We’re in a market downturn. These are expected, happen fairly frequently, and contain strategies to efficiently optimize the times they happen. One of those strategies is tax loss harvesting.

This year, we “benefit” even more from this strategy because the downturn is happening at the end of the year, at a time when savvy personal finance folks are thinking about all the varying ways they can reduce their tax liability for the closing year.

For the last decade, we’ve been in an uncommonly long and strong bull market, so many young people have no experience adapting to a struggling market and understanding ways to harness the red numbers.

Tax loss harvesting involves selling shares of a “losing” stock, fund, bond, etc and immediately purchasing a similar asset that’s “on sale” to maintain exposure to the market, hopefully buy at the low point, and prepare yourself for the eventual market upturn.

You cannot sell and buy the same stock or fund in this process because that would invoke the “wash sale” rule that disallows claiming capital losses. If you re-buy after thirty days, it’s no longer considered a wash sale.

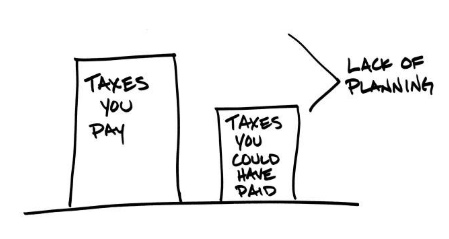

The reason for utilizing this strategy is to be able to write off capital losses on taxes come April. This could offset earned income, other capital gains, dividends, passive income streams, etc. Paying fewer taxes is the goal, always, right?!

It could even have the double benefit of allowing you to get rid of a stock that doesn’t have a bright future in exchange for one that you think might be better.

Minor issue

One caveat to this strategy: you’ve now placed yourself in a lower dollar value cost basis in the new security you’ve purchased. When you choose to sell that, you’ll be subject to higher capital gains amounts. There are strategies to minimize that too. Tax gains harvesting is something people frequently employ. You do this in a year where your taxable income is lower (preferably below the $77,400 married filing jointly threshold for 2018) so that you can pay less or zero in capital gains taxes.

My circumstances

Personally, with Mrs. One Dollar Allowance quitting her job in 2019 to focus on child rearing and managing our rental properties, this year should be the highest tax liability we have in quite some time. Harvesting our losses this week will have a more substantial effect than it would in future down years, and will make the availability for tax gain harvesting in future up years more “profitable.”

Good luck to everyone in this tumultuous holiday week. Shutdowns and market losses don’t lend to great things on the news, but at least this strategy can add a silver lining to your end of the year tax decisions.