We have been busy! The kids ended school the first few days of June, we’ve taken two trips, and one kid is has done a camp so far. The rest of May had finished up graduation and baseball things. I’ve taken a step back from work a bit. I’m not on a schedule going into work now that the kids are out of school, but I’m helping train the new girl. I eventually will get the chance to step out of the day to day, and then we go into a mode where I do more behind-the-scenes work.

PERSONAL

I started working less. At least that’s the goal. I had been working part time, and for a long while, there was another guy there to fill in my absences. He left a few months back, and it was becoming too much to manage. Even if I logged 20 hours per week, there was the weight of feeling I had to check in on things and needing to be responsive. Then there were all the random texts or calls that would take my attention, even if they were much less than they ever were. The office was in the process of hiring a full time position person for that role, but I wanted out. I wanted to enjoy my summer with my kids and not have the pull to be there. I tried to quit twice. They pushed forward the position that we had been discussing for a year and made it official, while calling in a promotion with no added pay (I guess the increased flexibility will be the benefit). The new person started on the 15th. She has been really great, but I’ve still put in more hours than I wish. The good thing is that I stepped foot in the office for the first time this week for a couple of hours yesterday. My general goal is to get to like 15 hours per week, and my tasks will be organizing financial data and not agent-facing anymore.

I’ve been working on getting my things in order as a notary. At work, we have our own title company, and there have been several issues with the closings. Their work load is down, and I wouldn’t be surprised if it’s because our own agent investors are tired of the problems and letting their clients go elsewhere. It’s quite frustrating to see. Well, I’m a fixer and helper. I wanted to get my notary so I could manage these relationships better. I got the main paperwork in order, but now I need to do the classes to be a title closer and get myself registered online so I can be selected for business. It wasn’t that expensive. I’m all in for about $120 once I buy a stamp (more if there’s a fee for the classes). Supposedly one closing could bring in that amount, so we’ll see.

Mr. ODA is working still, and it’s going better than it was. It’s become less of a hurdle to figuring out the schedule and conflicts with baseball season and end-of-year school activities out of the way. Now the hurdles are the swaths of days off for our trips.

We’ve taken two trips so far this month. We have another one next month. We’ve also gone to Kentucky Kingdom on our season pass for a day, with a few more planned for the summer. Our trip there was awesome. The kids had such a great time and everyone was in a good mood all day. We did the regular rides and were there for about double the hours I had expected because it was going so well. Our next trip will explore the water park, and I think it’ll be a perfect day for that next week in the 90s (our last trip was 73, so we intentionally didn’t plan to get in the water).

We have one camp week of the summer done for one of the kids. Two big kids go to an outdoor camp soon, and then there’s a half day camp for the oldest later this summer. This week’s camp has been across town. I was looking forward to getting things done with 2 kids in tow instead of 3, but I haven’t been able to prioritize playing with them and running errands like I had hoped, which you’ll see why in the next section.

RENTALS

Well, this post is late, so technically the blog world shouldn’t know about the week we’ve been through yet, but let’s lay it out. I actually had quite a few people pay rent late this month, but everyone communicated their issues and timing, so it worked out fine. Two people paid a late fee because they didn’t tell me the right information or told me late (and they’re repeat offenders on poor communication). If you communicate with me and give me the right information and uphold your commitment, I won’t charge you a late fee. That’s not income I’m expecting, so it does more to a tenant’s life to not have that money going out than it does to my life to have the money coming in. However, if you can’t tell me the truth or communicate clearly, I need to protect myself. I don’t want to set a precedent that you can walk all over me or pay whenever you feel like it because I still have my bills to pay for that house to stay standing. Anyway, with that rant out of the way, one house has not paid rent still.

We have a tenant who fell on hard times in February. She intends to pay June rent on July 3rd. She has been consistently later and later in paying her rent. While we work with our tenants regularly, they have to do their part and show their effort to prioritize us. It will never cease to amaze me how many people do not prioritize the roof over their head. Her financials were questionable when she applied, but she technically qualified for our list. The fact that there have been no partial payments and she continuously tells us a date she’ll pay, but she doesn’t pay then, has made me lose patience. She said she prayed on it, and she wants to stay in our place for another year. We said we needed to see rent paid, and if she could make a partial payment on the 12th, then we’d consider an extension. No payment. And then when I finally got Mr. ODA to take the hard stance in their communication, she tried to guilt us that she did tell us she’s working on it, and he had to explain that she in fact did not follow through on what she’s been saying. She was supposed to vacate June 30, but now that this has dragged on, she’s vacating July 31, which makes me mad. I had purposely put her as June 30 so that I wouldn’t be looking at an August rental period with back to school for a house that is notoriously hard to get rented because of all the stairs, and now here I am again. Oh well, I have no control over that anymore and just need to get through it.

Last weekend we received inches of rain. One of our KY houses has a history of water intrusion at the back door. We can’t figure it out, but the lack of lip/sill/curb because the door was installed at concrete level is really the issue. We probably need to install a curb and get a smaller door in there now that I think of it. Well, the tenants have been really patient with the water intrusion and they just lay towels when it happens. Last weekend, it was way worse. They had water in two spots they never do, and a lot more water than usual by the back door. It happened on Monday, and on Thursday, I could still get water to come through the floor boards. I started pulling the LVP out. As soon as I got everything exposed, it dried really quickly. The problem was that the washer was blocking my ability to get anymore boards out. I tried to get a board out of the middle that I could just reinstall with wood glue down the road, but my utility knife was useless. The board was eating more out of my blade than the blade was doing damage to the board connection. I regrouped. I went to Lowe’s and got a new tool and a different kind of blade for the utility knife. We’re heading over there today to get some more flooring out of the way. While this sounds awful – for me to pull out the floor at the back door, where there’s been consistent water intrusion, and not see any mold, was absolutely the best thing on my day yesterday. There was mold behind the baseboard in the drywall at the back door, which wasn’t surprising in the least. I threw that away and will be able to install new stuff. We’ll likely go with the plastic version of that so that it keeps the water away better because this isn’t a problem that’s going away any time soon. There’s a flood advisory for the next couple of days, so it’ll be good that the floor is out of the way for a bit.

So while Mr. ODA and I are grappling with next steps on this basement water issue, a tenant in VA texts me. I love my tenants that apologize profusely for telling me something is wrong. I promise, it’s OK to report that there’s an issue to me! This is the house that had MAJOR termite damage (look, another storm we’ve weathered!). She reported that a burner on the stove won’t turn on anymore and that the toilet in the bathroom is taking a long time to fill up. I texted my handyman buddy and he said he could get out there. That’s off my plate now. I’ll just pay an invoice when it comes in.

And finally (dare I say, this is the last issue of the month??), a house in KY also apologized profusely, telling me the AC is out. I checked my maintenance log, and while I’ve managed issues at this house for the AC, it hasn’t been replaced. Knowing the house, this HVAC guy this morning is going to tell me to replace the whole thing. HVAC is one of those things that I can’t do a single thing to trouble shoot it, so I just contact “my guy” and he’ll tell me what’s next. This is definitely a “throw money at the problem” situation, but it doesn’t take any of my time, and that’s the priority to me these days.

SUMMARY

Over the years, I’ve learned to just get through things. I’ve learned that even the biggest seeming problems subside. A tenant trashes a house; we get junk luggers out there and replace everything. Our wallet hurts for a bit, but then you move on. A house floods; insurance kicks in, and we basically did nothing except send a few emails. When I started my job, there was a bison on the front cover of my welcome binder. They were pointing to the fact that bison will walk into a storm because the fastest way through a storm is through it, not trying to outrun it. This thought consumed me. I had heard it before, but it didn’t stick like it did then. So while there may be juggling for a little while, it’s not the end of the world.

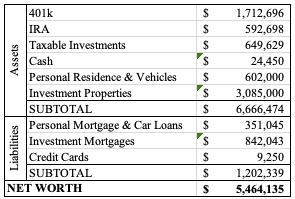

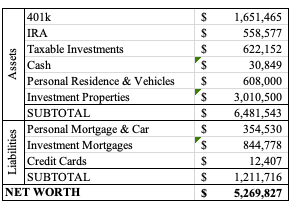

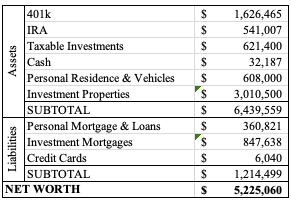

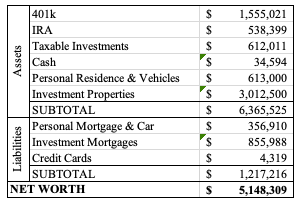

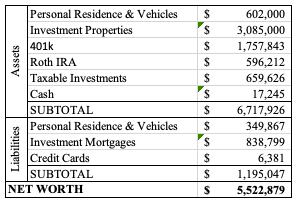

NET WORTH

Because of the things I’m juggling these days and trying to prioritize time with my kids, I don’t have a break down of our spending since the last update. Mr. ODA also asked me to split out our Roth IRA accounts from the investment line item because we’re going to be doing Roth conversions. Maybe I’ll do a post about what that is, and that’ll help me finally know what that even means to us. I’m a very visual person, so once I start seeing the implications of that, I’ll understand it better. He’s been managing that and how it affects our money/income/taxes all along.

Our credit cards are $3k less than last month, and the majority of the balance is because of the windows we replaced in our personal residence. We paid the deposit back in January or February. They came and replaced the windows in March, but there were two broken frames and several sashes with imperfections. They came a couple of weeks ago with the replacements, only for one sash to have broken glass. I had also found the same etching on the inside of the glass in the mean time, so they have two sashes to bring me. For some reason, they haven’t come looking for the balance owed while they’re still not installing complete windows, which I appreciate, but also would have understood if they wanted their payment. At some point in the near future, about $5k will be added to the credit card balance for that. It’s on a 0% interest credit card so that we can manage our cashflow and not have to pay that off until the promotional rate expires (this is a regular thing we do, and I have posts about it). It would seem there’s a high probability our next promotional rate credit card we open is for braces because we’re at that age now – eek.

This past month, I paid multiple insurance premiums for rental properties and our car insurance (which is paid twice a year). In May I had paid just under $2k for taxes on rental properties. But overall, our net worth is higher than last month.

Now I’m off to make a lunch for my camp kid, get her across town to camp, tear up some more tenant basement flooring, play some pickleball, and maybe lay on the couch for a quick minute before I go across town for her camp pick up and a 90 minute gymnastics sessions.