Well, tracking spending is just bugging me. We’re over where I want to be in monthly spending. I registered the kids for summer camps, so that was $580 more than usual spending. I also paid for a kid to take swim lessons ($85) and our gymnastics cost went up because she earned a spot in an advanced class that’s a half hour longer. If I take out the camp registration cost, then our spending is about $1700. My goal is $1350 per month. That’s not what we can actually afford (Mr. ODA’s number is higher), and I’m learning may not be realistic, but that’s my general goal each month. I’m halfway into March and can tell you that we’re going to be nowhere near that number this month, which is frustrating, but also reality.

RENTALS

We had two service calls this last month. One was a water heater being out and the other was unnecessary but cost us $100. This lady has actually been a problem in this realm. She claimed the mail key didn’t work for weeks and took forever to respond to messages. Mr. ODA finally went over there and it turned out she was trying the wrong box and not paying attention to what Mr. ODA was telling her. Then she said the microwave wasn’t working. The circuit was tripped, and Mr. ODA let her know that she can’t run an airfryer and microwave at the same time. Then she said the washing machine wasn’t working. We had an appliance guy go out and he said, “it’s working fine. There’s not supposed to be any more water than this in a high efficiency machine.” So much fun.

I’m expecting a tenant to move out at the end of this month. I still haven’t heard the final information on that, which isn’t surprising, but that’s on the horizon.

I increased the rent on two units over the last couple of weeks, which is in addition to a raise I put into effect on another one last month. I also have let three renew at the rate they were at the past year (or more) based on their cash flow numbers and the tenants in there.

PERSONAL

I’m still working part time. Although, these hours are 50% more than I had signed up for. I’m helping get another office organized and training a new hire. It’s been a lot. I feel productive, but I want more hours in my day. Mr. ODA started a part time job as well. We’re on the hunt for insurance help. We’re paying out of pocket for the whole policy that we were under for the last 5-6 years. While we’re not expecting a lot of coverage to be paid by the employer, there is a benefit to having the funds come out pretax.

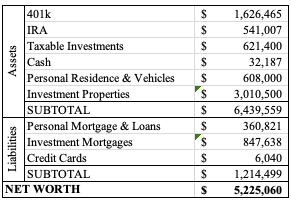

NET WORTH

Well, my update isn’t really that accurate. I’ve updated the numbers I could, but I’m already days behind on my schedule, so I couldn’t wait for Mr. ODA’s numbers anymore. We are still carrying half of the window order on credit cards (and that install should be next week… hopefully… it’s been pushed back once already). Our investments are down even more than last month, but I don’t know the extent at this time. Our net worth decreased from last month, with 10 accounts not updated, so I’d say it’s a substantial hit.

Before I get into an update, I have a quick perspective moment. Our preschool has a 3.5% processing fee to pay monthly tuition online. Tuition is $265, so the processing fee comes to $9.27. If I paid it online instead of writing a check each month, that would be an extra $83.43 I paid for basically nothing. For perspective, I spent $82 on a grocery run of essentials (e.g., dog food, paper towels, milk, eggs, etc).

RENTALS

I had to give notice to one household by 1/31 if I were to raise rent. Their lease ends 3/31, and that will mark 3 years with me. I was panicking because it’s our most expensive house (it’s also our nicest and biggest, and it’s fairly close to downtown). Rent has been $1750 for the last 4 years. Last year I missed the notification to raise it because a January deadline surprised me, but this year I put it on my calendar for January 1st to do. And then I dragged that calendar reminder through the whole month, only needing to then set an alarm to make sure I did it at 8pm on the 31st. I raised it to $1800 and they accepted within the hour. Phew. They’ve been late three times in 4 years and clearly communicated what was happening each time. We’ve had two major issues at the house that they rolled up their sleeves and helped mitigate the damage before the tech could get out there. They’re just really great tenants.

I had two tenants pay rent before the 1st and one partially pay before. That was surprising since the last two months I’ve had very late payments come through. I still have one person with a partial payment outstanding as of this morning.

We had a water heater go out on Thursday in one property, but otherwise I’m counting all my blessings that we made it through 2 weeks of below freezing without incident.

PERSONAL

I’ve preached monitoring your spending by writing it down for years, but I hadn’t done it. I had done it a few times retroactively, but I never made the time to keep on top of it to make pivots. With Mr. ODA leaving his career, that’s a high six-figure income that we’re without now. I’m working part time, but that’s basically a one-to-one ratio of income to health insurance. I’ve calculated that we need to be about $1350 per month in spending outside of the mandatory bills (e.g., mortgages, utilities, tuition, insurance). My threshold is lower than what Mr. ODA said is his threshold, so this isn’t a hard-and-fast amount, but one that is my “I feel OK if we’re close to this number” concept.

We screwed that up a good bit by purchasing a new vehicle and putting new tires on said vehicle immediately. We also had to pay for a previous heating issue fix in our house and a downpayment on new windows (which, quick side note, are glaringly needed as we go through 2 weeks of single digits and can feel the drafts). I’m also not counting the things that we do as mystery shops since those are effectively reimbursed (sometimes our cost isn’t fully covered since it’s a whole family outing and not a single person, but I’m not drilling down in that detail since I don’t have the specific break down of how Mr. ODA is getting paid). If I take those things out and remove expenses for rentals, then we spent $1597 in January.

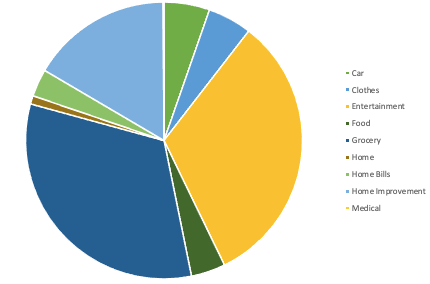

This isn’t the best representation of our spending, but I’ll develop this information as I have comparisons month over month. I also can’t seem to pick a better color scheme without it being a very manual process. Grocery, Entertainment, and Food are our biggest slices there. The entertainment category is basically why I gave up categorizing things years ago. Here I put things like going out for a drink, because while it’s at a restaurant or bar, the sole purpose was to have a drink and hang out. It also includes going to a gymnastics meet with my daughter, my fitbit purchase (I guess because I’m counting it as extra spending and not a necessity), and gift giving costs. We spent $528 on groceries this month, which feels low. I pushed really hard to clear out the food we have in the house already during our 2 weeks of being snowed in, but I hope that this is an accurate representation of monthly spending on groceries.

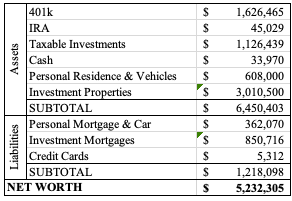

NET WORTH

It is higher than last month, so that’s good. Credit cards are carrying $4500 worth of windows, so it’s nice how low of a balance those are outside of that 0% interest balance we’re holding onto. Our investments struggled a bit over the past month, but the payments on mortgages and loans helped offset that.

In November 2023, I posted about rental changes that had occurred over the previous year. I wanted to update that analysis a few months ago, but I didn’t have all the KY data. I recently shared that my rent increases aren’t covering my cost increases, and my portfolio’s cash projections are lower now than when we first purchased all the houses. Here’s more of a breakdown of those changes per house.

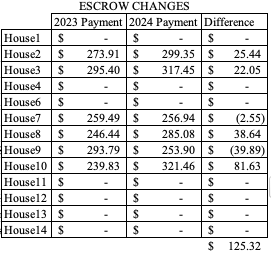

ESCROW

Escrow is an account that your mortgage company holds money to pay your insurance and taxes on your behalf. I have little faith in their management, as I’ve had to follow up on balances in the account and payments made incorrectly.

I created this table to show the differences between escrow payments over the two years. I kept the houses that don’t have an escrow because it can be compared to a future table in this post. There is no House5 in this table because we sold it several years ago (houses didn’t get renumbered because House5 still exists in terms of tax documentation).

INSURANCE

We had 3 insurance claims last year, and a big one the year before. It turns out, our portfolio is looked at as a whole, so 4 claims in a 12 month period doesn’t look good, especially when one of those was 6 digits and one was 5 digits. None of it was egregious, and they were each necessary. We were just a victim of poor timing (and for some reason, the 12 years prior to that with 0 claims of any kind mean absolutely nothing). While our own history is to blame in some aspects, insurance costs as a whole are increasing quickly over the few years. Here’s Google’s AI response:

And with that between payments made in 2023 and payments made in 2024, insurance is costing us almost $2,000 more for the year. I also just made my first 2025 payment, which increased that one house by $343. The total increase from 2022 and 2024 is over $3,000.

From the initiation of insurance on each house (so, when we first bought the house, which were mostly between 2015/2016) to today, we’re paying over 43% more in total for insurance.

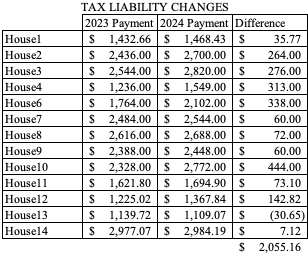

TAXES

The table below shows the change between 2023 and 2024 for our tax payments. Last year, many jurisdictions that hadn’t captured the assessment changes since the pandemic made up for it last year, when we saw about a $3,500 increase for the year. This year, our increase was over $2,000. Fifty-five hundred over two years is nearly $230 per month, spread over 13 rental properties is $17 each. So for those that I didn’t increase rent last year, they’re not capturing that cost increase for our portfolio.

RENT INCREASES

So far this year, I’ve missed two opportunities to increase rent. I had planned on increasing one house by $25 to keep up with inflation costs, but it didn’t register that their notice had to be given by 1/1 (every one else is by the end of the month). The second is above market at this time, which was by design since they’re not easy to work with (tried to phase them out, but they accepted the rent increase). We last raised their rent in September 2022, so it’s been two years. But I couldn’t bring myself to do it. Next year we’ll increase them by $50 per month.

My plan is to increase the rent for 5 of our other houses. Four of these houses are planned to be $50 per month of an increase, and one is planned to be $75. Our management is generally to increase rent by $50 every two years if you’re a long term renter. There have been a few that we didn’t increase for a while, and the carrying costs have drastically increased, so we’re behind now.

SUMMARY

For our cost increases between taxes and insurance, we have over $4,000 that was paid out last year (and it’s really more than that in cases where the house has escrow, so our escrow was increased more drastically that the specific amount of change in bills).

We had 3 houses turnover from long term tenants, so we were able to increase the rent to market value. I prioritize keeping long term tenants, so I don’t always do rent increases. That means that sometimes the rent is stuck below market value, but I’d rather keep a good tenant than push them out with large annual rent increases.

By bringing those houses up to market rent, I’ve made up a good amount of our deficit. Now remember, these rent increases are catching up on multiple years of drastic increases. So even though it seems we’ve brought in more, we’re both making up for previous years that didn’t have such large rent increases and paying for more large scale improvements to these houses, in addition to larger contractor costs.

Every once in a while, I like to share what I’ve been doing to manage the properties. There was a lot of activity needed over the last two months.

RENT INCOME

One of our usual suspects for late rent payments was late again. We seem to only have a one-month streak for on-time payments with them. She at least communicates with us that they’ll be late and gives a projection on when we’ll see it. She ended up paying rent on the 14th, and said she needed to pay the late fee on the 21st.

Two other houses haven’t paid rent, but they’ve applied for rental assistance.

RENT RELIEF PROGRAM

House2 applied for rent assistance in September, and we still haven’t received that from the State. I did finally get a tracking number on the 19th that it’s on its way. She paid $400 worth of January’s rent on a Friday and said she’d have the rest on Monday. Well, as she has a history of not communicating and not upholding her word, I wasn’t taking a chance with her. I served her the default notice on Saturday to indicate that she didn’t pay rent in full and had 14 days to remedy that. She remedied that by applying for rental assistance again. She said that she only applied for January assistance, so hopefully we’ll have February rent on time. I wish I could dig into her finances and find out how she didn’t have to pay any rent for September, October, or November, only had to pay $600 towards December because she had a credit from a payment plan previously in place, and then can’t pay January rent in full.

House3 had to apply for rent assistance. They’re great tenants and have been with us since we purchased the house. In November, she applied for December, January, and February assistance. The application expires 45 days after it’s sent, as a means to protect the landlord from floating the expenses on the property indefinitely. This tenant ended up paying December’s rent, but hasn’t paid anything towards January. Luckily, we did receive approval for their application on January 11. Hopefully we’ll receive that money in less than 3 months time like the last time this program was involved. What she paid in December will be counted as March’s rent (2021 income for tax purposes, but she won’t pay March rent because she has that credit now).

REFINANCES & MORTGAGES

We had to provide several post-closing documents on the refinances. It was horrendous. They asked for new types of documentation. Clearly, whoever is purchasing our loans didn’t like the lack of due diligence done pre-closing. Except for the new request, everything else they requested could have been ascertained by looking at the documentation already on hand, so we didn’t appreciate that. Then the new request was to explain how we paid off a mortgage, which was paid off 4 months prior to us establishing a relationship with this company to refinance the other loans. I had to provide proof that it was paid off, and then I had to provide the funds used to pay it off. The balance was $3,100. Paying a $3k bill hardly touches our finances. I want to become an underwriter so I can understand how they need so much detail and are sticklers for the type of detail, but they don’t need to know how to read the details they request.

We had an escrow analysis done on House7. It said that our mortgage was going to increase by $183 each month, but the increase should have been just about $60. I’ll explain details in another post, but that took some time. Mr. ODA called and walked the representative through the error. He said it took a while for her to get there, and we’re awaiting an update.

Since our refinances occurred at the end of the year, and all our city tax payments are due in January, I was nervous about the right amounts getting paid. The initial closing disclosures had the old tax payment amounts on it, but every one had increased. I was able to catch it and request that they be updated before our closing, but it was a day or two before closing. I was afraid it wouldn’t catch correctly. I had to stay on top of the payments and make sure they were all paid in full, and I had to pay the property taxes for those that aren’t escrowed. I was most worried about the three properties that were being refinanced, but then the issue ended up being one of our other houses. The escrow check was sent on 12/21, and it still hadn’t processed as of the tax due date of 1/14. I sent an email to the finance office hopefully showing that I had done my due diligence timely. Luckily, when I checked on 1/20, the taxes were processed by then.

LEASE MANAGEMENT

We require action from the tenant no later than 60 days from the end of their lease. There are 3 properties that have an April 30 lease term expiration. One tenant already reached out and asked to renew their lease. They’ve already been there for two years, and their rent has remained steady at $1300. We have precedent of increasing long-term tenant rent every 2 years by $50 (but we also have precedent of not actively managing houses and not increasing the rent at all.. oops). I explained to this tenant how there have been several increases in our expenses over the last two years. They’re really great tenants, and they hardly ever ask for anything from us. I felt guilty, but we’re trying to run a business, so we need to take care of that side too. Plus, if we didn’t increase slightly this coming year, it’ll be hard to manage future increases. It’s a lot harder to keep a good tenant if you don’t raise their rent and then hit them with $100-$200 increase down the road, so it’s best to keep with inflation. I did the cash-on-cash analysis for this property and discovered that the $50 increase falls slightly short of our expenses and keeping our rate of return the same.

I have to work with two other houses (via a property manager on those) to determine their new rent amount. One house negotiated a lower rent for a longer lease term at their lease initiation, which was October 1, 2019. This property in particular has had the highest jump in taxes. We grieved them to no avail. They’re claiming our neighborhood is part of a more affluent neighborhood and refuse to see how their district lines aren’t accurate for the type of house and street it’s on. I plan to push for an increase of $75 on that one, since their original lease amount is based on a discounted rate. One the other house, the tenants wield a lot of power to our property manager. We tried to increase rent last year, and the tenant flipped out on us about it. We’re already below what we thought market value was on the house, so 2.5 years without an increase is insult to injury. I’m going to request an increase from $875 to $950 on the house and see what the property manager says. If she agrees to a $50 increase, that’d be acceptable, but it’d be nice to recoup some of the other expenses too.

EXPENSES

We have a tenant in one of our houses that is amazing. He treats the house as if he’s the owner. He’s quick to take care of problems, and only seems to let us know when it gets to be a certain level of problem. This house has always had a mice problem. One tenant, who we evicted, created a really big problem that involved several mice making this house their home. She refused to do her part in cleaning up food messes, be it old food sitting on the counter or in the sink, grease splattered all over, or just general mess left behind. We got it under control, but the occasional mouse still rears its head. He sent us an email saying he’s been having an issue, and he’s tried really hard to address each individual mouse appearance. He said it has gotten to the point where he wants to do something more drastic, but wanted our permission. I said that it was absolutely at the point where it’s our issue to deal with, not his, but we thank him for his efforts. I called our pest control company, and we’ll see if that helps. One or two mice is one thing, but for him to say he’s caught 9 in a year, that’s a bit much. The pest control was $165.

One of our KY houses has a bunch of little and weird expenses pop up. This month’s explanation on my report from the property manager simply said “Repaired door by adjusting door to fit opening and resetting stuck plates.” I don’t know what door or how the plates got stuck, but I threw in the towel on that $60.

We were also informed that a toilet at another property stopped flushing. When asked for more detail, we were told that she presses the handle and nothing happens. My response? “Please don’t tell me I’m going to have to spend $125 for someone to reconnect a chain.” Our property manager’s husband said he’ll go look at it, for $80. That’s a downside to not living near the property and being able to check on the issue yourself. We got a text later saying that he talked the tenant through the issue, and it turned out that the flapper was just stuck. So luckily it’s nothing at the moment, but it could be an expense down the road.

SUMMARY

So that was a lot for one month. Luckily, our expenses themselves were low (225), even though we’re missing some rental income ($1,900 and $145 worth of a late fee) and we had to do more management than usual. By having 12 properties, late rent payments or non-existent payments don’t create a strain on our finances. For example, if we only had House2, who paid $1550 worth of 5 months of rent because of the rent relief assistance program, then we’d be floating those mortgages each month. By having more houses, those other rents are covering the expenses on the one house.

In 4 weeks time, a ‘full time job’ would be 160 hours of work. I estimate that all the action that I took this month (and the phone call Mr. ODA had to make to our bank on the escrow issue) comes out to about 6 hours. There’s the perspective. Even when it seems like a lot, because it’s more than nothing, it’s still hardly anything.

This house was purchased in 2018, and it was actually purchased by our Realtor and friend, under the plan that we would formalize the partnership after closing. Mr. ODA had been searching for another investment property, but we had 10 mortgages already (9 investment properties and our personal home), which is a Fannie Mae cap (see the Selling Guide, section B2-2-03). One of our loans was a commercial loan, and we had hoped that it didn’t count against the 10 mortgage limit, but it did. Fannie says that the cap is the number of properties being financed, regardless of type, when looking to originate a new loan. Our Realtor had one rental property on his own and had mentioned how he wanted to purchase more properties to create an income stream through that option.

Mr. ODA and our partner went to see the house without me in March 2018. After the initial visit to see the house, they requested the information for the tenant that was living there. We received their applications, current lease, move in check list, and rent roll. They had started living there October 1, 2015, and while they had been late, they had always eventually paid rent with the late fee. During some of our initial searches, we had someone tell us that rent on the 6th was more profitable because they’re pay with a late fee. While we don’t encourage late payments (and we’re actually really lenient with late fees in general), this eased our tension when we saw late payments.

The house is a 4 bedroom, 2 bath, with a fully finished basement. The condition of the house was probably slightly lower than what I would have accepted based on the pictures, but I hadn’t seen the house in person. I actually had only seen one room of this house before our walkthroughs this past July. Our partner and Mr. ODA said that the pictures didn’t do the house justice, and it was worth purchasing.

After our partner purchased the house in April 2018, we established a Limited Liability Corporation (LLC). My last post goes through the details of why we established an LLC for joint ownership, but we don’t use LLCs for our personally owned properties at this point.

LOAN TERMS

We requested three different options for the mortgage numbers: A) 20 year fixed with 20% down was 5.125%; B) 20 year fixed with 25% down was 4.75%; or C) 30 year fixed with 25% down was 4.875%.

All of the options included ‘points’ without us being told upfront or requesting it. We questioned the reason for the quotes having these points and were given a half-hearted response that sounded sketchy. We ended up with a 30 year fixed, no points, and a rate of 4.875%. There wasn’t an incentive to go with a shorter loan (and therefore a higher payment each month) at a higher rate just to put 20% down. We went for the 30 year instead of the 20 year to increase our cash flow opportunity since we have a partner on the house and are only getting 50% of the income and taxable expenses.

PARTNERSHIP

Our partnership actually started with a loan for the down payment of this house. Mr. ODA and our partner agreed to allow us to pay him back over time for our 50% of the closing costs. We didn’t have the amount needed liquid, but we knew we could make up the amount owed over a short period of time instead of liquidating money from our investment accounts. We were able to pay most of what was needed for his closing, but we “took” a loan from him for $8,000. I used a loan agreement template that I found online and manipulated it for our purposes.

We established the loan terms to be the same as the mortgage he was entering into (4.875%). Most personal loans are for five years, so we chose that timeframe, even though we knew we’d pay it off much earlier than that. We could have just agreed to the terms and not documented it based on our relationship, but I’ve always felt better having things overly documented. I was basically an auditor in my career, and I’ve seen how “gentlemen’s agreements” over rental-related things haven’t worked out. I formalized the process through this contract and had all of us sign it. While the contract was mostly for our partner’s benefit (to make sure we paid him and he received interest), this was the only documentation we had that once he closed on the house, he then had to give us 50% share of the property ownership.

I established a simple amortization schedule through Excel’s templates. We established the loan terms as 5 years (60 months) at 4.875% (same as the mortgage being executed). When I made extra payments to him, I logged them in the spreadsheet. We only made two payments to him, but he made $44 for not having to do anything except accept our money. 🙂

We had to establish an LLC to be able to claim the tax benefits on this house for our 50% share. The attorney required us to have the tenants acknowledge the transfer of ownership to the LLC since we hadn’t executed a new lease in our names. The attorney then took care of the establishment of the LLC with the State and transferring the deed of this house to the LLC.

RENT COLLECTION

We’ve had the same tenants since we purchased the house. We inherited the tenants, who had moved in 2.5 years before we purchased it, and had rent established at $1300.

As a reminder, we purchased the house in April 2018. They paid that July’s rent late, and despite reminders about the late fee, they didn’t pay it. And so began this constant story with them. The main frustration was that they wouldn’t tell us to expect rent to be late, so we kept having to follow up with them. After two months in a row of it being late at the beginning of 2019, Mr. ODA actually explicitly said: In the future, it’s better to communicate issues with rent payment up front to see if there’s an opportunity for us to work with you. We had been lenient and informally requesting the status of rent, but this was their warning that we’d be sending notices of default going forward.

In January 2021, we hit a wall with rent payment. I sent the notice of default on the 6th of the month like usual. However, because of the pandemic, I had to adjust my verbiage to highlight all the rent relief options available and remove the late fee requirement. My understanding is that a late fee can still be collected in Virginia, but I can’t proceed with eviction just because they don’t pay the late fee portion (which isn’t something we’ve ever held any tenant to regardless). While the rent payment is typically due within 5 days from notice, Virginia now required me to give them 14 days to request a payment plan or pay rent owed. We then had to text and email them several times and never got a response. I finally sent an email with the following at the beginning:

We are very flexible landlords and willing to work with all our tenants. However, we are unable to work with anyone who does not preemptively share possible rent payment delays nor respond to requests for information. Please respond to this email by noon Sunday January 24, 2021 or pay the rent owed by that deadline to prevent proceedings for eviction filing with the court.

Virginia was very lenient with rent payment throughout the pandemic, but they were also fair. The lack of response from a tenant or the tenant not working with the landlord didn’t protect them from eviction. I finally got a response that the rent would be paid that week.

Since then, we’ve been told that rent will be late. We’re simply sent an email that says “you’ll receive rent on 2/12. Sorry for the inconvenience.” It’s as if they feel they have the upper hand and control. We hadn’t received any late fees until I finally sent an email in response to their “you’ll receive rent when we get to it” email for August’s rent that there’s a late fee due.

In 3 years, they’ve been late 14 times. When I put it in that perspective, it doesn’t seem that bad. In the moment, it seems like it’s a constant battle with this house. That’s probably because a majority of our houses pay rent without making it a painful process!

RENT INCREASE

We hadn’t raised rent in the 3 years we owned the house, and they had been paying $1300 since they moved in on October 1, 2015. That’s a great deal for them! Depending on our ownership costs, we would typically look at raising rent every 2 years, and likely around $50. We’ve raised the rent on only 2 tenant-occupied houses we have (meaning, raised the rent on people who continued living there, versus raising it between tenants); both were rented under market value when we inherited the house, and both have received a $50 increase every two years. We typically raise the rent during vacancy times, which has worked out pretty well for most of our other properties.

For a 4 bedroom and 2 bath house, $1300 is low. We mulled over our options. The house is currently on an October 1st renewal, which is a poor time to be looking for new tenants. I wanted to get the house on a spring lease moving forward. My original proposal to our partner and Mr. ODA was to offer them a 6 month lease (ending 3/31/22) at $1400. Our partner said we should include our expectation that we’ll be raising the rent to $1500 for a year long renewal as of 4/1/22. I struggled for weeks on the verbiage for this double proposal. Eventually, Mr. ODA said we should just risk it. We should lay out an 18 month lease at $1450 to split the difference, and if they don’t want it, they can leave or attempt to negotiate.

We offered them just that, and they accepted. Of course, true to form, they were a week late in meeting the deadline to sign the selection that they want to continue living there at the increased amount. Now the rent will be $1450 as of October 1, 2021, and their lease will run through March 31, 2023.

MAINTENANCE

We started with a clogged drain right off the bat. We had our partner go over there and try to unclog it with store-bought items, but it didn’t work. We ended up hiring a plumber for $300 to work on it. We’ve had several plumbing issues in this house, including a clogged sink that backed up and flooded the kitchen and basement. We ended up needing to have the line jet blasted and a camera put through it for $550! This plumber’s quote for the ‘fix’ was $6k. Mr. ODA sent the video footage to another plumber, and that guy said he didn’t see that anything was needed, so we didn’t proceed with the ‘fix.’ The jet blasting appears to have worked, and we haven’t had any damage reported. The other plumbing issues included fixing leaks in the basement bathroom and replacing that toilet.

The inspection didn’t identify active leaking on the roof, but our insurance company was hounding us over the condition of it. We ended up sending our roofer out there to do the items that came up on the inspection report. This was $350.

We then had several more issues with the roof that cost us $125 before we just decided to replace it. The replacement was quoted at $5,500 and surprisingly that’s what we paid. We expected to have additional costs for plywood replacement due to all the damage we had seen.

Interestingly, while not communicating about rent nor paying rent, they felt the need to tell us the washing machine wasn’t working. We ended up replacing the washing machine for them. We try to not supply any non-required appliances because then it’s on us to fix them or replace them, but since the tenants already lived there when we bought the house, we inherited that the washer and dryer are our responsibility. More interestingly, as I was writing this post and going through my receipts, it dawned on me that the washing machine that was in the house when I did my walkthrough last month isn’t the one that we just sent them in February.

While collecting rent has been frustrating with this house, and we’ve had a lot of plumbing and roof expenses, the house is still profitable and worth our investment. The house is in an area of Richmond that’s being revitalized, yet at the same time it’s in its own pocket of the city that’s also protected from big changes and is mostly original owners. Appreciation has really taken off, so even though our maintenance issues have eaten big chunks out of our cash flow, this house will be well worth it when we eventually sell it and move on to a new investment.