There’s a lot of chatter online these days about a “90s summer.” I’ve also been fed some reels about what “rich” looks like, and it’s not about money or flashing the perception of money. Mr. ODA and I are working very few hours these days. My job is because I’m a “helper” in life, and I know this group needs my help for a bit longer (I also tried to quit and they said no). Mr. ODA’s job is to qualify for health insurance so we save about $1500 per month in direct expenses for health insurance.

When I first started working, my goal was to climb the ladder. I wanted to be the youngest CFO in my Federal agency. Then a 34 year old woman got the job and crushed my dreams a bit, but I was still a good amount younger than her, so I just needed her to move on in the next few years. Then I went to DC. I left the house between 5:30 am and 6 am, and I got home between 4:30 and 5:30. I kept looking around thinking, “when would I see my kids if I had them?” In fact, we were denied adopting a dog because we both had full time jobs. That still fascinates me. During my fight to climb the ladder in DC, I realized that wasn’t what I wanted. I wanted to live a few miles from work where I could have more free time. I wanted to own a little piece of the pie, so to speak (my job in DC was very high level, but I loved working with the State level where I could actually see the road and bridge projects I approved in progress). But even as I made that transition, it didn’t feel right. I wanted to be home with the kid I was about to spend $30k to have. I didn’t want to put all that money into making a baby for him to sit in daycare for a whole work day and commute time (I get it – it works for people, but not for me).

FIRE. Financial independence, retire early.

While our path didn’t go as we expected as we learned more, and we both worked longer than we intended, the goal was always the same – be home with our family while they’re little. And that’s what we have. Even when I took this new job, I said my kids come first. I didn’t sacrifice in all those ways before kids, give myself freedom, and then take on a full time job. Most people struggle to understand that. Even the agents who I’m paying $600k each year can’t understand when they hear I don’t “need” to work.

So that’s my rich. I’m at the kids’ school all the time. I’m at nearly every drop off and pick up. Heck, I discharged from the hospital AMA so that I could get to a baseball game in May. I will be there. I will be cheering them on. I will lay in bed at bed time, read them books, and then ask them about their day while they tell me the most obscure things…but it’s because they just want to fill that time where they get to talk to me without a sibling interrupting.

I’m not driving a fancy car. I’m not living in a 7000 sf house just because I can. We’re not going out for drinks and sitting at restaurants multiple times per week. We’re not going to the movies every month (umm, actually, or ever, unless it’s the $2 summer flicks series). I’m making my money work for me, so that I can focus on pouring into my kids and enjoying the time of their lives that they actually want to be around me all the time.

Disclaimer: I am not personally making my money do anything. That’s all Mr. ODA. I’m just the bookkeeper, collecting rent and tracking what’s happening and trusting he has the answers on how to move the money around.

In January, I shared why we chose to finance our new (used) car. To those who know us, they would think paying interest would be an immediate no, but there are reasons that it may work in our favor. We also have a mentality that the best decision is the one that makes our money work the hardest, not an overarching thought that debt is bad.

The dealership was offering $1000 off the purchase if we financed. Mr. ODA ran the numbers, and we decided that was worth paying the minimum 4 months of interest. I paid off the loan, so now we have the actual numbers.

Here’s what I had said back in January: The financing was 6.99% and we chose the option that allowed pay off after 4 payments. There was an origination fee of $175, which is rolled into the principle. Our payment is $151.94. The first 4 payments hold $175.07 worth of interest. So we will pay $175.07 of interest and the $175 origination fee as a means of taking $1,000 off the list price. That nets us, including the $30 of credit card rewards, $679.96 less on the list price. After the 4th payment is made in May, we’ll make a lump sum payment of about $7,134 to pay off the loan.

I did not read any prepayment penalty data, but Mr. ODA wasn’t so sure. We made a lump sum payment to bring the balance down to about $2500 in February. What I wasn’t prepared for was that the loan system decided that I didn’t owe any monthly payments for several years at that point. I decided to just go ahead and make my monthly payment a couple more times after that even though it was being applied as principle only and not a monthly payment.

We paid $175 origination fee and $112.49 in interest. So our net save on the final purchase was $712.51. I also included the fact that we made $30 by only financing the bare minimum and putting the rest on a credit card that got us 2% (there was no fee from the dealership to put this on the credit card, which was also a factor in the decision), bringing the net to $742.51 worth of the $1000 off the purchase price. This was better than projection because of the way their loan system applied our lump sum payment.

I’m working with Keller Williams, and in a lot of ways, I see the parallel with Amway, which I also have experience with. People love to have their negative opinions about these companies, but both companies are teaching money management in a productive way if you’re coachable and paying attention. They’re teaching you to think outside the box.

I recently listened to Dianna Kokozska’s Ted Talk “Why Wealth Creation is the Ultimate Act of Love.” It makes the point that putting the effort in to being financially successful provides security, freedom, and opportunities for not only you, but others close to you in the event of a need. A phrase stuck with me: wanting money isn’t greedy; wanting money is strategic.

She shared how her son’s wife’s health was in trouble, and they needed money for a treatment. Not that everyone should have the ability to write a check for $35,000 on a whim, but do you have the ability to manage a crisis? Are you learning from others around you who have been successful? Are you keeping an open mind and actually making the attempt to build wealth?

Choose to be around people who challenge you. Look at your closest 5 people; are they where you want to be in life, or could you find a sphere of influence that can challenge you and teach you how to make money?

VICTIM MENTALITY

She quickly touches on the victim mentality. I see this around me at work often. People who seem to always have a crisis to manage. It’s in your head, and you’re focused on the negative instead of creating a positive outlook to be more productive with your money. Are you stuck in a spiral of “why does this keep happening to me,” or are you finding a path forward? Sure, we hit rough patches and things go wrong. The path forward comes in your decision as to whether you’re going to let these issues define you or if you’re going to find a way to make things better.

I have a family in one of my rentals that has both parents working blue collar jobs. He works in a kitchen and she usually works reception type jobs. I’ve known them since 2016. At that time, she delivered her 3rd child really early (I can’t remember, but it was like 30-32 weeks). There were extensive medical bills. They taught their children to work hard and to respect others. They had their own medical challenges. They lost several jobs over the last 9 years. They’ve had car trouble, making it a challenge to get to work. They ALWAYS find a way forward. If the car doesn’t work, they figure out uber and buses. If they don’t have money to pay bills, they tap into resources. They take initiative to find ways to get help with rent. I see a few splurges in their home, but they always seem like something they really appreciate. It’s not an excess of things that they’re spending money on. They communicate their challenges and let me know if something they’re working on is going to take more time. The rent they pay me is significantly under market value for that house, but I can’t bring myself to raise the rent that quickly or force them out to get it re-rented. They work so hard and are raising their kids to be resilient, and I just appreciate it so much. That’s the type of person who does not have a victim mentality.

While their efforts aren’t yielding them an extensive savings account or the ability to write a $35,000 check, they keep moving forward. Each set back is a lesson for them. They’re learning and growing. They’re not blaming others. They don’t tell me it’s someone else’s fault they don’t have money to pay rent on time.

POSITIVE APPROACH

You can be positive without being unrealistic. Optimism looks like focusing on the good in a situation, expecting a positive outcome, and approaching challenges constructively rather than ignoring them. There are many studies out there that will tell you having a positive thought process will lead to better stress management and overall well-being. It involves self-talk, reframing negative thoughts, practicing gratitude, and believing in your ability to overcome difficulties, fostering hope and improved health.

If financials are a struggle, plug in with someone who is doing well. Surround yourself with those who are meeting the goals you have for yourself. By being around these people, you will pick up on their thoughts and actions and find a way that you can implement some of those actions in your own life to start seeing success.

Before I get into an update, I have a quick perspective moment. Our preschool has a 3.5% processing fee to pay monthly tuition online. Tuition is $265, so the processing fee comes to $9.27. If I paid it online instead of writing a check each month, that would be an extra $83.43 I paid for basically nothing. For perspective, I spent $82 on a grocery run of essentials (e.g., dog food, paper towels, milk, eggs, etc).

RENTALS

I had to give notice to one household by 1/31 if I were to raise rent. Their lease ends 3/31, and that will mark 3 years with me. I was panicking because it’s our most expensive house (it’s also our nicest and biggest, and it’s fairly close to downtown). Rent has been $1750 for the last 4 years. Last year I missed the notification to raise it because a January deadline surprised me, but this year I put it on my calendar for January 1st to do. And then I dragged that calendar reminder through the whole month, only needing to then set an alarm to make sure I did it at 8pm on the 31st. I raised it to $1800 and they accepted within the hour. Phew. They’ve been late three times in 4 years and clearly communicated what was happening each time. We’ve had two major issues at the house that they rolled up their sleeves and helped mitigate the damage before the tech could get out there. They’re just really great tenants.

I had two tenants pay rent before the 1st and one partially pay before. That was surprising since the last two months I’ve had very late payments come through. I still have one person with a partial payment outstanding as of this morning.

We had a water heater go out on Thursday in one property, but otherwise I’m counting all my blessings that we made it through 2 weeks of below freezing without incident.

PERSONAL

I’ve preached monitoring your spending by writing it down for years, but I hadn’t done it. I had done it a few times retroactively, but I never made the time to keep on top of it to make pivots. With Mr. ODA leaving his career, that’s a high six-figure income that we’re without now. I’m working part time, but that’s basically a one-to-one ratio of income to health insurance. I’ve calculated that we need to be about $1350 per month in spending outside of the mandatory bills (e.g., mortgages, utilities, tuition, insurance). My threshold is lower than what Mr. ODA said is his threshold, so this isn’t a hard-and-fast amount, but one that is my “I feel OK if we’re close to this number” concept.

We screwed that up a good bit by purchasing a new vehicle and putting new tires on said vehicle immediately. We also had to pay for a previous heating issue fix in our house and a downpayment on new windows (which, quick side note, are glaringly needed as we go through 2 weeks of single digits and can feel the drafts). I’m also not counting the things that we do as mystery shops since those are effectively reimbursed (sometimes our cost isn’t fully covered since it’s a whole family outing and not a single person, but I’m not drilling down in that detail since I don’t have the specific break down of how Mr. ODA is getting paid). If I take those things out and remove expenses for rentals, then we spent $1597 in January.

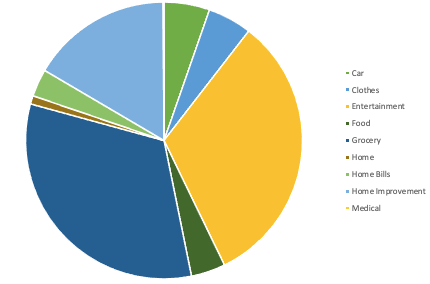

This isn’t the best representation of our spending, but I’ll develop this information as I have comparisons month over month. I also can’t seem to pick a better color scheme without it being a very manual process. Grocery, Entertainment, and Food are our biggest slices there. The entertainment category is basically why I gave up categorizing things years ago. Here I put things like going out for a drink, because while it’s at a restaurant or bar, the sole purpose was to have a drink and hang out. It also includes going to a gymnastics meet with my daughter, my fitbit purchase (I guess because I’m counting it as extra spending and not a necessity), and gift giving costs. We spent $528 on groceries this month, which feels low. I pushed really hard to clear out the food we have in the house already during our 2 weeks of being snowed in, but I hope that this is an accurate representation of monthly spending on groceries.

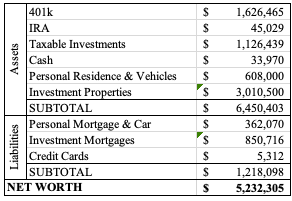

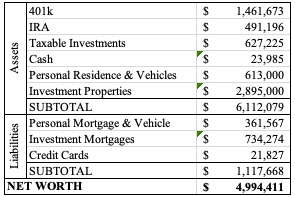

NET WORTH

It is higher than last month, so that’s good. Credit cards are carrying $4500 worth of windows, so it’s nice how low of a balance those are outside of that 0% interest balance we’re holding onto. Our investments struggled a bit over the past month, but the payments on mortgages and loans helped offset that.

We are 2 months without Mr. ODA’s pay check. I honestly haven’t noticed because my day to day is just managing how much is coming in against how much is going out. My concern is the net I have for this year is $30k less than what Mr. ODA brought in. We’re adding nearly $2k per month for insurance costs, so that net difference is $42k. That’s a gap we’re going to need to focus on here shortly. I should note that our spending includes rental work that we pay out, and we had some major purchases in there (e.g., roof, HVAC). I could say I hope that our investments in the rentals will be less next year, but we seem to track the same expense totals each year.

End of year means I need to get my spreadsheet organized. I need to make sure all expenses are logged, that all logged expenses have receipts and documentation to support them, and that all our maintenance actions are logged in my maintenance sheet. The maintenance sheet is what I use to check back easily on what work we’ve done on each house. I was taking too much time trying to remember which house we replaced things in, so now I have this sheet that I can pull up and easily say, “I just replaced a valve in that toilet 4 months ago; this isn’t normal wear and tear.”

RENTALS

The 5th was a Friday, so you know what that means – I didn’t see most of our rent until then. After the 5th was over, I was short 25% of our rental income. That is fascinating to me. Everyone had told me what their plan was, but I can’t fabricate money where there isn’t any. I have a tenant that is using a program to pay partial payments throughout the month. I can’t stand it. It ensures I get my money at the “beginning” of the month, while it puts them on a payment plan. However, they have the payment set as the 5th, and then it doesn’t clear and hit my account until about the 12th. I’ve expressed my frustration that this has gone on for several months instead of it being a one or two month stopgap, but nothing is changing.

We got our new townhome rented right before Thanksgiving. That was helpful and a literal last minute prayer that was answered in a crazy fashion. She’s been in for 3 weeks now, and I haven’t heard anything.

I had a tenant inform me that she’s hit rough times and wants to be released from her lease. I was really hopeful for a calmer month, but I need to reset my expectations. 14 rental properties and 12 months out of the year = there probably won’t be a month where nothing comes up. The good news is that we can likely get it turned over and a new person in there for market rent. She’s currently paying $975, and we’re looking for about $1300 going forward. Because she always pays and I knew her financial situation, I’ve always held back on her increases. There was another $25-50 increase coming this year, but it still wouldn’t have made up the increases in carrying costs over the years.

PERSONAL

We’ve just been so busy that we’re not really spending that much. Most of our spending is for regular purchases. We had a huge purchase hit our credit card, but that was split among our family for the purchase of new phones. I did all my Christmas shopping in the last month, so that’s higher than usual spending on the cards, but overall still pretty low.

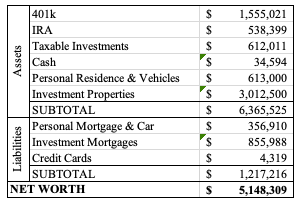

NET WORTH

I got a new phone number and updated all my accounts before my old number was deactivated (lovely two factor authentication). One of my accounts (401k) updated my phone number, but that apparently didn’t correlate to updated the number associated with two factor authentication – ugh. I need to address that, and for the time being, that’s just a placeholder number that I guessed based on Mr. ODA’s 401k increase over the last month.

We had two tenants move out at the end of July. We also had back to back trips scheduled for the end of July and beginning of August, with the kids starting school on the 13th. We also had the cruise planned for the end of September into October, so that was a decent push to get the rentals rented before we left. We put countless hours into those two houses and it definitely took its toll.

RENTALS

As of October 1st all our rentals are rented! That’s a good feeling after two months of vacancy. This is the month of taxes. We have several houses that are paid off, which means they aren’t escrowed, and I’m responsible for paying the taxes and insurance on them. The 4 houses we have in KY are owed this month, and it’s about $7k worth. We’ll owe 2 houses in VA that come to about $3k next month.

I have a couple of houses that are struggling to pay rent on time. Usually it happens for a couple of months and they get back on track, but that’s not happening quickly. I’m trying to remain optimistic, but there isn’t a track record of it getting easier if they have taken this long needing to catch up.

We closed on a new property near our house. It’s a townhouse that we hope to get rented later this month. We’ll see what it looks like once it’s empty, but it didn’t appear we’ll need to do anything to it to get it rented (which is how we buy our rentals). There will be separate posts going into the details of each rental turnover and the purchase of House15 using a commercial loan.

PERSONAL

This is the last month for the 0% interest credit card. When we have a major purchase on the horizon (it was house-wide carpet this time last year), we open a 0% interest credit card. We started this concept about 8 years ago. We look for a credit card that has 0% interest for at least 12 months and that gives us a bonus of some sort. We make more than the minimum payment each month and then pay it off before the deadline. A default payment can cause you to lose your 0%, so it’s important you’re making your payments. But we don’t pay a lot towards it because the money is doing more for us in our savings account (or the investments) than it would by paying down a 0% interest balance. This time around was a bit different. The carpet only cost us $10k, but the balance is over $14k. This credit card had the same incentive as our typically used card (2% cash back), so Mr. ODA used it a majority of the time. For a while, my goal was just to pay what gets our balance lower than the original balance from the carpet. But then we had some big rental purchases that we put on the card, and it just wasn’t worth paying $5k+ to the card. We will make a transfer from our big savings account to make that payment at the end of the month.

Mr. ODA’s last pay check arrived on October 11. He took the “deferred resignation program” as of April 30. The sunset date was September 30, so that covered the payout that we just received, including his balance of annual leave.

Outside of rentals, our spending has been minimal. With the cruise, we didn’t spend much since that was a week of almost everything paid for in advance. The dog had his annual check up, so he was the bulk of our costs. We have our routine costs we see, but happy to see lower balances after all the rental work costs.

SUMMARY

I don’t even want to admit what is about to leave our account this month. I guess the positive is that it’s under $100k..? We have to pay the taxes on the houses that aren’t escrowed, pay off that credit card, and buy a house. At least the house purchase goes right towards equity. Since I didn’t get all the account numbers yesterday morning like I planned, here’s an update that captures our new purchase.

After each trip, I typically summarize how much it cost us. I like talking about money, mostly to work towards eliminating the stigma about talking about money. The more information you have, the better informed you are when it comes to decisions, so here’s a reference point to file away. We sailed Royal Caribbean’s Oasis of the Seas. I loved it!

COST BREAKDOWN

Flights – 25,000 miles + $273 We looked at several different flight options now that we’re a family of 5 flying and that adds up quickly. The first night we were looking to book the cruise, there was a group of 5 tickets for just under $700, which we thought was a great deal, but once we were ready to book, it wasn’t there anymore. We ended up going with Frontier for one direction and using American Airline miles for the other direction. When booking with miles, you only need to pay the taxes on it, so that’s what we did.

The flight options were very limited for the way home. We ended up just sucking it up and picking a 9 pm departure. Not long after the booking, we received an email saying our itinerary was changed and now the departure is 12 pm. While that seemed concerning at first – to get off the cruise, through the airport, and to our gate before noon – I had hoped it would be just fine, and it was. We got off the ship around 8:30, took an Uber to the airport, and arrived too early to check in for our flight. They built the airport expecting this isssue, so they sent us to the waiting room. We sat there for about 45 minutes and then checked our bags and got to our gate. We sat at our gate for a couple of hours and got home on time.

On the way down, we each got a checked bag because of our American credit card. However, we still needed to prepare for “carry on” status on the way home with Frontier. Then, once we were already packed, Frontier offered us to upgrade all our bags to checked bags. Had I trusted that they wouldn’t have said “no, you have to check a carry on size,” I would have happily changed our 3 carry on bags to one big bag to make traveling through places with 3 kids easier. So while some parts were harder because we had 3 rolling suitcases to account for, it was nicer through the airport to not have suitcases to manage.

Hotel – 34,000 points If you’ve ever had to fly into a cruise port, you know it’s less stress-inducing to fly in the day before. I went on a cruise a year and a half ago, and we were flying out during a snow storm that was affecting travel all over the area. We ended up arriving at our hotel near midnight, so we were happy to know we were there for the cruise boarding time and not stressing about delays that morning. That means there’s a cost for a hotel one night.

The hotel was booked with points, so it wasn’t a literal cost to us. We stayed at the Tru in Dania Beach. They had a shuttle from the airport to the hotel, so when we arrived, Mr. ODA called the hotel to come pick us up, and it worked out well. We had to wait 20 minutes for a crib to arrive, even though it was on our reservation as a request. This isn’t a huge deal, but when it’s 10 pm and I’m just setting up a crib to get over tired kids to sleep, I’m not thrilled. Otherwise, the hotel was nice and it provided a good breakfast.

Uber – $58; Airport Parking – $70; Dog – $289 The hotel provided a shuttle from the airport to the hotel, so we didn’t have to pay for that part. Then we needed an Uber from the hotel to the port, and then from the port to the airport. We requested a car seat in the Uber on the way to the port, so that limited our options. Then she was 23 minutes late to our pick up time, didn’t get out of the car to greet us or help set up the car (pick up the 3rd row to fit our 5th passenger we disclosed ahead of time), didn’t acknowledge being late, and generally didn’t speak to us except to say get our IDs out for the port. That’s not an Uber issue, it’s a specific driver issue, but that was not a great experience. On our way from the port to the airport after our cruise, we got charged a wait fee, even though the wait was because security was stopping our Uber from getting to us. Uber removed that charge though.

The CVG airport parking is $10/day for economy. That’s my first economy experience instead of the ValuPark lot, which is $12/day. I didn’t really think anything of it, but it wasn’t a great experience. I always thought it odd that the ValuPark lot has shuttles that pick you up at exactly your car, but the economy lot has the shelters. I didn’t properly account for the time to wait for the shuttle and then to have the shuttle drive through all the shelters.

Food – $44 Obviously most of the food was part of our cruise fare. We had McDonalds on the way to the airport, Burger King during our layover, and then McDonalds on the way home.

Cruise – $3,099 The big one! We did not prepay gratuities, so that was billed as we left the ship. Gratuities are $18.50, per person, per day. We had $50 on board credit. Ironically, and just coincidentally, we spent $50.40 between drinks and child care (the babies room (0-3 years old) is $6 per house before 7 pm and $8 per hour after). Royal Caribbean only requires $100 per person as the deposit, and then the balance is due a few months before the cruise departure. We booked right at that threshold, so we paid our deposit and then a few days later paid the balance.

LOGISTICS

The booking of the cruise could have been a bit more forward. Cruises are not family-of-5-friendly. There’s an option on Royal Caribbean to book a “guarantee” or GTY room. You get a discount for allowing them to assign you in an open room (of the category you picked (e.g., interior, ocean view balcony)) about a week before the departure. I did this for a cruise I took in January 2024, and it worked out perfectly fine. So we see these prices quoted online for GTY rooms, but they always make you call to book for more than 4 people. We’re expecting the cost to be just the taxes and port fees for the 5th person, but when we call, the difference is over $500.

We tried to explain how that feels like a bait and switch and that there’s no indication of that on the website, and they basically said “well, that’s the way it goes.” They can’t guarantee a 5+ room available at the time of sailing. This makes sense, but it also eliminates our ability to use that cheaper booking option. We asked if there was something they could do to help make us feel whole since we were being forced to spend $500 more than if we could be put into the guarantee-pool, and they gave us $50 on board credit.

Mr. ODA’s parents book Celebrity (same parent company) all the time, and if they book their next cruise while on their current cruise, they are given OBC. Turns out Royal Caribbean doesn’t have the same philosophy, and they hardly give OBC. We tried to see if there was a special deal for a cruise if we book on the ship and they had nothing to offer.

Our departure experience was horrific, and I’m not even sure how we timed everything so poorly. At CVG, the kiosk jammed printing our tags, so we had to wait in line to get to the counter for the last luggage tag. Well, the line took forever because there was a large group in front of us that couldn’t speak English, so the workers couldn’t get everyone checked in quickly. Then we were too late for her to print checked bag tags because it was 30 minutes before the flight. So now we’re stressed trying to get through her attitude, us being late, and having to get through security and run through an airport with 3 little kids. This is the first time I’ve ran to my initial flight (ran for connections countless times!). I’ve never had this issue before, but everything along the way took just a few more minutes than I had planned for, and the luggage tag issue stole about 15 minutes of time from us (plus, our flight was delayed by 20 minutes and then 45 minutes before the original flight time, they said it was on time… we hadn’t delayed our departure from home, but it was wiggle room we thought we had and then suddenly didn’t). After the attitude from the ticket counter, then we encountered two more attitudes from the gate agents. It was a rough start, but the flight attendants were nice, and we had plenty of time to catch our breath at our connection.

Child care is provided on the ship. They have a few hours in the morning (maybe 9-12?), then 1-5 for the afternoon, and then 7-1 am. For the kids 3-12 (split between two rooms of 3-5 year olds and 6-12 year olds), it’s free until 10 pm; then it’s $10 per hour per kid after 10 pm. For the babies (0-3 years old), you need to make a reservation for times when you arrive on the boat. We prioritized the buffet, so by the time we got to the kids area, lots of time slots were booked already. She offered me 6 hours worth of booking, which I split between 3 days. Our youngest is 7 weeks shy of being 3, but he wasn’t 100% potty trained (although we did try) so they wouldn’t let him move up. If he was potty trained, they would have let him go up to the 3-5 room. The first 2 hour block, we only used 1.5 hours worth of it based on the activities we were trying to get done. The second 2 hour block, we only used 1 hour worth. And then we didn’t use our final day worth of time because he got sick, and I didn’t want to contribute to the spread of it. We dropped the big kids off a few times and just took the baby with us to activities, which worked out fine. He’s so good when he’s alone, but the 3 kids feed off each other!

I brought lots of hook magnets. I used them to hang everyone’s lanyards with their seapass cards, hats, and to dry bathing suits. I also used them to hang from the ceiling and utilize curtains that I brought (actually, I bring these curtains everywhere we travel because a really dark room is important to getting the kids to sleep past sunrise when bed time is 2-4 hours later than usual). There were 2 hooks in the shower, 3 hooks on the bathroom door, 2 hooks in the bathroom with 2 towel bars, and 2 hooks outside the bathroom. We’re going on another cruise next year, and I’m going to bring more hooks because we could have used more space to dry out bathing suits. Having the curtains hanging to separate the kids from each other and then from us was great.

I also bought a pack of decorative magnets. This is very unlike me; I don’t like anything extra. But I put them on the stateroom door, and it helped the kids identify which one was ours. The door is textured, so they didn’t all fit. I put them inside the cabin on this big blank wall, and I actually really appreciated the decoration.

You’re allowed to bring on 12 cans/bottles that are less than 17 ounces each, so we did that for Mr. ODA’s sodas. We didn’t buy any drink packages. I don’t know what sodas cost on the ship. At the buffet, we have lemonade, iced tea, and water available. At some of the included restaurants, they have other flavored water type drinks like strawberry melon. At breakfast they had apple juice and orange juice. There are enough options for variety if you’re not looking to buy a package. I had Mr. ODA bring a non-diet/zero type drink in case I wanted some variety, but I was so full that I didn’t end up wanting any sodas and had a couple of lemonade and juice options throughout the week. The alcoholic mixed drinks are about $15 a la carte. They offer a happy hour special of margarita (and maybe one other option that’s $6-7) and have a drink of the day that’s $8. I didn’t know about the drink of the day special until day 3 and didn’t know about it at all on my last trip, so that’s a positive to know. I think the Truly/beer type option was around $8-9 each.

When buying the drink package, that’s your baseline. Are you going to drink 5 mixed drinks or 8 beers/Truly each day to make paying up front worth it? I’ve heard some people say “I just like not having to think about what I’m ordering.” But, do you enjoy paying $65 for 2 drinks? I understand it’s vacation and many people have the mentality that money is no object, but it is something to pause, have the perspective, and make an informed decision on.

The app is really good. There’s a little room for improvement, but everything you need is there. We’d like to see a search feature, where you can search “bingo” or “laser tag” and see the offerings instead of scrolling every day and hoping you catch the times. I like the daily tips they post about what’s happening that day and some good reminders. I also like how many activities are offered. I wish there were a few more things in the 6-8 timeframe for those with a 5:00 dining time, but I understand that’s not the worst problem. There is so much offered for other times, and I found myself juggling wanting to do all the things, but also not wanting to be on a schedule.

A few weeks before your cruise, the app will have most of the shows and activities available. One example that we didn’t have until we were on the ship was laser tag’s schedule. But you should get on your app a month in advance and keep checking for the show reservations to be opened. They seats go fast. We were able to reserve the ice skating show and Cats, but we weren’t able to get a seat at the aqua show. I was really bummed about that, but we went to the aqua theater at the beginning of the show and were able to get a seat.

We did not pay for a wifi package, nor did we set up our phones for an international plan. I was looking forward to being completely cut off from the world for 4.5 days. To my surprise, iMessage worked the whole trip. It wasn’t too bad, and I got to share stories as we went with some people.

LESSONS LEARNED

Book any 0-3 year old child care slots ASAP

Pack half the pajamas you need (our kids wear pajamas through breakfast at home, so there’s no re-wearing, but they don’t eat anything in the cabin, and they don’t leave the cabin once in pajamas, so don’t use up the space)

Prepare accordingly for theme nights (I may have not planned well for my oldest)

Bring as many magnets as you can hold (although you may get flagged for a bag check in security)

Read the daily tidbits in the app each morning

Don’t pack lots of snacks (I thought I’d be looking for breakfast faster than everyone being ready to go, so I packed granola bars. I also thought we’d want more snacks, but we’re so full from eating bigger meals and being on a different type of meal schedule that eating in the room was never a thought)

If you’re on the cusp of 52″, 48″, age 3, or age 6, I may wait until those milestones are hit. While it’s not the end of the world and doesn’t kill your cruise, we had kids disappointed they couldn’t do some things based on height (water slides) or age (rock climbing).

Drink the happy hour or daily special beverages if you don’t have the drink package

THE CRUISE

We took a 5-night cruise. It was more time than I had planned for originally. I didn’t want to be stuck on a boat in case the kids didn’t take to sailing well, but the price was $1000 less than the 3-4 night offerings, so we went for it. It worked out well. Everyone’s first question seems to be, “were you afraid of them going overboard?” Turns out, there are very limited options for that to even occur. We were in an ocean view balcony, but the glass goes higher than the littlest ones, so that wasn’t an issue. Most decks have the staterooms on the outside, so the only real place they could attempt to get overboard is on decks 15 and 16, and a little spot by rock climbing on deck 7. It was barely a thought of mine the whole week.

The biggest hurdle of the week was getting the kids through crowds. There’s a lot of people on the boat, and people tend to congregate in certain areas. Keeping 3 little ducklings together in a crowd could have been worse, but it wasn’t the easiest either. The cruise ship gives you bracelets for your kid to wear with their muster station on it. I wish there was more information on it, so I put their names and room number on the back. The youngest didn’t have a yellow bracelet, and I wasn’t happy about that. Luckily, I had packed a bracelet that I could put his information on. I used a regular sharpie and the lettering was legible until about the last day. I could have rewrote the information, but by then I was feeling more comfortable.

We did not push too hard to get to all the activities. We made a concerted effort for a few activities, but I didn’t want to be tied to an agenda all week. We generally started the day with breakfast. We ate in the main dining room twice, which was quieter and calmer, but also slower. One morning, I ordered a small breakfast, and the waiter pushed me to get the “express” breakfast. It came with 2 things I didn’t want, and I was frustrated that he pushed me to waste food. We usually then went to the pool or splash area (the splash pad is pretty cool with slides and activities within it for the kids). Ice cream opened at 11:30, so that worked well as a way to get out of the pool and start drying off for lunch. We ate lunch in the buffet (Windjammer). I personally liked the variety of options with the kids, but it wasn’t the easiest process. Apparently kids really struggle holding plates flat. We only lost one apple once, but it was stressful every time trying to make sure they kept the food on the plate while walking. Our afternoon was spent either with the kids in the kids club area (Adventure Ocean) while we did trivia, or they came to trivia with us. We rode the carousel, the big slide (Abyss), and participated in some random activities (family festival, scavenger hunt). We would get back to the room at about 4:55, rush to change, and then run to the main dining room for our 5:00 dinner. On my last cruise, there were only 2 dinner times, so being on time seemed less of a priority. This sailing had a 5:00, 6:45, and 8:00, so I felt the push to be as close to 5:00 as possible so we didn’t delay a 6:45 sitting. We ate all our dinners in the main dining room. I truly appreciated the themes, but perhaps only 50-60% actually participated.

At Cozumel, we got off the boat, had a beer at a tourist trap, and got back on the boat. I don’t think we were off the boat a full hour. There was swimming available in some pretty water just next to the cruise ships. There are shops for trinkets and a few places to eat or drink. It was an area that clearly catered to cruise ships and I felt perfectly safe.

Our second stop was Royal Caribbean’s island, CocoCay. I can’t sing enough praises about this concept. All your food is available. There are servers just like on the boat if you want a drink. It’s clean. There were some concerns about jellyfish while we were there, but we didn’t have any problems. My youngest was struggling with the sand concept (and not touching the sand and then rubbing his eyes or sucking his thumb), so we eventually moved over to the pool. The pool was packed, and I almost said lets just go, but we got in. Once you were in, it wasn’t uncomfortable at all, and there was plenty of room. There’s a 0 entry area with water fountains, which kept the kids entertained well. There are life vests on the island for your little swimmers. I did hear that snorkeling was sold out when we arrived around 10, so you could keep that timing in mind. The ship staff give you towels as you get off the boat (you sign them out with your seapass card), and there are towel stands on the island if you want to swap out your wet, sandy towel for a new one.

I will note that we had a medical emergency just hours into the cruise. It didn’t affect us at all. We heard the “alpha alpha alpha” call while we were at dinner, and about an hour later, the captain came on the loud speakers and announced the plan. We departed Ft. Lauderdale, but we were going to return to Miami to get this patient off the ship. They were making a plan on whether we’d have to fully dock or if the coast guard could come out to us. They announced a bit of time later that they decided the coast guard could come out. Then about a half hour after that, they said that the swells from the tropical storm we were near were too rough and the coast guard couldn’t get close to our ship to safely transport the patient between the two boats. So then they decided to send out a helicopter, and that happened just as the sky opened up on us at the aqua theater and we gave up and went to bed. So even though the course changed, it really didn’t affect anything we were doing on the ship. The patient actually got off and received emergency coronary bypass surgery that night and was recovering, so that was a blessing. There was also supposedly a death in another cabin, which I knew nothing about until after I got back home. I share this just to say – things happen, and there’s so many people, so it’s not surprising, and it didn’t affect the rest of the trip.

Getting on the ship and off the ship on the bookends of our cruise was extremely easy. I had a similarly easy experience at Cape Canaveral (actually probably easier). On the way there, we went through the security check points. I was flagged for my magnets, and in the process, they found my extension cord. Honestly, it wasn’t clear what the rules were about the extension cords. I wasn’t worried about the number of plugs as much as I was the extension to an outlet. They’re quick to say “there are plenty of outlets,” but they don’t address the fact that 3 outlets are on one end of the room and there’s only 1 at the bed. It didn’t matter though. We plugged in a phone overnight by the bed, and the sound machine was over by the kids with that 3 outlet option on the desk. They confiscated my extension cord, but they tagged it, and I got it back at the end of the cruise. After that, we went upstairs to a huge waiting room. We were told to sit in order as we entered. The place was packed; I expected this to take a while. It was less than 2 minutes. We scanned our boarding passes and walked right on. On the way off, everyone just left when they were ready. We walked right into the main dining room, scanned our seapass cards, and left the ship. There was luggage areas to pick up any luggage you had carried off the ship overnight, but we hadn’t done that. Then you go through the immigration check where they take your picture and approve you to continue. And that’s it. There was no queuing through either process except for the 2 minutes we sat in the waiting area at the port on the way on the ship. It’s incredible to me.

SUMMARY

I was a reasonable level of nervous taking 3 young kids on a cruise for 5 nights, but it went significantly better than I expected. Our next cruise isn’t until this time next year, but I wish it were sooner! I highly recommend cruising, especially with Royal Caribbean.

This month was unbelievably painful financially. And yet, I appreciate that we’ve set ourselves up that we can handle these things without stress, even though the balances on credit cards made me feel like I was drowning. At one point, we had over $30k on credit cards. I’m still juggling life as a mom, financial consultant, part time worker, and volunteer on the HOA board. Oh, and managing two vacant rental turnovers, throw in 2 trips away from home, and school starting.

RENTALS

We had one house pay late, with little notice and communication (if you’ve been here, you know this is a pet peeve of mine). They paid the late fee at least. I had another house pay partial on the 3rd and then true up on the 6th. Again, no communication, and she beat me to asking what the deal is. I also had a tenant who already pays twice per month be late on both of this month’s payments, so that also brought in late fees.

In a story for another time, we have two vacant rentals. 11 of 13 houses renewed. Two houses each actually moved out of state, and unfortunately, my kind heart scheduled both of them to end their leases on July 31st. We’ve been spending all our time at these two houses. The one had smokers in it (against the lease) and we’re struggling with that. We’ve replaced the carpet and painted all the walls (except 2 closets and a powder bathroom) and it still smells funky when you walk in. Then there’s just the routine type turnover things like scrubbing and wiping dirty hand marks off the door frames. All of these things will be detailed in separate posts. The other vacant one was quite the story, so that’ll be multiple posts. Our attention isn’t as heavily on that one because we’re going to likely sell it instead of re-rent it.

We replaced a roof ($5500), replaced an HVAC ($8300, but split with a partner), evicted bats ($1480), and made decisions on flooring replacement in another house with extensive termite damage. Seriously. Financially painful. Coming this next month, we will also be paying for termite repairs at another house where we tore out carpet and laid LVP.

HEALTH COSTS

I tend to focus heavily on this topic in this blog. It’s surprising because it’s not really the niche of making money, but insurance and doctor bill processing seem to be wrong more than they’re right. Therefore, it falls more into “protect your money” than anything else.

This is a longer story for another post yet again, but the gist is that the insurance company took 6 months to process a claim. They sent me the bill in June. I called 3 weeks after the bill arrived to find out they had sent my balance to collections because their system flagged it as a January overdue balance…even though this was my first invoice on the matter. Love it.

The end result here is that we needed to add $1600 to the credit card.

PERSONAL

I don’t know that there’s much personal life happening with all those other things we’re managing. We took 2 trips. One didn’t cost us much because the grandparents take care of a lot of the cost, another one cost us more than usual because I put a lot of effort into food that we usually don’t do when we travel there. Overall, the trips were fairly inexpensive financially, but they took a toll on me due to the time commitment and what we had to give up by doing these trips.

Otherwise, we’ve just been wrapping up summer and starting school. We’re about to get back into baseball season with lots of practices.

NET WORTH

The market had a big jump last week and my update of financials occurred Thursday morning. Unfortunately, life put a blog post on the back burner while we were turning over a rental, so I’m only getting around to posting this now. The market is in a fairly similar spot as of yesterday’s close, and I’m thinking we’d even be over $5 million if I were to fully update our financial status right now. We’ll just hope for the best for next month.

In October, we’ll pay off our $15k credit card that we’re carrying, so that will be a big swing in our credit card balance two months from now. We need new windows at our house (the seal keeping in the gas between the panes is going on quite a few windows (or went years ago), and it creates this streaky dirty look to them), but I think I’ll appreciate not carrying this large credit card balance month to month while we utilize the $0 interest for a while.

Over a year ago, we opened a new credit card because we replaced the carpet in our house. This year, we finally were able to make a purchase we’ve been waiting for: a hot tub.

Mr. ODA has wanted a hot tub for a while. We did some exploratory searching in May, thinking our deck project was nearly over. Then the waterproofing was never waterproofed. The contractor ghosted us on it. Mr. ODA bought his own supplies, but it was never enticing to tear up our brand new deck boards in 95 degrees to diagnose and fix the problem. We finally got around to that project in August. Once that was done and life calmed down a little bit, we decided to put more effort into the search. We went to 3 different places one day to get information. Then we sat on that for a week and decided on which one we liked the best and ordered. They told us 3 weeks, and it’s expected to be delivered and installed this coming Tuesday, which is over 5 weeks from our down payment, but such is life.

WHAT WAS THE BACKGROUND?

When we were in the process of IVF to have our first child, Mr. ODA was discouraged by the lack of financing availability. We could either take out an outrageous personal loan, or we could pay it in cash. Their “guarantee” program was $22,000. Up front. That didn’t include the medications that were bought separately.

We never like the idea of paying large sums of money out at once if we can help it. We make our money work for us.. meaning money is constantly moving and being invested in short term securities for us to earn interest on it. Mr. ODA had the idea to open a 0% interest credit card for the IVF payment, and this idea has carried us through several large purchases now.

WHY A CREDIT CARD?

By opening a new credit card, which we strategically pick, we give ourselves a personal loan for 0% interest.

A personal loan averages 12% at the moment. Since we have the cash available to pay for a hot tub outright, paying any percentage of interest to a bank is not something we’re interested in. We could just pull about $10k out of our savings account, our short term securities, or cash out a taxable investment. However, that costs us interest that we’d be paying ourselves. In our savings account, our current balance yields us about $120/month in interest earned. If we reduce that by about $10k, we’d lose about $30/month in interest payments. Instead, a new credit card is opened. It gives us the ability to pay the minimum balance (or more if we want) each month, leaving that cash in our account to earn interest or be invested.

WHICH CREDIT CARD?

When we search for a new credit card, not only are we looking for 0% interest rate for an introductory period of at least 12 months, but we’re looking for another incentive. Many people were talking about “credit card hacking” a few years back, where they’d open a new credit card to get the bonuses and then render that card obsolete (not close it). There are negatives to opening too many credit cards that I’ll get into later.

Not only are we looking for 0% interest, we also would prefer to receive another incentive for the credit hit. This new card gives us $200 cash back for spending $500 in purchases in the first 3 months, which we’ve done without any problem. This particular company has other options on the market. One card gives you 4% back on certain purchases, but there was no introductory rate on purchases. Other cards have an annual fee, which we try to avoid unless it’s glaringly obvious that you’re going to make that fee back in rewards you can’t get elsewhere (e.g., I’m not going to pay a $99 fee to get 2% cash back when I have a credit card that gives me 2% cash back without a fee).

Typically, these credit cards don’t offer us a better incentive than other cards already in our portfolio. However, this new card actually gives us 2% cash back, which is the same as the Citi Double Cash card. This will change our equation of managing the balance a little. Historically, I’ve had a balance on the new credit card, paid $500 per month towards it, and then paid it off before our introductory interest rate period expired. The balance almost always was decreasing, so I knew what I was working with. This card is being used more often, with 4 transactions in the last 3 weeks already on it. I’ll be interested to see if that changes how I manage the balance.

WHAT ARE THE CAUTIONS TO CONSIDER?

First of all, the most important thing to consider is where this purchase is something that you can and want to afford. When your money goes towards one thing, you’re taking it from something else. Weigh whether that’s worth it. In the case of IVF, having a child was more important than any other place those dollars could have gone. In the case of the new carpet, all of the carpet in the house was old and, frankly, disgustingly stained; I wanted the carpet replaced as soon as possible so that I could enjoy what I was living in. And now, the hot tub. This is one of the few splurge purchases we’ve made. We have gotten to a point on making decisions that bring us joy. We were also gifted money over the last year or so that was earmarked for this.

When putting a large sum of money on a credit card, you can’t forget about it. You still have to make the monthly minimum payments. If you don’t, you could have to pay back all the free interest you’ve received thus far and/or start paying interest (to the tune of 22%…so that’s $2,200 in interest on a $10k balance) on the balance immediately. You also need to be able to pay the entire sum by the end of the introductory interest period (or, again, you’ll be paying interest on the balance).

For the credit card that we used to pay for new carpet and new windows on a rental, we put nearly $12,000 on the card in October to December of 2023. We also used it to make 2-3 more relatively smaller purchases. I paid $500 every month towards it. The minimum payment was typically around $100, but I wanted to see the balance dwindle a bit faster than just the minimum. My current balance is $6,500. I’ve been been monitoring our money movement for a month or so, preparing to pay off this balance no later than December 13th (I appreciate this company explicitly listing the date of the introductory rate expiration because they don’t always do that). A balance of $6,500 is obviously less than needing to outlay the full $10k-12k last Fall, but it’s still not a small chunk of change that needs to be fit into our cash flow right now.

Opening a credit card will affect your credit score and history. This may not matter to you if you don’t have any large purchases (e.g., buying a home) on the horizon where you’ll want the highest credit score you can get yourself. However, if you believe there will be large loan-seeking opportunities in the next 1-2 years, opening a new credit card should be carefully considered. – It’ll count as a hard pull on your credit, which degrades your credit score for one-two years. Credit Karma says the “ding” on your credit lasts only about 3 months, but too many at one time could cause a bigger drop in your score. – Opening a new card lowers your average credit history. This is why people say not to close any accounts. If you close an older account, it brings your average down. My average is currently 6.5 years, and it’s listed as “fair.” If you have old cards that you’ve kept open, you may need to use it for a transaction to keep it active and open. – If you’re adding a large sum on the credit card, your credit utilization could be higher than preferred for your credit score calculation. According to Credit Karma, you should be below 30% credit utilization, and being below 10% is even better.

SUMMARY

If you’re about to make a large purchase that you’ve considered carefully and have decided is worth the cost, then opening a new credit card with a 0% interest for an introductory period could be a beneficial option. It’s a way to give yourself a personal loan for no interest. Be sure that you have projected the cost over the course of the introductory interest period so that you know you’ll be able to pay off the balance in time, and that you make all minimum payments on time.

Here’s an unpopular opinion: you don’t need to buy all the amenities to have a good vacation.

Our financial advisor has a saying in his family, “we can’t afford ice cream.” If they wanted to, they could clearly pay for their family to have an ice cream night on vacation. However, they choose not to spend their money in such a way for the sake of the big picture.

The point I’m trying to make here is that you need to stop and think about an expense. I can’t remember what the item was, but when I went to pay for it, it was $8. It’s not that I couldn’t afford to purchase something at $8. It was simply that this item was worth $2 to me. The value of it was not $6 more of my money.

This post (or rant) started because of this Facebook post that was made in a local mom’s group. Apologies for the large image, but you couldn’t read the numbers until I got it this big.

Quite a few people echoed my point – stop with the add-ons. You can have a great day without the additional amenities/activities, and without the all day dining options. We had a season pass to the Cincinnati Zoo. We ate before we entered, packed snacks, and then ate on the way home if needed – at McDonald’s, with deals (we lived over an hour away from the zoo, so sometimes we couldn’t plan it to have only one meal while out). At a similar place to Kings Island, I know people who have packed coolers and left them in the car because you’re allowed to exit and re-enter.

Not buying extras holds true for any event. Your kid doesn’t need a $20 light up wand, that will be promptly forgotten about at the 48 hour mark, at Disney on Ice. The show itself was exciting and a “treat,” so let it stand alone. Your kid doesn’t need a $15 ice cream at the theme park. Simply let them enjoy the experience without developing a sense of entitlement or expectation that they’re going to get a “treat” every time you’re out.

I completely understand the mentality of “go big” for vacations because it’s a special time. But what is that worth? I know some people spend all year saving up to go to Disney, and they want the “full” experience. Disney itself is very expensive, but then you start spending on gift shop paraphernalia and food in the park, you’ve now spent a small fortune for hours of entertainment.

DISCIPLINE

Instead of only being disciplined for those few days per year, focus on the question: what is each individual dollar worth? I have an entire post where I share the thought process and conundrum I faced for purchasing a $4 weighted tape dispenser. Seriously. While you’ve “saved” for this vacation, what if that saving mentality helped you be able to pay your regular bills along the way? Or what if instead of spending extra money on vacation, that money went towards paying for school supplies? It’s all about creating the mentality and discipline to ask yourself what the value of something is, both to you and to the economy – if you’d pay $2 for a water bottle outside a stadium, is it worth paying $6 inside the stadium? Or could you plan ahead and bring your own water?

This irritation isn’t only for vacations. A friend of mine would leave their house to go to a nearby gas station to buy gatorade and soda bottles. You were at home! If going to the gas station is a regular occurrence, and you enjoy drinking soda out of a bottle, why don’t you get a multi-pack and keep it in your refrigerator? Then there’s the person I used to live across the street from who would order door dash regularly. It probably averaged to once per day; some days there was two deliveries, and some times she may skip a day. Then she posted a GoFundMe for help to pay for her tuition and books to finish her RN. She also posted all the amazing toys (excessive and expensive) she got her kids for Christmas, while also complaining about her son’s behavior being out of control, and that her daughter was being so bad that she got tv in her room taken away – wait, why does a THREE YEAR OLD have a tv in her room? So tell me again how you can’t make ends meet, and how you need help finishing your degree, while you have zero discipline on spending the money you do have. Why is it everyone else’s problem to fix for you when you’re putting no effort yourself? I’ve digressed.

OUR RECENT TRIP

We just went on a trip to Jellystone. My son had asked to go back to a cave since we left a cave last year. He’s obsessed with space and Earth. He was 4 at the time of this trip. For 2 adult tickets, all 5 of us were able to take a 2-hour tour at Mammoth Cave (children 5 and under are free). That was $40 worth of entertainment. I figured it was a good time to take advantage of their pricing structure before it would become $60 next time we’d try to go. While I felt the $40 was worth our time and money, I mildly regret it. His excitement for the caves was worth it, but we missed out on activities at Jellystone that I think they would have enjoyed. At 4 years old, we could have easily skirted the cave desire because he doesn’t know that a cave is 20 minutes away when we’re at this location.

We paid $433 for a 4 bedroom cabin for two nights, and that included a $50 charge for bringing a pet. We packed all our food for all the meals. My choice to allow the kids to stay up way past bedtime and for the two older ones to share a room cost us on day 2; I promised them ice cream if they powered through the cave, so that was $14 for all of us to have ice cream, which wouldn’t typically be an expense we incur. Other than the cost of gas to go 260 miles roundtrip, we spent nothing else.

There were opportunities to pay for things. We could have rented a golf cart for $70 per day. We could have paid for the mining sluice, which didn’t have a price advertised, and would have been 3 minutes of entertainment. We actually did try to do their obstacle course, but none of our kids were tall enough. Instead, we took advantage of their amenities. We drove pedal cars, played at their numerous playgrounds, went swimming, went to their beach to play in the sand and swim, ran around the splash pad, did their craft times, attended their character greetings, played bingo, played minigolf. We probably just sat at the cabin for a total of 3 hours between 3 pm check in on day 1 and 11 am check out on day 3; we even let the kids stay up until 8:30/9 (their usual bed time is 6:30).

UPCHARGES

So let’s look into amenities at GWL. I’m going to look at Mason, OH’s location. First, because it’s the one closest to me, so I’m familiar with it, but also because whenever there’s a Groupon for $99 nights, Mason is always $149. That tells me that Mason’s probably on the middle-to-higher end of amenities and their cost.

For a weekend in October, my room options range from $410 to $1035 per night. They provide a rate calendar option for you to see the rates on other nights because you may feel that $1035 for a night in a water park and hotel is absurd (I hope you do….). I also encourage booking with a code (there’s a Facebook group that shares active codes for deals), using a Groupon, or planning in advance and being flexible on dates.

You select a room option (I picked $410), and then it offers you a late checkout option. Check out is 11 am. For $50, you can stay in the room until 2 pm. What are you going to do with your room between 11 am and 2 pm? When this option is presented to you on the screen, what are you thinking? Are you thinking it must be a necessity because it’s being offered? Are you thinking that it’s needed because you don’t want to “leave” at 11 am? Or are you really thinking about the cost/benefit ratio of this charge? Are you expecting to be done with the water park for the day at 1:30, so you’ll go shower and change before the 2 pm check out? If I’m spending the day at the resort, I don’t see where I need the room between 11 and 2. I have one exception, which is very specific right now. If I hadn’t just paid $400 for a night there, I may consider the upgrade because we still have a napping kid from 11-1, so that could be helpful, but that’s not worth the additional $50 to me, personally.

GWL does a good job at pushing their pass options. There are 3 levels, ranging from $50-70. The options include a variety of: MagiQuest, Build-A-Bear, Mining Sluice, mini golf, bowling, GWL goggles, $5 to the arcade, candy, and an ice cream. Purchased individually, the price for the pass is a better deal by a few dollars than if you purchased these individually. However, do you have the time to do ALL of these activities and enjoy the water park? If you’re staying one or two nights, you likely don’t have the time to get the most out of everything. Don’t forget that they offer several ‘free’ activities (e.g., yoga, character greetings, bed time story, crafts, etc.) each day as well, not to mention that you’ve just spend $400 on the stay to play in the water park.

Don’t forget that on top of the room rate, there are taxes and a resort fee. If I wanted to stay for two nights with 2 adults and 3 kids (even though one is less than a year old), with no extra purchases, my total is $1,023.70. That’s $820 for the room, $124 for taxes, and $80 for resort fee.

These options that are presented don’t even include all the options you can pay for. For instance, you can rent a cabana. You have to call to book it, but I’ve seen it priced at $200 and at $500 for it. It’s not private. It’s not secluded. It’s not secure for your belongings. Make sure you ask yourself what you’re getting for that cost and if that money could be put to better use.

As a kid, we used to go to Lake George. We joked that it was our vacation from our vacation. The point of Lake George was to do nothing. You played in the pool at the hotel, walked the town, and got ice cream each night. It was relaxing. I remember lots of our trips, but Lake George sticks out as a favorite. Even our trips that were busy – it was busy because we were sightseeing and driving far; it wasn’t busy because we were paying for activities and trinkets.

We went to Disney on Ice, and my son still thanks me for the experience; he didn’t get any trinkets while we were there, and he still loved the experience. Your kids will remember the time they spent with you. That’s the point of the vacation – spending uninterrupted time with your family, not making it an exhausting, jam packed few days where kids are overstimulated and sleep deprived.

This isn’t a parenting advice post. It’s simply a moment to stop and think about your spending. Take the time to determine whether a dollar spent on an activity is worth that dollar’s cost in your day’s/week’s/month’s/year’s goals. The tape dispenser. Truthfully, I didn’t know it only cost $4. Regardless, I still took the time to consider whether buying this thing that I need for 1-2 days per year was really worth spending our money on, or could that money be put to better use.

In 2021, we purposefully took trips each month. We had looked into buying a vacation home, and we decided that we’d rather go to different places each trip than the same place over and over. The mortgage was going to be about $1200, so we allocated that much as our trip budgets. In May, we spend $618; June was $200; July was $690; August was $1069. I say this for perspective.

Take the time to analyze the spending that you’re doing, independent of the deals being offered. Will that one trip be worth the cost of it? Will the money spent for that trip be worth anything that you may have to give up to make that trip happen?