I have heard many comments about the cost of school supplies, and someone just said to me they spent $400 on two kids’ supplies in elementary school. I spent $140, and this included all the wish list items for two teachers. Pause. According to our school district, teachers can’t put things like paper and tissues on the supply list, but they can have a wish list. I assume it’s because the implication is that everyone is expected to purchase all the supplies, but a wish list gives relief. I don’t actually know. I also note that when something is on one wish list, it’s on another supply list. Even looking at other school lists now, they’re all over the place. But have you ever been in a Kindergarten classroom? I’ll supply a years worth of paper towels, tissues, and hand sanitizer. Let’s not forget that while the district is telling the teachers they can’t ask for these basics, they’re also not supplying it because we’ve had several years of poor budget management and just had to take a loan to pay summer salaries. I digress; let’s get back on track.

I shopped Target, Walmart, Office Depot, and Amazon. Amazon is actually awful in this area. I need 3 erasers, not 60. Target was working really hard to be competitive, but Walmart won out by a few cents each time (I’m also a Walmart+ member, so my preference is buying there). Last year, Office Depot ran a sale in June that was incredible, but we were so busy that I didn’t think about supplies. Their prices were fine at the end of July, but they were slightly higher than the rest.

So my main order was $84.97 from Walmart. Then I had to order two packages of white cardstock and a wireless mouse through Amazon, which totaled $22. My second needed a new backpack, which was $33. Here are items we are reusing from last year.

This is actually the thing I was most proud of: Ticonderoga pencils. I bought a 96 count of unsharpened pencils last year for $11 (they’re $11.87 this year) (DO NOT SEND UNSHARPENED PENCILS). I sat one night, watching tv, and sharpened them myself. If you purchase a 12 pack of these pencils already sharpened, you will pay more than double per pencil than what I paid. Everyone sees a 12 pack or 2 12 packs are requested, and that’s just what you purchase. If you stop and think, you’ll see that those few dollars will make a difference. So I purchased these last year, sent in what was requested at the beginning of the year, sent in what was requested for this year, and I still have 24 pencils waiting for the next request.

We plan to reuse the pencil boxes from last year, but my mother in law has mentioned she’s getting them new ones. She puts their name on them with Cricut. I said let’s just fix the name on the ones they have, but she had already purchased them. This is $1 I didn’t spend (they’re $0.49 at Walmart).

Each child needs a plastic blue folder and a plastic red folder. They’re plastic and don’t leave the classroom, so after one year, they’re still in excellent condition. This wasn’t about the money, as this saved me $0.92.

Last year, I bought a giant pack of glue sticks. I figured as teachers asked for supplies during the year, I could easily grab and send in. No one ever asked for glue! I was able to provide all requested glue sticks for this year from the left overs. I needed 24 sticks; Target has a 30 pack for $7.49 right now.

We are reusing the headphones they used last year. My son has had the same ones since K and is going into 2nd. Sure, there may be a time that they die and I need to replace them, but there’s no reason to purchase new every year if they’re working. Target has wired headphones for $5. Now here, when I first purchased them, I went cheap because my thought was, “surely these will get broken and I’ll be replacing them constantly, so I’ll stick to $5 for now.” Well, they’re about to enter their 3rd year.

We are reusing my son’s wireless mouse. My daughter didn’t need one last year, so I had to purchase her one. I spent $10. Pro tip: I added the battery to it before I put it in her supply bag; don’t make the teachers add batteries to everyone’s on the first day. 🙂

In the November of last year, my third got into preschool where he was wait listed. Instead of buying him a new backpack, I handed my oldest’s Paw Patrol backpack to him and my oldest got a new one. I purposely had him pick a JanSport because they last. I also purposely had him pick a neutral of some sort so that it’s not a fad that he’ll want to replace in a year. Long story, but he wanted black and that wasn’t unexpected. My daughter picked a $17 clearance backpack at Kohl’s. It was purple and sparkly, and it was so her. We didn’t go shopping for a backpack at the time, but she saw it and wanted it, so I let it happen. Well, it was $17 for a reason, and it barely made it through the school year. I pre-picked 4 or 5 JanSport options during a Target 40% off sale and she picked a pretty, neutral (black with small pink bows) option. With the sale, it came to $33. Again, great that it’s on sale, but the point is that I’m also making an investment in something that’s going to make it through many years, so I would have paid full price if I hadn’t caught the sale.

All in all, had I purchased everything, even down to another backpack, my total would have been $230. And that includes substantial wish list items (e.g., ziploc bags of all sizes, paper towels, tissues, hand sanitizer, all kinds of printer paper and cardstock). I purchased name brand where it was requested – Crayola, Ticonderoga, Elmers, Expo.

Circling back to what made this post idea: I looked up this one person’s supply list. It is about half the size of what I was asked to provide, and I would have spent $39. If I add the wish list items in, it would have been another $36.

People are quick to complain about the cost of things, but they’re not willing to take the time to stop and think. Did you purchase out of convenience? Did you buy name brands where the brand probably doesn’t matter (e.g., a Ziploc sandwich bag doesn’t work any differently or better than a Great Value zipper sandwich bag)? Did you purchase things because it’s on the list without considering reusing items? Did you purchase things that you already have in the house that are adding clutter?

So, if you’re reading this, please realize you have more control than you think.

There’s a lot of chatter online these days about a “90s summer.” I’ve also been fed some reels about what “rich” looks like, and it’s not about money or flashing the perception of money. Mr. ODA and I are working very few hours these days. My job is because I’m a “helper” in life, and I know this group needs my help for a bit longer (I also tried to quit and they said no). Mr. ODA’s job is to qualify for health insurance so we save about $1500 per month in direct expenses for health insurance.

When I first started working, my goal was to climb the ladder. I wanted to be the youngest CFO in my Federal agency. Then a 34 year old woman got the job and crushed my dreams a bit, but I was still a good amount younger than her, so I just needed her to move on in the next few years. Then I went to DC. I left the house between 5:30 am and 6 am, and I got home between 4:30 and 5:30. I kept looking around thinking, “when would I see my kids if I had them?” In fact, we were denied adopting a dog because we both had full time jobs. That still fascinates me. During my fight to climb the ladder in DC, I realized that wasn’t what I wanted. I wanted to live a few miles from work where I could have more free time. I wanted to own a little piece of the pie, so to speak (my job in DC was very high level, but I loved working with the State level where I could actually see the road and bridge projects I approved in progress). But even as I made that transition, it didn’t feel right. I wanted to be home with the kid I was about to spend $30k to have. I didn’t want to put all that money into making a baby for him to sit in daycare for a whole work day and commute time (I get it – it works for people, but not for me).

FIRE. Financial independence, retire early.

While our path didn’t go as we expected as we learned more, and we both worked longer than we intended, the goal was always the same – be home with our family while they’re little. And that’s what we have. Even when I took this new job, I said my kids come first. I didn’t sacrifice in all those ways before kids, give myself freedom, and then take on a full time job. Most people struggle to understand that. Even the agents who I’m paying $600k each year can’t understand when they hear I don’t “need” to work.

So that’s my rich. I’m at the kids’ school all the time. I’m at nearly every drop off and pick up. Heck, I discharged from the hospital AMA so that I could get to a baseball game in May. I will be there. I will be cheering them on. I will lay in bed at bed time, read them books, and then ask them about their day while they tell me the most obscure things…but it’s because they just want to fill that time where they get to talk to me without a sibling interrupting.

I’m not driving a fancy car. I’m not living in a 7000 sf house just because I can. We’re not going out for drinks and sitting at restaurants multiple times per week. We’re not going to the movies every month (umm, actually, or ever, unless it’s the $2 summer flicks series). I’m making my money work for me, so that I can focus on pouring into my kids and enjoying the time of their lives that they actually want to be around me all the time.

Disclaimer: I am not personally making my money do anything. That’s all Mr. ODA. I’m just the bookkeeper, collecting rent and tracking what’s happening and trusting he has the answers on how to move the money around.

Mr. ODA’s retirement account surpassed $1 million last month!

Mr. ODA and I worked for the federal government. Our retirement account is called the Thrift Savings Plan, but it’s essentially a 401k, and includes a 5% salary match on contributions. My parents were adamant that I put at least the amount in to get the full match, and to increase my contributions as I received raises. Mr. ODA entered into my life and said I was to max it out no matter what, and so I did. The point here being he’s maxed it out from the beginning. I worked for about 11.5 years, and he worked for about 16 years. My last contribution was May 2019, and his last contribution was October 2025.

I share this background to make the point about compound growth. The max I could have contributed over my working time was about $190k. The max Mr. ODA could contribute was about $305,000. So that means that based on $305,000 of his own money, he now has a valuation of over $1 million.

In January, I shared why we chose to finance our new (used) car. To those who know us, they would think paying interest would be an immediate no, but there are reasons that it may work in our favor. We also have a mentality that the best decision is the one that makes our money work the hardest, not an overarching thought that debt is bad.

The dealership was offering $1000 off the purchase if we financed. Mr. ODA ran the numbers, and we decided that was worth paying the minimum 4 months of interest. I paid off the loan, so now we have the actual numbers.

Here’s what I had said back in January: The financing was 6.99% and we chose the option that allowed pay off after 4 payments. There was an origination fee of $175, which is rolled into the principle. Our payment is $151.94. The first 4 payments hold $175.07 worth of interest. So we will pay $175.07 of interest and the $175 origination fee as a means of taking $1,000 off the list price. That nets us, including the $30 of credit card rewards, $679.96 less on the list price. After the 4th payment is made in May, we’ll make a lump sum payment of about $7,134 to pay off the loan.

I did not read any prepayment penalty data, but Mr. ODA wasn’t so sure. We made a lump sum payment to bring the balance down to about $2500 in February. What I wasn’t prepared for was that the loan system decided that I didn’t owe any monthly payments for several years at that point. I decided to just go ahead and make my monthly payment a couple more times after that even though it was being applied as principle only and not a monthly payment.

We paid $175 origination fee and $112.49 in interest. So our net save on the final purchase was $712.51. I also included the fact that we made $30 by only financing the bare minimum and putting the rest on a credit card that got us 2% (there was no fee from the dealership to put this on the credit card, which was also a factor in the decision), bringing the net to $742.51 worth of the $1000 off the purchase price. This was better than projection because of the way their loan system applied our lump sum payment.

Several months ago, we went on vacation. While there, we got the kids ice cream from McDonald’s. It was $1.79 each. They had been given multiple “treats” during the day (not of the food variety, but riding the carousel and train at the zoo), and I didn’t see it necessary to spend $10-14 on ice cream after a big day. But it was something that would bring them joy, and it would be a surprise since it’s not a regular occurrence.

Our financial advisor told us that he has a saying in his family, “we can’t afford ice cream.” The statement isn’t meant as a literal statement of “we can’t spend $5 on ice cream because then we won’t be able to pay our necessities.” The statement is meant as a frame of mind. It’s meant to teach an understanding that you need to prioritize your spending and have the big picture in mind.

Treating our kids to the occasional ice cream is ok. Giving them the ability to know that ice cream is not going to happen all the time, but we can get it once in a while shows that we have to prioritize our spending and determine where this ice cream splurge fits in our budget and long term goals.

That comes across with a much higher sense of philosophy than I intend for this example, but the general concept is there. We take the time to determine whether spending money on something is valuable to us and worth the cost.

THE STARBUCKS / CONVENIENCE PAIN

So many people knock the concept of buying or not buying a Starbucks. I see things said all the time like, “I didn’t buy my daily coffee this week, so I’m practically a millionaire.” That density is keeping you in your poor mentality. You think that not purchasing a coffee and getting the instant gratification should yield the instant gratification of wealth. Instead, the point all along was on your mentality. Do you find it a priority to spend $6-8 on a coffee routinely? Perhaps that means you’re also thinking you can treat yourself to that new shirt, new shoes. Perhaps that means that you’re also willing to walk into a convenience store, like at the gas station, and buy a soda or an energy drink.

I also think back to a friend who would leave their house to go get a gatorade at the gas station down the road. They once left their house while we were there, bought 3 gatorades, and came home to play a game with us. This was routine. What if you went to the store and bought a case of gatorade? You’d have a cold drink that you want in your fridge on demand, you wouldn’t be taking the time to leave your house, you wouldn’t be spending money on gas, you wouldn’t be adding to the wear and tear on your vehicle (which eventually costs literal money), and you wouldn’t be paying a premium for the same drink.

A quick search tells me I could buy a 28 oz Gatorade for $3.69. I can buy a 12 count of 12 ounce Gatorades at the store for $7.98. In a given sitting, do you really want 28 ounces or can you get by with 12 ounces? Even if you want more and want to drink 2 Gatorades in one sitting, it would cost you $1.26 to have two of them at the ready in your refrigerator.

I recently was behind someone on a drive down a two-lane road. They were going 35 in a 45, in a car that had plastic as the driver side window, half the bumper missing, the passenger mirror missing, and a tail light busted out. They finally got out of my way at the gas station, where I watched them park in a spot and walk into the store.

STOP AND THINK

People don’t think about how that small decision can snowball. You’ve been trained through social media to think that you have “earned” a “treat.” Marketing by these companies tell you that it’s not a big deal to spend your money this way. Be stronger. Think about the decision. Take just one month to physically write down everything you spend. Yes, I mean take a pen and paper, write where you spent money and the amount. Categorize the spending. See if you can find just how much money went somewhere that could have cost you less or was unnecessary. I bet you’ll find at least $100 that was spent unintentionally, and it’s very likely more than that.

The TREAT for yourself is being more financially secure. It’s having the money for the necessities. It’s being ready for an emergency, but still being able to make your mortgage/rent/utility payment.

We last purchased a rental property in 2022, after most of our purchasing was done in the the 2019 era. We were busy with 3 kids, and I recently felt like I was coming out of the fog. Mr. ODA and I went to a wealth building seminar in the Spring; my intention was to have that seminar reinvigorate our desire to build our portfolio. It worked well for Mr. ODA, but once options started to show up, I started to panic.

We first went to an open house. It was a bit further away that I’d prefer to maintain a house, and there were a few red flags. For one, it frustrates me that landlords can fill out a seller disclosure claiming they know nothing about the house. I can tell you if I had any roof issues or major system issues in any of my houses, even though I haven’t physically lived there. Mr. ODA wanted to pursue it, but I couldn’t bring myself to get on board.

We were then sitting with his parents one night, telling the story of this open house, and his mom said that she saw a townhouse posted on Facebook that she thought we’d be interested in. It was owned by the son of an old friend of her’s. We asked our real estate agent if she’d show it to us, but she was out of town. So then his mom texted her friend to see if they were there and we could go look. They weren’t there, but they gave us the contractor box code (which is surprising in itself that there wasn’t a sentribox on the door). We went over and the house looked to be in good order, so we put an offer in. We like to surprise our agent with these types of things where all she needs to do is get the contract ratified.

UNDER CONTRACT

The house had been listed for some time when we came across it. It was was listed at $182,500. We offered $182,000 with $2,000 worth of seller subsidy on September 2, 2025. They agreed that day. We ended up needing to redo the contract because the wife wasn’t on the deed of the house, but she had signed the contract, but that wasn’t a big deal.

We had the inspection scheduled for September 10th. There was hardly any issues in the report, and we picked a few of the bigger things to ask for them to fix. They agreed to our list. They gave our agent a receipt showing they had paid someone to fix the items on our list. We did our final walk through the afternoon before closing and were disappointed to find that two of the bigger items (leaks) were not addressed properly and the house was dirty (including things left in the fridge and freezer). Our agent reported that to their agent, and they addressed everything that evening. We swung by the next morning before closing to see it all cleaned up and the leaks addressed.

The appraisal was ordered by our lender and came back at $188,000. That was a pleasant surprise to see we had immediate equity in it.

COMMERCIAL LOAN

We chose to go a commercial loan route. Interest rates aren’t falling as quickly as we expected to see. We have a commercial loan on one of our other properties in town, and I was still surprised to see how easy this process is. The loan qualifications are mostly based on the cash flow of the property. I filled out an application, submitted a ledger of our other property cash flows, and sent in 3 years worth of tax returns.

We were quoted at 6.74% interest. The loan terms are a bit different. Our last commercial loan was amortized over 25 years, but there’s a balloon at 5 years. This time around, it’s amortized over 25 years, but the balloon is at 15 years. A commercial loan also means that the taxes and insurance are not escrowed, and I’m responsible for paying them on my own.

The loan is an Adjustable Rate Mortgage (ARM) too. There was no different to us in the 3 year or 5 year ARM, so for the first time, we picked a 3 year ARM. In the past, it was related to securing our low rate. This time around, we’re expecting rates to drop in the near future, so we locked in our rate for only 3 years. It only changes on 3 year increments (some of the others will change every year after the initial lock period). It also has a clause that indicates the rate has a floor of 4%. I also don’t see a maximum adjustment that can happen (we have other ARMs that state an adjustment can’t be more than 2% at the change date).

We were expected to put 25% down. That would be $45,500 based on the $182,000 purchase price, and would leave 136,500 worth of a loan. They ran some numbers and determined that we could only qualify for a loan of $132,000 based on a rent of $1,400. They only us the cash flow to determine the eligible amount and not the rest of our portfolio. Let’s break that down to the fact that a loan of $136,500 equates to a monthly loan payment of 942.23, and a loan of $132,000 equates to a monthly payment of 911.17. So at a rent rate of $1,400, we could cover the monthly payment of $911.17, but we could not cover a monthly payment $31.06 higher. We pushed back for a second, but in the end it didn’t matter and we accepted the loan of $132,000.

PROS

When I look at this place, it feels like a place someone will rent. It’s clean, feels like home, and has a good layout. It has a closet available for a washer and dryer, which is a plus. Both bedrooms are upstairs and each has its own bathroom, and there’s a powder room on the main floor. It’s more secluded than other units in the complex, giving the occupant more grass area to hang out in the front and back.

CONS

We do have some concerns. The townhouse is at the back of the neighborhood. The entire rest of the community has parking right outside their front door. This group of 4 townhomes is separated from the parking lot, so you have to walk a bit further. The trade off there is that it’s secluded, you have a front “yard” (instead of pavement), and you’re more secluded from your neighbors.

I didn’t want another townhouse in our portfolio. With a townhouse, your value is strongly dictated by what your neighbors have done (or not done) to the property. As much as we don’t plan to resell these properties in a short time frame, I do have the thought that I want to be able to sell it when the time comes.

Also with a townhouse, you’re also at the whim of a community manager that is likely not putting utmost effort in. We asked about the HOA at closing and the previous owner said the cost used to be $35 per month. When it was that cheap, they weren’t paying their bills, so the lawn wasn’t mowed and the trash wasn’t removed. They increased the price to $95 two or three years ago, and that has made a difference in the community’s upkeep.

The HOA is due monthly, which is an inconvenience and a surprising process on their part. I plan to pay it monthly until I have confidence in their ability to process my payment and apply it to my account timely. After some time, I may pay in advance. I just went to process the first payment and planned to pay 3 months worth, but then realized that will create a harder tracking mechanism on me right now.

CLOSING

We had our closing on October 16th. It was super quick and easy. I listed the house for rent that evening.

SUMMARY

At this point, we have the house listed for rent at $1375. We had determined the range for rent during our purchase evaluation. Unfortunately, I hadn’t looked at the current market by the time we went to list, and there’s quite a bit out there. I’ve shown it to 2 people and have another showing today. One of the people from the weekend said they were seeing other places on Wednesday, so I’ll hold out on any changes to the rent price until this weekend.

After each trip, I typically summarize how much it cost us. I like talking about money, mostly to work towards eliminating the stigma about talking about money. The more information you have, the better informed you are when it comes to decisions, so here’s a reference point to file away. We sailed Royal Caribbean’s Oasis of the Seas. I loved it!

COST BREAKDOWN

Flights – 25,000 miles + $273 We looked at several different flight options now that we’re a family of 5 flying and that adds up quickly. The first night we were looking to book the cruise, there was a group of 5 tickets for just under $700, which we thought was a great deal, but once we were ready to book, it wasn’t there anymore. We ended up going with Frontier for one direction and using American Airline miles for the other direction. When booking with miles, you only need to pay the taxes on it, so that’s what we did.

The flight options were very limited for the way home. We ended up just sucking it up and picking a 9 pm departure. Not long after the booking, we received an email saying our itinerary was changed and now the departure is 12 pm. While that seemed concerning at first – to get off the cruise, through the airport, and to our gate before noon – I had hoped it would be just fine, and it was. We got off the ship around 8:30, took an Uber to the airport, and arrived too early to check in for our flight. They built the airport expecting this isssue, so they sent us to the waiting room. We sat there for about 45 minutes and then checked our bags and got to our gate. We sat at our gate for a couple of hours and got home on time.

On the way down, we each got a checked bag because of our American credit card. However, we still needed to prepare for “carry on” status on the way home with Frontier. Then, once we were already packed, Frontier offered us to upgrade all our bags to checked bags. Had I trusted that they wouldn’t have said “no, you have to check a carry on size,” I would have happily changed our 3 carry on bags to one big bag to make traveling through places with 3 kids easier. So while some parts were harder because we had 3 rolling suitcases to account for, it was nicer through the airport to not have suitcases to manage.

Hotel – 34,000 points If you’ve ever had to fly into a cruise port, you know it’s less stress-inducing to fly in the day before. I went on a cruise a year and a half ago, and we were flying out during a snow storm that was affecting travel all over the area. We ended up arriving at our hotel near midnight, so we were happy to know we were there for the cruise boarding time and not stressing about delays that morning. That means there’s a cost for a hotel one night.

The hotel was booked with points, so it wasn’t a literal cost to us. We stayed at the Tru in Dania Beach. They had a shuttle from the airport to the hotel, so when we arrived, Mr. ODA called the hotel to come pick us up, and it worked out well. We had to wait 20 minutes for a crib to arrive, even though it was on our reservation as a request. This isn’t a huge deal, but when it’s 10 pm and I’m just setting up a crib to get over tired kids to sleep, I’m not thrilled. Otherwise, the hotel was nice and it provided a good breakfast.

Uber – $58; Airport Parking – $70; Dog – $289 The hotel provided a shuttle from the airport to the hotel, so we didn’t have to pay for that part. Then we needed an Uber from the hotel to the port, and then from the port to the airport. We requested a car seat in the Uber on the way to the port, so that limited our options. Then she was 23 minutes late to our pick up time, didn’t get out of the car to greet us or help set up the car (pick up the 3rd row to fit our 5th passenger we disclosed ahead of time), didn’t acknowledge being late, and generally didn’t speak to us except to say get our IDs out for the port. That’s not an Uber issue, it’s a specific driver issue, but that was not a great experience. On our way from the port to the airport after our cruise, we got charged a wait fee, even though the wait was because security was stopping our Uber from getting to us. Uber removed that charge though.

The CVG airport parking is $10/day for economy. That’s my first economy experience instead of the ValuPark lot, which is $12/day. I didn’t really think anything of it, but it wasn’t a great experience. I always thought it odd that the ValuPark lot has shuttles that pick you up at exactly your car, but the economy lot has the shelters. I didn’t properly account for the time to wait for the shuttle and then to have the shuttle drive through all the shelters.

Food – $44 Obviously most of the food was part of our cruise fare. We had McDonalds on the way to the airport, Burger King during our layover, and then McDonalds on the way home.

Cruise – $3,099 The big one! We did not prepay gratuities, so that was billed as we left the ship. Gratuities are $18.50, per person, per day. We had $50 on board credit. Ironically, and just coincidentally, we spent $50.40 between drinks and child care (the babies room (0-3 years old) is $6 per house before 7 pm and $8 per hour after). Royal Caribbean only requires $100 per person as the deposit, and then the balance is due a few months before the cruise departure. We booked right at that threshold, so we paid our deposit and then a few days later paid the balance.

LOGISTICS

The booking of the cruise could have been a bit more forward. Cruises are not family-of-5-friendly. There’s an option on Royal Caribbean to book a “guarantee” or GTY room. You get a discount for allowing them to assign you in an open room (of the category you picked (e.g., interior, ocean view balcony)) about a week before the departure. I did this for a cruise I took in January 2024, and it worked out perfectly fine. So we see these prices quoted online for GTY rooms, but they always make you call to book for more than 4 people. We’re expecting the cost to be just the taxes and port fees for the 5th person, but when we call, the difference is over $500.

We tried to explain how that feels like a bait and switch and that there’s no indication of that on the website, and they basically said “well, that’s the way it goes.” They can’t guarantee a 5+ room available at the time of sailing. This makes sense, but it also eliminates our ability to use that cheaper booking option. We asked if there was something they could do to help make us feel whole since we were being forced to spend $500 more than if we could be put into the guarantee-pool, and they gave us $50 on board credit.

Mr. ODA’s parents book Celebrity (same parent company) all the time, and if they book their next cruise while on their current cruise, they are given OBC. Turns out Royal Caribbean doesn’t have the same philosophy, and they hardly give OBC. We tried to see if there was a special deal for a cruise if we book on the ship and they had nothing to offer.

Our departure experience was horrific, and I’m not even sure how we timed everything so poorly. At CVG, the kiosk jammed printing our tags, so we had to wait in line to get to the counter for the last luggage tag. Well, the line took forever because there was a large group in front of us that couldn’t speak English, so the workers couldn’t get everyone checked in quickly. Then we were too late for her to print checked bag tags because it was 30 minutes before the flight. So now we’re stressed trying to get through her attitude, us being late, and having to get through security and run through an airport with 3 little kids. This is the first time I’ve ran to my initial flight (ran for connections countless times!). I’ve never had this issue before, but everything along the way took just a few more minutes than I had planned for, and the luggage tag issue stole about 15 minutes of time from us (plus, our flight was delayed by 20 minutes and then 45 minutes before the original flight time, they said it was on time… we hadn’t delayed our departure from home, but it was wiggle room we thought we had and then suddenly didn’t). After the attitude from the ticket counter, then we encountered two more attitudes from the gate agents. It was a rough start, but the flight attendants were nice, and we had plenty of time to catch our breath at our connection.

Child care is provided on the ship. They have a few hours in the morning (maybe 9-12?), then 1-5 for the afternoon, and then 7-1 am. For the kids 3-12 (split between two rooms of 3-5 year olds and 6-12 year olds), it’s free until 10 pm; then it’s $10 per hour per kid after 10 pm. For the babies (0-3 years old), you need to make a reservation for times when you arrive on the boat. We prioritized the buffet, so by the time we got to the kids area, lots of time slots were booked already. She offered me 6 hours worth of booking, which I split between 3 days. Our youngest is 7 weeks shy of being 3, but he wasn’t 100% potty trained (although we did try) so they wouldn’t let him move up. If he was potty trained, they would have let him go up to the 3-5 room. The first 2 hour block, we only used 1.5 hours worth of it based on the activities we were trying to get done. The second 2 hour block, we only used 1 hour worth. And then we didn’t use our final day worth of time because he got sick, and I didn’t want to contribute to the spread of it. We dropped the big kids off a few times and just took the baby with us to activities, which worked out fine. He’s so good when he’s alone, but the 3 kids feed off each other!

I brought lots of hook magnets. I used them to hang everyone’s lanyards with their seapass cards, hats, and to dry bathing suits. I also used them to hang from the ceiling and utilize curtains that I brought (actually, I bring these curtains everywhere we travel because a really dark room is important to getting the kids to sleep past sunrise when bed time is 2-4 hours later than usual). There were 2 hooks in the shower, 3 hooks on the bathroom door, 2 hooks in the bathroom with 2 towel bars, and 2 hooks outside the bathroom. We’re going on another cruise next year, and I’m going to bring more hooks because we could have used more space to dry out bathing suits. Having the curtains hanging to separate the kids from each other and then from us was great.

I also bought a pack of decorative magnets. This is very unlike me; I don’t like anything extra. But I put them on the stateroom door, and it helped the kids identify which one was ours. The door is textured, so they didn’t all fit. I put them inside the cabin on this big blank wall, and I actually really appreciated the decoration.

You’re allowed to bring on 12 cans/bottles that are less than 17 ounces each, so we did that for Mr. ODA’s sodas. We didn’t buy any drink packages. I don’t know what sodas cost on the ship. At the buffet, we have lemonade, iced tea, and water available. At some of the included restaurants, they have other flavored water type drinks like strawberry melon. At breakfast they had apple juice and orange juice. There are enough options for variety if you’re not looking to buy a package. I had Mr. ODA bring a non-diet/zero type drink in case I wanted some variety, but I was so full that I didn’t end up wanting any sodas and had a couple of lemonade and juice options throughout the week. The alcoholic mixed drinks are about $15 a la carte. They offer a happy hour special of margarita (and maybe one other option that’s $6-7) and have a drink of the day that’s $8. I didn’t know about the drink of the day special until day 3 and didn’t know about it at all on my last trip, so that’s a positive to know. I think the Truly/beer type option was around $8-9 each.

When buying the drink package, that’s your baseline. Are you going to drink 5 mixed drinks or 8 beers/Truly each day to make paying up front worth it? I’ve heard some people say “I just like not having to think about what I’m ordering.” But, do you enjoy paying $65 for 2 drinks? I understand it’s vacation and many people have the mentality that money is no object, but it is something to pause, have the perspective, and make an informed decision on.

The app is really good. There’s a little room for improvement, but everything you need is there. We’d like to see a search feature, where you can search “bingo” or “laser tag” and see the offerings instead of scrolling every day and hoping you catch the times. I like the daily tips they post about what’s happening that day and some good reminders. I also like how many activities are offered. I wish there were a few more things in the 6-8 timeframe for those with a 5:00 dining time, but I understand that’s not the worst problem. There is so much offered for other times, and I found myself juggling wanting to do all the things, but also not wanting to be on a schedule.

A few weeks before your cruise, the app will have most of the shows and activities available. One example that we didn’t have until we were on the ship was laser tag’s schedule. But you should get on your app a month in advance and keep checking for the show reservations to be opened. They seats go fast. We were able to reserve the ice skating show and Cats, but we weren’t able to get a seat at the aqua show. I was really bummed about that, but we went to the aqua theater at the beginning of the show and were able to get a seat.

We did not pay for a wifi package, nor did we set up our phones for an international plan. I was looking forward to being completely cut off from the world for 4.5 days. To my surprise, iMessage worked the whole trip. It wasn’t too bad, and I got to share stories as we went with some people.

LESSONS LEARNED

Book any 0-3 year old child care slots ASAP

Pack half the pajamas you need (our kids wear pajamas through breakfast at home, so there’s no re-wearing, but they don’t eat anything in the cabin, and they don’t leave the cabin once in pajamas, so don’t use up the space)

Prepare accordingly for theme nights (I may have not planned well for my oldest)

Bring as many magnets as you can hold (although you may get flagged for a bag check in security)

Read the daily tidbits in the app each morning

Don’t pack lots of snacks (I thought I’d be looking for breakfast faster than everyone being ready to go, so I packed granola bars. I also thought we’d want more snacks, but we’re so full from eating bigger meals and being on a different type of meal schedule that eating in the room was never a thought)

If you’re on the cusp of 52″, 48″, age 3, or age 6, I may wait until those milestones are hit. While it’s not the end of the world and doesn’t kill your cruise, we had kids disappointed they couldn’t do some things based on height (water slides) or age (rock climbing).

Drink the happy hour or daily special beverages if you don’t have the drink package

THE CRUISE

We took a 5-night cruise. It was more time than I had planned for originally. I didn’t want to be stuck on a boat in case the kids didn’t take to sailing well, but the price was $1000 less than the 3-4 night offerings, so we went for it. It worked out well. Everyone’s first question seems to be, “were you afraid of them going overboard?” Turns out, there are very limited options for that to even occur. We were in an ocean view balcony, but the glass goes higher than the littlest ones, so that wasn’t an issue. Most decks have the staterooms on the outside, so the only real place they could attempt to get overboard is on decks 15 and 16, and a little spot by rock climbing on deck 7. It was barely a thought of mine the whole week.

The biggest hurdle of the week was getting the kids through crowds. There’s a lot of people on the boat, and people tend to congregate in certain areas. Keeping 3 little ducklings together in a crowd could have been worse, but it wasn’t the easiest either. The cruise ship gives you bracelets for your kid to wear with their muster station on it. I wish there was more information on it, so I put their names and room number on the back. The youngest didn’t have a yellow bracelet, and I wasn’t happy about that. Luckily, I had packed a bracelet that I could put his information on. I used a regular sharpie and the lettering was legible until about the last day. I could have rewrote the information, but by then I was feeling more comfortable.

We did not push too hard to get to all the activities. We made a concerted effort for a few activities, but I didn’t want to be tied to an agenda all week. We generally started the day with breakfast. We ate in the main dining room twice, which was quieter and calmer, but also slower. One morning, I ordered a small breakfast, and the waiter pushed me to get the “express” breakfast. It came with 2 things I didn’t want, and I was frustrated that he pushed me to waste food. We usually then went to the pool or splash area (the splash pad is pretty cool with slides and activities within it for the kids). Ice cream opened at 11:30, so that worked well as a way to get out of the pool and start drying off for lunch. We ate lunch in the buffet (Windjammer). I personally liked the variety of options with the kids, but it wasn’t the easiest process. Apparently kids really struggle holding plates flat. We only lost one apple once, but it was stressful every time trying to make sure they kept the food on the plate while walking. Our afternoon was spent either with the kids in the kids club area (Adventure Ocean) while we did trivia, or they came to trivia with us. We rode the carousel, the big slide (Abyss), and participated in some random activities (family festival, scavenger hunt). We would get back to the room at about 4:55, rush to change, and then run to the main dining room for our 5:00 dinner. On my last cruise, there were only 2 dinner times, so being on time seemed less of a priority. This sailing had a 5:00, 6:45, and 8:00, so I felt the push to be as close to 5:00 as possible so we didn’t delay a 6:45 sitting. We ate all our dinners in the main dining room. I truly appreciated the themes, but perhaps only 50-60% actually participated.

At Cozumel, we got off the boat, had a beer at a tourist trap, and got back on the boat. I don’t think we were off the boat a full hour. There was swimming available in some pretty water just next to the cruise ships. There are shops for trinkets and a few places to eat or drink. It was an area that clearly catered to cruise ships and I felt perfectly safe.

Our second stop was Royal Caribbean’s island, CocoCay. I can’t sing enough praises about this concept. All your food is available. There are servers just like on the boat if you want a drink. It’s clean. There were some concerns about jellyfish while we were there, but we didn’t have any problems. My youngest was struggling with the sand concept (and not touching the sand and then rubbing his eyes or sucking his thumb), so we eventually moved over to the pool. The pool was packed, and I almost said lets just go, but we got in. Once you were in, it wasn’t uncomfortable at all, and there was plenty of room. There’s a 0 entry area with water fountains, which kept the kids entertained well. There are life vests on the island for your little swimmers. I did hear that snorkeling was sold out when we arrived around 10, so you could keep that timing in mind. The ship staff give you towels as you get off the boat (you sign them out with your seapass card), and there are towel stands on the island if you want to swap out your wet, sandy towel for a new one.

I will note that we had a medical emergency just hours into the cruise. It didn’t affect us at all. We heard the “alpha alpha alpha” call while we were at dinner, and about an hour later, the captain came on the loud speakers and announced the plan. We departed Ft. Lauderdale, but we were going to return to Miami to get this patient off the ship. They were making a plan on whether we’d have to fully dock or if the coast guard could come out to us. They announced a bit of time later that they decided the coast guard could come out. Then about a half hour after that, they said that the swells from the tropical storm we were near were too rough and the coast guard couldn’t get close to our ship to safely transport the patient between the two boats. So then they decided to send out a helicopter, and that happened just as the sky opened up on us at the aqua theater and we gave up and went to bed. So even though the course changed, it really didn’t affect anything we were doing on the ship. The patient actually got off and received emergency coronary bypass surgery that night and was recovering, so that was a blessing. There was also supposedly a death in another cabin, which I knew nothing about until after I got back home. I share this just to say – things happen, and there’s so many people, so it’s not surprising, and it didn’t affect the rest of the trip.

Getting on the ship and off the ship on the bookends of our cruise was extremely easy. I had a similarly easy experience at Cape Canaveral (actually probably easier). On the way there, we went through the security check points. I was flagged for my magnets, and in the process, they found my extension cord. Honestly, it wasn’t clear what the rules were about the extension cords. I wasn’t worried about the number of plugs as much as I was the extension to an outlet. They’re quick to say “there are plenty of outlets,” but they don’t address the fact that 3 outlets are on one end of the room and there’s only 1 at the bed. It didn’t matter though. We plugged in a phone overnight by the bed, and the sound machine was over by the kids with that 3 outlet option on the desk. They confiscated my extension cord, but they tagged it, and I got it back at the end of the cruise. After that, we went upstairs to a huge waiting room. We were told to sit in order as we entered. The place was packed; I expected this to take a while. It was less than 2 minutes. We scanned our boarding passes and walked right on. On the way off, everyone just left when they were ready. We walked right into the main dining room, scanned our seapass cards, and left the ship. There was luggage areas to pick up any luggage you had carried off the ship overnight, but we hadn’t done that. Then you go through the immigration check where they take your picture and approve you to continue. And that’s it. There was no queuing through either process except for the 2 minutes we sat in the waiting area at the port on the way on the ship. It’s incredible to me.

SUMMARY

I was a reasonable level of nervous taking 3 young kids on a cruise for 5 nights, but it went significantly better than I expected. Our next cruise isn’t until this time next year, but I wish it were sooner! I highly recommend cruising, especially with Royal Caribbean.

We bought a Tesla. In the process, they’re offering a 0% APR promotion. They let you see how your credit rating affects your monthly payment (through different APRs). The final column in the table below shows the increase each level adds from the previous level.

This is based on a 60 month term. So, ignoring the promotional option available, between the ‘>720’ and ‘680-720’ would cost you $39 per month. That’s a total of $2,340 over the loan term. By using the promotional rate, that’s $88 per month “saved,” which is $5,280. Don’t let it be lost that working on your credit history and credit worthiness is something that pays off into the future.

When we look into a large sum of money leaving our account, we consider the “net present value” of the dollars. The net present value is the difference between the present value of cash inflows and the present value of cash outflows over a period of time. Investopedia uses the following over-simplified example. “An investor could receive $100 today or a year from now. Most investors would not be willing to postpone receiving $100 today. However, what if an investor could choose to receive $100 today or $105 in one year? The 5% rate of return might be worthwhile if comparable investments of equal risk offered less over the same period.”

The 0% interest loan through Tesla is for about $40,000. Mr. ODA calculated that our net present value of money, based on our approximately 4% savings interest rate, is $36,017. Taking nearly $40k out of our savings account wouldn’t be a financial problem, but it’s not the smartest financial move in our portfolio. Instead, we’re going to pay about $580 per month, while the “balance” of that $40k earns interest. At 4% interest, the balance of $40k earns nearly $1,000 in a year. That balance will continue to dwindle, therefore lowering the interest earned each year, but it’s still a significant sum of money. In the first few years, the interest earned is essentially paying a couple of months worth of the car payment.

By being conscious of our financial standing in the world, we’ve set ourselves up for earning these promotions. Had our credit worthiness been below a score of 720, it would have cost us over $5k more over those 5 years of the loan. While I understand that purchasing a Tesla may be considered a luxury, this concept and awareness can be applied across all financial decisions, which is why I wanted to highlight it here.

When I was little, we had friends come to our house a lot. When a certain crew came, they raided the candy drawer like they hadn’t eaten in a week. It was quite a binge. It’s because there was no candy in their house. They were fed 3 small meals each day, and that was it. They had the mentality that they needed to get everything they could in a small period of time. Because they hadn’t been taught self-regulation by having regular access to things, they didn’t understand moderation.

To me, I had access to the candy drawer in my house whenever I wanted. Therefore, it wasn’t exciting to me. It was there if I wanted something here and there, but it wasn’t something I felt the need to covet. I do the same with my kids. They have full access to the pantry. They know the things that are “good” for you, and they know they can take that without asking. They do ask if they can have any of the treats in there, and unless it’s close to a meal time, I try to give more “yes” responses than denials (and my denials always come with a reason).

I use this story regularly in my life it seems. It seems focused on a healthy relationship with food, but it’s really an overall concept of understanding the mentality it takes to make informed and beneficial decisions all day, everyday.

DELAYED GRATIFICATION

We did a stent with a multilevel marketing company. They preached “delayed gratification.” It was meant to say that you shouldn’t spend now because you’re going to produce a significant amount of income in the future, and you’ll be able to spend greatly at that point. Unfortunately, Mr. ODA and I are too cynical to watch that unfold. We took note of every “extra” our “upline” spent that wasn’t hitting that mark.

They who would go on a big trip with the statement, “well it’s ok because it’s for my birthday” or “it’s ok because it’s the last big trip that I’m going to take with my mom.” There was always another trip. Or the big, fancy, rent out a space, decorate to the nines, buy a new outfit, birthday party that happened almost annually. There were excuses to justify these actions that were clearly against their “delayed gratification” preaching, but they thought it was ok because they were “debt free.” They didn’t buy a house, continuing to throw money to rent year after year so that they wouldn’t have a mortgage.

There was a guise of having a “big picture” mentality, but the execution of the financials didn’t add up to us. If you were really in delayed gratification mode, the $3,000 you spent on a trip could have been saved towards a 20% down payment on a house at 2.5% interest rate. That’s what Mr. ODA and I did when we had to pay for a wedding and buy a house in the same year. We set a goal to spend no more than $5 per person, per day on food. We didn’t eat at restaurants. We didn’t go on huge trips (although we did do some weekend trips to visit family). Because of those years of ‘pain’ we went through, we bought a house with no mortgage insurance, and that house turned into 4 houses when we sold it.

I digressed. The point here was that creating a mentality of “delayed gratification” is setting yourself up for failure. If you created a habit of proper spending and a mentality of being able to discern whether the cost of something is worth it to you and your goals in real time, there wouldn’t be these “slip ups” of wanting to take that big trip or wanting to fill a void by throwing a lavish party.

In February, I started a diet. I was working out for a year at that point (after having our 3rd baby), and the number on the scale was exactly the same. I felt better, but I wanted that number to go down. I started reading up on diets, and this concept I found clicked with me. If you commit to a diet that is really restrictive, you’re going to fail. If you can’t have any carbs, then you end up having a binge day to make up for that desire. The concept of depriving yourself of something is more thought-consuming than if you had taught yourself moderation.

This diet concept was to alter your eating each day so that it keeps your metabolism on its toes. One day, eat a lot of protein. The next day, eat your carbs. Go back and forth. I was consistent on this for 3 months (see, best laid plans fail – between end of school things and travel, I haven’t put the effort in), and I lost 17 pounds with little effort. I haven’t been paying attention to this eating pattern, and I’ve been stagnant again. The whole point was that if you deprive yourself of something you want, then it’s going to consume you and make you unhappy. But if you eat in a thoughtful manner, then you’re happier and have an easier time reaching a goal and sticking with it.

RIPPLES

The decisions you make today affect tomorrow. The habit formed by thinking you had a hard day and deserve a “treat,” or that “it’s vacation so we should each have a $10 ice cream at the amusement park,” have ripple effects. I have another post about how people make fun of those who say don’t spend $5 on coffee everyday if you want a better life. Most people see it as a literal $5 per day (granted, it’s more like $7 or $8 at this point), do the math, and then say sarcastically “wow I’m a millionaire.” No, it’s the mentality. It’s the concept of teaching yourself that you don’t need to purchase an expensive coffee everyday, or you don’t need to buy lunch everyday at work, or you don’t need to overspend on treats once per week.

Someone once made fun of us because we like to go exploring new towns and find hikes, while his family goes to Disney at least once per year. I’d venture to say that our trips, where we spend time with our family and learn about new places and things, are more stimulating. I don’t hate Disney (Mr. ODA does though 😉 ), but I don’t see it as something to go to every year with no other experiences. But our trips that end up costing about $1,000 allow us to go do more things. We can do more activities when home, we can go on more trips, we can put money into savings accounts for our kids.

This summer, we have plans to be in 7 states outside of our home state. My kids are extremely happy with just the concept of staying in a hotel or “vacation house.” Add in swimming in a pool somewhere, and they’re ecstatic. I don’t have a desire to teach them that vacation is when you get to eat everything you see and buy whatever trinket you want. If you intentionally spend throughout the year, you end up with things that are more valuable to you than if you buy several trinkets just because you’re on vacation (really – when was the last time your kid played with that light up spinny stick from Disney on Ice). I want to teach them the value of their time, their money, and their family. I want to try my hardest to set them up for success because they understand the value of things in the big picture, and not just the instant gratification that lasts for a couple of days because they go that little toy we walked by.

The rentals were expensive this month with $4600 paid out. This doesn’t include work that’s currently under way, but not paid for yet.

I paid for a water heater replacement, which was $1,904. I had to pay insurance on a larger property ($793). I paid the balance of the window replacement at one property, which was $1,064. I also paid for a plumber to address a leaking toilet and a rotted faucet ($325). We had a new tenant move into a vacant property, so we had that cleaned before her arrival ($165).

I had to pay for a plumber’s service call ($95) for clogged drains, for them to refer me to a rooter company ($250). I emailed that tenant that preventive measures need to be taken because I’ve not had so many calls to one property. She assured me they have taken appropriate measures and it’s just old pipes. The only problem being that we have several other properties with old pipes that never call for clogs.

We’ve turned over two properties and are about to turnover another property in the dead of winter. It’s so frustrating to be in such a position. All of those stories will be elaborated on in future posts. – On one property, we charged a lease break fee of one month’s rent to cover our losses (the fee was different based on the month in which they broke the lease). Luckily, that covered our entire month of January being vacant, but we found someone for 2/1. – Another tenant asked to leave a property because he lost his job. That was handled a bit different because we didn’t know in advance that this tenant would want to leave mid-lease. We told them there’s a fee of $250 (which is what it costs us to pay the property manager to find a new tenant), and that they had to pay rent until we found a new tenant. We didn’t lose any rent on that property. – Now, we have a newly vacant property because the tenant can no longer afford it. I’m not expecting to recover her unpaid rent at this point. We approved a tenant to start 2/28, leaving us with 27 days of lost rent. However, we sent a lease over for them to sign. They’re currently dragging their feet on signing because they want to pay with their tax return. I don’t love that idea. They’ve been easy to communicate with up until this point, just slow. I’m hoping this gamble works out.

PERSONAL FINANCES

I had to transfer money to Mr. ODA’s account to cover the purchase of our new back door and a new treadmill (although that was only $400). This is an interesting concept for us. Mr. ODA had an account before we met. His account was grandfathered in to new terms and conditions at this bank. He’s kept his checking account and credit card for the rewards (I have access to the account; my name just isn’t on it). Any online purchases go on that credit card. However, that account only receives $250 every other week from Mr. ODA’s pay check (occasionally it’ll receive rent via Zelle). So sometimes, we need to transfer money from our main checking account to cover that credit card payment. All our security deposit accounts are with that bank too. So I had to then transfer from a security deposit account into his checking account, and then have him send that money to our main account. It wasn’t our finest money management moment.

Not much else happened this past month. We’ve gone skiing with the kids some more, I went on a moms’ cruise (which was amazing), took a small trip to piggyback Mr. ODA’s work trip, and have done activities around town. We’re gearing up for a procedure at a local children’s hospital next week, which I’m expecting will wipe out our deductible. Luckily that’s only $3,000, but I’m sure we’ll hit it. We’ll actually be late hitting it this year; it’s usually done in January.

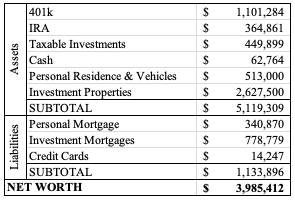

NET WORTH

One of this year’s goal is to hit $4 million net worth. I thought it was going to be a ways away, but the market has been up big recently. We’re only about $14k away from that goal now!