Before I get into an update, I have a quick perspective moment. Our preschool has a 3.5% processing fee to pay monthly tuition online. Tuition is $265, so the processing fee comes to $9.27. If I paid it online instead of writing a check each month, that would be an extra $83.43 I paid for basically nothing. For perspective, I spent $82 on a grocery run of essentials (e.g., dog food, paper towels, milk, eggs, etc).

RENTALS

I had to give notice to one household by 1/31 if I were to raise rent. Their lease ends 3/31, and that will mark 3 years with me. I was panicking because it’s our most expensive house (it’s also our nicest and biggest, and it’s fairly close to downtown). Rent has been $1750 for the last 4 years. Last year I missed the notification to raise it because a January deadline surprised me, but this year I put it on my calendar for January 1st to do. And then I dragged that calendar reminder through the whole month, only needing to then set an alarm to make sure I did it at 8pm on the 31st. I raised it to $1800 and they accepted within the hour. Phew. They’ve been late three times in 4 years and clearly communicated what was happening each time. We’ve had two major issues at the house that they rolled up their sleeves and helped mitigate the damage before the tech could get out there. They’re just really great tenants.

I had two tenants pay rent before the 1st and one partially pay before. That was surprising since the last two months I’ve had very late payments come through. I still have one person with a partial payment outstanding as of this morning.

We had a water heater go out on Thursday in one property, but otherwise I’m counting all my blessings that we made it through 2 weeks of below freezing without incident.

PERSONAL

I’ve preached monitoring your spending by writing it down for years, but I hadn’t done it. I had done it a few times retroactively, but I never made the time to keep on top of it to make pivots. With Mr. ODA leaving his career, that’s a high six-figure income that we’re without now. I’m working part time, but that’s basically a one-to-one ratio of income to health insurance. I’ve calculated that we need to be about $1350 per month in spending outside of the mandatory bills (e.g., mortgages, utilities, tuition, insurance). My threshold is lower than what Mr. ODA said is his threshold, so this isn’t a hard-and-fast amount, but one that is my “I feel OK if we’re close to this number” concept.

We screwed that up a good bit by purchasing a new vehicle and putting new tires on said vehicle immediately. We also had to pay for a previous heating issue fix in our house and a downpayment on new windows (which, quick side note, are glaringly needed as we go through 2 weeks of single digits and can feel the drafts). I’m also not counting the things that we do as mystery shops since those are effectively reimbursed (sometimes our cost isn’t fully covered since it’s a whole family outing and not a single person, but I’m not drilling down in that detail since I don’t have the specific break down of how Mr. ODA is getting paid). If I take those things out and remove expenses for rentals, then we spent $1597 in January.

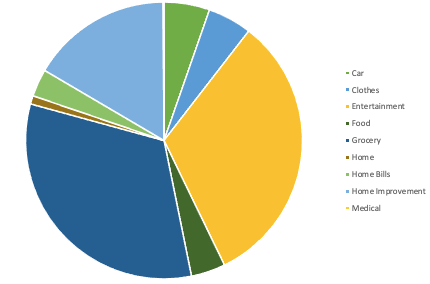

This isn’t the best representation of our spending, but I’ll develop this information as I have comparisons month over month. I also can’t seem to pick a better color scheme without it being a very manual process. Grocery, Entertainment, and Food are our biggest slices there. The entertainment category is basically why I gave up categorizing things years ago. Here I put things like going out for a drink, because while it’s at a restaurant or bar, the sole purpose was to have a drink and hang out. It also includes going to a gymnastics meet with my daughter, my fitbit purchase (I guess because I’m counting it as extra spending and not a necessity), and gift giving costs. We spent $528 on groceries this month, which feels low. I pushed really hard to clear out the food we have in the house already during our 2 weeks of being snowed in, but I hope that this is an accurate representation of monthly spending on groceries.

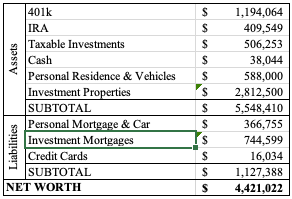

NET WORTH

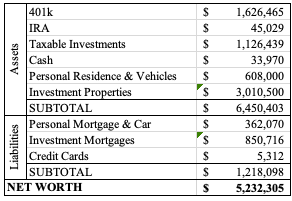

It is higher than last month, so that’s good. Credit cards are carrying $4500 worth of windows, so it’s nice how low of a balance those are outside of that 0% interest balance we’re holding onto. Our investments struggled a bit over the past month, but the payments on mortgages and loans helped offset that.

I wrote most of this post 5 months ago, but I’m going to finish it now for the longevity of what we’ve done with these rental houses. The house has been rented since September and was vacant for 43 days. She agreed to a shorter lease term, so it goes through June 30, 2026.

The tenants in this house moved in 3 years ago. They were good tenants. They hardly asked for things and were super understanding and gracious when we had the HVAC go out (granted it was their lack of filter changing). They brought a dog into the mix and tried to hide it (not well), and I eventually called them out on it to let them know they don’t need to keep finding a way to hide the dog every time I need to come over. They added a 3rd person on to their lease about a year ago. The only major issue I have is they smoked inside the house. I knew it constantly because (just like with the dog cover up) they weren’t great at hiding their evidence.

Earlier this year, I reached out that if they want to renew, I’d be raising their rent from $1200 to $1275. The girl who usually handled the bidding called me and explained they had intended to move to Georgia for a job, but they weren’t ready to move as fast as the end of the lease. I told them they could do month to month for a little, and we agreed to June 30th. I knew I had another lease ending July 31st, so I thought it would work out well that we could address the one house before the other became vacant. In theory. They ended up asking for another month, and we were busy with summer things at the end of June that I agreed, even though it meant two houses were vacating at the same time. I told them that I wouldn’t be able to extend any further though because it’ll be hard enough to rent end of August time frame, let alone into September or later.

On July 29th, they asked me what time they had to be out on the 31st. I said 5 pm. The next day, they asked me if they could have a couple more hours, but I let them know that I had already booked someone to meet them for their keys at 5 pm, and that’s all I could give without it costing them more. I was out of town for this vacancy and asked a friend to be my property manager to walk the property and gather the keys.

They ended up being out and basically cleaned up by 5 pm. I was impressed. The fridge was completely wiped down. The bathrooms were in rough shape, but overall, it was one of the cleanest vacancies we encountered.

THE TURNOVER

We had to have a friend go out to get their keys because we were out of town. I tried to get them to stay until the weekend to make it easier to move, and so that I could be the one to meet them (not that I said that), but they didn’t want to pay the per diem for that option. They ended up keeping their timeframe perfectly.

The turnover took longer than I had planned. I was working part time without a real ability to give up those hours because I had things that needed to get done, and it was summer, so we had 3 kids in the mix. Not to mention, we basically had back to back trips planned for the end of the summer. Overall, it was a learning experience.

We spent about $800 on supplies for the turnover, outside of the carpet, which was about $3,000. With the extra cleaning of the bathrooms and the time it took us to clean and paint the property, we kept their security deposit of $1,200. We could have gone after them for more because of the smoking (I have pictures from when I was doing work in the house of ashtrays with used cigarettes upstairs in the house), but it’s not worth the effort and cost.

FLOORING Before they moved in, we had ripped out the carpet and installed luxury vinyl planks (LVP). Conceptually, the goal was to not need to work on the floor anymore. We had limped along with the carpet, especially in the living room, since we bought the house, and it just wasn’t worth it anymore. We did the install over two days back then. Now that they were out, there were several gouges in the floor and the floor was separating in some spots. Mr. ODA handled fixing the separation, and he replaced a few boards that were damaged and noticeable.

The kitchen floor was so dirty and it’s the first thing you notice when you walk in. I spent many hours on my hands and knees cleaning out the grout to make it look less dingy. I didn’t get it perfect, but it was fixed. It’s one of those things that no one will ever know just how much time I put in for it to not be perfect, but it would have been so much worse had I not done anything.

BATHROOMS The bathrooms were a wreck. I’m so lost when I walk into homes and the bathrooms are dirty. Do you want to sit on that toilet or clean yourself in a shower that is dirty? It seems counter productive to me. Mr. ODA had to take over with Bar Keepers in one of the bathrooms to remove the staining and soap scum build up, but we did pretty dang good.

I wish I had a ‘before’ picture easily available to show, because this picture does not do justice to how much time went into this tub.

CARPET We bought this house 9.5 years ago. The carpet was questionable when we bought it. We would have it professionally cleaned between tenants, and it would look amazing compared to what we saw at first, but the stains would always come back because they were deep in the pads. Before these tenants, we ripped out the carpet in the living room area and laid LVP because the living room was especially bad. Well that still left carpet in the 3rd floor bedrooms, hallway, 2 stairwells, and the whole basement. With the smoking by the tenants and knowing we had far surpassed the useful life, we went ahead and planned to replace the carpet.

There were delays in getting the appointment scheduled and making it all work. The lady who did the measure appointment said installations were 3-4 weeks out. That was disheartening because we had already lost over a week by having back to back trips at the beginning of August. We went into Home Depot to find something else. I ended up settling on something because it said 5 day install. Well, 5 days came and went. I was so frustrated that I had settled on this worse-off carpet just because I wanted to meet a timeline, and now the timeline meant nothing. Then suddenly, we got a call and they said “can we come install the carpet today? We’ll load it now and be there within the hour.” That they did. They installed it in 7 hours and that was behind us.

PAINTING This took forever. Two big stairwells really take a lot out of your time. Every surface needed to be painted just to work on covering the smoke smell. While we didn’t spend a lot on the turnover (outside of carpet), this house just took so many hours from us. We painted every wall. I painted some of the trim that had not been previously painted, but it was in rough shape. We also had to repair several walls because they had sticky things to hold shelves up and they didn’t remove it.

MISCELLANEOUS THINGS DONE

Replaced the dryer door handle (that had actually broken off before they moved in, and I thought this was an insurmountable task to fix/replace… well, it was a $6 plastic piece off Amazon that popped right in. Welp.)

Replaced window screens that were worn away and in disrepair.

Cleaned out all the air filter areas for the HVAC.

Replaced all the rusted and broken floor vent covers.

Installed a doorbell because they installed a Ring, took it with them, and didn’t put the old one back in.

Replaced the cabinet knobs (it appeared someone had spray painted over the original 90s brass with something to mimic a stainless steal look, and they were all worn and chipped).

Wiped down the cabinets and walls to get them to be less sticky. Wiped down all the doors, light switches, and outlets because they were so gross.

Replaced the broken light in a stairwell that they broke on their move in (and reported).

Repaired some ceiling areas that were damaged due to a roof leak before the HOA replaced the roof.

Replaced a shower curtain rod that they took with them instead of leaving behind.

Painted the front door. It looked like someone had taken steel wool to it to clean it.

LISTING TIMELINE

We got the property to “good enough” stage so we could get it listed. There was still things to get done, but we didn’t want to wait until it was perfect and lose interest as we got further into the school year under way.

We listed the property at the end of August for $1,400. I thought we were golden. The location of this property is excellent, and it’s on a bus route that takes you downtown and to the outskirts of the city for shopping. There were two other listings for $1,500. It didn’t move. I didn’t even get productive bites.

I dropped the price to $1,350 two weeks later. I did show it a few times. I was happy that when I made appointments, people actually showed up, but they didn’t qualify. Mr. ODA hosted an open house and had one person come through. That one person was our person though. I removed the listing two days after the open house and we have it rented at $1,350.

I offered her $1,325 for an 18 month lease or $1,350 for a lease through June 30th so I could get back on a Spring schedule. She agreed to the shorter timeframe. She was looking for a quick move because her landlord was selling her place. Our house seems too big for her needs, so I wouldn’t be surprised if she leaves at the end of June and we need to find a new tenant.

SUMMARY

We knew a September listing was going to be tough, but I didn’t expect it to be that tough. When we had a property managing on this place, they always took 5-6 weeks to get it rented and it drove me crazy. At least 3 weeks from start to finish isn’t terrible, but I’m definitely used to it moving faster. It’s also nice that had my tenants stayed, we’d be getting $1,275, and now we’re getting $1,350. Thus far, this lady hasn’t asked for much. We struggled with the utilities getting into her name. For some reason, the utility companies credited my accounts and billed it directly to her, so I didn’t even need to work on capturing that money from her, which was nice.

I have so much to say. January is a big time where people are willing to talk about finances, so many thoughts enter my mind that I want to squash some preconceived notions. Unfortunately, I just don’t have the time.

PERSONAL

At work, I’ve spent this year managing year end things and getting the 2026 processes stood up. I’m supposed to be part time, but I’ve been putting way more hours in because of that process. The guy who was helping me left for another position and was out of the country all last week, so I had to make sure I was extra on top of things. With all those actions going on, I also was pulled into hiring someone to be my assistant (for lack of better term… it’s not assistant as in answering the phone and getting the mail… it’s doing the daily bank reconciliations and those types of tasks so I can focus on policy development). This has taken a significant amount of my time, but hopefully this person will be on board to help in a week.

Our youngest started preschool last month. He only goes 2 days per week, and both are my work days. I’d really like to get to a point where I can actually take advantage of guilt-free, kid-free time.

I have a new years resolution that I’m keeping close to the vest, but one part of it is to walk 10,000 steps per day. I’m failing miserably, but it’s a work in progress. My 7 year old son asks me constantly if I’ve hit my step goal. So…. maybe I’m teaching him it’s ok to fail, but keep trying? His new years resolution is to get better at being his nicest, and that’s just adorable. He also says he wants to learn basketball, and I just can’t bring myself to do that. We are signed up for Spring baseball that should start in March. The youngest has to wait until next Spring, but I can’t wait to see what he can do. I’ll probably also be putting swim lessons back on the docket in the next couple of months. The youngest hasn’t had any lessons. The oldest passed the test for his yellow band, but he needs to have a free style stroke to get the green band. The middle needs confidence; she can absolutely swim, but she likes to pretend she can’t do things.

RENTALS

Last month I reported that at the end of the day on the 5th, I was still missing 25% of the month’s rent. As of 7 am on the 5th, I had only received 30% of rent. Many came through, but there were more than the usual amount that didn’t. For one, I had to manage a grant program from one of the places a tenant lives. The check finally arrived yesterday, but it’s dated December 12th. They mailed to my PO Box, in a town I left in 2020. I didn’t even know my lease had an address on it, but that’s how long these people have been there. The check was returned to them, so my tenant went down there to give them my new address. I don’t love these people having my address, or that they now officially know I don’t live in the same state as them, but I needed to get this check. I gave them the address over her phone and received confirmation she typed it in. Somehow the check was returned to them, so my tenant had to pick up the check and FedEx it to me (I told her she didn’t have to pay that kind of money for that!). I have a tenant that pays twice per month (and pays a premium for that); her second part of rent is due tomorrow, so we’ll see if I can finally be fully paid for this month by the 19th.

I have a tenant who fell into some unfortunate circumstances. Her current plan is to vacate her place by the end of March. She’s lived there since 2019 with a dog and 5 cats, so that place will need all new carpet and a new paint job, but hopefully will be ready for a May 1 rental. Because she’s always paid and I knew her financial circumstances, I’ve been slow to increase her rent. She’s paying $975, but the market rent should easily get at least $1200. The house is in really good shape and is newer. We had people fighting over the other house in that town at $1150, and it’s an older house with only one bathroom.

FINANCES

Well we traded in our van for a newer year, but that’s a story for another post. I also still haven’t fixed my retirement account access from when I got a new phone number, so that’s a made up number.

I’m going to be tracking our spending much closer this year. We’re generally on the same path with our spending, and I know we don’t do anything extravagant. With Mr. ODA’s lack of income, I just want to keep a closer eye on that and pivot if we need to.

Mr. ODA has a more exact approach to figuring out what we can spend per month without dipping into savings. I like my number better (and it’s lower). I took our rental income, deducted rental fixed expenses, deducted our typical bills, and was left with just over $1300 per month. That would go towards food, clothing, gas, etc. If I remove things that are offset by a shop (Mr. ODA is a secret shopper) and the long term investment purchases (i.e., car and windows), we’re at $987 as of the 18th.

NET WORTH

We put $1500 on a credit card and finances $7500 to be able to save $1000. We also put $5500 on credit cards towards windows, which is also another post that’s coming. Our net worth took a hit for both these things. I also wasn’t able to update 3 accounts, so they’re just estimates, but at least our net worth still went up.

We are 2 months without Mr. ODA’s pay check. I honestly haven’t noticed because my day to day is just managing how much is coming in against how much is going out. My concern is the net I have for this year is $30k less than what Mr. ODA brought in. We’re adding nearly $2k per month for insurance costs, so that net difference is $42k. That’s a gap we’re going to need to focus on here shortly. I should note that our spending includes rental work that we pay out, and we had some major purchases in there (e.g., roof, HVAC). I could say I hope that our investments in the rentals will be less next year, but we seem to track the same expense totals each year.

End of year means I need to get my spreadsheet organized. I need to make sure all expenses are logged, that all logged expenses have receipts and documentation to support them, and that all our maintenance actions are logged in my maintenance sheet. The maintenance sheet is what I use to check back easily on what work we’ve done on each house. I was taking too much time trying to remember which house we replaced things in, so now I have this sheet that I can pull up and easily say, “I just replaced a valve in that toilet 4 months ago; this isn’t normal wear and tear.”

RENTALS

The 5th was a Friday, so you know what that means – I didn’t see most of our rent until then. After the 5th was over, I was short 25% of our rental income. That is fascinating to me. Everyone had told me what their plan was, but I can’t fabricate money where there isn’t any. I have a tenant that is using a program to pay partial payments throughout the month. I can’t stand it. It ensures I get my money at the “beginning” of the month, while it puts them on a payment plan. However, they have the payment set as the 5th, and then it doesn’t clear and hit my account until about the 12th. I’ve expressed my frustration that this has gone on for several months instead of it being a one or two month stopgap, but nothing is changing.

We got our new townhome rented right before Thanksgiving. That was helpful and a literal last minute prayer that was answered in a crazy fashion. She’s been in for 3 weeks now, and I haven’t heard anything.

I had a tenant inform me that she’s hit rough times and wants to be released from her lease. I was really hopeful for a calmer month, but I need to reset my expectations. 14 rental properties and 12 months out of the year = there probably won’t be a month where nothing comes up. The good news is that we can likely get it turned over and a new person in there for market rent. She’s currently paying $975, and we’re looking for about $1300 going forward. Because she always pays and I knew her financial situation, I’ve always held back on her increases. There was another $25-50 increase coming this year, but it still wouldn’t have made up the increases in carrying costs over the years.

PERSONAL

We’ve just been so busy that we’re not really spending that much. Most of our spending is for regular purchases. We had a huge purchase hit our credit card, but that was split among our family for the purchase of new phones. I did all my Christmas shopping in the last month, so that’s higher than usual spending on the cards, but overall still pretty low.

NET WORTH

I got a new phone number and updated all my accounts before my old number was deactivated (lovely two factor authentication). One of my accounts (401k) updated my phone number, but that apparently didn’t correlate to updated the number associated with two factor authentication – ugh. I need to address that, and for the time being, that’s just a placeholder number that I guessed based on Mr. ODA’s 401k increase over the last month.

We last purchased a rental property in 2022, after most of our purchasing was done in the the 2019 era. We were busy with 3 kids, and I recently felt like I was coming out of the fog. Mr. ODA and I went to a wealth building seminar in the Spring; my intention was to have that seminar reinvigorate our desire to build our portfolio. It worked well for Mr. ODA, but once options started to show up, I started to panic.

We first went to an open house. It was a bit further away that I’d prefer to maintain a house, and there were a few red flags. For one, it frustrates me that landlords can fill out a seller disclosure claiming they know nothing about the house. I can tell you if I had any roof issues or major system issues in any of my houses, even though I haven’t physically lived there. Mr. ODA wanted to pursue it, but I couldn’t bring myself to get on board.

We were then sitting with his parents one night, telling the story of this open house, and his mom said that she saw a townhouse posted on Facebook that she thought we’d be interested in. It was owned by the son of an old friend of her’s. We asked our real estate agent if she’d show it to us, but she was out of town. So then his mom texted her friend to see if they were there and we could go look. They weren’t there, but they gave us the contractor box code (which is surprising in itself that there wasn’t a sentribox on the door). We went over and the house looked to be in good order, so we put an offer in. We like to surprise our agent with these types of things where all she needs to do is get the contract ratified.

UNDER CONTRACT

The house had been listed for some time when we came across it. It was was listed at $182,500. We offered $182,000 with $2,000 worth of seller subsidy on September 2, 2025. They agreed that day. We ended up needing to redo the contract because the wife wasn’t on the deed of the house, but she had signed the contract, but that wasn’t a big deal.

We had the inspection scheduled for September 10th. There was hardly any issues in the report, and we picked a few of the bigger things to ask for them to fix. They agreed to our list. They gave our agent a receipt showing they had paid someone to fix the items on our list. We did our final walk through the afternoon before closing and were disappointed to find that two of the bigger items (leaks) were not addressed properly and the house was dirty (including things left in the fridge and freezer). Our agent reported that to their agent, and they addressed everything that evening. We swung by the next morning before closing to see it all cleaned up and the leaks addressed.

The appraisal was ordered by our lender and came back at $188,000. That was a pleasant surprise to see we had immediate equity in it.

COMMERCIAL LOAN

We chose to go a commercial loan route. Interest rates aren’t falling as quickly as we expected to see. We have a commercial loan on one of our other properties in town, and I was still surprised to see how easy this process is. The loan qualifications are mostly based on the cash flow of the property. I filled out an application, submitted a ledger of our other property cash flows, and sent in 3 years worth of tax returns.

We were quoted at 6.74% interest. The loan terms are a bit different. Our last commercial loan was amortized over 25 years, but there’s a balloon at 5 years. This time around, it’s amortized over 25 years, but the balloon is at 15 years. A commercial loan also means that the taxes and insurance are not escrowed, and I’m responsible for paying them on my own.

The loan is an Adjustable Rate Mortgage (ARM) too. There was no different to us in the 3 year or 5 year ARM, so for the first time, we picked a 3 year ARM. In the past, it was related to securing our low rate. This time around, we’re expecting rates to drop in the near future, so we locked in our rate for only 3 years. It only changes on 3 year increments (some of the others will change every year after the initial lock period). It also has a clause that indicates the rate has a floor of 4%. I also don’t see a maximum adjustment that can happen (we have other ARMs that state an adjustment can’t be more than 2% at the change date).

We were expected to put 25% down. That would be $45,500 based on the $182,000 purchase price, and would leave 136,500 worth of a loan. They ran some numbers and determined that we could only qualify for a loan of $132,000 based on a rent of $1,400. They only us the cash flow to determine the eligible amount and not the rest of our portfolio. Let’s break that down to the fact that a loan of $136,500 equates to a monthly loan payment of 942.23, and a loan of $132,000 equates to a monthly payment of 911.17. So at a rent rate of $1,400, we could cover the monthly payment of $911.17, but we could not cover a monthly payment $31.06 higher. We pushed back for a second, but in the end it didn’t matter and we accepted the loan of $132,000.

PROS

When I look at this place, it feels like a place someone will rent. It’s clean, feels like home, and has a good layout. It has a closet available for a washer and dryer, which is a plus. Both bedrooms are upstairs and each has its own bathroom, and there’s a powder room on the main floor. It’s more secluded than other units in the complex, giving the occupant more grass area to hang out in the front and back.

CONS

We do have some concerns. The townhouse is at the back of the neighborhood. The entire rest of the community has parking right outside their front door. This group of 4 townhomes is separated from the parking lot, so you have to walk a bit further. The trade off there is that it’s secluded, you have a front “yard” (instead of pavement), and you’re more secluded from your neighbors.

I didn’t want another townhouse in our portfolio. With a townhouse, your value is strongly dictated by what your neighbors have done (or not done) to the property. As much as we don’t plan to resell these properties in a short time frame, I do have the thought that I want to be able to sell it when the time comes.

Also with a townhouse, you’re also at the whim of a community manager that is likely not putting utmost effort in. We asked about the HOA at closing and the previous owner said the cost used to be $35 per month. When it was that cheap, they weren’t paying their bills, so the lawn wasn’t mowed and the trash wasn’t removed. They increased the price to $95 two or three years ago, and that has made a difference in the community’s upkeep.

The HOA is due monthly, which is an inconvenience and a surprising process on their part. I plan to pay it monthly until I have confidence in their ability to process my payment and apply it to my account timely. After some time, I may pay in advance. I just went to process the first payment and planned to pay 3 months worth, but then realized that will create a harder tracking mechanism on me right now.

CLOSING

We had our closing on October 16th. It was super quick and easy. I listed the house for rent that evening.

SUMMARY

At this point, we have the house listed for rent at $1375. We had determined the range for rent during our purchase evaluation. Unfortunately, I hadn’t looked at the current market by the time we went to list, and there’s quite a bit out there. I’ve shown it to 2 people and have another showing today. One of the people from the weekend said they were seeing other places on Wednesday, so I’ll hold out on any changes to the rent price until this weekend.

We had two tenants move out at the end of July. We also had back to back trips scheduled for the end of July and beginning of August, with the kids starting school on the 13th. We also had the cruise planned for the end of September into October, so that was a decent push to get the rentals rented before we left. We put countless hours into those two houses and it definitely took its toll.

RENTALS

As of October 1st all our rentals are rented! That’s a good feeling after two months of vacancy. This is the month of taxes. We have several houses that are paid off, which means they aren’t escrowed, and I’m responsible for paying the taxes and insurance on them. The 4 houses we have in KY are owed this month, and it’s about $7k worth. We’ll owe 2 houses in VA that come to about $3k next month.

I have a couple of houses that are struggling to pay rent on time. Usually it happens for a couple of months and they get back on track, but that’s not happening quickly. I’m trying to remain optimistic, but there isn’t a track record of it getting easier if they have taken this long needing to catch up.

We closed on a new property near our house. It’s a townhouse that we hope to get rented later this month. We’ll see what it looks like once it’s empty, but it didn’t appear we’ll need to do anything to it to get it rented (which is how we buy our rentals). There will be separate posts going into the details of each rental turnover and the purchase of House15 using a commercial loan.

PERSONAL

This is the last month for the 0% interest credit card. When we have a major purchase on the horizon (it was house-wide carpet this time last year), we open a 0% interest credit card. We started this concept about 8 years ago. We look for a credit card that has 0% interest for at least 12 months and that gives us a bonus of some sort. We make more than the minimum payment each month and then pay it off before the deadline. A default payment can cause you to lose your 0%, so it’s important you’re making your payments. But we don’t pay a lot towards it because the money is doing more for us in our savings account (or the investments) than it would by paying down a 0% interest balance. This time around was a bit different. The carpet only cost us $10k, but the balance is over $14k. This credit card had the same incentive as our typically used card (2% cash back), so Mr. ODA used it a majority of the time. For a while, my goal was just to pay what gets our balance lower than the original balance from the carpet. But then we had some big rental purchases that we put on the card, and it just wasn’t worth paying $5k+ to the card. We will make a transfer from our big savings account to make that payment at the end of the month.

Mr. ODA’s last pay check arrived on October 11. He took the “deferred resignation program” as of April 30. The sunset date was September 30, so that covered the payout that we just received, including his balance of annual leave.

Outside of rentals, our spending has been minimal. With the cruise, we didn’t spend much since that was a week of almost everything paid for in advance. The dog had his annual check up, so he was the bulk of our costs. We have our routine costs we see, but happy to see lower balances after all the rental work costs.

SUMMARY

I don’t even want to admit what is about to leave our account this month. I guess the positive is that it’s under $100k..? We have to pay the taxes on the houses that aren’t escrowed, pay off that credit card, and buy a house. At least the house purchase goes right towards equity. Since I didn’t get all the account numbers yesterday morning like I planned, here’s an update that captures our new purchase.

Well, we started the month with way too many things hitting the credit card: 2 insurance policy renewals, a new insurance policy, air conditioning fix at a rental, and bathroom replacement at a rental. That eventually led to a $1500 charge for bat removal at another rental.

PERSONAL

My big news this month was handling my HOA’s annual meeting. We’ve been working so hard for the last year, and I tried really hard this year to increase communication between the Board and community. I think I did a good job because there wasn’t any contentious point of this meeting and there were very little questions. I received nice feedback on how I presented the budget and that I did a good job throughout the year. It was a welcomed win since there was a lot of heat in the previous couple of years.

The family’s big news is getting passports for a trip this Fall. The parents already have theirs, but we got the kids their pictures and submitted their application. So our credit card balance is higher than normal because we paid for flights and the cruise itself.

It took us until the last week of June to meet our deductible on our health insurance. It’s only $3,300, so that’s quite the impressive feat. I’d point out that my March surgery took until then to get processed correctly, but at least we eventually got there. I have very little faith that it’s all processed correctly though, so it’s on my to do list to verify that we’re not overpaying into that deductible, which they don’t make easy because they don’t show me prescription fills clearly.

We went on a trip for a long weekend to visit Mr. ODA’s aunt in WV. They have a vacation house there, so we didn’t pay for lodging. Unexpectedly, they provided all our meals. I bought them a gift card and some beer. So between that gift, gas, and the meals on either end of the trip, we spent about $200 for a trip, and it was one of the best vacations I’ve been on.

Two of the kids spent this past week at camps. One was 3 hours per day at a dance studio, and the other was 9.5 hours of all outdoor time for the week. He had a blast, and I’m kind of jealous that he got to play all those games and have a great week.

RENTALS

This month, I received an email from Rent App that a tenant was paying their rent. She didn’t give me a heads up, so I wanted to verify things with her. She said this app pays me in full, but it takes the first half of the payment from her account at the beginning of the month and then the second half of the payment in the middle of the month. They’ve lived with me for for 8 years, so I’m surprised she sought out this option instead of talking to me about a payment plan. The program was extremely sketchy and I didn’t feel good about a single step of it. I gave up the registration process at the point that it required untethered access to my phone, but I wish I would have followed my gut at the first personal information step, as if it wasn’t bad enough I had to give my bank account details for the transfer to happen. The payment eventually came through on the 10th, but I didn’t feel good about it.

Another tenant paid late with the late payment. And another tenant paid late with little to no communication and several follow up conversations. I can’t stand when I have to hunt down money. I’m willing to work with everyone who reaches out. She paid the first one with a (1/3), so clearly she knew the plan. And yet, on the 6th, I had to ask where the rest of the rent was. She said it would be done that day. A partial payment was made on the 7th. Then another partial payment on the 8th to finish it out.

We hired someone to clean out the gutters at two houses. Both houses are inundated with trees over the roof, so it’s something we need to stay on top of because they back up every 6 months. We could add gutter guards, but just didn’t see the point since we could do it. Now we don’t live there. He is also going to cut trees 10′ back from the roof on one of those houses.

And then the bats. One house had a bat show up last Monday. My property manager didn’t think much of it, so we didn’t do anything (I wasn’t even told about it at that point). Another bat showed up on Saturday. The tenant went for rabies shots and got boosters for her dogs. She then took a bat to get tested, which came back negative. She said she wasn’t comfortable staying there, so she stayed with a friend. We had traps set so bats could get out of the attic, but they couldn’t get back in. The pest people will go back next week to check on things.

We have two houses that will be vacant at the end of this month. We were supposed to have one at the end of June and one at the end of July, but the June one asked for an extension. I let them have it, but I’m not thrilled about my timing now. We won’t be able to truly get to work in there until mid-August, and it’s going to require a lot of work (not hard work, just time consuming). Then for the other one vacating at the end of the month, we don’t intend on renting it again. We’re going to let it sit over the winter and sell it in the spring.

NET WORTH

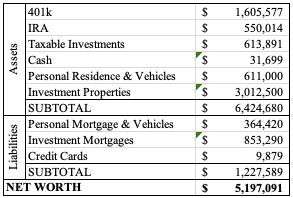

The way that I update our net worth each month involves overwriting the numbers from last year. So I can easily see that we’ve gained over half a million net worth since July 2024’s update. What’s nice about that is that it’s all appreciation, paying down mortgages, and the stock market with continued savings. We didn’t make any large financial moves that would have adjusted our net worth in one large move like buying a house. I had a conversation with someone about our net worth and goals recently. It would be nice to cross the $5 million threshold, but we’re not actively managing our funds in a way that will cause drastic swings outside of market movement. We crossed $4 million in March 2024.

We’re over $200k from last month’s update. Our credit cards are much higher than last month because of trip purchases and rental work that was unexpected, but needed. Here’s to the last month of summer.

We started getting emails about end of school year activities, and boy was that a surprise that we’re at that point. The middle one is done mid-May and the big kid is done at the end of May. Less than 2 months until summer break.

Mr. ODA took the second round of the government’s offer for administrative leave, which means he would only have a few weeks left working. I’m still working my part time job, which is taking way more hours than we had planned for. I’m enjoying it, but it’s been a juggling act with the family, which is probably why my son who absolutely loves school begged me to stay home because his belly hurt last week.

Buckle up because apparently I have a lot to share this month.

RENTALS

We received about $600 in tax payment reimbursements from one of our localities, so that was a fun surprise this month. Really helps my psyche that I have a tenant who hasn’t fully paid, didn’t tell us why ahead of time, and hasn’t been up front with when she’s going to actually pay us.

I executed 2 short term leases. Both included a rent increase for their short term period; one house is increased by $75 and the other by $25. Luckily, both are here in the Central KY area, so we can flip it between tenants. One is scheduled to leave June 30th. That house will need new carpet in the bedrooms, and it’ll need probably a whole-house paint job again. They smoked in there, even though we covered the lack of smoking rule multiple times. I’d be more upset about it if the carpet hadn’t reached its useful life years ago. The other house leaves July 31, and I can’t even tell you where we’ll need to begin with that one. She made a wood feature wall without permission. She had a giant fish tank without permission. She spent a lot of time doing things that really weren’t an improvement, so I’m definitely worried about what we’re going to uncover in that house. Mr. ODA and I are talking about fixing it up and selling it. We may look for a short term renter so that we can sell it in the Spring instead of this Fall.

I had 2 other properties accept a rent increase that will go into effect later this year. I require 60 days notice for changes so that starting at the 30 day mark I can begin advertising it if needed. One house goes up by $25 per month as of June 1, and the other goes up by $50 per month as of July 1. I also have another property that has a rent increase of $50 per month going into effect next month.

I have 4 houses that renewed another year, and I didn’t change their monthly rent rate. There are 4 more houses that haven’t been discussed. My intent is to have them renew for a year at their current rate. There are 2 of those 4 that could leave at the end of this term, but time will tell.

We have multiple maintenance issues to address. One house requires a tree trimmed off the roof, the siding cleaned, and the back deck stained/painted. We still have termite damage we’re dealing with at a house in Richmond. I have a leaking toilet that was just addressed, and then they hit me with a faulty HVAC unit during a heat wave. Then we have some houses that really need eyes on them to see what condition they’re in at some point this summer back in Richmond. It’s amazing to me how people just don’t care to tell a landlord that something is broken. I woke up this morning to a text that one of the houses here has a flooded basement due to a water heater failure.

I spent some more time fighting my insurance guy here. It irks me so much when I see him offer up his services on the local facebook group for property owners. He’s quite terrible. I sent him photos of a house that had some issues with a cluttered backyard and had the tenant clean that up. I had to fight him last month on an increase where he changed one house from a crawl space to a basement when I assure you that the vines growing through the windows solidify it should not be deemed a “basement.” When the dust settled from that debacle that he was insanely unresponsive to, I ended up owing $9.68. When I asked why my account wasn’t put back the way it was found before this mess he created, he said he didn’t know but it’s probably from the audit and changing square footage. HIs guessing and not actually answering infuriated me. I gave up and paid it, but then I ran to get quotes from other people. I hadn’t done that before because our 4 claims in a 12 months period are killing us (again, because I really wanted trees to fall on us!). I hate when people make the claim that because it’s not a lot of money, I should just give up and accept it. That’s a ridiculous way to treat people.

PERSONAL

Our electric bill is almost double what it was this time last year thanks to the vehicle charging and hot tub. Our electric bill is relatively low, so that’s not all that surprising. We also have 5 full people in this house now (as much as you can count a 2 year old as a full person… but he knows how to control light switches and eats a ton of food that we need to cook him, so I’m sure he’s a factor there!).

I’ve been working at my new part time job for over a month now. Mr. ODA was making fun of my hourly rate, but I’ll tell ya, it felt good to receive a paycheck that wasn’t $45 like it was for a day of subbing at the preschool.

I took the kids to get haircuts. My middle has had her hair cut once before, but I’ve cut the boys’ hair forever. I had family coming into town and the oldest was looking really shaggy. So I swallowed my pride and threw money at the problem, which is very out of character in this household. I just didn’t have the time to cut their hair, clean them, and clean up the mess. For $66 and 45 minutes from the time I left home until I got back, it was well worth it to me.

I had a medical procedure done this month. We haven’t met our deductible. In February, they said I had to pay my deductible to them. I said that didn’t make sense and refused to have them hold $2800 of my money for 2 months. They gave me an attitude and said I could never ever ever ask for a payment plan in the future, so that I could pay $500 to hold the date. I then showed up for the procedure, knowing I haven’t met my deductible, and they didn’t take any money from me. Another business model that bullies the customer into illogical money decisions. I also had an eye doctor appointment that was frustrating in itself, but I’ll spare you those insurance and communication details.

On top of everything else I’m juggling, Mr. ODA is coaching our kids’ t-ball team. Coaching means that I am team mom. That means that I’m responsible for communicating updates from the league (in the slow and haphazard fashion I receive information), gather value card sales that are required of every team member, organizing a basket for a raffle, and the best one – raising $350 for team sponsorship. What the heck, man?! Where did I say that my signing up of two children to play in the league means I have history or ability to gather money from businesses?? Well, I did it. I raised $350 and another mom raised $200 for the team.

No financial impact, but I’m also juggling our HOA board duties. I released our longstanding property manager and hired a new company, which took effect April 1. That’s taken a lot of time to get them stood up and make sure we stay on track for our annual meeting schedule in June.

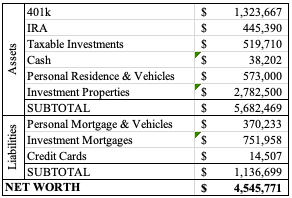

NET WORTH

And with all of that said, that doesn’t even address the giant reduction in our investments that continues to happen. To counter some of the loss, I updated our property values for our houses. I don’t do that every month because they don’t move very much, but I can usually count on a few increases as the spring market ramps up. Our net worth did slightly increase (based on yesterday’s market closure, not today’s) from last month, which was a nice surprise.

I wonder why I’m tired and bogged down, but that post outlining what I’ve done recently made me realize all I was able to accomplish even though I felt like I was a jack of all trades and master of none. Hopefully things will settle down in our lives going forward now, even if I know there are definitely two house turnovers in my future.

There are options that give the tenant flexibility, while protecting your financial interests in a rental property. I talk about this in some fashion about once per year, but I like to give the reminder.

In January, I ran all my usual numbers to determine if any properties needed a rent increase. The last few years have really hit our margins – insurance has drastically increased, taxes have increased significantly, and the regular trades costs have increased over time as well. During this process, I determined that 5 houses needed some sort of increase in their rent. One was the responsibility of my property manager, and the other four I wrote up the notifications, put them in the mail, and then emailed them also.

I’ve had two tenants respond back that they intend to move in the next year, and they wanted month to month. We don’t agree to month to month options. Well, I should point out that for significant financial compensation, we would consider month to month. However, the expectation is that having a long term tenant renew their lease is less work month over month. If they’re on month to month, I’m constantly watching and waiting for their 30 day notice. Additionally, there’s a concern that their 30 day notice comes in October or November, leaving me with a mid-winter lease that I’m trying to get filled.

Instead, I provide a few options that protect me. I’ve done the “buy out” or “penalty” option multiple times in the past, and that has served me well. I haven’t needed a short term lease option, but since there are certain circumstances with these houses, I put that offer out there.

In both cases, the tenant said she wants to be able to leave sometime in July/August. This is manageable to me because I can likely rent it under a fairly quick turnaround.

Short-term lease While I would typically require an increase in rent to cover a short term lease, I was already in conversation about rent increases, so I let it be. I offered a July 31st or August 15th move out. In both cases, I know the house is going to require work. I’d like to have the last two weeks of August available to me for construction activities, instead of going into September and trying for an October 1 lease start date.

“Buy out” options (e.g., penalty payments) In this case, I have the tenant sign a year lease. However, the lease comes with “lease break clauses.” The penalty for breaking the lease ranges based on the time of year. In all cases, I require 30 days notice and full payment of rent through the date given as notice. If the tenant wants to leave before 8/15, then there’s no penalty.

If they want to leave between 8/15 and 9/30, then they have to pay the equivalent of one-month’s rent.

If they want to leave between 10/1 and 1/31, there’s a two month penalty. This is because finding a renter during this period is difficult. There aren’t as many people looking during the winter because most leases are spring to spring, so the turnover is fairly cyclical, and because most people are distracted with starting school and all the holidays happening during that time rather than looking to rent (or even buy) a house.

If they want to leave between 2/1 and 3/31, there’s a one-month penalty. Again, this is to cover the longer time it will take me to find someone to take over the lease period, and it provides me with a year-long lease (which most people are looking for) that ends at another inconvenient time for turnover in the next year.

If they want to leave between 4/1 and 5/31 (which is the end of their lease term), then there’s again no penalty just as there wasn’t for the first few months of the lease term. I’ll be able to get work done on the house and list it for rent, expecting a decent pool of people interested in a rental.

Lease transfer option As a final option, which was offered to us when we lived in an apartment building, a tenant can agree to a year-long lease with no extra terms. They then have the knowledge that if they want to “break” the lease agreement at any time in the next year, they are responsible for paying rent until a new tenant is found. They can move out, but they’re on the hook for paying rent until a new tenant has sign a lease.

This is risk on their end. In some cases, I may be able to get someone in just a week or two. However, if it’s the winter, it could mean that they’re paying a month or two months worth of rent while they’re also living and paying rent somewhere else.

The only time that I’ve used this option, the tenant provided notice on December 1st, which as I’ve pointed out is not a great time to be searching for a new tenant. Since he was already not living in the house (he had moved back in with his parents), he agreed to empty the house of his furniture so that we could still show it during that time. He paid rent on January 1st per our agreement, and luckily we found someone to take over the lease as of January 7th or 8th, so I refunded him the prorated amount of rent.

The “lease take over” concept was done by a management company in a fancy apartment building outside Washington D.C. It never hurts to ask for options if you’re the tenant. Just understand that managing the rental is work that the landlord has to do, and their “profit” is how they’re paying themselves for that. Especially in today’s environment, that margin is quite small. So when they tell you they don’t want to have a lease fall through in the Fall or Winter, understand how this is their investment and their income, so they need to protect themselves, even if it’s not necessarily what works for you or is your preference. And as for landlords, treat your tenants nicely and be as flexible as you can; it always pays off for me.

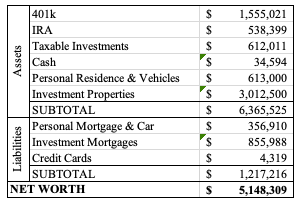

We’ve done a good job at enjoying time together this past month. We haven’t had a lot of expenses pop up, which was a nice reprieve. However, the market is much lower at this time this month than it was last month, so our net worth actually decreased. I keep focusing on the long term picture though, and our net worth is much higher than a year ago.

RENTALS

We have 13 rental properties. They were mostly purchased in 2016-2019, with one purchased in 2022. Most of them have sustained very little tenant turnover.

I had 4 houses not pay their full rent on time this month. As of this post, only 1 is still outstanding. They’ve had car troubles and have communicated regularly with me. While I’d prefer to see at least something paid towards rent by now, they’ve been with us for 8 years, and I know they’ll eventually be whole. They never take more than the month to get rent fully paid. Of the other 3 that were late, I only charged one a late fee. The others aren’t usual offenders and communicate up front, but this one has been more difficult to get rent paid from the time we purchased the house.

While looking back at last year’s January post, I must note that this past year has been fairly easy on the rental front. We’ve had a lot of frustrations and things to manage, but it hasn’t been as time consuming in the “people management” side of things. We had a few issues with a tenant that first moved in last winter, but they’ve been quiet since. We had 4 houses turnover tenants in 2024, with fairly little loss of rent.

PERSONAL

We have been battling snow for almost two weeks now, which is very unusual in Central KY. We’ve already taken the kids skiing twice this year. Even the baby got on skis! He’s 2, so I guess he isn’t such a baby anymore, but that’s the earliest we’ve put a kid on skis. He’ll slide down the mountain, but he doesn’t stand on the skis; he’s just squatting the whole way.

NET WORTH

Last year at this time, I was sharing that our goal was to reach $4 million. We were at $3.869 million.

Our net worth is about $66k less than last month. I don’t always update the value of our assets, so that’s a fairly static number. Everyone few months, I’ll check on the ‘zestimates’ though. Typically, we expect to see the total decrease in the winter months because there are less sales and less activity to raise the sale prices like you see in the Spring months. On top of that, all of our investment accounts (except one that increased by $22) decreased a bit.

We have a 0% interest credit card that has a balance over $12k on it. We also added a car payment, which we haven’t had since about 2015. Tesla was offering a 0% interest loan, so that monthly payment isn’t going away for nearly 5 years. Overall, our credit cards balances total more than $3k less than last month’s, which makes me happy to see.