After not wanting to know the details of March’s expenses because Mr. ODA threw me a surprise party, I was pleasantly surprised to see our spending in April. Now, with that said, while my categorization of expenses cover April 1-30, my stories here go through this date in May. And May has been a doozy.

We changed our insurance carrier as of May 1. We put a concerted effort into getting some routine things out of the way before our insurance changed because we weren’t too confident in the new policy’s coverage. Mr. ODA got a physical. I got an eye exam, which is more expense ($116) due to the contact fitting, and became more expensive when we moved on to acknowledging the astigmatism that we’ve ignored for the last 5 years because it’s so slight. Then that leads to buying contacts ($300). I do need to submit the reimbursement request for the contacts that I paid out of pocket for, so at least some of that should come back.

In mid-April, I started having chest pain. That lead to us wiping out the deductible. Such unfortunate timing. We could have walked away from that policy only needing a couple of hundred applied to the deductible, and then I didn’t take care of myself while sick, so the virus attacked the wall of my heart. Lovely. My first office appointment was at a new clinic, and they said if I paid in full, they’d apply a 10% discount. I’ve had to learn to navigate the world of medical billing (even more in depth than I already had due to poorly executed claims) because of the deductible concept. So the lady’s statement was correct – I still owed about $3000 on my deductible. That’s what she billed me. That’s a normal statement for me to hear. What I hadn’t thought about was – but who will get there first? If her claim wasn’t first in line, then my deductible payment wouldn’t go to her. Narrator: she was not first in line. So now I’ve paid $3k to this company, but I only actually owe her about $900. Meanwhile, the one who was first in line now wants their payment, understandably. I’m trying to hold off on that until after the 20th so that it’s on the next credit card cycle. And through all of this, I also need to fix my log in to my old insurance account to be able to verify that they’ve even accounted for my deductible correctly because I swear I’ve overpaid my deductible the last two years due to too many claims happening at one time, but it’s convoluted and I’ve just given up tracking it both years (I know, this is against everything I tell you to do, but shew, it’s been quite the year or so around here).

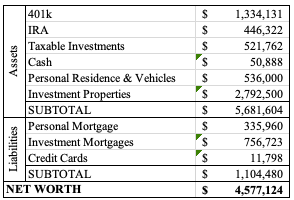

On top of that, Mr. ODA works at Lowe’s, and they have a spring holiday period where employees get a 20% discount. So now there’s a ton of Lowe’s transactions on our credit card that’s inflating our spending. While the details of that will be in next month’s update, it is reflected in the net worth calculation I have here since these are current numbers.

RENTALS

We got one house rented as of May 1. That was an anticipated project, and the tenant who left had lived there for 6.5 years. We were gone the first week of April, so we ended up losing the month of income, but the actual work to turn it over took very few hours (at least compared to most of the turnover we do). There’s one more house outstanding to know if she’s renewing, and there’s one house that will turn over at the end of June. That woman moved in over the winter on a 6 month lease. She’s been extremely difficult, and I’m not sad to see her go. For instance, it’s the 22nd, and she still hasn’t paid May’s rent. The good news is that the turnover should go quickly since we did a massive effort to spruce it up at the last turnover.

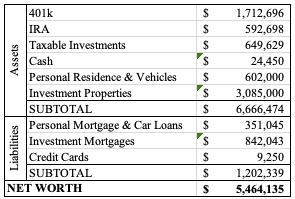

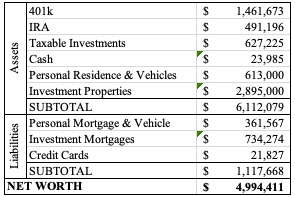

NET WORTH

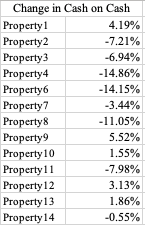

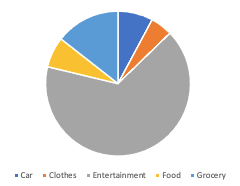

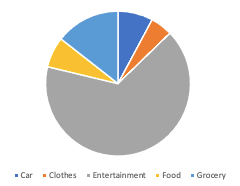

The market has recovered a bit, so we’re trending up again instead of stagnant on the net worth. I categorized our spending for April, but since we took a trip, the ‘entertainment’ category is taking over the graph.

I took out the expenses related to our trip to see what was left. Entertainment is still high because we spent $785 on season passes for skiing next year. This also include our daughter’s gymnastics and our gym membership. Just funny that the graph didn’t change because our proportion of spending was the same.

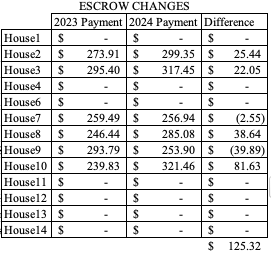

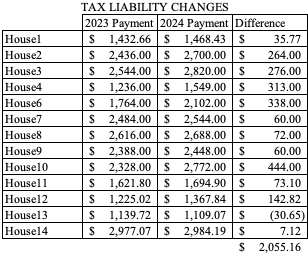

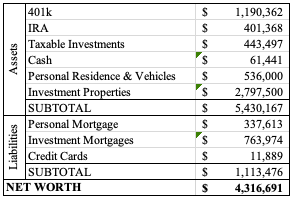

Over the past few months, I’ve worked on increasing our monthly cash flow a bit with rent increases. This isn’t a money-maker, but just trying to stay on top of the routine cost increases (e.g., taxes, insurance) that are coming our way. Once all the increases go into effect, it’ll be another $400 per month. But that’s also contingent on what we get the house that’s turning over rented at. That seems like a lot, but you’d be surprised at what our cost increases are. I usually do a post comparing all those changes in the Fall.

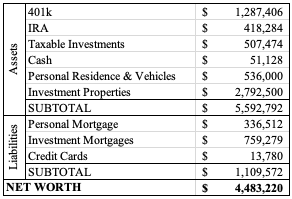

This month our cash went down too because I had to pay the health insurance costs and three houses worth of taxes. I updated our home values now that it’s the spring market; I update these numbers about twice per year.