This month was unbelievably painful financially. And yet, I appreciate that we’ve set ourselves up that we can handle these things without stress, even though the balances on credit cards made me feel like I was drowning. At one point, we had over $30k on credit cards. I’m still juggling life as a mom, financial consultant, part time worker, and volunteer on the HOA board. Oh, and managing two vacant rental turnovers, throw in 2 trips away from home, and school starting.

RENTALS

We had one house pay late, with little notice and communication (if you’ve been here, you know this is a pet peeve of mine). They paid the late fee at least. I had another house pay partial on the 3rd and then true up on the 6th. Again, no communication, and she beat me to asking what the deal is. I also had a tenant who already pays twice per month be late on both of this month’s payments, so that also brought in late fees.

In a story for another time, we have two vacant rentals. 11 of 13 houses renewed. Two houses each actually moved out of state, and unfortunately, my kind heart scheduled both of them to end their leases on July 31st. We’ve been spending all our time at these two houses. The one had smokers in it (against the lease) and we’re struggling with that. We’ve replaced the carpet and painted all the walls (except 2 closets and a powder bathroom) and it still smells funky when you walk in. Then there’s just the routine type turnover things like scrubbing and wiping dirty hand marks off the door frames. All of these things will be detailed in separate posts. The other vacant one was quite the story, so that’ll be multiple posts. Our attention isn’t as heavily on that one because we’re going to likely sell it instead of re-rent it.

We replaced a roof ($5500), replaced an HVAC ($8300, but split with a partner), evicted bats ($1480), and made decisions on flooring replacement in another house with extensive termite damage. Seriously. Financially painful. Coming this next month, we will also be paying for termite repairs at another house where we tore out carpet and laid LVP.

HEALTH COSTS

I tend to focus heavily on this topic in this blog. It’s surprising because it’s not really the niche of making money, but insurance and doctor bill processing seem to be wrong more than they’re right. Therefore, it falls more into “protect your money” than anything else.

This is a longer story for another post yet again, but the gist is that the insurance company took 6 months to process a claim. They sent me the bill in June. I called 3 weeks after the bill arrived to find out they had sent my balance to collections because their system flagged it as a January overdue balance…even though this was my first invoice on the matter. Love it.

The end result here is that we needed to add $1600 to the credit card.

PERSONAL

I don’t know that there’s much personal life happening with all those other things we’re managing. We took 2 trips. One didn’t cost us much because the grandparents take care of a lot of the cost, another one cost us more than usual because I put a lot of effort into food that we usually don’t do when we travel there. Overall, the trips were fairly inexpensive financially, but they took a toll on me due to the time commitment and what we had to give up by doing these trips.

Otherwise, we’ve just been wrapping up summer and starting school. We’re about to get back into baseball season with lots of practices.

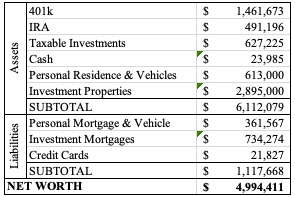

NET WORTH

The market had a big jump last week and my update of financials occurred Thursday morning. Unfortunately, life put a blog post on the back burner while we were turning over a rental, so I’m only getting around to posting this now. The market is in a fairly similar spot as of yesterday’s close, and I’m thinking we’d even be over $5 million if I were to fully update our financial status right now. We’ll just hope for the best for next month.

In October, we’ll pay off our $15k credit card that we’re carrying, so that will be a big swing in our credit card balance two months from now. We need new windows at our house (the seal keeping in the gas between the panes is going on quite a few windows (or went years ago), and it creates this streaky dirty look to them), but I think I’ll appreciate not carrying this large credit card balance month to month while we utilize the $0 interest for a while.

*I’ve been working on this post for a week, so my numbers are a week old, but I don’t want to re-update them. I’m also posting on a Tuesday just to get this ‘out the door.’*

I’m starting to pull myself out of the overwhelmed hole I felt I was in. There’s still a lot going on, but I feel better equipped to stay on top of things. I had just been so exhausted, that I didn’t have the energy to do anything extra each day, and I was just getting by. Last weekend, I was able to work on pressure washing our patio and deck furniture (which was long overdue), and then I stained our deck. That’s been a pretty good springboard to me getting a fire lit under myself to get other things done, so that’s felt really good.

Our middle child graduated pre-k on Thursday. That was a big milestone, and my poor girl is so sad that she’s going to miss her teachers. She’s really struggled with my going to work and not being home all the time (although my time not home, while she would be home, averaged about 10 hours per week). I have things better organized at work, and I’m feeling good about my tasks and role in the office, so the hours I’m spending there are dwindling. I had agreed to about 20 hours per week, but I was closer to 26/28 each week. The biggest issue was waiting for someone to be available to help me, and then that everyone else is full time, so they don’t realize I’m trying to get out of here by 2 pm each day. This week our oldest graduates kindergarten and has many events around end of school.

RENTALS

One of the mortgages has been paid enough that the balance dropped from 6 digits to 5 digits. It’s still a lot of money owed there, but that felt like a nice accomplishment when I went in to capture the balance!

June is Richmond tax season for these houses. That means I’ll be paying out large chunks of money for the houses we have no escrow on.

We had a few maintenance needs come up. One house had the water heater flood the basement. Luckily, I think we’re OK on that front. We replaced the water heater. The gas wasn’t hooked up right, so the tenant called the plumber to get that squared away. This happened while I was in a different state, and I’m so grateful it happened in a house with a handy tenant.

We had some flashing fall off a roof line. This wasn’t a priority to address at the time, but the tenant started claiming allergies were flaring up because birds were getting in the attic. Sometimes you just need to accept that’s the story you’re hearing. We had a handyman go over there and verify there are no birds anywhere. The “hole” she thought she saw was just where the soffit was hanging a bit, but there were no gaps in the wood structure itself. He tacked up the soffit, and I contracted with another company to repair the one piece of flashing.

That handyman also went out and handled a wasp nest. At that house, the tenant says a window won’t stay open when she opens it, and we let her know it’s on our radar now, but it won’t be fixed just yet as our people are spread thin and that’s not an emergency. That house had a temporary tenant in it (housing with our current tenant). To cover the tenant and us, I asked for a $500 deposit. When they moved out, I had our tenant sign that there was no damage, and I returned the deposit.

We’re still working on the major termite damage that occurred at another house. There was quite the domino effect. Leaks from bathrooms and the laundry room created a very wet environment, which created a breeding ground for termites, which feasted on our wood all over that place. The crawl space got cleaned up, but we’ve been waiting over a month for the bathrooms to get replaced and fixed. I’m hopeful that it’ll start next week, but frustrated nonetheless.

I had a leak from a toilet bolt at another house. I was frustrated because we had just been called out for water on the floor at this house recently, but it turns out this was necessary. When the house is a certain age, things just wear away and need replaced.

We also had a limb fall from a tree at another rental. The tenant explained how much of a liability it was for me. I love when tenants instruct me on my level of liability (that’s sarcasm). We have a tree guy that’s been super useful for many things and he handled it the next day with no problem.

PERSONAL

We haven’t been spending much money. Most of our money these days goes to grocery shopping. On our current statement for our main credit card, we only have 11 transactions recorded for over 3 weeks.

We paid our last month of pre-school for our second. They are closing the school and they didn’t want to add on days for the snow days that occurred, so they gave us $50 off the last month of tuition to cover the 2 days we were owed for make-ups. Since the school is closing, everyone scattered, and we ended up not getting into another preschool next year for our youngest. So at this point, that’s an extra $375 per month in our pockets next year – unless a spot opens up for the littlest.

Mr. ODA took the buy out, which I think I mentioned last month. His last day of work was April 30th. He said he’s settling into the not working concept and starting to get over the desire to know what’s happening at work and with his programs he worked so hard on. He’s done a lot of work around the house here, including treating for termites in a very intense fashion, but that was cool to see.

NET WORTH

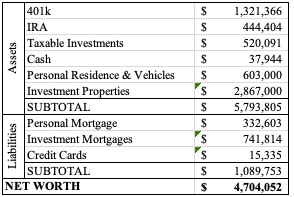

Two months ago, my job asked for my goals. It’s a specific document that I was to fill out. Someone else had mentioned their net worth goal, and our next big step would be $5 million net worth. Well, the market has been in shambles, and our net worth plummeted from where it was. I thought it prudent to not make such a goal when our net worth is completely reliant on the market actions right now (i.e., we’re not selling/purchasing or making any big moves that would drastically change our net worth outside of the market actions). We’re finally on the upswing and now at the highest net worth we’ve been, so that’s encouraging after those big dips recently.

Well, my desire to post every Thursday fell off there. I started a new job, Mr. ODA’s Federal job has been in limbo, and just general life things have been going on and keeping us busy. The kids started t-ball in the past few weeks, our youngest was waitlisted at both of the preschools we tried for, and the rentals have needed more attention than average. Let’s dive in.

NEW JOB

I was approached by someone I serve with on our HOA board. They were looking for a new person who has a financial background, was really organized, and could handle talking to people regularly. It appears that I made such an impression on him and his wife. I wasn’t ready to get back into the workforce. While I have enjoyed my temporary jobs I’ve done since I quit my career in May 2019, I always had a ‘sunset date’ on those activities. I knew that each job was only for a short period of time, and I’d get back to freedom/flexibility. This was a new territory they were asking of me – be on a set schedule and away from my kids.

I expressed that my need for entering back into the workforce was that I wanted to be part of my kid’s activities and I needed to work between school hours for the most part. They expressed a desire for me to work 30 hours, and that just wasn’t feasible. Based on what they told me about the tasks required of the job, I was able to come up with about 18 hours of work, knowing it would likely become 20 hours. So far, I’ve worked more than 20 hours each week as I’m learning, and things are not moving as quickly as I expected them to. I’m 2.5 weeks in, and at this point I can do all the main tasks. Where I’m struggling is the knowledge of all the “one off” transactions and how some people are treated a little differently than the standard.

Overall, I’ve been super grateful that Mr. ODA has given me the space I needed to get my feet under me these past couple of weeks, and I’m really enjoying learning these new tasks and being involved in this sector.

FEDERAL WORKERS

It’s been rough around here for almost two months now. While Mr. ODA is still employed, there is a daily concern that the news will come in. There’s no security like there used to be expected for a government position. The blows have become a bit more scattered than it being such a daily barrage, but there’s still uncertainty and daily updates and waiting for more information that’s occurring.

PRESCHOOL

Both old kids will be in regular school next year. Our youngest has a late-in-the-year birthday, so he wasn’t eligible for preschool until this coming school year even though he’s already 2. The preschool where both of the other two went to shut down. My middle is finishing out the year there, but next year, they sold the preschool concept off to a third party. The company that took over has terrible reviews, and everything about them screams ‘daycare.’ While people need daycares, and that’s fine, we don’t need that. I wanted a space that had a curriculum.

The school previously had a daily agenda and an expectation that the kids were there from 9 to 12. This new school has a come and go as you please set up, and they couldn’t provide me a break down of their daily schedule. The admissions person was actually quite rude and condescending to me, after taking 4 days to return my phone call. I’m not in a desperate need for our youngest to go anywhere, so I won’t be trying to enroll him there.

We had hoped to get into another preschool by our house, but the closure of our old school sent a mass exodus to the nearby preschools. I told Mr. ODA that I wanted to join their church so I could get 3 weeks ahead on signing up, but he said that wasn’t ethical and was more than just saying “I want to join your church.” So I didn’t. But several other families did. And they got in. And I’m still really sad about that. He’s waitlisted there, and there’s been no indication of hope that he’ll get off the waitlist.

I tried for a “moms day out” program, which would cover one or two days per week (I was looking for 2 days previously). He’s waitlisted there, but she gave me a glimmer of hope that even though they don’t have a lot of turnover, there is a chance a space opens up either right at the end of this school year or at the beginning of next school year.

I had originally ‘mourned’ the loss of my freedom with the preschool closing down. I have been at my kids’ beck and call for 7 years by the time our youngest would go to school. Even though it was only going to be 6 hours per week, I was excited to get things done that have been on my to do list for years and just run errands unencumbered. I’ve lessened my extreme feeling on that over time, but it still would be nice to have a few hours dedicated to me and my schedule at some point.

RENTALS: RENT RATE

I evaluated our current tenants and their rent rate back in December. I should have just written the letters at that point and been prepared for the deadlines, but I didn’t. So this week, I got those rent change letters prepared, printed, and mailed. We typically change the rent by $50 every two years for our long term tenants. That’s the approach we took here except for a couple that needed more catch up. One tenant has already responded and executed a change to increase their rent. I have 4 more out there waiting for the tenant to tell me they accept the adjustment or will be leaving at the end of their lease. I also have another tenant who will be staying another year, but I didn’t change their rate since I had changed it by $25 last year.

RENTALS: TERMITES

We have a house that we purchased with termite issues. We knew it going in. We had it treated, and then we fixed the really bad areas. We then didn’t get notification about an annual warranty payment they would do, so our coverage lapsed for a few years. We saw swarmer termites in one part of the house and called them back. They offered to let us backpay those missed warranty years, saving us about half the cost it would have been for a new treatment. Well, we’re paying for that now. For the last 4 years, they’ve checked the property once per year. They’ve noted termites actively being there with more damage, and they didn’t clearly communicate the concern of the condition until this month. We have major problems in the house. One wall in the laundry room is so bad that the termites ate the backing off the drywall and the drywall is all cracking off the wall because it’s not being held onto anything. It really hasn’t been fun, but I know we will be able to fix it. So far, we’ve had the crawl space cleaned out and relined with a vapor barrier, and some plumbing issues fixed that were creating a perfect moist condition for termites to gravitate to. We still have to rip up the carpet, fix the subfloor, lay LVP, rip out a shower insert, reinstall the insert, and get the shower operational after that. It’s a lot.

PERSONAL FINANCES

Mr. ODA reduced our monthly contributions to our investments. We were putting $3,000 per month in (3 separate $1,000 transactions), and now those have been reduced to $500 three-times per month. The kids still get $100 per month each into their UTMAs.

We’ve been so busy that we have hardly spent any money. Outside of insurance and medical payments, the only extra spending I’ve done is for our daughter’s birthday parties we’re having this month. I’ve bought some clothes since I’ve lost weight on my post-three-kids journey too. Usually, we’ve booked a trip by now, but we haven’t done that either. Overall our spending is lower than it has been.

NET WORTH

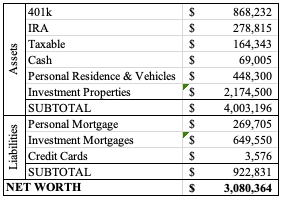

The market is well below where it has been, and all our numbers show it. We are over $189k lower than last month. I haven’t updated our property values yet. I’ll probably do that next month as the spring market ramps up.

While the housing market has cooled some since I started this post in the Spring, there are still some areas that are moving quickly and aggressively, and this information is still helpful regardless of you being in a multiple offer scenario. Over the course of 6 years and 18 properties purchased (and countless offers made), we’ve caught on to some helpful parts of contracts. Again, keep in mind that I’ve seen real estate contracts in New York, Virginia, and Kentucky; this is not all encompassing or what may work perfectly in your market. This also doesn’t include all parts of a contract since most of them are standard and/or can’t be anything but matter-of-fact (e.g., will the property be owner occupied; is the property subject to a homeowner’s association).

BASICS

Your contract is going to encompass the basics of the purchase each time. This would be the buyer and seller names, address of the property, offer price, and closing date.

Typically, the buyer’s agent draws up the contract with the information being offered. If the offer is accepted by the seller, the seller signs the contract. If there are negotiations, the buyer’s agent will adjust, have the buyer re-sign, and then submit to the seller for signature. When the buyer makes the offer (which is just filling out the contract and sending it to the seller), the buyer will typically include an expiration date of the offer. This isn’t always enacted, but it’s there as a protection so the buyer isn’t sitting idle for extended periods of time waiting for a seller to make a decision. For example, we had an expiration clause in a contract recently where our offer expired at 8 pm that night, but we knew they weren’t going to review offers until the end of the weekend; we had put it in there as a way to hopefully push the seller to make a decision with just our offer instead of waiting for more offers to roll in. We ended up getting the contract on the house, even though our expiration date had technically expired.

In Virginia, the closing date language says “on or before X date, or a reasonable time thereafter.” In Kentucky, it says “on or before X date,” and if you can’t close by that date, you and the buyer have to process an addendum to the contract with a new closing date. We had a contract, as the seller in Virginia, close 2 months after the date in the contract. We were furious about that. We could have walked away and kept the buyer’s earnest money deposit, but then we’d have to formally list (it was an off market deal) and manage that process along with the home inspection issues that may arise. We also had a contract in Kentucky where our lender messed up and delayed our closing, so we had to sign an addendum to the contract to allow us to close a week late.

EARNEST MONEY DEPOSIT (EMD)

Earnest money, or good faith deposit, is a sum of money you put down to demonstrate your seriousness about buying a home. In most cases, earnest money acts as a deposit on the property you’re looking to buy. You deliver the amount when signing the purchase agreement or the sales contract, and it’s applied to your balance owed at closing.

This is not a requirement, but it’s showing your “good faith” to purchase the property because there’s a penalty to you if you try to walk away from the purchase.

In most cases, you pay the EMD to your realtor’s office and they hold it until closing. In Kentucky, they’re on it right away, asking you to send the check as soon as the contract is signed. In Virginia, I didn’t always send the EMD. The amount is listed in the contract, so if I were to default on the contract as a buyer, I would still owe that amount even though I hadn’t paid it to my realtor’s office.

Typically, you’re looking to put 1% down. On a $90k purchase, we gave an EMD of $900. On a purchase of $438k, we gave an EMD of $5,000 (but there were other factors at play as to why we went higher than 1% on that, which I’ll cover later).

CONTINGENCIES

Some items we’ve seen in our contracts are options for the buyer to back out of the contract, or a contingency.

Financing

A sale can be subject to financing. If it’s not an all-cash offer, and there will be a loan secured to purchase the property, data can be entered to protect the buyer’s interests. Typically, it’s going to list the years of the loan to be secured (e.g., 30 year conventional), a downpayment amount, and a maximum interest rate. The interest rates hadn’t been fluctuating much, but this would play into things in the past few months. If you tried to purchase a home when the prevailing interest rate was about 4%, and then interest rates rose to 5.5%, it may affect your ability to qualify for the loan or put you outside a comfort zone for your monthly payment amount. For example, on a $250,000 loan at 4%, your monthly payment is about $1200 per month (principal and interest); if the rate raises to 5.5%, your monthly payment becomes $1420 per month.

This information does not lock you into that break down. If the contract says 80%, and you decide to put 25% down based on the rate sheet, the contract isn’t changed nor is it voided.

Appraisal

If the sale is subject to financing, then it has to be subject to the appraisal. This is a lender requirement to protect their interests. There are some caveats to this, but I will cover them later since they’re more advanced. An appraisal will cost the buyer in the realm of $450-600.

If you’re attempting to qualify based on rental property income, the lender may require you to pay for a rental appraisal as well. We’ve seen this cost at an additional $150, but we’ve typically been able to negotiate our way out of that by providing leases and income history.

Home Inspection

This is one that I almost always recommend including in your offer. This is your “out” in almost every situation. If you get a home inspection, and it finds anything, you can walk away from the contract and not lose your EMD. If a house is important enough to you (a personal residence that you want regardless of what you find on an inspection report), you may eliminate this contingency, but you’ll typically include it. You can even include that you’ll do a home inspection and decide to not do it.

If the house is being sold as-is, it doesn’t mean you can’t get a home inspection. You can still get the inspection to know whether you want to move forward with the purchase. Being sold as-is just tells the buyer that the seller is not willing to negotiate price or fixing items if the home inspection finds something.

The buyer is responsible for the cost of the home inspection. We’ve paid between $300 and $650 for it. The inspector will take about 2 hours to look through the house, including the roof and mechanical parts behind the scenes. Sometimes the inspector will say “this doesn’t look right, but you need to consult a professional in that trade,” which is usually what happens when it comes to roofing. We have done a home inspection, found too many issues to manage (e.g., stairs built out of code) and walked away from the contract. In that scenario, we don’t lose our EMD, but we did pay about $500 for “nothing” (unless you count all the savings of not throwing money into the house to make it safe and livable).

If you find items on the home inspection that you don’t or can’t fix yourself, and the house isn’t being sold as-is, you can request the seller address them. An addendum to the contract will be filed to identify what the seller agrees to fix, and professional receipts have to be supplied before closing to satisfy the requirement. A seller may say they don’t want to be bothered with coordinating the trades to fix the items and offer financial compensation (e.g., we project the cost of these fixes to be $1000, so we’ll take $1000 off the purchase price).

In the realm of “the contract can say almost anything you want,” here’s an example of an additional term that was in one of our contracts. On this particular house, we should have walked away. The closing process was a nightmare because the seller hadn’t paid the electric bill, so we should have known that them wanting a free pass on inspection items was a red flag.

Virginia has a clause to protect the seller’s ability to walk away from the contract in the event of drastic home inspection repair costs.

Wood Destroying Insects (WDI)

A WDI is basically your termite inspection (may include carpenter bees, ants, etc.). We learned with our very first home purchase that this inspection is pretty useless. You can teach yourself what outward signs to look for regarding termite damage. It’s a visual inspection of what the technician can see. But the damage caused by WDIs is behind the drywall. If there’s signs of WDIs outside the studs of the walls, you’ll see it, and that means you have a big problem. Pay the $35 for a professional to say there are signs of active termites.

Another way we found that the WDI is useless is that we had a major termite problem in our house. We were paying for treatment when we sold the house. The treatments weren’t working and the next step was pulling up all the flooring in the basement and treating under the foundation ($$$). The termite company wrote their report: There is an active infestation of termites that are actively being treated. Technically, true. Productively, not the whole picture.

‘ADVANCED’ CONTRACT OPTIONS

I don’t know that these are necessarily advanced, but they’re less common options when making an offer. Some of them come in handy at opportune times, so it’s helpful to know the options at your disposal.

Seller Subsidy

The seller subsidy is the seller’s contribution to closing costs. It reduces the seller’s bottom line based on the offer amount, and it reduces the amount of money the buyer needs to bring to the settlement table. If a contract offer is $102,000 purchase price with $2,000 seller subsidy, then the seller’s bottom line is $100,000.

There is a limit of how much seller subsidy can be in a contract, which is based on the lender’s requirements and is typically 2% of the purchase price. We have had to adjust the contract to account for this limit before we were aware of it; we kept the seller’s bottom line the same, but adjusted the numbers so that we could maximize the seller subsidy.

In Virginia contracts, there’s a boiler plate section identifying the possibility of seller subsidy. In Kentucky, it has to be written into the additional terms section.

Escalation Clause

If you’re in a multiple offer scenario, it may be helpful to offer with an escalation clause. This is an option that a prospective buyer may include to raise their offer on a home should the seller receive a higher competing offer. The buyer will include a cap for how high the offer may go. It’s essentially a way for the buyer to compete with other offers, but not necessarily pay top dollar for the house.

Most recently, our offer was $420,000 and we were told there were at least 4 other offers. We added an escalation clause to our offer. We decided to make it a strange number (e.g., increase by $1770 at a time), and we capped it around $450,000. We were basically saying that we were willing to pay up to $450,000 for the house, but we didn’t have to commit to that number by making our offer at $450,000. The highest offer outside of our offer was about $436k, so our escalation of $1770 over highest offer got us the house for about $438k.

AppraisalGap Clause

As mentioned, a home purchase with financing is going to be subject to an appraisal. With the housing market exploding purchase prices in the last couple of years, houses have been selling for well over list price. This is nice in theory, but that doesn’t mean that a bank is going to agree that your purchase price is “fair market value.” If your contract is for $500,000, but the home values in the area only support $420,000, the bank is not going to give you a loan based on $500,000. Either the seller has to agree to accept the lower purchase price, end the contract and start over with the listing, or the buyer has to agree to pay the difference in value in cash. A gap clause is preemptive attempt to address this difference between the contract price and the potentially lower appraisal price.

If the buyer believes that the area’s home prices will support a purchase price of about $450,000, but they want to make an offer of $500,000, the buyer may include a gap clause of $50,000. This means that the buyer is more attractive to the seller because the seller’s risk of the contract falling through after the appraisal comes back is minimized. This also means that a buyer would have to be able to show the lender that they have the cash to cover the gap clause needed (if needed), the down payment, and the closing costs.

We used a gap clause on our most recent purchase. The list price was $415,000. I was confident that an appraisal would cover up to $425k, but I didn’t see many comparable sales higher than that without venturing into different neighborhoods. We offered, with an escalation clause, up to about $450,000. Since we weren’t sure that the appraisal would go that high, we offered a gap clause of $25,000. Our final purchase price was $438k, and the lender waived an appraisal need, so our gap clause wasn’t enacted.

RANDOM CLAUSES

I mentioned that a contract can almost say whatever you want. Here are a couple of examples of protections we put in an offer that had to be satisfied within the term given or we could walk away from the deal with no penalty.

SELLER THOUGHT PROCESS

The seller’s comfort comes into play when you’re in a multiple offer scenario. A buyer can make an offer saying almost anything they want (within reason of a residential real estate transaction). You can manipulate your offer to show the seller how vested you are in the purchase. Sometimes a seller just cares about the bottom line numbers, but sometimes (like if you’re competing with a similar offer), a few tweaks to your offer may make you more desirable.

I mentioned that we went higher than 1% on our EMD for our personal residence purchase. We wanted to show that we were very interested in the property, so one way to do that is to show that we have a lot of “skin in the game.” If we default on this contract, we’re out $5,000 and getting nothing. Whereas, when we’re purchasing a rental property without emotion, if it doesn’t go through, it doesn’t go. Sticking to about 1% is showing that we’re “checking the box,” but not that we’ll do anything and everything to make sure this deal goes through. We would still be out some money and get nothing if we walked from a contract without enacting a contingency, so the higher EMD you include, the more serious you appear.

A seller may not understand the big picture of providing the subsidy, so that could be risky. If a seller sees that they’re contributing to $2,000 of your closing costs, they may balk at it. Hopefully, they have a realtor on their end that can explain “think of your offer as $100,000 instead of $102,000.”

Eliminating a home inspection may make a seller feel more comfortable too. They may know of some issues in the house and are waiting for the “shoe to drop” through the inspection process, so it could eliminate a stressor for them. I wouldn’t recommend eliminating a home inspection unless you’re confident there aren’t any fatal flaws in the house (e.g., quarter width cracks in the foundation, wet marks on the ceiling, warped/sunken flooring).

The housing market has slowed down, so some of the out-of-the-norm clauses may no longer be worth the buyer’s risk just to compete for a house, but these are some options out there. The general concepts still apply, like when to pay for extra inspections or to expect financing and an appraisal to go together. Know that everything is a negotiation and don’t feel stuck in a contract if red flags are flying.

We have been surprisingly busy around here. I’ve been juggling a few rental issues, staying on top of some billing issues, and trying to make it through a commercial loan process.

At one point, most of our loans were held by one company. That was a more simple life. Even though we’re down to 6 mortgages under our name, it’s through 5 different companies. I’m really struggling keeping up with them and getting in a groove after our most recent refinance. I’ve mis-paid things 3 times now. I’m always on top of our payments, but something just isn’t clicking right now for me. I just paid one of our mortgages due April 1 instead of changing the date to be an April pay date. At the moment, we have a buffer in our account because we’re getting to this closing next week, but we usually don’t, so hopefully I have this figured out now that I’ve made so many mistakes.

RENTAL PROPERTIES

LEASE RENEWALS

We had 3 properties process their renewals this past month. Each of them had cost increases to their lease renewal (875 to 950 effective 5/1, 850 to 900 effective 8/1, and 1025 to 1100 effective 5/1). We have another property that will have a renewal offer go out this week. Then we have 3 that will need action by the end of April because the leases expire 6/30, and one that will need action by the end of May because it expires 7/31.

MAINTENANCE

We had a tenant reach out to us that they found bugs in their bathroom tub. She sent pictures and, sure enough, they were termite swarmers. I have way too much experience with termites. I called our pest company, and they sent someone out for an inspection to confirm they were termites. Then I got a call that because we didn’t pay the annual fee to keep our warranty current for the last 3 years (we had the house treated for termites in February 2019 when we bought it because there were active termites and extensive damage by the front door that needed repaired), they could charge us $650 again. However, since we’re considered a business account, she’d be happy to let us back pay the termite warranty and they’re treat it. So I paid $294 for the treatment instead (split with a partner on this house). She also informed me that they had cut off the hot water to the kitchen sink because there was a leak. I don’t know why tenants don’t tell us these things right away! I had my plumber out there the same day, and he replaced the whole faucet. That was $378. That’s one of those charges that’s frustrating because we could have replaced the faucet on our own, but we don’t live there anymore. Oh well; it’s also a cost split with our partner, so that helps.

We had another tenant reach out saying that her kitchen sink drained slowly. She’s been with us since we bought the house and never asks for anything. She’s on top of communication and was super appreciative each time we agreed to renew her lease. We had done a huge sewer line replacement project at this house, so I was skeptical of the issue. It turns out there was a plastic fork lodged down there, but I just let it go (meaning, she’s then technically responsible for the cost). Our property manager let her know that if it happens again, she’s financially responsible, but we’ll cover the cost ($200) this time.

RENT COLLECTION

We FINALLY got the check for one of our tenants that had an approved rent relief application. They submitted an application in November to cover December, January, and February rent. By mid-December, they ended up paying December rent because they hadn’t heard (and the application expires, meaning their protection from eviction expires (not that I would have pursued eviction for this group because they’ve been great tenants for several years)). They received approval for 3 months worth of rent and 2 late fees on January 11. We received the check on March 4th. So frustrating in that process, but still better than an October approval and us getting those 3 months paid at the end of January.

We had our usual suspects not pay rent. On the one house, they didn’t tell us they weren’t paying rent for the longest time. Now, they tell us they’ll pay us on a later date. I let it go this month, but with them paying on the 23rd, that means we’re in a perpetual cycle of not getting rent on the 1st. We have a partner on this house, so I plan to address it next month if they claim another 3+ week delay in getting us the rent. On the other house, she let us know in February that she’d struggle to pay rent and she gave us random amounts throughout the month. I let her know she was still $106 short from February and that she was now in default of March’s rent, and I got no response. Then Mr. ODA had $1000 show up in his account on Friday. She still owes $371 between the two months, but at least we have the mortgage payments covered. She’s also the tenant that we plan on not renewing her lease because she’s caused issues throughout her tenure.

BUYING A NEW PROPERTY

We’re still in the process of getting through closing on a new rental property. We’re expecting to close not he 24th, so we’ll see how that goes. It’s a commercial loan, and it operates different from residential mortgage underwriting, so we’re in the dark. Communication has been next-to-nothing. We’re currently waiting on the appraisal to come back. That was our one hurdle to getting into the house. I said once the appraisal clears, then we (as the buyer) shouldn’t have any risk in getting to closing. Therefore, we were hoping to have the house painted before we close (I would do the painting), then we could refinish the floor and get the rest of the cleaning done the weekend after closing, and get it listed for rent for April 1. I suppose I wouldn’t be trying to get to the house before Friday, so I guess I can be patient and wait to see what happens with the appraisal for a few more days (even though the appraiser was on site last Tuesday, and I’ve never had it take more than a day or two to get the paperwork).

REFINANCE FOLLOW UP, STILL

We still have an issue with the mortgage that I ended up paying 3 times for the 2/1 due date. Our refinance was difficult, and the communication continued to be difficult after closing. I asked on 2/1 whether our loans had been sold yet because I was surprised I hadn’t heard. Usually, I see a note saying to pay the new company before the first payment, thereby not paying the first payment to that “first payment notice” place that comes with the closing documents. The company’s contact said to keep paying them because they hadn’t sold the loans yet. I didn’t open the attachments in his email because I assumed he was reiterating what he said in the email. Turns out, one of the loans was already sold, and I should have paid the new company. Well, I processed a paper check to go to a completely different company (started with a C, and I didn’t catch that I selected the wrong one in bill pay). Luckily, that company sent us our check back, saying they think our loan is closed with them and they can’t process the payment (thank goodness we once had a loan with the address I put in the memo line so they could clearly make a connection and say “we don’t want this!”). When I noticed my mistake on the 14th, I sent a handwritten check that I rushed to the post office at 4:55 to get post marked. In the meantime, I found out that I was able to set up an online account with the new company even though I didn’t have the loan number yet (they gave it to me over the phone). I paid the new company online to make sure I didn’t have anything on my record claiming I didn’t pay by the 15th and it was late. I figured I’d rather manage 3 payments being made than fight the credit companies to change my credit report. Well, the initial company cashed my handwritten check, but they still haven’t sent the money to the new mortgage company. They just kept telling me they have 60 days to get it to them, and I said that’s unacceptable that they’re holding my money. That was a week ago that I was told I’d get a call back, and I haven’t heard from them.

PERSONAL EXPENSES

Now that the basement is done, I had a strong urge to finish projects. There were several things that were starting but not completed. Those final punch list items always seem to take forever. I was impressed that Mr. ODA pushed to get some of the things in the basement done right away, even though they weren’t on a critical path. However, I didn’t uphold my end of the project by painting those things, so I got back to that. I mentioned several of the projects in a recent post, and I’ve done a whole lot more since that post. But all that to say, I’ve spent a lot of money in the last month. I bought a lot of supplies to finish off these open projects. I also had big purchases of cabinet hardware, a dining room table, a desk, and a wood. We haven’t done very much out of the house, so we don’t have a lot of other expenses than these projects, which means our credit cards are actually have the usual balances. We did book an AirBnB for a trip at the end of the summer with friends of ours. That was a big hit on the credit card for a week at the beach, but they reimbursed us for their half.

SUMMARY

It feels like I just keep lowering the balance in our investment accounts each month, but I went to look at February 2021 to see the total. Even though some balances have decreased, we’ve still contributed to the accounts, so overall they’re $21k higher than last year, which is encouraging. I guess I should also focus on the property values raising significantly. We’re over $500k higher than last year in our assets, and our liabilities (i.e., mortgages) are about 13k less than February 2021. We’re also still over $3M on net worth, even if we’re hovering right around that. We’ll add about $50k to our net worth by the end of the month, as long as we close on the new property on time.

Our 11th purchase was a 4 bedroom and 2 bathroom house, which we were excited about. We only had one other 4 bedroom, and it only had 1.5 baths, so this was a new demographic we could meet. We again needed a mortgage, but we were tapped out (max of 10 mortgages allowed per Fannie Mae), so we went to our partner. I went through the process of establishing the partnership in the House 10 post.

The house had been listed for sale in July 2018, dropped the price in October 2018, and we went under contract on it on December 1, 2018. We went under contract at $129,000, which meant, according to the 1% Rule, we would look to rent it for at least $1290.

The house required a lot of cosmetic work (relative to our usual purchases) before we could rent it. The biggest hold up was the carpet replacement, but we had to do a lot of cleaning and painting also. We closed on February 4, 2019; got to work on the house on the 6th; and then had it rented on March 3, 2019. That’s a longer turnaround time than we’d like, but we thought the long-term benefits of a 4/2 house would be worth it. Plus, with our goal being $1290 based on the 1% Rule, we were happy that we rented it at $1300 and through March 31, 2020.

LOAN TERMS

We were given two options from the loan officer. Both options required 25% down. We could do a 15 year mortgage at 5.05% or a 30 year mortgage at 5.375%. The 15 year mortgage payment was $865, while the 30 year was $640. Since both options required 25% down and we aren’t concerned with our monthly cash flow (as in, we’re not living off of every dollar that comes out of these houses right now), we chose the 15 year. Escrow changes over the last few years have increased the mortgage to $941, unfortunately. However, we’ve been paying off this loan with pretty substantial chunks of money thrown at it. The loan started at $96,750, and the current balance is $21,350. We would have liked to have this paid off a few months ago, but we need to time our payments with our partner, who recently paid for a wedding, renovations to a new house, and a new tear-down property adjacent to his personal residence that he’s going to build a garage-type thing (city living = street parking for him).

We went under contract at $129,000, and the house appraised at $140,000, so that was a nice surprise. The current city assessment is at $148k, but it would likely sell for more than that.

PARTNERSHIP

Since the LLC was already under way when we purchased House 10, we needed to add this one to the LLC. We contacted our attorney. He processed all the paperwork, and we showed up just to sign everything in a quick meeting. At this time, we also requested an EIN be established for the LLC. To process adding this to an established LLC, it cost us $168 (which we paid half of since we’re split 50/50 with our partner).

PREPARING TO RENT

This house was probably the second most effort we had to put in to prepare it for renting. We had to replace quite a few blinds that were broken, do a deep clean of everything, install smoke alarms, paint, replace the carpet, and do some subfloor work.

We had to paint nearly every room (one room we even painted the ceiling the same color as the walls because the ceiling was in rough shape, and it wasn’t worth the time for precision of the edges).

The floor at the front door was rotted by termites. The guys had to cut out the floor and replace the wood before the new carpet could be ordered. We needed the house treated for termites at that point since there was an active infestation that we found. Depending on time and price, I’d rather replace carpeted areas with hard surface flooring for easier maintenance. Since we were already losing time with all the maintenance on this house to get it ready to rent and it was a small area, we just went the easy way out and put new carpet in. The carpet was only in the living room and hallway; all the bedrooms have hardwood flooring.

FIRST TENANTS

We were able to get a family in the house fairly quickly after we finished our work. We rented it at $1300. They signed it on March 3rd, and I had set the terms until March 31, 2020 (this comes into play later). The family had been renting with a roommate (and the husband’s boss!), and that guy had wanted to leave the house. In January 2020, the tenant said, “we signed the lease on March 3rd, so we want to be out at the end of February.” That’s not how leases work. The lease signed said until March 31, 2020. Some time between us telling him that he was in our lease until the end of March, not February, and the end of February actually coming, they decided they wanted to renew their lease. They signed a new lease with us on March 11 to cover 4/1/2020 through 3/31/2021.

In April 2020, the tenant received a job offer in Texas. He asked about a lease break, and we offered an option. All the communication was done via text message, so it was technically in writing, but there was never a “wrap up” text that identified all the agreed upon terms to allow for the lease break. I used this as a teaching opportunity for the 3 of us in the LLC that clearly documenting agreements in writing (preferably with signatures) is important.

The tenant offered to pay May rent without prompting, so we thought that was covered. The part that needed to be detailed was what was considered a “lease break” fee. We had agreed to 60 days worth of rent, and the security deposit couldn’t be used to pay that. Mr. ODA tried to contact the husband on multiple occasions to get rent paid at the beginning of May, but there was no response. I finally sent an email, detailing that they agreed to pay May’s rent, and that technically, they were on the hook for the entire year’s worth of the lease (quick aside: while that’s what the lease says, I think a caveat in the law actually means they’re not really liable for the whole amount because once the house is vacant for 7 days, it defaults back to our ownership, and then we have to show due diligence to re-rent it, leaving them liable for only the gap period). Well, as usual, the landlord gives us a guilt trip (their daughter was in the hospital in TX) instead of separating that from the concept of “pay your debts owed.” As a person, I feel for you on this; as a business owner, it’s not my responsibility to manage your finances and personal life.

The tenant called Mr. ODA and yelled at him. A few hours later, presumably with a more clear head, we received a fair response via text. He even apologized for yelling on the phone. He paid the last few hundreds that were owed, and we all moved on.

SECOND TENANTS

After our first tenants vacated the house, we had to get the house turned over. There was a good bit of work that needed to be done for just a year of someone living there. They had also left stuff behind that became our responsibility to get out of the house. We listed the house for rent. Our partner showed it to 3 younger people who would rent it together. They seemed great until we ran their background and credit check. They had evictions they didn’t disclose (claimed they didn’t know), so we shared the report with them and continued showing it.

We ended up showing it to a couple, and they liked it. After we accepted their application, we were able to get the lease signed on May 7, 2020. Since this was at the very beginning of the pandemic, we had to get creative. I signed this lease on a street corner (hadn’t realized that the place I had selected with outdoor seating was closed!), and they paid their first month’s rent, security deposit, and pet fee in cash that he handed to me in a sock (with a warning that told me this wasn’t the first time he handed someone cash like this haha). They’ve been great tenants, and they renewed their lease.

MAINTENANCE

The new carpeting when we first bought the house cost us $700. Between the termite treatments and other general pest control, we’ve spent $950.

Once the first tenant moved in, we learned of some other issues that weren’t apparent by us just working there and not living there. We had the plumber come out to fix several issues with the hot water that cost us $1450! Then we found out that the master bathroom shower wasn’t installed properly, and it was missing a p-trap; that cost us $325.

Our insurance carrier didn’t like that there wasn’t a handrail for the front steps of the property, so in March 2020, we had to have one installed at $190.

We had to replace the washing machine in April 2020 for about $500. As I’ve shared, we try to not include any ‘extra’ appliances because then maintenance and replacement are our responsibility. This was a fun one – we replaced it just to make the tenants happy and not deal with maintaining it, and then those tenants left right after that, and our new tenants brought their own appliances (so they just have two washers and two dryers in their kitchen).

We had an electrical issue with the master bathroom that cost us $150.

Luckily, I did the inspection over the summer, and nothing came of that initially. We did end up replacing a fan in the master bedroom because the light part of it stopped working with the switch. Since we don’t live near the house anymore, and our partner was in the middle of getting married, we went through Home Depot to have it installed, so all together (fan/light and install) it was about $175.

SUMMARY

This has been a good house. We didn’t realize that the house is located outside the city limits, so we needed to figure out trash pick up in the county (not included in the taxes). Other than a few maintenance hiccups, things have been smooth sailing. We’re happy with the tenants who are there, that they’re maintaining and cleaning the house, and we’re getting our desired rent amount (that they pay on time every month). The street is in a decently nice neighborhood with a lot of original owners, which helps it keep (and increase) its value.