I grew up in a middle class household; my dad set us up with a system to understand the value of a dollar at a young age.

Our allowance each week was a dollar. (Hey, that’s the name of this blog)

We had our typical household chores, and expectations were set early on that straight A’s were the expectation in school. Since we weren’t rewarded for specific actions, like getting good grades, allowance was how we got our money.

It came with a catch.

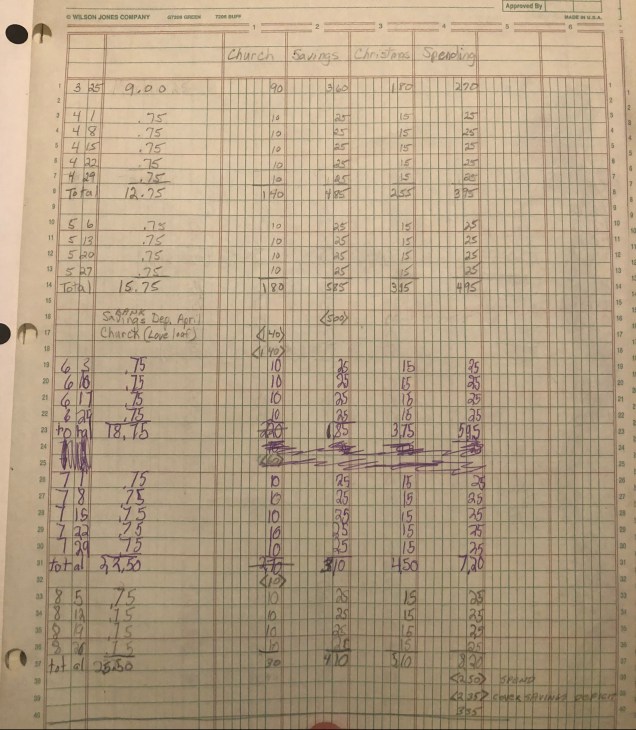

Each dollar had to be split into 4 categories. Each of these categories had to be logged in an accounting ledger book that my dad provided, to keep a running total of the balance. Categories were:

- Savings

- Tithing (Church)

- Christmas gift savings

- And the leftover: free spending

(Dad setting the template for how to track)

As you might imagine, these categories didn’t grow quickly – 35 cents in spending per week doesn’t buy you much! So it made us learn what was valuable and “worth it” when it came to spending our money.

Who knew that as an 8 year old, I was learning what it meant to be frugal, assign value to any purchase I made, and establish the difference between needs and wants.

As much as we complained about this forced treatment of money at the time, laughed about it when we went on to get our own high school jobs, and look back at it as a family now that we’re adults, this household policy was the single most important thing that shaped my philosophy on finances in my life.

I was just talking about it with my brother: “ah, memories of learning how to split a nickel!”

(Me trying my hand at tracking; with some mistakes and fascinating hand writing!)

This was reinforced in the way my parents handled their own finances – a high savings rate, smart spending, and strategizing for their whole family’s future.