We have been financially secure for Mr. ODA to quit working for years. In fact, the plan was that after he met the requirements for his paternity leave taken (which was essentially work the number of hours you took as leave), he would quit. That goal was met back in early 2023. The hold up for him quitting was always health insurance. Him working wasn’t a huge detriment to our life and things we wanted to do, and he was getting most of his health insurance cost covered by his employer.

Well, at the beginning of 2025, the deferred resignation program was introduced. While the first round was very questionable, our life was greatly affected by his employment and the government over the next few weeks, so it was a no-brainer to take the program during the second round. His last day of work was at the end of April, but he was considered employed and paid through September 30th.

As part of his separation, his health insurance was covered for about another month. He had the option to extend his current insurance for another 18 months after that, and that he’d be responsible for paying the full premium. At the time, it was about $1700, and the 2026 premium is $1900 per month.

MRS. ODA’S INSURANCE OPTION

Meanwhile (just coincidental timing), my current employer was investigating a new insurance policy for their employees across 4 offices. They were originating their insurance through the Ohio office. It was a really expensive policy for them. For the 5 people who were taking advantage of that insurance policy, they could have covered 23 employees on this new policy. We learned that Ohio is one of the most expensive states to originate insurance out of it, so we moved the policy to Kentucky.

Anyway, through that process, the insurance sales person was completely incapable of answering basic insurance type questions. Mr. ODA asked for the brochure of benefits. He said, “I emailed you the summary of benefits.” Mr. ODA pointed out that the summary of benefits was a summary of a much larger document, and we wanted those details. He said that didn’t exist. Mr. ODA called the actual insurance company, and that lady laughed and said they definitely have that.

The policy also required a gap coverage policy. The information given to me did not make me feel like it was going to be a smooth process. It sounded like the doctor’s office would submit the claim to my main insurance company. Once it was processed, I’d have to take my bill and EOB and submit it to the gap coverage company for payment. So I’d have to manage the paperwork processing and the payments between everyone.

Their quote for the family policy was about $1750. I told Mr. ODA that it wasn’t worth all that extra effort and the concern that this insurance policy would even work right (because this sales person was not able to answer questions or quell concerns), just to save about $150.

FINAL DECISION

So in the end, we decided to keep the enemy we know. All of our doctors are now solidly in place since we’ve been in Lexington for 3.5 years. I didn’t want to risk needing to switch to a different doctors office because of eligibility and coverage. I didn’t want to risk the coverage being a fight even more than my current policy creates. But mostly, in case something did end up going awry with this new policy option, we couldn’t get our old policy back. So while adding $1900 to our monthly expenses while losing Mr. ODA’s income isn’t the most ideal situation, this is where we’re at in life.

On April 6, we submitted our taxes. Honestly, I think that’s the earliest we’ve ever done it. We usually owe a good amount, so there’s no incentive for us to do it early. After owing a penalty last year, we pushed to be on top of the projected tax liability. It looks like we’ll owe a bit on the Federal side and get a refund on the tax side.

And so here’s my annual reminder that if you take the time to manage your finances all year long, then tax season is not a hurdle. I find it much easier to maintain 13 houses worth of data if I do it during the time it’s happening. Life has gotten in the way a bit, and I find it hard to even make sure I have one or two months worth of things logged correctly. I hope to be more on top of it in this coming year.

I have a spreadsheet where I log all our income throughout the year. I set up a formula where I can track each month’s income to ensure I receive the total amount that I expect to receive. I found that since some of our houses pay the same dollar amount of rent, it’s harder for me to mentally track each month’s payments, and I like having the visual and verification through this sheet.

Then there is a tab for each property in that same workbook. The sheets are set up based on monthly expenses, and I plug in projected expenses (e.g., taxes, insurance, utilities). This helps give me a verification that expenses have been paid when owed. By now, I have nearly every invoice emailed to me, but I like having this ‘fail safe’ look at what may be owed that I hadn’t paid in a given month.

Then Mr. ODA enters our investment items, W2 income, and interest income into our tax software. Then I sit down next to him and dictate the numbers from my spreadsheets so he can enter them into the software. We have 13 rental properties, so this is time consuming. However, it’s really easy. We enter our data into the fields for each house. This year took us about 90 minutes to enter the rental property information.

I know multiple people who file extensions because it takes so much time and effort to gather the documents for their accountant to do their taxes. It’s like they don’t think about their taxes until April 1 and then decide it’s too much to do in two weeks. This is where being prepared all year long comes into play. Make it easier on yourself and put yourself in a position where it doesn’t feel overwhelming.

We started getting emails about end of school year activities, and boy was that a surprise that we’re at that point. The middle one is done mid-May and the big kid is done at the end of May. Less than 2 months until summer break.

Mr. ODA took the second round of the government’s offer for administrative leave, which means he would only have a few weeks left working. I’m still working my part time job, which is taking way more hours than we had planned for. I’m enjoying it, but it’s been a juggling act with the family, which is probably why my son who absolutely loves school begged me to stay home because his belly hurt last week.

Buckle up because apparently I have a lot to share this month.

RENTALS

We received about $600 in tax payment reimbursements from one of our localities, so that was a fun surprise this month. Really helps my psyche that I have a tenant who hasn’t fully paid, didn’t tell us why ahead of time, and hasn’t been up front with when she’s going to actually pay us.

I executed 2 short term leases. Both included a rent increase for their short term period; one house is increased by $75 and the other by $25. Luckily, both are here in the Central KY area, so we can flip it between tenants. One is scheduled to leave June 30th. That house will need new carpet in the bedrooms, and it’ll need probably a whole-house paint job again. They smoked in there, even though we covered the lack of smoking rule multiple times. I’d be more upset about it if the carpet hadn’t reached its useful life years ago. The other house leaves July 31, and I can’t even tell you where we’ll need to begin with that one. She made a wood feature wall without permission. She had a giant fish tank without permission. She spent a lot of time doing things that really weren’t an improvement, so I’m definitely worried about what we’re going to uncover in that house. Mr. ODA and I are talking about fixing it up and selling it. We may look for a short term renter so that we can sell it in the Spring instead of this Fall.

I had 2 other properties accept a rent increase that will go into effect later this year. I require 60 days notice for changes so that starting at the 30 day mark I can begin advertising it if needed. One house goes up by $25 per month as of June 1, and the other goes up by $50 per month as of July 1. I also have another property that has a rent increase of $50 per month going into effect next month.

I have 4 houses that renewed another year, and I didn’t change their monthly rent rate. There are 4 more houses that haven’t been discussed. My intent is to have them renew for a year at their current rate. There are 2 of those 4 that could leave at the end of this term, but time will tell.

We have multiple maintenance issues to address. One house requires a tree trimmed off the roof, the siding cleaned, and the back deck stained/painted. We still have termite damage we’re dealing with at a house in Richmond. I have a leaking toilet that was just addressed, and then they hit me with a faulty HVAC unit during a heat wave. Then we have some houses that really need eyes on them to see what condition they’re in at some point this summer back in Richmond. It’s amazing to me how people just don’t care to tell a landlord that something is broken. I woke up this morning to a text that one of the houses here has a flooded basement due to a water heater failure.

I spent some more time fighting my insurance guy here. It irks me so much when I see him offer up his services on the local facebook group for property owners. He’s quite terrible. I sent him photos of a house that had some issues with a cluttered backyard and had the tenant clean that up. I had to fight him last month on an increase where he changed one house from a crawl space to a basement when I assure you that the vines growing through the windows solidify it should not be deemed a “basement.” When the dust settled from that debacle that he was insanely unresponsive to, I ended up owing $9.68. When I asked why my account wasn’t put back the way it was found before this mess he created, he said he didn’t know but it’s probably from the audit and changing square footage. HIs guessing and not actually answering infuriated me. I gave up and paid it, but then I ran to get quotes from other people. I hadn’t done that before because our 4 claims in a 12 months period are killing us (again, because I really wanted trees to fall on us!). I hate when people make the claim that because it’s not a lot of money, I should just give up and accept it. That’s a ridiculous way to treat people.

PERSONAL

Our electric bill is almost double what it was this time last year thanks to the vehicle charging and hot tub. Our electric bill is relatively low, so that’s not all that surprising. We also have 5 full people in this house now (as much as you can count a 2 year old as a full person… but he knows how to control light switches and eats a ton of food that we need to cook him, so I’m sure he’s a factor there!).

I’ve been working at my new part time job for over a month now. Mr. ODA was making fun of my hourly rate, but I’ll tell ya, it felt good to receive a paycheck that wasn’t $45 like it was for a day of subbing at the preschool.

I took the kids to get haircuts. My middle has had her hair cut once before, but I’ve cut the boys’ hair forever. I had family coming into town and the oldest was looking really shaggy. So I swallowed my pride and threw money at the problem, which is very out of character in this household. I just didn’t have the time to cut their hair, clean them, and clean up the mess. For $66 and 45 minutes from the time I left home until I got back, it was well worth it to me.

I had a medical procedure done this month. We haven’t met our deductible. In February, they said I had to pay my deductible to them. I said that didn’t make sense and refused to have them hold $2800 of my money for 2 months. They gave me an attitude and said I could never ever ever ask for a payment plan in the future, so that I could pay $500 to hold the date. I then showed up for the procedure, knowing I haven’t met my deductible, and they didn’t take any money from me. Another business model that bullies the customer into illogical money decisions. I also had an eye doctor appointment that was frustrating in itself, but I’ll spare you those insurance and communication details.

On top of everything else I’m juggling, Mr. ODA is coaching our kids’ t-ball team. Coaching means that I am team mom. That means that I’m responsible for communicating updates from the league (in the slow and haphazard fashion I receive information), gather value card sales that are required of every team member, organizing a basket for a raffle, and the best one – raising $350 for team sponsorship. What the heck, man?! Where did I say that my signing up of two children to play in the league means I have history or ability to gather money from businesses?? Well, I did it. I raised $350 and another mom raised $200 for the team.

No financial impact, but I’m also juggling our HOA board duties. I released our longstanding property manager and hired a new company, which took effect April 1. That’s taken a lot of time to get them stood up and make sure we stay on track for our annual meeting schedule in June.

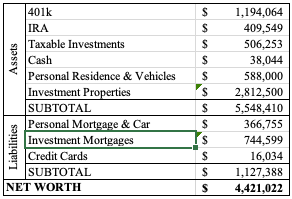

NET WORTH

And with all of that said, that doesn’t even address the giant reduction in our investments that continues to happen. To counter some of the loss, I updated our property values for our houses. I don’t do that every month because they don’t move very much, but I can usually count on a few increases as the spring market ramps up. Our net worth did slightly increase (based on yesterday’s market closure, not today’s) from last month, which was a nice surprise.

I wonder why I’m tired and bogged down, but that post outlining what I’ve done recently made me realize all I was able to accomplish even though I felt like I was a jack of all trades and master of none. Hopefully things will settle down in our lives going forward now, even if I know there are definitely two house turnovers in my future.

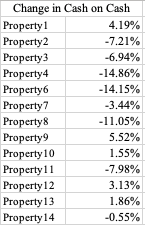

When we consider purchasing a house to be used as a long term rental unit, we perform a “cash on cash” analysis. I’ve discussed this in the past, and I regularly share this with other people for their use. The gist of this calculation is to determine whether we would get a return on the cash put into the house.

The calculation considers the cost of taxes, insurance, homeowners association fees, vacancy expectation, maintenance expectation, costs to get the place rented, property management, etc. This is compared to the projected rental income. The upfront costs are compared to the annual cash flow projection. That ratio is hopefully in the 8%-10% range to be considered a reasonable cash flow to look further into the purchase.

Since we’re not really looking to purchase properties these days, I use this spreadsheet to consider changes in a tenant’s rent when it’s time for renewal. I kept all the original cash flow amounts to see how things change over the years. As I sat down to determine what changes, if any, are needed in the rents I charge, it was disheartening to see how our portfolio has dwindled in profitability over the years.

A few years back, housing prices skyrocketed, which drastically increased our taxes owed. Unfortunately, I hadn’t increased everyone’s rent consistently. I kept many people level or did small increases every two years, but that means I’m now “behind the 8 ball” in trying to make up for those drastic increases that happened in 2021-2022. In addition to tax increases, we’ve also seen huge insurance premium increases that weren’t projected in our portfolio.

Our total “cash on cash” started at 11.42%. It’s now projected to be 7.58% – if the increases I project actually go into effect over the next few months.

We historically increased long term tenant’s rent by $50 every two years. Some of these tenants have been with us for over 5 years, and the $100-200 changes in their rent have not covered the increases we’ve seen. I hadn’t worried too much about it because the losses on those houses were offset by houses where we saw greater margins. Now, everything has leveled out, so those losses are felt harder.

The table above shows the change from our original “cash on cash” to our current status. In some instances, we’ve been able to increase our margins. But there are 8 instances our margins decreased, with some being drastic. Even though some are drastic decreases, there are only 5 properties that fall below the 8% goal we have.

For Property2, the projection shows that rent would need to be at $2,500 for us to hit our cash flow goal. The rent is currently at $1,600. The neighborhood doesn’t call for $2,500. I also don’t want to be in a position where I’m floating someone’s rent at that price. From the time we bought the house to now, our taxes and insurance have increased by $1575. That number only continues to grow. Our insurance started at $390 and is now at $765. Our taxes started at $1,500 and are now at $2,700.

On top of the obvious ones like that, our maintenance costs have also increased. As one example, our HVAC technician first was charging $125 per site visit. He now charges $325 just to show up. I’ve found someone who charges $200, so I’ve been going with that guy, but just knowing that there’s been such a change in pricing structure needs to be factored into our costs.

These are really big affects on our houses that a tenant and the average public opinion don’t seem to grasp. I don’t get paid hourly or per transaction I perform to manage these properties, so that decrease of 3.8% in our cash-on-cash analysis is actually a net loss in my “income.” In many cases, we catch up when there’s tenant turnover, but watching the rent compared to our expenses are things that I need to be more on top of year-to-year.

I grew up in a private school setting, and we didn’t have a cafeteria that made us food to purchase. Everyone once in a while, we’d have “pizza day,” where we could bring in a dollar or two and buy pizza that they had delivered from somewhere. My high school had a full cafeteria that prepared breakfast and lunch to purchase. It was a private school, so there weren’t any state subsidies. All that to say, bringing my lunch to school wasn’t even a thought. I packed a lunch and a snack every morning. In 2nd grade, I started doing that for myself and my sisters because my mom was really sick, and it just stuck as a chore I did.

I have a child who just started Kindergarten last month. Since my background was bringing my lunch to school, I expected to pack his lunch too. He’s bought school lunch just once so far, and it was for his birthday. I figure there will be a few days throughout the year that he’ll want to buy lunch, but so far he’s content with my packing it.

Last week, I was volunteering at the school, and another mom said “I don’t bother packing anything. For $2 they get breakfast and $2.75 they get lunch; I can’t make meals for that little.” And so, this post was born. Now, I don’t know the outcome, but my hypothesis is that what I pack for his meal is less than that. So let’s dive in.

BREAKFAST

First, breakfast for my kids nearly every day is cereal. That’s their preference. For all the things we don’t buy name brand, cereal is one we keep name brand. We buy it on sale on Kroger. Mr. ODA likes to stock up, even though he admits that the sales are every other week and we may not need 5 boxes of Honey Nut Cheerios in our pantry at any given time. 🙂

We paid $2 per regular-sized box. The box says a kids serving size will get 12 servings per box. That would come to $0.17 per bowl. Regardless, I do know that $2 per box is less than $2 for one breakfast though.

My kids don’t eat much for breakfast. At home, they have a snack around 10, a hearty lunch, another snack, and then dinner. They’re really good about eating when they’re hungry and not eating when they’re not. Even when my son got free breakfast at the orientation events, he ate a partial bowl of cereal and some fruit. We go through a lot of fruit in this house. But mornings before school don’t have the time to get fruit and cereal into him. I forced it on testing mornings, but he still wanted to eat just the fruit and nothing of more substance, so I had to bribe him.

LUNCH

This is where fruit comes in. We also have fruit as part of the after school snack.

Here are some options that I mix and match throughout the week (though not exhaustive). I’m also taking suggestions!

Yogurt Covered Raisins: $2.97/pack, 6 in a pack = $0.50 each.

Clementines: $3.50 per bag. I’m estimating there’s about 20 in a 3 lb bag. $0.18 each.

Grapes: We purchase these at $0.98-1.98 per pound. At the high end, for what I pack, I’m going to assume $0.20 per serving I give.

Oreos: Family size is $5.28 with maybe 48 cookies (that was a quick google). I put two in his lunch box if I put any at all, so that’s $0.22.

Fruit snacks: Honestly, we have a gigantic box that was given to us at some event, and that’s lasted us since the end of last year’s school year. But I’ll include this cost anyway because eventually I’ll buy more. $15.99 at Costco for 90 = $0.18.

Applesauce pouches: I buy Walmart’s version of this. $5.68 for 12 pouches = $0.47 each.

Peanut butter and jelly sandwich: A jar of peanut butter is $1.94, jelly is $2.74, and bread is $1.42 for 20 slices. The bread is $0.14 per sandwich clearly. The other two are harder to quantify, but both are minimally used per sandwich I make, so let’s say $0.15 total for those, bringing a sandwich to $0.19.

Chicken nuggets: $5.97 for a 32 ounce bag. I have no idea how many are in there. The package says 4 nuggets are a serving and there are 12 servings in the bag, so let’s say there are 48 nuggets. That seems low though. That means each nugget is $0.12.

Pizza: We seem to have pizza once per week, and there always seems to be 1 or 2 slices left over. $4.97 for the pizza, where we get 8 slices, so $0.62.

If I pack a peanut butter and jelly sandwich, grapes, clementine, and oreos, that’s a total of $0.79. Today I put a PBJ, raisins, grapes, and oreos. He actually got 3 oreos because there were only 3 left in the package; that total came to $1.22. Yesterday’s lunch was 7 nuggets, an applesauce pouch, grapes, and a clementine; that came to $1.69 (actually, that doesn’t include the bit of ranch I put in there, so perhaps add a few cents).

The first few weeks of school, I had been putting more food than this in his lunch box. He had told me he was eating everything, but grandparents day had grandma eating with him so she saw he was throwing some things away. I had asked him repeatedly to tell me what he likes or doesn’t, or if there’s not enough or too much food so that we can make adjustments.

There are other things like puffed corn, chips, and cheez-its that I buy for his snack. He eats lunch at 10:30, so they give him a snack in the classroom at 1:30. There’s no option to buy a snack at the school at this time, so everyone needs to pack their own snack.

SUMMARY

By the time my child gets home from school, I’ve spent approximately $1.80 to feed him for breakfast, lunch, and snack. On the high end, it may be about $2.25. This also assumes that the child is happy to eat all the options presented for the meal. When my son bought his lunch, he ate the orange slices, bread, and half the spaghetti. He didn’t touch the broccoli (that I put on his tray for myself), and he didn’t even pick from all the options presented in the cafeteria line. Whereas I know what I’m packing includes things that he eats regularly at home.

While I agree that $2.75 for a meal is cheap relative to buying at a restaurant or fast food, the assumption that it’s cheaper than what you could pack a lunch for doesn’t appear accurate.

Back when I spent my days working in front of a computer, it was easy for me to analyze our spending. These days, with 3 kids in tow, I’m lucky to record our finances timely. There’s no time for analyzing. But over the past two years, I haven’t been happy with our spending total for the year, so it was time to look into it a bit more. It’s hard to know what has changed since I don’t have month over month, or year over year, trends to compare this data to, but it’s a start.

There are some caveats.

I don’t include any spending that isn’t on a credit card here. That means some of our rental property bills aren’t captured (they’re paid via Venmo or check), but I decided that’s ok because I can see that in a different way (a separate spreadsheet). Those expenses are reactive and a necessity to running the business, so it’s not like I can change a spending trend there. I’m more curious about our actual expenses and where our money is going for personal decisions. There will be some rental expenses captured here though.

I’m doing this analysis for the first half of the year. If this was for a month at a time (which is a goal), then I’d be able to dive deeper into spending at each place. For instance, at Walmart, those expenses aren’t always ‘grocery.’ However, I don’t have the time to go through all the purchases and siphon out non-food purchases. I did go through most of the Amazon purchases and categorize them.

If a purchase was made at Lowe’s or Home Depot, it’s classified as home improvement. It may have been rental property work, but generally it’s related to something we’re doing at our house.

If a purchase was made while on vacation (such as amusement park, tolls, hotels, dog sitting) , it’s categorized as ‘vacation.’ If we were on vacation and purchased food, it wasn’t labeled as vacation. All fast food or restaurant purchases for the first half of the year are categorized as ‘restaurant.’

If we did an activity from home, it’s labeled as ‘entertainment.’ If we did something related to sports (this includes swim lessons, ticket purchases for performances, etc.), then it’s labeled as ‘sports.’ The entertainment versus sports delineation is because something like a single tournament could be considered entertainment, but I kept all sports items as ‘sports.’

None of this includes whether we were reimbursed by someone else for a purchase. For example, we purchased tickets for 15 of us to go to an amusement park on vacation, but we only paid for 4 tickets of that personally. Mr. ODA is a personal shopper for restaurants, so much of our restaurant shopping around town is actually later reimbursed in that process (but not captured here because it’s not a credit card line item).

In the process of going line-by-line on my expenses, I discovered that I never received a refund for something. I placed an order on Etsy for a personalized gift for my niece’s birthday. A few days later, I went to check the status of the order, and I discovered that the shop I ordered from was no longer selling on Etsy. I was frustrated that I received no email that told me my order wouldn’t be fulfilled. I contacted Etsy customer service. At the time, I misunderstood Etsy’s billing process. I assumed it was charged when the item shipped. As I was just going through charges, I realized that the amount was charged on the date of purchase (e.g., not when shipped), and I had never received a response from Etsy. After another frustrating round of attempting to contact customer service this morning, I finally received a resolution. Now my ‘to do list’ has to keep track of this refund appearing. It’s $10.01, so it’s not the end of the world. However, it would be nice if Etsy shuts down a seller (their words), that they manage the outstanding orders without me having to take my time to get it corrected. Plus, if I let every “it’s just $10” go, it could add up quickly.

FIRST HALF OF THE YEAR SPENDING

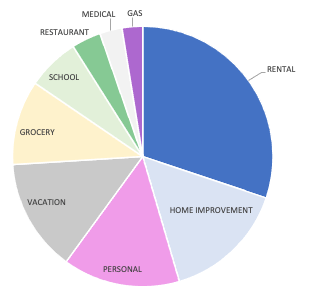

By far, our largest slice of the pie up there is for rental expenses. Honestly, I’m happy to see that so much of our credit card expenses are taken up by rental expenses we had. I pay our insurance premiums (where they aren’t escrowed) via credit card, and I can pay our county taxes for one house with a credit card, which I do for the cash back rewards. There was flooring replaced at one house, which was a significant amount of that slice.

The ‘home improvement’ category includes new patio furniture we purchased, but were reimbursed by insurance (a tree fell on our deck). It also includes the electrician work and dirt fill purchases that we needed for the deck rebuild. Our house has a few more fairly large projects we want to complete, so I expect that to continue being a larger chunk.

I know that our “grocery” expense isn’t completely groceries. I’d like to focus on this category of spending more in the second half of the year. I want to quantify what’s purchased at Walmart that is actually grocery versus personal shopping type purchases. I think that our grocery purchases are higher than they should be, but I can’t put my finger on exactly why. Historically, I’ve blamed it on ‘bulk’ shopping; Mr. ODA will go to Kroger for the “buy 5” type sales. I’m not sure that’s it though.

We don’t eat at restaurants very often. We usually eat at fast food places while we travel or are away from home at an inopportune time. When we’re at home, we’re usually eating at a “personal shopper” experience where our food cost is mostly reimbursed (although that’s not captured in the chart).

Our health insurance deductible is $3,200 per year, so we expect slightly more than that each year in the medical expense category (and based on how deductibles work, that expense is front loaded in the year). I actually pre-paid a bill at a child’s urgent care visit. I paid them $50, but that visit, along with two more visits since then, came to a total of $12. I’m waiting for their reimbursement of that difference.

PERSONAL SPENDING

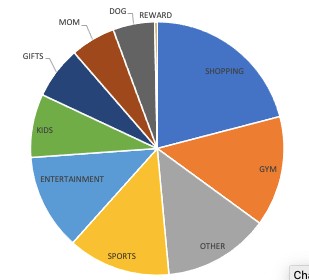

I’m going to dig deeper into the ‘personal’ category. I labeled a bunch of things as ‘personal’ as a means of not having too many small slivers of the overall spending pie. This includes all gifts, needs for kids (new shoes), clothing for kids, gym membership, sports, etc. It includes a ‘shopping’ category. I spent some time going through my Amazon orders and categorizing them, but the ‘shopping’ category was too daunting and difficult to parse out further. About a third of the ‘shopping’ category is Amazon orders through Mr. ODA’s account that I didn’t pull up to categorize. The rest is random purchases that were probably related to gifts or kids clothing.

For entertainment, this is small things like going to the movies (which we go for $2 per ticket), bowling, and aquarium. The largest chunk of this pie part here is actually 4 season pass lift tickets for our family’s future winter season. I put the ‘mom’ category to see what I’ve purchased for myself that wasn’t a necessity (e.g., a travel cosmetic bag, baseball shirts to wear to my son’s games), as well as my one hair cut and one pedicure that I’ve gotten this year so far. The ‘other’ category is boring stuff – utilities, car maintenance, professional fees, etc.

Had I gone through my Walmart orders in detail, I would have been able to identify some more purchases that could be removed from ‘shopping’ and put into other categories. For instance, the ‘dog’ category is actually higher because I order his glucosamine and tooth cleaning treats from Walmart most of the time, and that’s a monthly expense. His annual vet appointment is in the Fall, so this will be a larger slice of the pie for the end of the year.

SUMMARY

Our annual credit card payment total for the last three years have been about the same. While it’s a ‘win,’ that it isn’t increasing, it’s still at a number that I don’t like. Mr. ODA has been working towards a ‘retirement’ date. We’ve pushed it back just because his job hasn’t significantly impeded our lifestyle, but the day will eventually come. If it’s next year, I’d feel better if our credit card payments weren’t as high.

I went into this expecting my grocery category to be higher than I’d prefer. I didn’t identify much of what is causing that, so I’ll try to focus heavily on watching that expense each time it hits the credit card, rather than trying to remember what each purchase entailed six months later.

I was surprised to see the gas category such a small sliver of the pie. We’ve done a lot of trips (although, I suppose a majority were in July, which isn’t captured in this data). It appears living in a smaller city and doing things mostly on this side of town means we’re not having to fill up our tanks too often.

Overall, I didn’t notice any egregious spending. We don’t spend for the sake of spending. This year we traveled more than we had the previous two years, but mostly our spending is the same. Now that we’re two years into our house, there are less projects that we’re putting money towards. I’m encouraged that now that I’m looking at this, I’ll be able to identify areas to scale back.

At the end of last year, I received each property’s revised assessments for 2024 tax purposes. To no surprise, every single property drastically increased. A harder pill to swallow is to see how much it increased just from two years ago.

Higher home sales are great – if you’re in the market to sell. If not, it’s just fueling the local jurisdiction’s ability to increase their tax income. Again, this increase is great for a resale opportunity, but it’s not great when we’re content in our “buy and hold” at the moment.

Where I live, we received our property assessments recently as well. There was an uproar from the citizens. The Property Valuation Administration explained the increases and how they work, noting that home values in our area have exactly doubled since 2014. While their valuation process only occurs every few years, and home prices are increasing about 10% each year, people are seeing 30-50% valuation increases when they receive their notice.

COMPARABLE SALES

When determining a property’s assessed value, whether it’s for tax purposes or a bank loan or such, nearby home sales are used as the basis. Home sales denote what buyers are willing to pay (and likely what an assessor determined as fair market value) for a home. To determine your home value, you would need to look at sales in your neighborhood or close geographic area, for homes (and lots) that are of similar size with a similar number of bedrooms and bathrooms. There are factors that you can use to compensate for a different number of bedrooms and bathrooms, but it’s easiest if you find homes with similar data points.

In today’s market, you’re also going to focus on home sales in very recent months. The amount that a person is willing to pay, and the amount that a bank is willing to loan, is increasing regularly. A home value in 2021 is different than today’s.

HOW DOES A PROPERTY ASSESSMENT AFFECT YOUR RENT?

I wrote a post that went into the details of how our expenses have changed over the last year on these rental houses. It’s noteworthy, as a renter, to be aware of the changes in property assessments because it’ll help you anticipate and understand the need for rent increases that will be coming.

I recently saw someone complain that a landlord was raising rent with no improvements. Rent increases aren’t tied to improving the house (well, they can be). Rent increases are keeping up with the costs that are increasing for the landlord.

I’m a broken record on this, but I’ll continue to work to educate. When you rent a house, you see the one cost. You don’t see that the landlord is holding the mortgage. That mortgage likely has escrow that pays for insurance and taxes, which both increase every year. Even if it’s not escrowed, the landlord is taking the time to manage the income/expenses of the house and paying out the taxes and insurance.

You also don’t see the maintenance costs. When you call me to have a plumber come out, that’s an expense. I used to pay $125 for a service call and minimal work. Now that’s $200-375. Your rent is covering that possible future expense. Could you imagine if you found out you needed a new water heater in the house; would you have $1500 to hand over in a day’s time? As a renter, your rent is set to cover those future expenses.

We typically reserve rent increases for every other year, and it’s usually $50 per month. There have been some cases where a tenant has negotiated less, and a few other cases where we increased the rate more than $50 per month because of the drastic expense increases we incurred. I learned that if I don’t increase $50 every two years, I end up behind on the increases that are coming in future years. I don’t want to increase rent by $100 /month on a good tenant, so I try to keep with this schedule. I always explain that this increase is due to carrying costs. I also always provide a written documentation and give the tenant the option to move out. I’ve never had a tenant move out because of a proposed increase.

SUMMARY

If you’re interested in knowing more about these numbers, review the post that I linked. You’ll see that my annual costs increased by over $4,500 on these properties. You’ll also see that in some cases, where I prefer to only increase rent every two years instead of annually for tenant satisfaction, I’m not keeping up with the cost increases I’m incurring. House3’s two year cost increases of that property’s insurance and taxes total over $125 per month; I increased their rent $50 per month. I have other properties that can float that loss I’m taking there, but having happy, polite, and courteous tenants who take care of the property like its their own is more important to me than drastic rent increases and risking someone less vigilant moving in.

So the next time a landlord increases your rent when your lease term expires, understand that it’s to cover the expenses they’re covering for you to live there. When the property sales in the area increase, know that the landlord’s taxes are increasing, which equates to a higher rent needed to cover it.

I’ve been working on the ‘year in review’ posts for 3 months. I really want to be consistent on tracking our spending and making sure I’m being intentional in our spending. Our main credit card had the nerve to tell me that it was exporting 461 line items for me to categorize and manipulate in Excel. We have 8 credit cards. So that wasn’t a fun realization.

Additionally, if I track it more than once every two years, I may be able to better categorize our spending. For example, a Walgreens purchase may be pictures that I printed, or it could be a prescription. My Amazon purchase may be clothes for the kids they needed, a gift for someone, something in the home improvement category, etc. The entertainment category can include exercise that we’ve paid for (e.g., 5K, ultimate frisbee, kids’ activities) or a trip we went on.

There’s also no direct way that I’m tracking where a credit card expense has been offset by someone paying us back. For instance, I put $980 on my credit card for a trip, but someone paid me $480 for it via Venmo. That offset is in my year’s total transactions, but not in a manner where I can capture it for this year-long-view of expenses. Additionally, we go out to eat at restaurants, but Mr. ODA gets paid for some of those as a secret shopper.

EXPENSES

This doesn’t identify the actual money spent in each category, but it shows how categories align with each other. To simplify this graph (and to allow all bars to even be seen), I combined several smaller categories into an overarching category. For example, the entertainment category includes anything from doing a brewery tour to traveling to another state. Home Improvement includes $10,000 worth of new carpeting, so it’s an outlier. This also doesn’t include expenses that were paid for out of our checking account(s); although nearly all of our expenses are paid via credit card to gain the rewards.

MEDICAL: We spent the first half of the year managing doctor appointments. They were mostly for the baby, and then halfway through the year, I started having serious vertigo issues. The baby was born a little early, had jaundice, diagnosed with reflux and put on medication, and then had trouble gaining weight. My 3rd baby then needed to have formula supplemented, after I nursed two kids and had extra milk to donate to NICU babies. That was an unexpected psychological and financial change. Once he started to become healthier, I hit a wall. After a week of wondering why I kept feeling lightheaded and dizzy, I woke up one morning not able to walk a straight line, and if I even attempted to, I’d throw up. I was diagnosed with an ear infection, which seemed to make sense, but the antibiotics didn’t stop the vertigo episodes. After several specialists, I was given the same thing that I always am: “your symptoms don’t fit neatly into any one category, and I don’t know what’s wrong with you.” Luckily, most of my symptoms have died down at this point. And thankfully, outside of random viruses and a bout of pink eye through 3/5 of us, the others were healthy.

SPORTS: We joined the Y and were really strong for the first 3 months. Once my mom died, I didn’t have it in me to go exercise, and then I got sick for most of the summer with that vertigo issue. Mr. ODA played softball, vintage baseball, and ultimate frisbee; I was able to play some ultimate frisbee and run a 5K. The kids did swim lessons at the Y (and was quite a terrible experience). Our oldest attempted soccer for the second time, and then cried through all practices and games. Our middle thrived in ‘acro’ for the second half of the year. I plan to finish our this semester with her in acro, but I think she’s going to love gymnastics after that.

TRAVEL: We traveled to NY for my mom’s funeral. I took 3 flights in a few days with the baby, all with points (which American Airlines was super easy to work with for last minute flights and using points). We went to the middle of nowhere Tennessee with Mr. ODA’s family, to NY two more times, a short family camping trip, to Indy for some kid-related fun, and a trip to Cincinnati to see Christmas lights and take the kids skiing for the first time. I bought myself new skis (I had been snowboarding for the last 13 years), which led to buying the kids ski equipment (although, it’s noteworthy that we bought them second hand and their skis and boots totaled $100 for two kids). That then led to buying mid-week season passes at our local ski resort. On top of our family trips, Mr. ODA took two work trips, a golf trip, and a mountain biking trip.

GAS: Typically, our gas usage can correlate to our travel because we usually drive somewhere instead of fly with 3 little kids and all the gear they come with. In June and November, we drove to NY, so those have bigger spikes in the graph below (June also included a trip about 4 hours away). In the beginning of the year, we were more interested in staying home because we had a new little baby, but we ventured out more towards the end of the summer.

RESTAURANTS: I was pleasantly surprised to see the amount spent each month in this category. I didn’t feel like we ate at restaurants all that much in the last year, but I was concerned with whether the numbers who support that. There’s an outlier in March because we spent a lot at one restaurant during the week of my mom’s funeral. On Long Island, food is a big deal; while every one else was paying for meals, I felt it was our turn. We don’t need to actually mention how much that meal was. May’s spike was simply the volume of times we went out to eat, and the majority of them being related to Mr. ODA’s secret shopper gig.

HOME: In July, we had a storm come through that wrecked our neighborhood. No one reported the damage to the National Weather Service, which makes me sad because I wanted to know if it was a tornado! We had several trees fall. One took out our deck, another took out our fence, and another cracked our driveway, but missed Mr. ODA’s car by centimeters. We fought insurance for 5 months, and now we’re in the queue to have it replaced some time late Spring.

CAR: We bought a car. That’s $6,000 worth of the “Home Bills” category. Since most of our bills actually can’t be paid by credit card, it’s surprising to have such a high category for that on the graph, but that’s why. They allowed us to do two $3,000 transactions on a credit card so we could get the points, and then we paid the balance by personal check.

GROCERIES: I’d like to watch this spending more in the future. A purchase at Walmart may include non-grocery items (e.g., shoes), but that is being lumped in with the groceries because I can’t possibly siphon out individual transaction expenses for an entire year in one sitting. So here’s a graph of our “grocery” spending per month, but noting such a caveat.

SUMMARY

While I know we’ve had some larger one-time expenses, I’m still not happy to see the amount spent in each category. I feel we’re diligent in our food spending, but I think we can reduce that amount.

I removed rental information, any rewards received, the $6,000 car purchase, and the $10,000 worth of carpet purchase to try to show that our spending is consistent month-to-month. Again, the baby kept us home in January and February, but we’re generally consistent in spending. I hope that I can review our expenses more often going forward so that I can more accurately categorize our spending.

A day late, but here we are. The market has gone up a bit, so that helped our net worth increase, even though we had a $10k increase in our credit card balances because we replaced the carpet in our house. Again, we opened a new credit card for this large purchase, which will give us 15 months of 0% interest. While we could pay the balance now, it’s a strategy to allow us to keep more liquid cash and earn interest on the money.

We have a tenant that only recently paid October’s rent, and has paid about $200 towards November rent as of today. I’m frustrated, but I have another post that will go into all the details for that. I can be understanding and work with you, but only if you talk to me. She doesn’t communicate, and she hasn’t upheld any part of what she said she’s going to do about payments.

I had one tenant ask me about moving out early, but we haven’t pursued anything yet. I have another tenant who is under contract on a house, so we’re waiting for notice from them. We knew they were looking for a house to purchase, so we structured our lease to allow them out of the lease at any time. It’s unfortunate for our timing that it’ll probably be a January/February rental now, but I’m happy for them moving on to their next phase of life.

I had to pay two small tax payments to a local jurisdiction this month, and then also paid taxes on one of our properties (luckily they still take credit cards with no fee, so we get rewards for that payment!). I’ve had to pay several medical bills (for myself) over the past month, which has been annoying. All that money to bills, only for there to be no answers.

We went to a local ski mountain to look for ski boots for my new-to-me skis that I purchased. In the process, we ended up buying the two older kids skis and boots, along with season passes for the family. So medical bills, ski equipment and passes, tax payments, and Christmas gifts have our credit cards high now (even without the 10k+ for carpet).

I manage all our income and expenses (at a high level, like credit card payments, not individual line items). I have a spreadsheet that I set up in 2012 and have used religiously since then. I’ve shared how I set it up in the past, but we’ve entered a new phase that makes my spreadsheet even more important to me.

BACKGROUND

FIRE. Financial Independence, Retire Early. This isn’t a post about FIRE specifically, although it’s the movement that sparked Mr. ODA to go down our financial path.

The purpose of our rental portfolio was always for both Mr. ODA and I to quit working. We had covered my income before any kids were born, but I kept working because there was no reason to not be working. Once our son was born, I took 14 weeks maternity leave (not a separate bucket for Federal employees back in 2018; it came out of my own accumulated sick leave), then I worked about every other day for 8 months while Mr. ODA and I swapped child care roles, and I burned down my leave.

While we don’t plan to work full time, we do plan on keeping part time positions. We’ll work on things that bring us joy, rather than an office job with office politics. Since I stopped working, I’ve done odd jobs, part time. For example, I worked as a census taker and served beer at a local race track over the last 4 years. These were all seasonal, part time positions, with no long term commitment.

Now that I quit working, it’s Mr. ODA’s turn. We hardly skipped a beat when we left my six-figure salary behind (although a pandemic probably helped curtail spending on our behalf!). However, the thought of losing his salary as a safety net and losing insurance are two items that have caused some pause.

THE SPREADSHEET

For you to understand my panic that I’ll get into here, I thought a quick reminder was necessary. This is how I manage our money. It’s nothing fancy, but it works. I don’t miss payments. I can allocate expenses to a specific 2-week period against what income is brought in at that time.

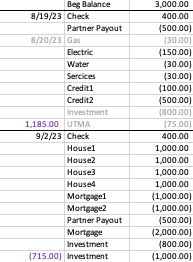

There are two parts to the spreadsheet. Well, there are about 10 tabs, but this first tab, with two sections, is what’s pertinent.

Part 1 is this section. This image is a very scaled down version of the section. We have 13 houses, 6 mortgages that get paid, 6 credit cards that get paid regularly, and a few other lines that I removed.

All numbers are made up place holders, except the investments. I deleted my IRA contribution line because it’s wonky (but I will max out IRA contributions), but I wanted to show how much we’re investing regularly. There’s $75, per kid, per month, going into their investment accounts. Then there’s general investing happening with one $1000 transaction and two $800 transactions per month. Mr. ODA is investing into his IRA to max it out ($6500/12=$541 per month..sort of).

You can see that I’ve listed Mr. ODA’s pay dates at the top, and then his salary income on the next line. The gray section accounts for all rental income. I’ve allocated the income into the salary two-week period that makes the most sense (about half pay me on the 1st or 2nd, and the rest pay on the 5th). The green section shows routine rental property expenses. The entire next section are our personal expenses. The blue is left over from when I was managing two personal homes last summer (but kept it to differentiate our house bills versus other bills). The next gray section (which I’m only just realizing is a second gray and should be a different color as to not conflate the two grays.. what a rookie mistake) accounts for expense that come out of Mr. ODA’s bank account. Finally, I have an “other” section. This is where I capture large expenses that don’t need their own line item because they only happen once or twice a year. Here I’ve put tax payouts that will be due in October (that’s 4 houses worth, and it’s last year’s numbers – because I want to know how this year’s amount owed, when it comes in, changed from last year’s to discern if it’s reasonable or if I need to dig into it).

This is part 2. Now, part 1 accounts for the general timing of income and expenses, but it doesn’t perfectly capture the due dates, scheduled payments, or whether I’ve paid it and it’s hit the account.

The top line is linked to the section that I update our checking and savings account balances. Then I transfer all the items per pay period into this list format. In this example, let’s say I’ve already scheduled the gas payment. So I mark it as gray and put the date in the left column. Similarly, our investments are automatic, so I mark them in gray as we get to that two-week period.

At each border lined, I put the total for that section. You can see that at the end of the 9/2/23 pay period, I project a negative balance. Truly, we seem to have more income than I project (rewards cashed out, someone paying partial rent a little early, etc.), so I don’t take any action until I need to. There are Federal regulations regarding savings accounts; so we can only make 6 withdrawals from the savings account before fees apply. I manage these projects to know whether I need to make a withdrawal. If I need to, then I project what other expenses I may have and transfer a little more than I deem necessary.

THE PLAN

So our first step to him leaving is to pretend we don’t have his salary. Mr. ODA set up a new bank account. The majority of his paycheck goes into that account. We still have $250 going into another account, and about $400 going into a third account because we need to meet the requirements of direct deposits to prevent any account maintenance fees.

Our general principals in account management was always to take money into our main checking account, pay out bills for that two week period, and put the balance into savings. However, that wasn’t creating any forced feeling of managing without Mr. ODA’s salary. I’m more of a visual learner, so I appreciated this concept of having the money automatically transferred to a completely separate account.

EXECUTION OF THE PLAN

The first month of this plan had me on edge. The accounting in the checking account meant I was constantly back down to a balance of about $500. When I worked in an office, I was at the computer everyday checking our money. Now that I’m responsible for 3 tiny humans, I’m rarely on the computer. I project out our routine expenses, but there have been plenty of times where a $100 or $500 charge goes through that I didn’t have listed in my expense column for that period. Therefore, I like to keep at least $1000 as a buffer in the checking account to cover those little expense that can add up. So keeping the projection to less than $500 in the checking account panicked me.

Now wait. It’s not that we only had $500. We have a savings account linked to that checking account. We have this online account that’s taking Mr. ODA’s salary and just building the balance because we don’t use that account for anything. We have Mr. ODA’s old personal checking account. And last but not least (as my adorable 3 year old says all day long), we have plenty of investments that can be liquidated within 24 hours. We have the money. It’s just the panic of having the money in the spot where the bills are being paid.

SUMMARY

I’m sure there are easier ways or “better” ways to account for this. I don’t like automatic payments for bills because I like scheduling them against our cash flow. I’ve used this exact set up since 2012, and it hasn’t failed me. Taking full responsibility to pay bills means I am very scared to miss a payment and cause a negative hit on either of our credit reports.

Now that we’ve eliminated about $5,000 per month of income, without changing our spending in any way, I’m interested to see how things go. We have a great spending mentality – we’re not spending on frivolous items and we weigh the cost benefit of a purchase to us. That’s not to say we can’t do better. I’m sure we can be more diligent about our grocery spending or at least cooking what we already have in the house (we don’t spend much at restaurants in a month). I’ve already started tracking our expenses month to be sure we can watch our trends and re-evaluate our spending if needed.

Now that we have this account growing with no need for it to pay the bills, we will use it for fun things. We’re not very good about doing fun things. Two summers ago, we wanted to buy a vacation home at a nearby lake. We decided that instead of spending $1200 per month on a mortgage to go to the same place all the time, we’d plan vacations each month and spend up to $1200 without “guilt.” It was great. We had so much fun. But it lasted 3 months. Having a newborn put a damper on activities, but we’re ready to do the same again.