March is always a crazy month. Busy is an understatement. Baseball starts, which means we’re at the field 2-4 times a week. Our extended family has a lot of birthdays, which includes the 3 of our immediate family. We had a freak snow storm on St. Patrick’s day. The city went into gridlock. Everything was ice and cars were sliding down any hill anywhere in the city. The kids were off from school, and our dog hit a wall in health unexpectedly, and we said our goodbyes that day. It’s been quite the month.

This was a milestone birthday for me, and Mr. ODA threw a big party. That’s outside my comfort zone, but it was amazing. For that reason, I’m not going through March expenses because I really don’t want to know what he spent on me. It felt like we were spending left and right all month long, but our credit card payments have tracked as usual.

On top of all the usual things, the kids had a skating session in gym for 6 weeks. Volunteers come in for assistance, especially with the younger grades who need help even standing up. Last year, I did one session. This year, I couldn’t make it to the first one, but both kids expected me at all the other sessions, and so I did. I think it’s so cool that they get to do that at school. We also had an event for 1st graders one night, career day, and my volunteering to manage the lost and found.

We went on a spring break trip to Kansas City. I have a separate post about that coming later, but it was a pretty low cost trip, and we just explored the city.

RENTALS

A tenant moved out on April 1. She had been hemming and hawing for years about moving out because her child’s father was going to get a place with them, but things kept falling through. She finally gave a final notice, but then back tracked saying instead of January 31, she would stay through March. She did a great job moving out. I expected things left behind, or a mess of some sort, but it was great. The carpet is well past its useful life, so we’re replacing that. The walls are gross, so we’re painting everything. Actually, it turns out that painting a one story ranch is significantly easier and less overwhelming than any other house we’ve painted. Mr. ODA is worried about timing, but I’m feeling good about it. We lost a week to spring break, but from carpet measurement to install is projected to be less than a week, so that’s great. We also have an applicant in the wings that we’re working through right now, so hopefully we’ll be down for one month.

We finished our taxes, which included verifying expenses last year. We were able to claim some costs in full instead of depreciate them this year, so that was a nice way to recoup that improvement. I’ve been working on rent increases, and there’s a big batch of renewals that need notification before the end of this month.

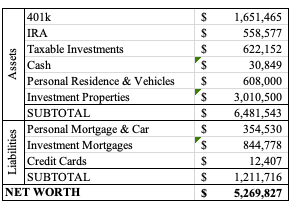

NET WORTH

I’m still struggling getting a few accounts updated since I changed my phone number in November. So this is not a completely accurate representation of our funds, but it’s pretty close. I can’t get into my retirement account, which is a significant chunk of money, so that estimate could be off by a bit.

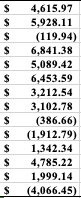

Our credit cards are a bit higher because we paid for carpet replacement in the rental. We also had to pay homeowners insurance on a few properties, and I always pay with credit card when I can so we get 2% back.

We also paid a chunk towards our new van loan. We had financed it to get $1000 off the purchase price. I have an earlier post that dug through those numbers to see why it was worth the few months of interest to get that price reduction.

Overall, our net worth went up from last month, so that’s a win.