I had this post mostly written by Wednesday, but we traveled earlier this week, and I haven’t kept track of the day very well. This is the first I’ve been able to update our net worth and get this done. Ironic, considering how I started this post when I expected it to be on time. And now..

This past month has been exhausting on me. I knew March was going to be busy. We had a bunch of sports schedules to manage, lots of kids birthday parties, hosting my dad for a long weekend that coincided with 3 family birthdays and the first anniversary of my mom’s passing, an assortment of Easter activities, a trip, and random other events. On top of managing these day-to-day things for our family, our deck replacement started, and we had to work on a massive turnover of a rental property. I’m in a perpetual state of tired these last few weeks.

DECK REPLACEMENT

On July 2nd of last year, a storm blew threw that destroyed our neighborhood. Honestly, we’re surprised by how little actual structure damage there was for our neighborhood because it looked like a war zone with the amount of trees down. A couple of houses had a tree fall on their roof, but only cause minimal damage that resulted in shingle replacement. We appeared to bear the brunt of the worst, which was a tree falling on our deck, crushing our furniture, moving all the supports, and cracking the concrete blow it. Another tree missed falling on one of our cars by centimeters, but that limb ended up cracking our driveway apron. We struggled communicating the extent of the damage with our insurance company, and they eventually realized what was needed and paid out on it five months after the incident. Our construction started on March 18th.

It hasn’t been an easy process. It’s emotionally draining on me because there were communication issues with our contractor that he wasn’t taking responsibility for. Then there were minor issues, but issues nonetheless. For instance, they installed waterproofing so the patio would be a dry area, but they cut through one of the barriers. Instead of realizing that was going to be an issue and fixing it themselves, I had to point it out. Then we went out there while it was raining to check it, only to see that there are 3 spots where water is just pouring through the seams. That just takes a lot out of me to have that conversation. They cracked off the top of our sewer cleanout, which not only made a mess in the yard, also caused a backup into our basement tub and toilet once it was glued back on because of a pressurizing issue (we think).

Then there are those hidden things that take energy, such as managing how to move money out of savings (while not exceeding the maximum of six transfers) and keeping track of all the bills, while ensuring the checking account has the right amount of money to cover the bills paid.

RENTAL PROPERTIES

Everyone paid rent on time! I had two technically pay on the 6th, but I sat waiting to see if it showed up before reaching out that morning. One of our tenants bought a house and vacated as of March 31st. They actually had left the house a little early, which was really helpful to us because the house needed a lot of work. The house had been flipped before we bought it. We knew everything was going to eventually need attention, but we hung on as long as possible. The neighborhood is really nice, so it was time to bring the state of the house up to a better standard. It had been “good enough” all these years, but there were definitely some items that should be replaced. This ended up being a huge overhaul, costing us over $10k. I’ll go into all the details in a future post.

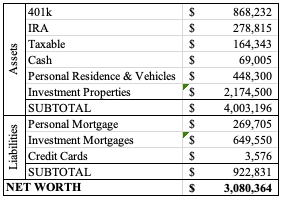

NET WORTH

We’ve made a few substantial payments on the deck. We had been investing the money from the insurance company, while we waited for them to finish their estimates and then while waiting for the contractor to begin. Our taxable investment accounts have decreased a bit from that, and they’ll continue to decrease as this project finishes up in the next 2-3 weeks. The market is lower than it was a month ago, but our house values are starting their upward Spring trend, offsetting some of that loss. Overall, our net worth increased over the last month, but only by about $4,500 instead of the drastic increases we had been seeing month-to-month.