market (maxing out the 401k, maxing out the Roth IRAs, and establishing regular investing and watching the market) is a large contributing factor to where we are 10 years later. If I take the investment properties out of the equation, we’re still over $2 million net worth. That doesn’t happen overnight, and it’s something you can start working towards today.

We ramped up our travel this month, which has actually led to us canceling a few trips that were planned for this next month. I went to visit my family for my sister’s baby shower, we went on a family trip for a long weekend, and then Mr. ODA was gone all week for work. We’ve done a few local activities, but several of our plans have been cancelled or postponed due to the current gas prices, which are about $4.75. Even Sam’s Club and Costco, which were holding strong in the low 4s, are both at $4.69 right now.

We’re working towards closing on a new house next Wednesday, so that’s been the stressor right now. We had a month and a half for closing, which is literally the longest we’ve ever had, and then yesterday I got asked for tax information. Seriously, what have you been doing for the last month since I signed off on the initial disclosures? We went with an online bank, so that’s been an extra factor in uncertainty through this process.

RENTALS

I served a notice of non-renewal to one of my tenants. Her lease ends on 6/30, and we want her out. It’s the first time in 6 years that we’re so fed up with a tenant that we actually said it’s time to leave. We’ve had issues with tenants in the past, but we’ve just increased their rent as a means of giving them the option to leave, or compensating us for our frustrations associated with them living there. She, of course, didn’t pay rent by the 5th. When I asked her where rent was, along with the balance of outstanding late fees and the current late fee, she said she was trying to secure a place to live, so she wouldn’t be able to “pay towards that” until the 17th. Pay your rent timely OR communicate a need for more time without the landlord having to hunt you down. That will keep a roof over your head so you don’t have to move when you don’t want to, and it’ll also put you in a position where your current landlord can actually provide a referral at a new place.

My other usual suspect, who I told needed to start getting their act together and pay rent before the last Friday of every month, paid half of rent on the 3rd and sent an email saying we won’t get the rest until the last Friday of the month. Progress, I guess.

We had a massive issue with our property manager in Kentucky. The accountant felt he had a little too much power and ran with it. Mr. ODA went to meet with them, where the accountant had to admit his mistake in charging us $900 in front of the owner. As a means of making amends, the owner credited us the management fee they took out of our security deposit. While I understand their thought process that our contract says “10% of income,” and a security deposit gets counted as income for tax purposes, I disagree with them taking a commission out of it. If that’s the case, our security deposits under them should be 10% higher than a month’s worth of rent. A security deposit’s purpose is to reimburse us for our costs to fix a unit that has been unreasonable mangled by a tenant before their departure. In this case, we have $4000 worth of costs. The security deposit was $895. Them taking $89.50 was insult to injury in this case, especially after they took 18 days before taking any action to confirm the place was abandoned. Moving on.

That house that was abandoned ended up getting rented for June 1st. We’re netting about $250 more per month with the higher rent there.

One of our mortgages was going to be paid off in May, which I mentioned last month. I scrambled to find out how to pay the taxes, which wasn’t easy (it’s a different jurisdiction than most of our houses… being in the county instead of the city). I finally got that figured out and paid the taxes at the beginning of the month.

PERSONAL FINANCES

This month we actually had a few “receivables” to expect. We learned that our lender wasn’t requiring an appraisal (we don’t get it), so they were going to refund us the appraisal fee of $525. We had a major issue with Home Depot and getting an appliance delivered, which ended with us going to the store, buying the appliance, putting it in our car, and driving it to the rental. We had to wait for the terrible delivery company to “scan” the not-delivered appliance back into their warehouse, and then we got $600 back. When I registered my kids for preschool, the system glitched and charged an extra $100, so we got that back. I had already registered my oldest at the same school as this year before we learned we’d be moving, and they were kind enough to return my registration fees, so that was $300.

All that to say, stay on top of your finances. Know what you owe so that you know when you’re overcharged. When someone says you’re owed a refund, pay attention that you receive it; we had to follow up on the refund, and it turned out she hadn’t processed it. Don’t be afraid to ask if there’s an option for a refund in some cases. Just those transactions are $1525 worth of money back in our pockets in a month’s time.

SUMMARY

We have work on a rental that’s still outstanding. I don’t expect her to actually be out on June 30th at 5 pm like she’s been instructed. I have our property manager handling the move out (even though she doesn’t manage that property). This way, if she’s not out on the 30th, I haven’t driven 8 hours to find out I can’t do any work on the property.

We plan on doing a lot of work on our new house after close next week. That’ll take up a lot of our free time over the next few months.

The stock market has somewhat rebounded. It’s not back to levels it was once at, but it’s nice to see balances go up instead of down. Our credit cards are down significantly because I am purposely keeping a low balance right before we close on a house (down by paying it off, not down by not spending…). Our funds for closing are coming from our HELOC, so it hasn’t been a stressor to keep a cash balance to go towards our cash-to-close.

These days, you’re probably not immune to being asked to join or buy from a multi-level-marketing (MLM) business. Also known as network marketing, it a way for companies to sell their product through individuals who market product(s) to their sphere of influence. It gets a bad reputation with “pyramid scheme” and the like, but it’s legitimate and makes sense if you take the time to step back and learn about it instead of repeating the rhetoric you’ve heard from your parents.

Our experience with an MLM led to being open to buying rental properties, which eventually led to me quitting my job and being happy outside of a career. Here’s what I learned by keeping an open mind to an MLM, even though we make $0 from that business today.

This is my experience with our time in an MLM. Mr. ODA would probably have something different to say. 🙂

AMWAY

BACKGROUND

By now, you may have seen the documentary on LulaRoe. Our experience was with Amway, and it was different from how LulaRoe operates. Now, Amway is the black sheep of the MLM world if you go just based on name. They’re one of the original MLMs. But they sell good products in the health, beauty, and home cleaning genres. As a “consultant,” you’re called an “independent business owner” or IBO. I thought the best part was that there’s no inventory you need to hold. If you want to do “parties,” then you need products on hand. However, it’s much different than how LulaRoe would have hundreds of leggings on hand and makes direct sales out of their on-hand inventory. To earn money, you can recruit more business owners, or you can have customers who just order directly from the Amway website each month. You make money off of what your customers buy, as well as the income that your IBOs below you generate.

TEAM SUPPORT

There are multiple “teams” associated with Amway. It’s the education arm of the business. Our team met once a week, and you were expected to be there if you really wanted to be in-the-know and considered serious about growing. They helped you structure your business to take advantages of bonuses offered by Amway, and they taught a lot about having the right mentality. Their goal was to foster personal and business growth, provide mentoring and coaching, and provide the tools to grow your business through conferences and seminars.

This is where we got our start. I know it’s hard to believe, but we both were exposed to a lot of growth through this team. The things we learned through the meetings and books we read during these couple of years gave us the courage to make the big decisions we did, getting us to currently having 13 rental properties.

THE CASHFLOW QUADRANT

Our introduction to the business was started by being given Rich Dad, Poor Dad by Robert Kiyosaki. The book references an earlier book of his, the Cashflow Quadrant. Each quadrant has its strengths and weaknesses. – The upper left corner of the quadrant is for those who have Employee mentality. This is someone who is trading time for money. You work an hour and earn $20. If you’re not working, you’re not earning. You’re making money in someone else’s system, and there are people over you who are making more than you (e.g., a supervisor is making more than a secretary). – The upper right corner is for Business Owners. You own a system that works for you. You have passive income in this quadrant. You may have an employee that is generating income that you earn. – The lower left corner is for Self-employed people. Here you’re still trading time for money, but you have control over how much you earn based on how much effort and time you put in. This is a risky area because you don’t have security and may not have an established system to rely on and project your income. – The lower right corner is for Investing. Your money makes money for you. This can also be risky because you’re not guaranteed positive returns on your investments. If you want to make a lot of money, you need to take on more risk.

The point here, according to the team we were on, was that you want to be a business owner. You want to generate passive income so that you’re not trading time for dollars. While someone else is selling to a new customer, you’re earning a percentage of that sale while not doing anything. As you grow your Amway business, you have more and more people generating income through these sales, which you get a percentage of. The kicker is that you need to hit a certain level within your own business before you earn. We set up recurring purchases to use the products we were selling, and had customers set up with recurring orders, so that we could hit that threshold to be eligible for the passive income.

OUR MOVE FROM MLM TO REAL ESTATE

The biggest hurdle to our success was the price of the products. We aren’t someone who values a better quality to be able to justify the higher price. There are people out there that value this, but it’s not our passion. A peanut butter meal bar comes to $3.14 per bar as a customer order (as an IBO, you get the product at cost, which would be $2.82 per bar). The peanut butter granola bars we buy are $0.50 per bar. Clearly, this isn’t a marginal difference in our expenses. The products were good, but not good enough for our finances to take such a hit. I tried to focus on the beauty side of the business and held parties where I recommend products and let women try it. I had passion behind it, but I wasn’t someone who washed my face regularly and put lotion on. I could see the benefits, but I wasn’t practicing what I preached, and I lost my drive.

The next hurdle was location. Our original meeting was with our specific team within the larger team (based on your “pin level,” you had a meeting with the people who were your “downline.”). We moved down to Richmond, and our closest meeting was Fredericksburg. It wasn’t insurmountable, but it was a 40 minute drive there and back once a week. The larger team would all come together in DC every quarter for a conference. We felt like time started moving faster, and we weren’t close enough to make these our friends between conferences, and so we stopped attending the big conferences. Then we stopped attending the weekly meetings. Then we cancelled our team membership. We still maintain our Amway IBO number, since it’s just $62 per year to do that.

The thought process that we learned from their weekly teachings and reading books we probably wouldn’t have read otherwise led to our desire to generate passive income. Mr. ODA had already been interested in the concept, and then when we were talking about venturing down that path with our Realtor selling our Northern Virginia home, he really got the urge to pursue it.

When we sold our Northern Virginia home, we had about $120,000 in our bank account. About $70k of that went to the downpayment and closing costs of our new house. The remaining went to finding a rental property… or two.

REAL ESTATE, PASSIVE INCOME, AND NO JOB

Real estate is in the business quadrant, but it’s not completely passive income. Truly, the Amway business wasn’t completely passive because you still needed to have the sales (either through your purchases or customer purchases) to be eligible to earn all the passive income available to you in the business. Most months with real estate, I take the rent money, pay out our mortgages, and that’s it. Sometimes I need to make some phone calls to contractors. However, we have to do very little to maintain our business of investment properties. We can also decide that we don’t want to field the phone calls and hand off the rest our properties to a property manager for 10% of rent. If we don’t have a new property or a property to turn over, then we probably put about 100 hours per year into managing the houses.

We knew we didn’t want to be in the employee mentality for the rest of our lives. Funny, because my goal when I was in college was to work for a “big 4” accounting firm and spend 80s hour per week at work. Then I started working for the government, and my goal was to be CFO in my 30s. Then I got to the headquarters office in my late 20s and hated the environment, so I decided I wanted to be no more than a state office’s financial manager. Then we had kids, and I decided I wanted to be home with them to see all the little moments. Things sure did evolve.

I believe that the time we spent with our Amway team changed my heart. I believe that time was important for me to see a different lifestyle and a different mentality. I don’t know that I would have seen the benefits of pushing ourselves to buy more rental properties had I not seen a lifestyle of entertainment.

I started to realize it would be nice to spend time with my family while the kids were little. Who wants to wait until retirement to spend time at home, when your kids are grown and moved out of your house? Why not spend the quality time in their early years? Let’s travel more and experience more in life. Let’s have more time with the kids than the hellish hours of 5 pm to bed time.

Our cash flow each month is about $7k, just based on the rental properties. That doesn’t include expenses that come up, and every once in a while we get hit with a major system that needs replacement, but most of the charges are a couple of hundred dollars here and there. Some days, I wish I could still do what I loved to do in the transportation world, but I don’t miss the office politics and the moderately strict work schedule.

I’m happy for all the experiences that have led me to this point in life. Perhaps you can read Rich Dad, Poor Dad or Cashflow Quadrant and learn a little bit more about all the options out there. Perhaps you just didn’t know that there are opportunities out there where you’re not trading time for money, or where you’re not cushioning the pockets of an executive while you make a certain salary. Perhaps you just needed your eyes opened to the chance to make your money work for you. Or, perhaps you’ll learn that you like the stability of being an employee, and you don’t want to change. But I urge you to take a look at the options and see what works best for you, now that you’re away that there are options.

I left my career exactly two years ago (on the 8th). My son was 8 months old. Honestly, I could have left my job years prior thanks to what my husband set up for us, but without kids, there was nothing to fill my time. I enjoyed my work a lot, so every day worked was another day of money ‘saved.’ I now have two kids and haven’t looked back. I’ve ‘retired,’ but I haven’t stopped producing some income in addition to managing our finances (although I managed the finances while employed full time also).

First, some background of my career.

When I first started working, I was very driven. My goal was CFO by my early 30s. That seemed crazy, until our CFO stepped in shortly after I started working there, and she was 32. Goal marked. I was on the General Schedule pay for the Federal government. I started as an intern in 2007 (GS-4) and joined the training program (GS-7) that gave you a salary increase every year (with acceptable performance) until your position’s max (GS-12 by 2011). I needed to devise a plan that got me to a GS-15 as fast as possible because in 2011 I was 25 years old, which meant I had 5-7 years to climb 3 grades (which takes at least one year in each grade). Not a lot of wiggle room. Well, I soon realized that there was more to life than climbing the ladder as quickly as possible.

I met my husband at work, and we ended up moving to DC for personal reasons and took a GS-12/13 (this means that I started the position as a GS-12, and after 52 weeks ‘in grade’ with acceptable performance, I was promoted to the GS-13 – in theory, not practice). I was warned that it would be an uphill battle to go from the 12 to the 13, and it wouldn’t be as easy and automatic as it had been to get to the GS-12. Commence years of frustration and extremely poor communication from my leadership on expectations. Without getting the promotion within my position, I applied for another position within the same office, and I got it. This was a GS-13/14. I never got the 14.

My experience within the CFO’s office was so hard on my psyche, and I felt that being a young female, rather than my excellent experience, production, and reputation, were playing into the decision making by my leadership to not promote me. I left and went “back into the field” instead. That position was a GS-13 with no promotion potential within that role. By that time, it didn’t matter to me. I didn’t want any more responsibility than what I had; I enjoyed the work I was doing.

My experience in the CFO’s office taught me that I preferred to be at home with my family and experiencing those things. Before my relationship with my husband, I didn’t realize how much I wanted to spend time outside of work traveling, playing sports, and being with my family.

MY LAST DAYS

When my son was born, I took 14 weeks off work (using my own built up leave since at the time the government didn’t provide maternity leave). The typical 12 weeks got me to just before Thanksgiving, and then I worked one or two days per week until after Thanksgiving. The goal was to work and burn my leave to zero before quitting instead of being paid out on it. If you’re paid out on it, then the tax bill hits hard and all at once. Plus, by burning the leave while still employed, I gained even more time off to burn during those pay periods, more 401k (TSP) matches, and added a few months to my back end pension calculation.

Based on my leave balance, being responsive at work, and managing child care, we first set a goal of January. Then, my husband pointed out that January and February had holidays, and I should try to work through those holidays to get those ‘free’ days off. The goal became March because March is long and without any holiday time off! Well, the Federal government shut down that winter for several weeks. My husband’s job was affected by the furlough, but my type of position was funded through a different mechanism that meant my agency still worked (and if you want a lot of detail on that, I’m always happy to talk about it, but I won’t bore the majority here 🙂 ). So I worked full-time while he stayed home with our son. This meant I wasn’t using my leave, so I could work the part-time schedule longer once he went back to work. We then set my goal for May. I probably could have made it longer, but I was afraid that if I got near Memorial Day, he’d say “work through that holiday,” and then 4th of July wasn’t too far away, so I forced my last day to fit.

I had a such a good reputation for the work that I did, that I still get asked questions by friends I made in the position. Plus, I help my husband get through some work things here and there since his position is similar to one I used to hold. I miss the work, but I don’t miss the office politics and red tape, so I’ll take these random questions from friends!

WHAT AM I DOING IN RETIREMENT

There are days that I miss the work I did. I certainly appreciate the flexibility we have now.

FLEXIBILITIES & MOBILITY

We had the opportunity for my husband to work in KY for the summer after I quit. We were able to capitalize on the per diem given for living away from your duty station, and my son was able to spend time with his cousins. I also learned to be extra grateful for our normal-sized house and that I wasn’t trying to live in a one-bedroom apartment for very long.

Since my husband’s job required fairly frequent travel, my son and I were able to join him for those work trips. We went to Orlando and Glacier National Park together! We also took several trips just for fun, like to the Braves Spring Training games.

Pandemic life made us realize that we wanted to be closer to family earlier than we had intended. We loved our neighborhood, and the schools were going to be great, but having to isolate from people for so long was hard. It was also a logistical nightmare to get things done sometimes without family to help watch the kid(s) in a pinch. Since I’m not working, we decided to move to KY to be near Mr. ODA’s family – a lot earlier in life than we had intended. We discussed the possibility in May, discussed it more seriously in June, had our house listed in August, and closed on it in September. Nothing like a hasty decision with a newborn and no house lined up to move into on the other end of this decision! But had we both been working and both needing to be employed once we moved, we wouldn’t have been able to make such a move as quickly as we did. You can read more about these decisions in my ‘Moving States’ series posted recently.

It’s been nice to be able to do activities with the kids during the week when things are less crowded. Sure, a pandemic limited our options for the last year, but we still have more freedom. I enjoy seeing all the things they learn in a day. There are hard days where I crave more adult conversation or the ability to sit quietly and get something done without being asked for the 90th snack of the day, but I still wouldn’t go back to work.

WORKING

I’m the type of person that wishes I knew the inner workings of so many things and have a strong desire for efficiency. When I took my first job in DC, I kept pushing that I wanted to bridge the ‘headquarters’ and ‘field’ communication gap. For instance, there was a process that the field would submit to headquarters for action. Headquarters had their own internal process of tracking and executing it, but the field didn’t know that process. Therefore, headquarters spent a lot of time answering “what’s the status of my request” type emails. I explained the process to the field, and then we were left to spend more time processing the actions than managing questions.

All this to say: I’m quick to jump at new opportunities where I’ll learn something. I like knowing the process for things and find these details help me better connect with other people. While not being employed full time, I’ve kept my eye open for short term and part time opportunities to do something different.

ENUMERATOR

In February 2020, before the pandemic started, I applied to work for the US Census. We don’t “need” the money, but it gave me something to do that’s different. The application said Census field work was expected to be conducted in April and May. This was going to be hard since my daughter was due at the beginning of April, but I figured I wanted to be in the mix for information instead of assuming I wouldn’t be physically able to do work. Well, the pandemic delayed everything. I didn’t get any information until June, went to training, and then started work in July.

I was able to set my schedule in advance, which was nice. I learned at the beginning that it was hard for me to manage pumping and for my husband getting our daughter down for naps. So I changed my future schedules to be in 2-3 hour segments so that I could go home to feed her and put her down for her next nap. I was given a cell phone that had my work assignments (addresses to collect census data) and my day’s hours. I went door to door trying to gather census data from addresses that hadn’t responded. Most people didn’t answer their door, which meant that I probably had to knock on neighbors’ doors until I could identify at least the number of people who lived at the address in question. That was probably the hardest part because I would introduce myself and immediately be met with “I filled mine out!”

The work was in my geographic area. The furthest I had to travel for my assignments was 25 minutes. We ended up moving out of the area in September, so I missed several opportunities to work more, but most of the work was dwindling by then (the work started to send us further and further from our ‘home base’… even an ability to go to other states).

Honestly, I wanted to be the number crunchers in the office, but that position wasn’t available. I thought if I started with the field work, I could get my foot in the door. Our move hindered that a bit, but I’m glad I did it. I learned how the Census gets tracked. I made some money. I have some good stories (encountered several types of animals, including being surrounded by two large dogs that got my adrenaline running; left a few houses because my gut said it wasn’t safe). The application used to track information needed help, as it assumed we were all working in cities, whereas I was usually out in the country (e.g., no close neighbors). I boosted my confidence with glowing remarks from my supervisor since I put more than bare minimum effort in and was efficient in getting the work done.

the giant dogs that circled me, but eventually let me back in my car

SEASONAL CHANGE RUNNER

A local race track had thought that a limited number of patrons would require less staff. Unfortunately, once the race meet started, they were surprised at where their deficiencies were. Less patrons doesn’t necessarily mean less activity at concessions and bars, for example. Mr. ODA and I were approached about an opportunity to fill this gap. We’d have to be ok being on our feet for 6-8 hours, pass a background check, and pass a COVID test (interest fact: this is my only COVID test I’ve taken).

The race meet is only 15 days. We were approached after the races had started. We needed a COVID test, but didn’t want to pay out of pocket for it, so we had to wait until the next Wednesday to get that. Between all these factors, we were left with only a few days that they needed help. One of those days, we already had plans to attend the meet as patrons, so we didn’t want to lose that ticket. Mr. ODA worked one day of the meet, while I worked 3. I then also picked up a shift for their Derby celebration (although it’s not where the Derby was held).

We had a security guard escort and walked between all the bars and concession stands making change. Patrons tend to start their day with large bills, so the cashiers need smaller bills changed out. That’s where we came in. On the first day, I walked over 26k steps – while wearing ballet flats. My feet and calves weren’t happy about it.

It was an interesting experience. I enjoyed watching the transactions that took place, and the time passed quickly. We didn’t even know what our hourly rate was until our first pay checks, but we thought it was something new and different, so we jumped at the opportunity.

BREASTMILK DONATION

I’ve breastfed both my children. For my first, I worked while he was 3-8 months old, so I needed to pump to leave him with someone else. I learned that I produced a healthy amount of milk and looked into donation methods. A friend of mine had donated milk to a milk bank that works with NICU babies, so I explored that option. I went through their rigorous approval process and took their oath on health standards. I donated over 1200 ounces to the bank that first time. They weigh the milk upon arrival, and I was paid $1 per ounce weighed.

It was a lot of work, don’t get me wrong. I agreed up front to provide 350 ounces per month for 4 months. I didn’t hit that mark. It was mostly to my lack of knowledge on how to freeze the milk so that it took up the least amount of space when packing a cooler. They also had a requirement that not more than 6 ounces gets put in a single milk bag, so that added up. I struggled with their packing mechanism; no matter how many of their videos and attempts I made, I couldn’t seem to get 350 ounces in one cooler. It’s nerve wracking when you’re trying to get frozen milk from a freezer to a cooler while it’s 80 degrees outside (garage freezer), and you feel like you only have one shot to do it right or you jeopardize your entire stash from arriving frozen and being worth all that time and effort. I digress.

My second child didn’t latch for the first 4 weeks of her life, so I was exclusively pumping. That meant that she wasn’t regulating how much I made, and so I was making a whole lot more milk than she needed. I knew the rules associated with this milk bank from last time, so I was on my A-game from the start. Lesson learned – double check their rules before any future donation attempts because they changed a couple of their rules. They now wanted 400 ounces per month for 4 months, and they allowed (and encouraged) as much milk in one bag as possible. I wish I had known that on the days where I was trying to figure out how to get 7 ounces into two bags and whether I wanted to hold off on mixing later pumping sessions. I did better with the packing this time around, but it still wasn’t great. I nailed it on my last cooler, but it was too little too late. After my last cooler went off, I only had about 150 ounces left over. We were about to be ‘homeless’ (remember when we sold our house but didn’t have a new one to go to yet!) for 7 weeks, and I couldn’t keep up with pumping and moving around to all different places, so again I didn’t meet their quota. They’re always so gracious for whatever they receive though. I ended up donating just over 1,100 ounces this time around at $1 per ounce.

Mr. ODA could retire today. But again: what would we do with all that free time, what would he do about his leave balances that we don’t want to cash out, what do we do about health care? Our monthly expenses are more than covered by our rental property cash flow, but we don’t want to be stuck at home not being able to spend any extra money because we don’t want to raise our expenses. Since Mr. ODA is going to keep his job for now, we’re planning a more extensive summer travel calendar and trying to shift the mindset away from super frugality since we’ve already met many of our financial independence goals. Our savings now will create lifestyle in the future once we’ve both taken the “retire early” plunge.

The biggest change since I was working is that the Federal government now pays paternity/maternity leave. As I shared, I had to use my own leave balance. The Family Medical Leave Act just holds your job – it allows you to use your own time off, but it doesn’t guarantee payment. So I was granted 12 weeks of unpaid leave that I was then “allowed” to substitute my own leave for. I had planned for babies, so I had a great leave balance to get me through my maternity leave. Now, my husband will get paid for 12 weeks without having to touch his leave balance! Since we’re talking about having another kid, he’s going to stick around to utilize that benefit.

I’ve done things here and there to keep me sane because talking to other adults is a big need for me. But I wouldn’t trade all the time I’ve had with my two kids thanks to Mr. ODA’s extensive research and aggressive saving/investing to get us set up for success and early retirement. I’ll continue to keep my eye out for these part time opportunities where I get to learn something new.

This month had a lot of money movement – tax payment out, stimulus check in. As I’ve shared before, we don’t budget. But you can start seeing how we’re pretty consistent on where we spend out money. This is because we have a spending mentality that we use to make each decision, rather than giving ourselves a ceiling in each category. I believe some may see a ceiling as a definitive amount to spend (e.g., if I’ve allocated $100 for restaurants this month, and by the last week I still have $75 in that budget pot, then I’m going to go spend it). If you know your long term goals and take responsibility for your decision-making, then you don’t need to pay close attention to each dollar.

With that said, my family came to visit for a week. It was our second’s first birthday, and my dad is helping us finish our basement. With 3 more adults in the house, we spent more than typical feeding them and eating at restaurants versus cooking after spending the day working in the basement. Mr. ODA and I share the same birthday, so we splurged for a nice meal that night. We actually spent about $300 at restaurants over this last month, but thanks to our Chase credit card, we received statement credits for $188 worth of these purchases!

We have also spent more on entertainment. We went to a winery and a brewery, purchased tickets for the local horse race season, and have done other activities now that the weather is nice. The pandemic and winter had our spending lower than our usual amounts, but I expect our spending to be more than it had been in these coming months. We’ve already put together our summer bucket list for travel.

We had all the tenants pay their rent on time, except one who eventually paid. Our rental income is $12,353, and we pay our business partner about $2,100 (we collect the rent and then pay him to cover the mortgages he holds and his half of the ‘profit’ after the mortgages are deducted from rent). We had to replace the HVAC in a rental. Luckily, this rental is owned with a partner, so only half the cost will affect us. We haven’t paid the bill yet, so that will hit next month.

We paid about $5,972 for our regular mortgage payments. We put an additional $5,000 towards an investment property mortgage, which now has a balance of $8,665. We also put $5,000 towards one of the properties that we have with a partner, which he matched, leaving that balance at $42k.

Every month, $1100 is automatically invested between each of our Roth IRAs and each child’s investment accounts. Our stimulus checks that we received for the kids went directly into the kids’ UTMAs.

Our grocery shopping cost us $539.

We spent $91 on gas.

$290 went towards utilities. This includes internet, cell phones, water, sewer, trash, electric, and investment property sewer charges that are billed to the owner and not the tenant. We still haven’t sought reimbursement from the builder on our electric bill, but this month’s bill was significantly less than the previous months.

About $1300 was spent on supplies for the basement bathroom work. We registered the kids for swim lessons, registered our son for pre-school in the Fall, did more activities with the nice weather, and I made several gift purchases (current birthdays, baby shower, next Christmas (I like buying when I find something that makes me think of a person rather than a mad dash in the Fall to buy gifts)), so that was about $400.

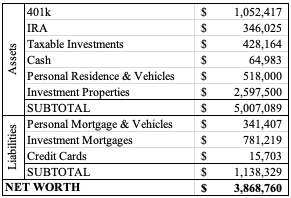

SUMMARY

Our net worth has increased over $123k since last month due to our investment accounts and property values increasing. Our cash balance is starting to dwindle down to what we typically carry as ‘cash.’ And our mortgage balance is decreasing more than average due to our goal of paying off two of the mortgages that we’re carrying.

I realize that some of the items that I share each month will be repetitive, but I’m catering to new readers that may not have seen the previous month’s details. As always, feel free to reach out if you have any questions about this information.

SPECIFIC LARGE CHANGES FROM LAST MONTH’S UPDATE

Paid $8,000 towards an investment property mortgage. This property’s mortgage balance is just under $14k, and we expect to have it paid off in the next 6 months. It would be earlier, but we’re also paying off another mortgage at this time, so we’re putting money towards that one next.

Mr. ODA cashed a few savings bonds that were mature, so we brought in $622 that wasn’t planned.

MONTH’S EXPENSES

Every month, $1100 is automatically invested between each of our Roth IRAs and each child’s investment accounts.

We had all the tenants except two pay their rent on time, and the other two houses paid on the 12th (typically when a tenant is late, the balance is paid on the next Friday of the month – pay day). Our rental income is $12,353, and we pay our business partner about $2,100 (we collect the rent and then pay him to cover the mortgages he holds and his half of the ‘profit’ after the mortgages are deducted from rent). We made it through the month with no investment property costs! We did have a tenant power wash our house out of the kindness of their heart though.

We paid about $5,900 for our regular mortgage payments.

Our grocery shopping cost us $500. We did the trial period for Walmart+. Unfortunately, the first two weeks of that trial period were destroyed by back-to-back ice and snow storms, so we couldn’t ever get deliveries scheduled within a couple of days. Once life went back to normal, there were plenty of delivery times available, even same day. While it was convenient, it wasn’t worth the annual fee and tipping the driver each time, so we cancelled it.

We spent $57 on gas, and $83 eating take-out.

We made some purchases that aren’t typical: ski season pass for next year ($119), medical bill ($70), and some furniture and odds and ends for the house (~$1,500).

$464 went towards utilities. This includes internet, cell phones, water, sewer, trash, electric, and investment property sewer charges that are billed to the owner and not the tenant. Last month I shared that our electric bill was very high. We learned through the course of 6 HVAC company visits that our unit was not running properly, and that meant our heat strips were essentially on since we moved in ($$$). We will seek financial compensation from the builder once our next electric bill comes in.

SUMMARY

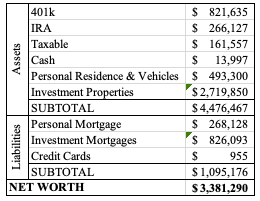

Our net worth increased by $45k from last month’s update. This change is mostly due to the value of our houses increasing and our mortgage balances decreasing.

I had so many things to share, and now it’s time for another net worth update, but I hadn’t gone into the details of our 2019-to-2021 changes! I promise, it’ll come.

SPECIFIC LARGE CHANGES FROM LAST MONTH’S UPDATE

We paid off $5,000 left on one of our credit cards. This credit card was opened for a large purchase, and the 0% introductory rate expires at the beginning of March, so I wanted to make sure it was fully paid off so we don’t pay any interest on the balance.

We put $2,000 towards an investment property’s mortgage, and we received $2,000 cash out from another investment property’s refinance.

MONTH’S EXPENSES

Every month, $1100 is automatically invested between each of our Roth IRAs and each child’s investment accounts.

Between our personal home and the investment properties, except for the one that we refinanced so we skip February’s payment, we paid about $5,500 in mortgages. To put this in perspective, we brought in over $8800 from those properties, which doesn’t count $900 worth of rent at this time that the tenant is late on. This doesn’t include the properties that we own with a partner through an LLC, which nets us $400 each month (although one of those properties hasn’t paid rent this month yet either).

Our grocery shopping cost us $409.

We spent $76 on gas, and $72 eating take-out. We typically visit family once a week (45 miles round trip), go to the grocery (10 miles round trip) once or twice a week, and get take out once a week (10 miles round trip).

I made two Amazon purchases for non-grocery items we needed (e.g., activities for our 2 year old, vitamins, items for our daughter’s 1st birthday, and – really important – potty training seat), which totaled $125.

We owed personal property taxes from last year’s time in Virginia, so I paid the $94 for that. I also paid the balance of our personal home’s HOA, which was $85 for the rest of the year.

As for the investment properties, we had to purchase a new washing machine, which was $528 (although that cost is split with our partner for this particular house). We also paid for the insurance on a property that isn’t escrowed, which was $203.

$430 went towards utilities. This includes internet, water, sewer, trash, electric, and investment property sewer charges that are billed to the owner and not the tenant. Our electric bill was insane this month. We moved into our new home in November and had previously been living with gas heat so didn’t know what to expect. Mr. ODA called the HVAC company to have them run a diagnostic check on our units, and we found that the downstairs condenser isn’t working. It isn’t resolved yet due to an ice storm here, but hopefully it’ll be fixed today, and we hope to see some sort of compensation for our high electric bills due to this not working properly.

SUMMARY

Our net worth increased by $102k from last month’s update. This change is due to fluctuations in the stock market and the value of the houses. Our 401k balances increased over $35k, our taxable investments rose over $10k, and home values increased over $42k all together. A difference of over $5k in our credit card balances also contributed to the change in net worth.