We started getting emails about end of school year activities, and boy was that a surprise that we’re at that point. The middle one is done mid-May and the big kid is done at the end of May. Less than 2 months until summer break.

Mr. ODA took the second round of the government’s offer for administrative leave, which means he would only have a few weeks left working. I’m still working my part time job, which is taking way more hours than we had planned for. I’m enjoying it, but it’s been a juggling act with the family, which is probably why my son who absolutely loves school begged me to stay home because his belly hurt last week.

Buckle up because apparently I have a lot to share this month.

RENTALS

We received about $600 in tax payment reimbursements from one of our localities, so that was a fun surprise this month. Really helps my psyche that I have a tenant who hasn’t fully paid, didn’t tell us why ahead of time, and hasn’t been up front with when she’s going to actually pay us.

I executed 2 short term leases. Both included a rent increase for their short term period; one house is increased by $75 and the other by $25. Luckily, both are here in the Central KY area, so we can flip it between tenants. One is scheduled to leave June 30th. That house will need new carpet in the bedrooms, and it’ll need probably a whole-house paint job again. They smoked in there, even though we covered the lack of smoking rule multiple times. I’d be more upset about it if the carpet hadn’t reached its useful life years ago. The other house leaves July 31, and I can’t even tell you where we’ll need to begin with that one. She made a wood feature wall without permission. She had a giant fish tank without permission. She spent a lot of time doing things that really weren’t an improvement, so I’m definitely worried about what we’re going to uncover in that house. Mr. ODA and I are talking about fixing it up and selling it. We may look for a short term renter so that we can sell it in the Spring instead of this Fall.

I had 2 other properties accept a rent increase that will go into effect later this year. I require 60 days notice for changes so that starting at the 30 day mark I can begin advertising it if needed. One house goes up by $25 per month as of June 1, and the other goes up by $50 per month as of July 1. I also have another property that has a rent increase of $50 per month going into effect next month.

I have 4 houses that renewed another year, and I didn’t change their monthly rent rate. There are 4 more houses that haven’t been discussed. My intent is to have them renew for a year at their current rate. There are 2 of those 4 that could leave at the end of this term, but time will tell.

We have multiple maintenance issues to address. One house requires a tree trimmed off the roof, the siding cleaned, and the back deck stained/painted. We still have termite damage we’re dealing with at a house in Richmond. I have a leaking toilet that was just addressed, and then they hit me with a faulty HVAC unit during a heat wave. Then we have some houses that really need eyes on them to see what condition they’re in at some point this summer back in Richmond. It’s amazing to me how people just don’t care to tell a landlord that something is broken. I woke up this morning to a text that one of the houses here has a flooded basement due to a water heater failure.

I spent some more time fighting my insurance guy here. It irks me so much when I see him offer up his services on the local facebook group for property owners. He’s quite terrible. I sent him photos of a house that had some issues with a cluttered backyard and had the tenant clean that up. I had to fight him last month on an increase where he changed one house from a crawl space to a basement when I assure you that the vines growing through the windows solidify it should not be deemed a “basement.” When the dust settled from that debacle that he was insanely unresponsive to, I ended up owing $9.68. When I asked why my account wasn’t put back the way it was found before this mess he created, he said he didn’t know but it’s probably from the audit and changing square footage. HIs guessing and not actually answering infuriated me. I gave up and paid it, but then I ran to get quotes from other people. I hadn’t done that before because our 4 claims in a 12 months period are killing us (again, because I really wanted trees to fall on us!). I hate when people make the claim that because it’s not a lot of money, I should just give up and accept it. That’s a ridiculous way to treat people.

PERSONAL

Our electric bill is almost double what it was this time last year thanks to the vehicle charging and hot tub. Our electric bill is relatively low, so that’s not all that surprising. We also have 5 full people in this house now (as much as you can count a 2 year old as a full person… but he knows how to control light switches and eats a ton of food that we need to cook him, so I’m sure he’s a factor there!).

I’ve been working at my new part time job for over a month now. Mr. ODA was making fun of my hourly rate, but I’ll tell ya, it felt good to receive a paycheck that wasn’t $45 like it was for a day of subbing at the preschool.

I took the kids to get haircuts. My middle has had her hair cut once before, but I’ve cut the boys’ hair forever. I had family coming into town and the oldest was looking really shaggy. So I swallowed my pride and threw money at the problem, which is very out of character in this household. I just didn’t have the time to cut their hair, clean them, and clean up the mess. For $66 and 45 minutes from the time I left home until I got back, it was well worth it to me.

I had a medical procedure done this month. We haven’t met our deductible. In February, they said I had to pay my deductible to them. I said that didn’t make sense and refused to have them hold $2800 of my money for 2 months. They gave me an attitude and said I could never ever ever ask for a payment plan in the future, so that I could pay $500 to hold the date. I then showed up for the procedure, knowing I haven’t met my deductible, and they didn’t take any money from me. Another business model that bullies the customer into illogical money decisions. I also had an eye doctor appointment that was frustrating in itself, but I’ll spare you those insurance and communication details.

On top of everything else I’m juggling, Mr. ODA is coaching our kids’ t-ball team. Coaching means that I am team mom. That means that I’m responsible for communicating updates from the league (in the slow and haphazard fashion I receive information), gather value card sales that are required of every team member, organizing a basket for a raffle, and the best one – raising $350 for team sponsorship. What the heck, man?! Where did I say that my signing up of two children to play in the league means I have history or ability to gather money from businesses?? Well, I did it. I raised $350 and another mom raised $200 for the team.

No financial impact, but I’m also juggling our HOA board duties. I released our longstanding property manager and hired a new company, which took effect April 1. That’s taken a lot of time to get them stood up and make sure we stay on track for our annual meeting schedule in June.

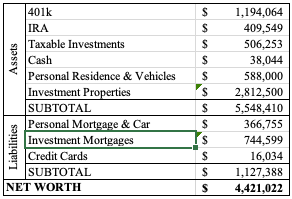

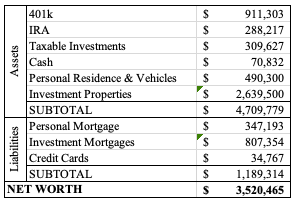

NET WORTH

And with all of that said, that doesn’t even address the giant reduction in our investments that continues to happen. To counter some of the loss, I updated our property values for our houses. I don’t do that every month because they don’t move very much, but I can usually count on a few increases as the spring market ramps up. Our net worth did slightly increase (based on yesterday’s market closure, not today’s) from last month, which was a nice surprise.

I wonder why I’m tired and bogged down, but that post outlining what I’ve done recently made me realize all I was able to accomplish even though I felt like I was a jack of all trades and master of none. Hopefully things will settle down in our lives going forward now, even if I know there are definitely two house turnovers in my future.

Well, my desire to post every Thursday fell off there. I started a new job, Mr. ODA’s Federal job has been in limbo, and just general life things have been going on and keeping us busy. The kids started t-ball in the past few weeks, our youngest was waitlisted at both of the preschools we tried for, and the rentals have needed more attention than average. Let’s dive in.

NEW JOB

I was approached by someone I serve with on our HOA board. They were looking for a new person who has a financial background, was really organized, and could handle talking to people regularly. It appears that I made such an impression on him and his wife. I wasn’t ready to get back into the workforce. While I have enjoyed my temporary jobs I’ve done since I quit my career in May 2019, I always had a ‘sunset date’ on those activities. I knew that each job was only for a short period of time, and I’d get back to freedom/flexibility. This was a new territory they were asking of me – be on a set schedule and away from my kids.

I expressed that my need for entering back into the workforce was that I wanted to be part of my kid’s activities and I needed to work between school hours for the most part. They expressed a desire for me to work 30 hours, and that just wasn’t feasible. Based on what they told me about the tasks required of the job, I was able to come up with about 18 hours of work, knowing it would likely become 20 hours. So far, I’ve worked more than 20 hours each week as I’m learning, and things are not moving as quickly as I expected them to. I’m 2.5 weeks in, and at this point I can do all the main tasks. Where I’m struggling is the knowledge of all the “one off” transactions and how some people are treated a little differently than the standard.

Overall, I’ve been super grateful that Mr. ODA has given me the space I needed to get my feet under me these past couple of weeks, and I’m really enjoying learning these new tasks and being involved in this sector.

FEDERAL WORKERS

It’s been rough around here for almost two months now. While Mr. ODA is still employed, there is a daily concern that the news will come in. There’s no security like there used to be expected for a government position. The blows have become a bit more scattered than it being such a daily barrage, but there’s still uncertainty and daily updates and waiting for more information that’s occurring.

PRESCHOOL

Both old kids will be in regular school next year. Our youngest has a late-in-the-year birthday, so he wasn’t eligible for preschool until this coming school year even though he’s already 2. The preschool where both of the other two went to shut down. My middle is finishing out the year there, but next year, they sold the preschool concept off to a third party. The company that took over has terrible reviews, and everything about them screams ‘daycare.’ While people need daycares, and that’s fine, we don’t need that. I wanted a space that had a curriculum.

The school previously had a daily agenda and an expectation that the kids were there from 9 to 12. This new school has a come and go as you please set up, and they couldn’t provide me a break down of their daily schedule. The admissions person was actually quite rude and condescending to me, after taking 4 days to return my phone call. I’m not in a desperate need for our youngest to go anywhere, so I won’t be trying to enroll him there.

We had hoped to get into another preschool by our house, but the closure of our old school sent a mass exodus to the nearby preschools. I told Mr. ODA that I wanted to join their church so I could get 3 weeks ahead on signing up, but he said that wasn’t ethical and was more than just saying “I want to join your church.” So I didn’t. But several other families did. And they got in. And I’m still really sad about that. He’s waitlisted there, and there’s been no indication of hope that he’ll get off the waitlist.

I tried for a “moms day out” program, which would cover one or two days per week (I was looking for 2 days previously). He’s waitlisted there, but she gave me a glimmer of hope that even though they don’t have a lot of turnover, there is a chance a space opens up either right at the end of this school year or at the beginning of next school year.

I had originally ‘mourned’ the loss of my freedom with the preschool closing down. I have been at my kids’ beck and call for 7 years by the time our youngest would go to school. Even though it was only going to be 6 hours per week, I was excited to get things done that have been on my to do list for years and just run errands unencumbered. I’ve lessened my extreme feeling on that over time, but it still would be nice to have a few hours dedicated to me and my schedule at some point.

RENTALS: RENT RATE

I evaluated our current tenants and their rent rate back in December. I should have just written the letters at that point and been prepared for the deadlines, but I didn’t. So this week, I got those rent change letters prepared, printed, and mailed. We typically change the rent by $50 every two years for our long term tenants. That’s the approach we took here except for a couple that needed more catch up. One tenant has already responded and executed a change to increase their rent. I have 4 more out there waiting for the tenant to tell me they accept the adjustment or will be leaving at the end of their lease. I also have another tenant who will be staying another year, but I didn’t change their rate since I had changed it by $25 last year.

RENTALS: TERMITES

We have a house that we purchased with termite issues. We knew it going in. We had it treated, and then we fixed the really bad areas. We then didn’t get notification about an annual warranty payment they would do, so our coverage lapsed for a few years. We saw swarmer termites in one part of the house and called them back. They offered to let us backpay those missed warranty years, saving us about half the cost it would have been for a new treatment. Well, we’re paying for that now. For the last 4 years, they’ve checked the property once per year. They’ve noted termites actively being there with more damage, and they didn’t clearly communicate the concern of the condition until this month. We have major problems in the house. One wall in the laundry room is so bad that the termites ate the backing off the drywall and the drywall is all cracking off the wall because it’s not being held onto anything. It really hasn’t been fun, but I know we will be able to fix it. So far, we’ve had the crawl space cleaned out and relined with a vapor barrier, and some plumbing issues fixed that were creating a perfect moist condition for termites to gravitate to. We still have to rip up the carpet, fix the subfloor, lay LVP, rip out a shower insert, reinstall the insert, and get the shower operational after that. It’s a lot.

PERSONAL FINANCES

Mr. ODA reduced our monthly contributions to our investments. We were putting $3,000 per month in (3 separate $1,000 transactions), and now those have been reduced to $500 three-times per month. The kids still get $100 per month each into their UTMAs.

We’ve been so busy that we have hardly spent any money. Outside of insurance and medical payments, the only extra spending I’ve done is for our daughter’s birthday parties we’re having this month. I’ve bought some clothes since I’ve lost weight on my post-three-kids journey too. Usually, we’ve booked a trip by now, but we haven’t done that either. Overall our spending is lower than it has been.

NET WORTH

The market is well below where it has been, and all our numbers show it. We are over $189k lower than last month. I haven’t updated our property values yet. I’ll probably do that next month as the spring market ramps up.

The President issued a statement calling on Congress to cap rent increases at 5%, specifically for corporate landlords. The statement appears to define corporate landlords as those owning over 50 units in their portfolio. This was not an executive action that is implemented. And while my numbers are different than the numbers of a “corporate landlord,” I do think it’s worth hearing a landlord’s side. I feel that there’s a lot of spite against landlords without a lot of knowledge about their actual financials.

I admit that there is a possibility that some of these companies with large complexes could be raking in on the fees or “utilities” that are in the unit, without actually providing a properly maintained building, but that’s not the case for everyone that’s labeled as a landlord. No one seems to step back and see that this is a business model for landlords, and while everything else around us is increasing in costs, rent needs to as well.

No one predicted such a significant rise in product costs or housing costs in such a short period of time, but here we are. And landlords aren’t in the business to graciously eat the costs of homeownership for renters.

LANDLORD COST INCREASES

The Presidential statement released refers to a press release that starts with, “Today’s U.S. Labor Department Consumer Price Index (CPI) report revealed costs remained largely unchanged in May, with overall inflation cooling faster than economists expected as the Fed considers finally reducing interest rates below a 23-year high.” Is there a comparison to costs that landlords had to take on because the costs of everything increased faster than expected back in 2020-2022? Increases have been seen on small things like a maintenance call for a technician, but also big things like property taxes and insurance.

That same article goes on to state, “Since 2019, the cost of rent has risen 31.4%, with wages only increasing 23%, as tenants on average need to earn nearly $80,000 to not spend 30% or more of their income on rent.” In 2019, on one of my properties, the taxable assessment was $95,000, which equated to about $1,200 per year in taxes. In 2024, the taxable assessment was $242,000, which equates to about $3,000 per year in taxes. That’s a 61% increase in just my taxes over that same period of time where they’re complaining that the cost of rent increased by 31.4%. If rent had been set based on the 1% rule in 2019, rent would have been $950 per month. Had I increased 5% each year from 2019, it would be $1,212 in 2024. If I set rent based on the 1% rule now, it would be $2,420. However, the rent on the property is $1,750. So while it’s more than 5% each year since 2019 (the baseline the government is using), it’s set at an amount where I capture my expenses for owning the house, while also turning a small profit.

It’s taboo for a landlord to turn a profit, but that’s why we’re here. It’s an income stream that we’re establishing for profit. I don’t get to pay myself an hourly rate for managing the property. So this “profit” can actually be looked at like a salary. Every time I need to show the property to a prospective tenant, the lease signing, the walk through, every call or text you make, every trade that I need to schedule and coordinate with the tenant on, any fixes or improvements that I do myself. All of these minutes in a day add up, and I’m not directly paid for any of them.

On the particular house that I’m using for the example, we are assuming $300 per month in profit, which comes to $3,600 per year. Would you work as a manager of a company (e.g., hiring trades to fix things, performing maintenance, making sure all bills are paid timely, general management of having liabilities), for only $3,600 per year?

I wrote a post last Fall about the changes in my rental fixed costs from a year prior. I plan on doing the same this fall when more tax information comes due. The house I’m referring to has been at $1,750 for the past two years. However, between 2022 and 2023, my taxes and insurance have increased by $255 per year. That’s a cost that I’ve “eaten” from my “profits.” I could have said that equates to $22 per month increase, and I could have projected a similar increase for the year coming. I could change their monthly rent to be $1,790-$1,800 to keep my profits on a similar path. However, I didn’t, because they’re good tenants that haven’t had many maintenance calls.

However, if I don’t increase every year, then I could find myself in a sudden deficit like I did during the pandemic because costs increased faster than projected. A 5% cap could actually incentivize annual increases because I wouldn’t want to be caught behind and not able to catch up down the road.

LEASE TERMS

The Federal Housing Finance Agency announced protections for renters in multifamily properties that are financed with loans backed by Fannie Mae and Freddie Mac. The protections include: (a) requiring 30 day notice before rent increases; (b) requiring 30 day notice on lease expirations; and (c) providing a 5 day grace period before imposing late fees on rentals. I know for a fact that every single lease I’ve executed personally already has all of these requirements in it, at a minimum. In many cases, there’s a clause for 60 day notice of a potential rate increase, with negotiations being completed before 30 days from lease expiration.

Some states already have this codified. Other jurisdictions have landlord/tenant agreements that give the tenants rights (and awareness of rights) that can be lobbied against if the landlord is noncompliant.

There’s a clause that I’ve seen that requires expired leases to auto-renew on a month-to-month basis instead of for another year. I would argue that a requirement to renew a lease month-to-month instead of annually actually hurts a tenant. A landlord then only needs to give 30 days notice of a rent increase, and they could technically increase it month after month.

SUMMARY

If the ‘cap’ were to apply to me, then I’d be more inclined to increase rent every year. As a general rule, I increase rent for long term renters by $50 every two years. When we turnover a property, we will evaluate market rent in the area and set the monthly rent at what we see (which could be more than $50). In some cases, the evaluation ends up being too high, and we set the rent at something we think more people can afford. For example, there were comparable houses renting at $2,200 near a house we had listed. We’d rather get the property rented than shoot for top dollar, so we listed it at $1,600. While lower than “market value” probably called for, it was $400 higher than what we had it previously rented at, which covered cost increases that weren’t previously covered.

In the post that I previously linked, I highlight that our standard for increases barely offsets our increase in expenses. While we manage each house individually on setting the rates (asking ourselves: do we think the tenant can absorb the increase, do we have to increase to cover actual costs now), our monthly income among all houses was increased by $475. If you add up the cost increases for taxes, insurance, and property management (increased rent means increased fees because fees are based on the rent price), our costs went up $415 (and that’s before any service calls). On a whole, we’ve offset the ‘fixed cost’ increases. We’re taking ‘losses’ on houses where our routine for increases is slower. Therefore, having 13 properties affords us the ability to be more lenient with tenants and to keep good tenants in the house instead of forcing them out with hgher rent increases.

I support having protections in place for tenants. I’m sure there are landlords out there that aren’t interested in playing ‘by the book’ and just being decent human beings like I intend to. However, landlords are people too, and they’re running a business. Creating boundaries without fully understanding both sides of the situation and focusing on data points that only support your theory is unfair. I’ve joined the Landlord/Tenant Advisory Committee in my city. I hope to bring more awareness to the landlord side of things and bridge the gap between landlords and tenants when it comes to responsibilities.

At the end of last year, I received each property’s revised assessments for 2024 tax purposes. To no surprise, every single property drastically increased. A harder pill to swallow is to see how much it increased just from two years ago.

Higher home sales are great – if you’re in the market to sell. If not, it’s just fueling the local jurisdiction’s ability to increase their tax income. Again, this increase is great for a resale opportunity, but it’s not great when we’re content in our “buy and hold” at the moment.

Where I live, we received our property assessments recently as well. There was an uproar from the citizens. The Property Valuation Administration explained the increases and how they work, noting that home values in our area have exactly doubled since 2014. While their valuation process only occurs every few years, and home prices are increasing about 10% each year, people are seeing 30-50% valuation increases when they receive their notice.

COMPARABLE SALES

When determining a property’s assessed value, whether it’s for tax purposes or a bank loan or such, nearby home sales are used as the basis. Home sales denote what buyers are willing to pay (and likely what an assessor determined as fair market value) for a home. To determine your home value, you would need to look at sales in your neighborhood or close geographic area, for homes (and lots) that are of similar size with a similar number of bedrooms and bathrooms. There are factors that you can use to compensate for a different number of bedrooms and bathrooms, but it’s easiest if you find homes with similar data points.

In today’s market, you’re also going to focus on home sales in very recent months. The amount that a person is willing to pay, and the amount that a bank is willing to loan, is increasing regularly. A home value in 2021 is different than today’s.

HOW DOES A PROPERTY ASSESSMENT AFFECT YOUR RENT?

I wrote a post that went into the details of how our expenses have changed over the last year on these rental houses. It’s noteworthy, as a renter, to be aware of the changes in property assessments because it’ll help you anticipate and understand the need for rent increases that will be coming.

I recently saw someone complain that a landlord was raising rent with no improvements. Rent increases aren’t tied to improving the house (well, they can be). Rent increases are keeping up with the costs that are increasing for the landlord.

I’m a broken record on this, but I’ll continue to work to educate. When you rent a house, you see the one cost. You don’t see that the landlord is holding the mortgage. That mortgage likely has escrow that pays for insurance and taxes, which both increase every year. Even if it’s not escrowed, the landlord is taking the time to manage the income/expenses of the house and paying out the taxes and insurance.

You also don’t see the maintenance costs. When you call me to have a plumber come out, that’s an expense. I used to pay $125 for a service call and minimal work. Now that’s $200-375. Your rent is covering that possible future expense. Could you imagine if you found out you needed a new water heater in the house; would you have $1500 to hand over in a day’s time? As a renter, your rent is set to cover those future expenses.

We typically reserve rent increases for every other year, and it’s usually $50 per month. There have been some cases where a tenant has negotiated less, and a few other cases where we increased the rate more than $50 per month because of the drastic expense increases we incurred. I learned that if I don’t increase $50 every two years, I end up behind on the increases that are coming in future years. I don’t want to increase rent by $100 /month on a good tenant, so I try to keep with this schedule. I always explain that this increase is due to carrying costs. I also always provide a written documentation and give the tenant the option to move out. I’ve never had a tenant move out because of a proposed increase.

SUMMARY

If you’re interested in knowing more about these numbers, review the post that I linked. You’ll see that my annual costs increased by over $4,500 on these properties. You’ll also see that in some cases, where I prefer to only increase rent every two years instead of annually for tenant satisfaction, I’m not keeping up with the cost increases I’m incurring. House3’s two year cost increases of that property’s insurance and taxes total over $125 per month; I increased their rent $50 per month. I have other properties that can float that loss I’m taking there, but having happy, polite, and courteous tenants who take care of the property like its their own is more important to me than drastic rent increases and risking someone less vigilant moving in.

So the next time a landlord increases your rent when your lease term expires, understand that it’s to cover the expenses they’re covering for you to live there. When the property sales in the area increase, know that the landlord’s taxes are increasing, which equates to a higher rent needed to cover it.

I keep updating my investment property tracking spreadsheet to reflect the current costs of insurance and taxes. My tracking shows last year’s amount, which I use as an indicator on whether I need to look further into this year’s bill (e.g., is the amount a reasonable increase?). For so many years, most of our insurance policies changed by a few dollars; now, I’m seeing large swings in what’s being charged. Where jurisdictions were slow to change property assessments, they’re now catching up, which increases the taxes.

As a renter, your rent is increasing to cover these costs of the landlord/owner. Here’s a comparison of my fixed cost increases against my rent rate increases. As you’ll see, I’m not trying to get top dollar out of these properties because the market has increased so much (and that leaves me more exposed if someone doesn’t pay their rent on time). My rent increases barely cover the cost increases that are happening on some of these houses. Remember that while I’m showing fixed costs, this isn’t covering the maintenance calls that I receive and how they’re more expensive than they once were also.

ESCROW, CONCEPTUALLY

In most cases, for a traditional mortgage, an escrow account is set up. It calculates your taxes and insurance payments for the year, divides by twelve, and is added to your principal and interest payment for the mortgage. In addition to covering the total payments to be made, there’s also a requirement that the balance of the account never falls below twice the required monthly payment.

If your taxes owed for a year are $1500, and the insurance is $300, then your monthly breakdown is $150 ($1500+$300=$1800; $1800/12=$150). The minimum monthly required balance is $300 (twice the $150).

As taxes and insurance increase each year (typically), there’s an analysis done to ensure the projected monthly balance never falls below that $300 threshold. If the balance is projected to fall below the required minimum amount, then it triggers an increase in your escrow payment. Your escrow payment will increase to cover the shortfall, but also to cover the new projected costs to be paid. So while you may be offered the ability to make a one-time payment to cover the shortfall, your mortgage payment may still increase to cover the projected costs. For example, if last year, your tax payment increased to $1750, and your insurance to $350, then your monthly payment to cover those charges is $175 ($1750+350=$2100; $2100/12=$175). Your mortgage will increase by $25 per month because now your escrow agent knows the projected costs to cover are higher.

The analysis uses the current year’s amounts owed to project the coming year’s monthly balances; it doesn’t account for the probability that these amounts increase each year, which essentially means that there’s perpetually a shortfall. In other words, while in Year3, they know that there was an increase in costs from Year1 to Year2, they don’t inflate the costs of Year2 to cover Year3 projected payments.

I prefer to not have an escrow, but at this point, for any mortgages we have, they’re all escrowed. We have six of thirteen houses with escrow. While I pay more as my mortgage to feed into that escrow account, it means I don’t have to manage the annual or semi-annual payments. On the contrary, this means I need to be managing our finances to prepare for large outlays throughout the year on seven houses (in the last quarter of the year, I’m paying out over $8,000 to cover taxes owed).

ESCROW REANALYSIS

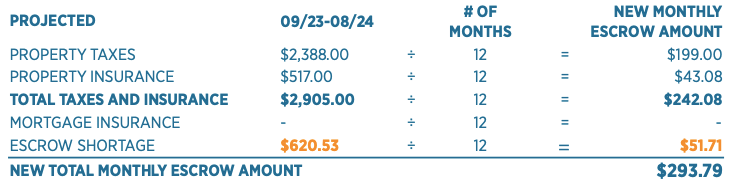

This post was prompted by a notification that an escrow reanalysis was done on a mortgage that was just transferred to a new company. I thought that their break down was the most clear I’ve seen. A quick note – your escrow will pay the bills that come due, regardless of the balance in the account, even if it means it’ll overdraw the account.

They clearly showed that the anticipated property taxes are projected at $199 per month (although, I’ll reiterate that this is based on last year’s actual outlay numbers, which aren’t accurate for the coming year). Then they show that the taxes are $43.08 per month. They then go as far to show the total of these two required outlays. There’s verbiage that explains the required minimum in the account must be twice the total taxes and insurance ($242.08 * 2 = $484.16).

There’s another detailed breakdown of each month’s escrow income and outlay (that I don’t have pictured here) that shows the month that is projected to fall below the required minimum. That month’s account balance is -$136.37. The difference between the required amount of $484.16 and the negative balance of $136.37 is $620.53 (pictured above). When that’s broken down by month, it’s $51.71. Take the total taxes and insurance payments and add the shortage amount to get the new monthly escrow amount of $293.79, a change from $222.25.

Below, they show you that there is no change in the principal and interest payment, then it shows how the current escrow payment is adjusted to the new escrow payment, along with the shortage amount.

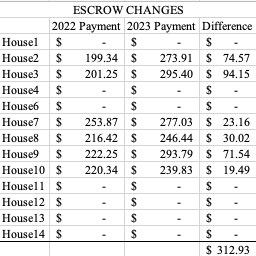

I created this table to show the differences between escrow payments over the two years. I kept the houses that don’t have an escrow because it can be compared to a future table in this post. There is no House5 in this table because we sold it several years ago (houses didn’t get renumbered because House5 still exists in terms of tax documentation).

TAX AND INSURANCE UPDATES

Each year, we see an increase in these amounts. Usually it’s across the board, but Kentucky districts had kept the housing assessments the same through the pandemic. As housing prices increase, your property assessment can be increased by your tax jurisdiction. The assessment increasing leads to an increase in taxes. This is why people getting excited that house prices in their neighborhood are selling higher than expected isn’t great if you’re not planning on selling any time soon; those increases in values means you’re paying higher in taxes.

In Richmond, VA, the property taxes are $1.20 per each $100 of the assessed value. In 2022, House2’s value $163,000. In 2023, the value was increased to $203,000. And let’s not forget that we purchased the house for $117,000. While it’s nice that the home values in the neighborhood are increasing significantly (and we knew the area was going to get better and better based on development happening), we can’t realize this gain until (and if) we sell. So in the meantime, we’re paying higher taxes on this amount. Although, I suppose the assessment could be even higher because the actual value of this house is probably more like $260,000.

Among 13 houses (don’t get confused – there’s no House5 up there because we sold it), I need to cover a total cost increase for taxes and insurances of over $4,500. This doesn’t include the higher costs of trades people if there are any maintenance calls, so this increase is the bare minimum for me to keep my same income.

RENT INCREASES

I constantly see complaints about the cost of rent, or that a landlord is increasing rent. Unless we’re looking for a tenant to move, our general philosophy is to increase rent $50 every two years. This worked fine because home assessments increased at a slow, reasonable rate until recent years. Now jurisdictions are capturing these larger increases based on those inflated sale numbers when competition was high in from 2020 through 2022.

In some cases, the rent for the area brought it in a higher amount than compared to our purchase price of a house. In those cases, we went several years without increasing the rent. Looking back, that probably wasn’t the best idea because now we’re behind on capturing how significant these last few year’s fixed costs have increased. However, the trade off to that is that we’ve kept great tenants in the house, haven’t had to pay to turnover the unit, and have minimal maintenance calls.

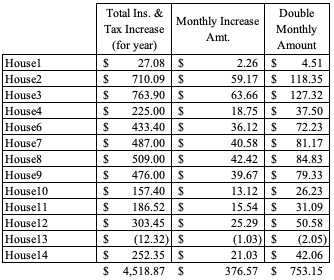

This table shows the total increase in insurance and tax payments from 2022 to 2023 in the first column. I divided that by 12 to get the monthly amount of that increase (second column). Then, since I said we typically increase our rent by $50 every two years for the same tenant, I multiplied that monthly amount by 2. I’m showing that if we want to only increase rent on long term tenants every other year, then I need to plan ahead on how much my costs are increasing.

This isn’t a perfectly accurate capturing of our cost increases since I’m not going back to 2021 to capture those changes in amounts, but it’s a general estimate. This shows that if I were to increase all houses by only $50 every two years, it’s cutting into my bottom line. Only 6 of the houses have increases less than $50 for two years.

SETTING THE RENTAL RATE

Let’s pause and talk about “bottom line.” Landlords have investment properties to make a profit. They’re looking for an income stream.

I regularly hear people say they can own a house for less than their rent, which is likely if you’re speaking only on principal and interest of a loan. However, you need to qualify for that loan. You may not have 20% down, so you may be required to pay private mortgage insurance (PMI). You may not have good credit, which means you’re probably going to pay a higher interest rate than I’m currently paying. You need to be able to cover taxes and insurance, which means you’ll have an escrow account set up, which increases your monthly mortgage payment. Then there’s all the other costs of home ownership.

That’s where people forget. When your hot water goes out, you call me. I spend $1,500 for about 2 hours worth of someone’s work to replace that. When you have a water leak, I spend $3,000 for a day’s worth of 2 plumbers’ work. When a storm drops a tree on your house, I’m the one spending hours on the phone with insurance, finding a contractor, getting quotes, and paying the contractor $3,700 before I get insurance reimbursement. Those are the big unexpected expenses. That doesn’t include all those smaller plumbing problems that cost $200 or $500 at a time.

Then in some cases, I probably put time and money into the house to even get it ready to rent to you. I didn’t always buy a house that was ready to live in. You may have projects that need to be done when you first move in also, so which costs money. Those are expenses that I’m trying to recoup through my rent rate also.

There may be other costs to my ownership that I’m trying to recoup through the rent, such as property management. I may have to pay someone else 10% of the rent, every month. I am projecting that there are going to be costs that I need to pay for also (e.g., water heater, roof replacement, plumbing issues). When I need to pay a plumber $3,000, I’m not coming to the tenant to say “I now need $3,000 to cover this cost.” Instead, I’ve set my rental rate the expect such a large payout on my part.

Not only am I trying to make sure that my rent is set at the right about to cover the costs that I’m putting into owning and maintaining the house, I’m also hoping that I’m going to make some money off owning this house so that I can live. I don’t get to pay myself for the hours I put into managing the property. Whether or not I have a property manager, there is still time that I put into managing the houses. Would you want to work for free?

BACK TO RENT INCREASES

While we manage each house individually on setting the rates (asking ourselves: do we think the tenant can absorb the increase, do we have to increase to cover actual costs now), this shows that our monthly income was increased by $475. If you look back at our total monthly increase in expenses of just taxes and insurance, it’s about $375; add in the cost increases for property management (increased rent means increased fees because fees are based on the rent price), and our fixed costs went up $415. On a whole, we’ve offset the increases.

However, you can see if we had one or two houses, some of those increases could be significant. House3 is costing us $64 more for each month, but our increases are typically about $50 at a time. We’ve had the same tenant in this house since we bought it. A $50 increase every two years hasn’t kept up with our costs. Since we have other houses, it helps cover the costs on House3.

House2 and House3 are identical in layout. House2 has been upgraded to all LVP, whereas House3 has carpet everywhere except the kitchen and bathrooms (granted, it’s new carpet two years ago). Since we purchased these two homes with tenants, rent was already set for us. House3 has been the same tenant since we bought the house, and the increases have brought us to $1200 per month in rent. House2 has been turned over 3 times: the first was a divorced lady who moved back in with her ex-husband; the second was there for several years, but we began having a lot of issues with her, and we told her the lease was up; the third was the one who flooded the house in December, and causing the need for the fourth. Now we’re renting that house at its market value of $1600. That means House3 is operating at a much lower rent than we could get if we rented to new tenants. However, the tenants are wonderful, and we’ve purposely not raised the rent on them in significant ways because we don’t want to cause them to move.

SUMMARY

Cost increases in rental properties can be significant over the years. With the rising costs of all goods and services, property values weren’t immune. The increase in property values leads to an increase in an assessment, which means an increase in taxes. That cost is relayed to the tenant, as this is a for-profit business. I’m trying to make an income for my family with rental properties.

I’m not trying to price gouge tenants, but make a fair living based on the costs of owning these houses. My first goal is to not turnover tenants, so I do what I can to make my tenants happy by taking care of the houses and not creating drastic rent increases each year. Secondly, I’m not going to set a price that my tenant can’t afford, thereby putting me in a hard position where I don’t have rent paid. Having multiple properties helps to offset the costs so I don’t have to play catch up on one or two houses worth of higher expenses, by putting my long-term tenants in an uncomfortable position where they can’t afford the rent.

Well, Mr. ODA didn’t like that I shared I didn’t know where our money was last month. They’re all kinds of Treasury accounts, and I’n just logging the transactions and leaving him to it. 🙂 I don’t have a lot of bandwidth these days, but I’m learning to juggle 3 kids and our finances.

PERSONAL FINANCES

We bought a new van this month. We’ve been wanting a new one for a while now. We bought our 2017 Pacifica in September 2020. It was a great deal, and it was a necessity as we were about to spend 7 weeks “homeless” and AirBnB/couch hoping. The car had some defects. We decided we’d keep an eye out for a newer version. Suddenly, Mr. ODA found a good deal on a 2020 Pacifica that had more options than we were actually looking for. We drove to Ohio about 36 hours later. They made us a good deal for our trade-in, and we went home with a new van! We put some of the purchase on two credit cards and then the balance with a personal check.

We’re currently paying close attention to credit card deadlines and our savings account. Where I used to pay a credit card bill almost after the statement closed so that it wasn’t hanging out there and I wouldn’t accidentally miss a deadline, I’m now leaving money in our savings account as long as possible. Our savings account is now earning 4% on the balance, so we’re seeing a significant amount of interest each month. I’m juggling managing our bills as close to their due date as possible, while also projecting future bills necessary since there’s a limit of 6 transfers out of the savings account per month.

All that was to point out that our credit card balances are high right now because of the van purchase, but the credit card statement hasn’t closed yet. Instead of paying the credit card balances down right now, the money is sitting in savings earning interest for 4-6 weeks between the purchase, to the statement closing, to the statement’s due date. More directly, we put $3,000 on one credit card for the van purchase. That was on 2/7. That statement, once it closes, will not have a due date until 4/20. That means that the money put on the credit card can sit in savings earning interest for about 70 days.

We also had to pay the initial payment for the restoration services on the rental that had a burst pipe. So while the insurance company sent us a check to cover the cost of this work, it’s still $17k sitting on our credit card, not being paid until the last minute. I should also note that our cash balance is inflated by about $50k because it’s the money from the insurance company that we’re waiting to pay the contractor as milestones are completed.

Had I seemed nonchalant about the plan? Because I’m definitely not. 🙂 I need to stay on top of how many transfers happen per month out of the savings account (while Mr. ODA randomly pulls money for investments), and not miss any deadlines and cost us interest charges or late payment marks on our credit. It’s stressful! Since we’re not doing anything that requires our credit to be pulled right now, it’s fine. If we were having our credit checked, having multiple cards nearly maxed out would be a problem. But we know we have the cash available to pay off all the credit cards if we needed to.

RENTAL FINANCES

I finally got through to someone on the issue with the improperly installed water heater. He says he submitted all the paperwork to send us a check for $200 to cover the plumber we paid to fix their issue. I haven’t seen any paperwork, nor have I received the check, but I’ll keep it on my radar and follow up in a couple of weeks.

I made all the decisions on the restoration of our flooded house. We’re expecting to hear a timeline for work to start next week, and then it’ll take about 40 working days to get the work done.

I paid a warranty for termites on another house. We had an infestation when we purchased the house, but we didn’t pay the warranty information. Our tenants found swarmers, and when we called to ask about treatment, they said they’d let us backpay the warranty and invoke that. We have a good relationship with this company and appreciated that offer, so we’re staying on top of the warranty payments now. The payment is $98 per year.

We received a surprise in the mail – the tenant had turned off the electric in the flooded house back on January 12th. The power company is supposed to notify me. I received an email on February 6th notifying me of an action on the account. So this was in my name from 1/12 to 2/1 for me to be billed $255 without my knowledge. Not to mention, there’s a bill hanging out there from 2/2 until the present that I’ll also get billed for. Mr. ODA sent our property management excerpts from the lease indicating that the utilities must be in their name for the entirety of the lease, that they’re responsible for this bill, and that they must get it back in their name immediately. We’ll see how that plays out.

RENTAL WORK

I picked up the keys from our property manager for the 3 houses I took over managing. I also worked on a rental here in town this week, which took about an hour including travel time, and I have another to work on later this week, which will be about 2 hours worth of work.

I sent a prospective tenant the pre-application we have, which he passed, so I sent him the application to submit. If all goes well, we’ll have that house re-rented with no vacancy period.

We have 3 leases that end at the end of April. We put a requirement that tenants give us 60 days notice, or that we give 60 days notice of any changes. That means that these leases need acknowledgement by the end of this month. So I ran the analysis on those 3 houses. We decided to increase the rent on 2 of them by $50 per month, each, and we’ll keep another house the same since it was increased last year. One house actually had an increase last year, but that house is well below market value, so we’re offering them to continue the lease with an increase because if they were to move out, we could get even more from the house based on it’s size and demographics. The 2 houses we’re increasing have a property manager, so she’s responsible for notification and signing an addendum before the end of the month. But once again, I need to manage the property manager and ensure we have action on time.

Surprisingly, I didn’t cover all our houses in posts last year. I was going to say, “let’s finish this up,” but we’ve since purchased #14! This is a long post. I tried to separate the stories, but since they were part of the same purchase, it was too convoluted to decide which story went with which house.

We spent the summer of 2019 living in Lexington, KY. Mr. ODA took a temporary job for 3 months, and we spent our summer looking for more rental properties to try another market. The housing costs in central Kentucky were less than central Virginia, but the rental rates were also lower.

We drove around with our Realtor for quite some time. We were hoping to find a multi-door complex. However, 4-8 door units have just not been well taken care of. We take care of our houses, and I didn’t want to inherit all the deferred maintenance of a poor landlord. Many of the places had long-term tenants, so there wouldn’t be a vacancy to ease getting work done either. Additionally, there were several that we saw where the tenant was home, smoking and telling us all that was wrong with the property. It was abysmal.

So after searching through many other options, we settled on two houses at the same time.

FIRST OFFER

Mr. ODA actually made an offer on a house in Winchester that I hadn’t seen. It was a large house that had been converted into 2 units. Mr. ODA and our Realtor went after work one day, and it wasn’t worth me packing up the baby and driving a half hour to meet them for one house. However, I did get to see some of it because I took on the home inspection appointment. Since I had never walked through the house, it was easy for me to objectively see the information on the inspection and convince Mr. ODA to walk away. There was just too many big-ticket items (e.g., not enough head room for stairs, water damage not properly cleaned up in multiple rooms, several code violations) and deferred maintenance that it wasn’t worth us putting the money into it. The tenants were sitting on the porch smoking during the inspection, and I didn’t love the idea of inherited tenants that were allowed to smoke in the house.

SECOND OFFER

I can’t tell the history of these purchases without this gem of a story. Mr. ODA found a house that was in a decent shape in Winchester.

Aside: We focused on Winchester because while the rent income was low, the housing cost was also low. Whereas in Lexington, the rent was low, but the housing prices were higher.

We made an offer on the house. In the offer, it lists the seller’s name. It was a State Senator! When we sent over the offer, the seller’s agent agreed to our details, but asked for a pre-approval letter before he’d sign. The amount of weight the people in Kentucky put on a pre-approval letter is absurd, in my opinion. We went through the effort to get the letter and send it over. About that same time, the seller’s agent said someone else came in with a better offer, so we could either submit our highest and best offer, or lose the deal. The sketchiness of the action floored us.

The house had been on the market for a month. We had a verbal agreement (that had even been put in writing, but not yet signed). What are the odds that someone came in at the same time as us with an offer over asking for a house on the market a month? We called his bluff, and we were wrong.

THIRD AND FORTH OFFERS – UNDER CONTRACT

In August 2019, we went under contract on two houses in Winchester, KY.

Property12 had been owner occupied and flipped to sell. The owner had lived there long enough that she wouldn’t Docusign the contract, and we had to wait for her to initial, sign, and date all the pages by hand. The house had been listed for 36 days when we made the offer. It was listed at $115,000, and we went under contract at $112,000 with $2,000 in seller subsidy (closing costs) on 8/7. It’s a 3 bed, 2 bath ranch at 1120 sf.

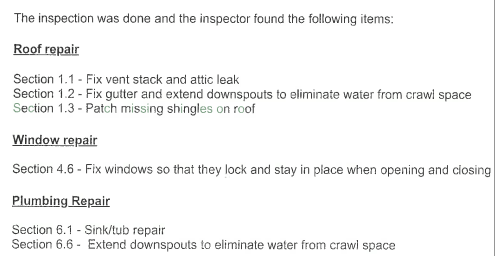

We received the home inspection on 8/14. We asked for the items below to be addressed, or to take $1000 off the purchase price. They agreed to fix the issues.

Property13 had been listed for nearly 3 months before we made an offer. It had been most recently listed at $105,500. Our offer was for $102,000 with $2,000 seller subsidy. We also included the following requirement in the contract: Seller agrees to remediate the water and mold in the crawl space, fix the down spout next to the crawl space door so that it channels the water away from the home, replace the missing gutter on the front of the house, and repair the rotted facia and sheathing on the front of the house.

Additionally, we had a home inspection on the house and identified the following items for them to repair.

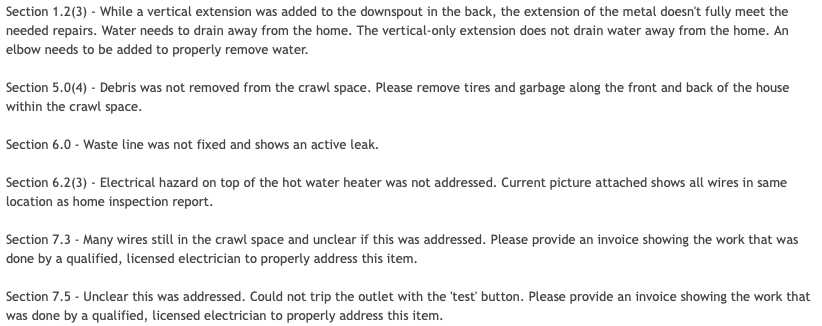

Getting the sellers to identify that these items were done before closing was not an easy task. We checked the day that closing was originally schedule for and noted that several things were not complete.

Then, at 7:30 pm the night before closing (which had already been delayed a week), we received one receipt identifying a couple of things were done. Eventually we received documentation that it was taken care of.

LOAN DETAILS

The options we typically ask for when considering the direction of our loan are as follows.

We chose the 25% down – 30 yr fixed option for both properties. Our goal is to not pay points, so that led us to the 25% down options. Since there was no incentive to take a shorter term (thereby increasing your monthly mortgage payments and decreasing your cash flow), we chose the 30 year option.

These loans were originated in September 2019. We processed multiple cash-out-refinances on some of our properties in December 2021; we used it to pay off about $66k on Property12 and about $74k on Property13.

LOAN PROCESSING & DELAYED CLOSING

We had a lender that we loved in Virginia. She couldn’t cover loans in Kentucky, but the company itself had a branch that could do it. She referred us to someone in Kentucky. It was the worst experience I’ve had in closings. Our closings are always annoyingly stressful in that last week, but this was bad throughout the month and then bad enough that our closing was delayed a week – completely due to the loan officer’s inability to manage the loan.

We had multiple issues over the course of the week we initiated our relationship just accessing the disclosures. They kept telling us to sign things we didn’t receive, or they’d tell us our access code and then when I say it doesn’t work, act like they never told us different information and give new information.

On August 16, I had to tell the loan officer that one of the addresses was wrong. THE ADDRESS. On August 26, we received conditional approval of our loan from underwriting. On August 27, we received our appraisal with no issues noted. But at that point, our August 30 closing was delayed a week already.

That’s where the problem was – our appraisal was ordered late, had to be rushed, and still didn’t make it in time for them to develop the Closing Disclosure (CD) and get us to a closing on August 30. The loan officer never once acknowledged that he ordered the appraisals late, causing this delay. It took asking for timelines from his supervisor, and piecing together emails we had on hand, to show that it was his fault.

On August 29, I finally made contact with the loan officer’s supervisor and was rerouted to someone else to get the job done. I had to repeat all of our issues and the errors that were found on the CDs.

On September 3, I was given disclosures that were still wrong. The new loan officer claimed that what she put in the system was correct, so she wasn’t sure what was wrong, causing me to once again outline all the errors.

On September 4, I was asked for more documentation that wasn’t caught during underwriting. I was furious.

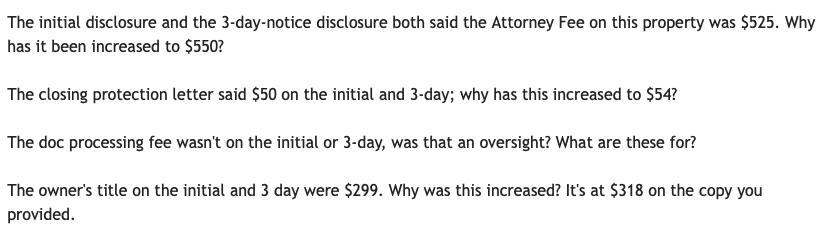

On September 5, I gave up talking to our lender about issues on the CD and spoke directly to the Title Attorney’s office, who was much more knowledgable and responsive. Here’s an example of what I’m questioning when I look over a CD. Some of these seem small (e.g., $4 difference, $25 difference), but you can see how these add up, both on a single transaction and when we’re processing several homes in one year. Not to mention – why pay more for something than you were quoted or you’re supposed to?

Another surprise that came our way was a “Seller Agent Fee” for $149 per transaction. At no point in time was an additional fee disclosed to us by our Realtor. A typical transaction has 6% commission paid by the seller, which is traditionally split 3% and 3% for the buyer and seller representation. Being that these were Rentals #12 and 13, in addition to 2 personal residences we had purchased, imagine the surprise when we, as buyers, were being charged for representation. We questioned why this wasn’t disclosed to us up front as a Re/Max requirement, and it was taken off our CD.

CLOSING DAY

I had planned to leave town the Friday after the original closing date because that was the last date that we had our apartment. I didn’t want to move me and the baby into my in-laws house and continue the poor sleep we had been dealing with by not being at home. So even though closing was delayed, I left. Mr. ODA had to be my power of attorney. He had to sign his name, write a blurb, and then sign my name on ALL those papers that are part of a closing….. times two. Eek. I didn’t know that at the time (but baby went back to sleeping perfectly once we were home, so it was worth my sanity 🙂 ).

At 11:30 am on closing day, the lender claimed that the power of attorney documents (from the lawyer…) were not complete enough to be counted as filed on their end. I appreciated the snip from the attorney when questioned.

I always wondered why tv shows always showed both at the closing table with a ceremonious passing of the key. We’ve had our share of weird closings (in a closet, in a parking lot, at our dining room table), but we never sat at the table with the seller in Virginia. We were so confused about how specific the closing attorney was being about the closing time options, and then we found out that the seller and buyer are at the table together in Kentucky. The seller for Property12 was so rude to Mr. ODA through the transaction! She kept grilling him on whether he addressed the utilities. The seller shouldn’t be allowed to talk to the buyer! We’ve since been able to process 3 transactions in Kentucky and avoid the seller at the table, but I’d like to advocate that Kentucky move away from this buyer/seller meeting process!

RENTAL HISTORIES

Property12 was listed at $895 on 10/2. Based on my birds-eye-view of the area, I thought $1000 was going to be easy to rent it at. Based on the 1% Rule that we had followed in Virginia, we should have a goal of $1,100 per month. However, we were trying for a Fall lease, which is more difficult than a Spring lease, so I thought listing at $995 would get quick movement instead of letting it sit for too long. Our property manager disagreed. She also said we were limited our pool of candidates by not allowing smokers; but, the whole house is carpeted and I was not budging on that.

We found a tenant on October 16 and allowed her to move in right away, but not start paying rent until November 1 if she agreed to an 18 month lease (we really wanted to be on a Spring renewal going forward). That was an unfortunate blow to our expectations – nearly two whole months without rental income on a house we didn’t need to do any work to.

We increased rent to $950 as of 6/1/2022 after no previous increases.

Property13 was listed for rent at $995 with no movement. We dropped to $875 and offered free October rent for however long was remaining in the month. A lease was established on 10/18/2019. Our property manager was supposed to establish an 18 month lease and didn’t. Luckily, the tenant agreed to a 6 month extension.

Property13 renewal came in April 2022. She had balked about the state of our economy in 2021, and we backed off the proposed increase at that time. Well, all the jurisdictions finally jumped on the increased assessments, and we saw a drastic increase in our costs. We told her that the new offer for a year lease is $950, which is higher than we’d typically increase in one year ($75 instead of $50). But we told her that we were willing to let her walk if she didn’t agree to it since she originally negotiated a lower cost and argued an increase at the 18 month mark, which we let go. She tried to fight it, but our property manager told her to check the rental options in the area to see that she’s still getting a deal. She agreed to the increase.

MAINTENANCE HISTORIES

Property12 requires a new heat pump in June 2021. We paid $3900 for a whole new system, which is a funnily low number just a year later.

The tenant there complained of high water bills. I asked to see a history of the water bills to know how much was considered higher than their average usage. The property manager agreed that the toilet was running and causing higher bills, but also admitted that they attempted to fix the toilet twice over a 3 week period, with multiple days between receiving a maintenance request and taking action. While I agreed that we could compensate her for the issue, I couldn’t quite pinpoint why this was my financial burden and neither the tenant’s nor the property manager’s. I followed up with more information from the property manager with questions like: Why did it take the tenant from 9/20 until 10/11 to identify the issue still remained and that there was a waste of water? They indicated that they believe they made a good faith effort to address the issues as reported. I eventually settled on a $25 concession on one month’s rent.

Property13 had several issues with the hot water installation that were eventually resolved, which was frustrating after we tried to manage issues with the hot water heater through the home inspection process and received documentation as if it was complete. The tenant requested pest control in July 2020 claiming that a vacant house next door caused an increase in pests. I was frustrated because that’s not how it works. I approved treatment at that time, and then she came back with another request in October. Luckily, I haven’t heard about pests since then. In my Virginia leases, we’ll handle some pest control requests, but if there are roach issues once a tenant has been there for some time, we don’t typically pay for that type of treatment.

SUMMARY

All in all, these tenants have been pretty quiet. They ask for random maintenance things here and there, but they’re not usually big-ticket items (except that HVAC replacement!). Our property manager has been more difficult than the tenants.

Being that we were used to the 1% Rule when we purchased these houses, it’s unfortunate that even at 3 years in, we’re not renting it at 1% of our purchase prices. Our cash-on-cash isn’t completely accurate right now because I won’t see our taxes for this year for another month or two. Being that jurisdictions kept the tax amount steady through the pandemic, I’m expecting to see an increase in assessments for this year. I’ve also seen big increases in our home insurance policies, so that will probably eat into our cash flow as well. Our cash-on-cash analysis on Property12 is about 6.5%, and it’s about 7.5% on Property13. These numbers are only slightly lower than our expectation/desire, with our average being about 8%.

In the upcoming year, we’re going to look to get rid of our property manager, so these houses may begin needing more attention from us. It’s been hard to take on more when paying a property manager has been a sunk cost at this point. However, the frustration of managing their management (e.g., making sure charges are correct, not getting a full picture of what work is being done, and then paying them a significant amount of management money and leasing money only for them to claim that checking on the property requires additional fees) has led to us wanting to take it on since we’re in town now. The current lease terms are up in April and May, so if we’re going to take on management, it should be before the possibility of paying them half a month’s rent for leasing it (not to mention they’re notoriously 4-6 weeks out in every leasing attempt they’ve done for us, whereas I’ve never had an issue getting a property leased within a week).

This month is basically just story telling, from insurance tidbits to mortgage annoyances, while not addressing the decline in the market and our investment accounts. 🙂

It seems all my mortgage payments are increasing on 3/1, so I’ve been managing those changes. I mentioned recently that one of our houses had the escrow analysis done incorrectly. Luckily, that was addressed, and the increase in our mortgage payment is only about $100 instead of nearly $200. Our personal mortgage increased by $16, another property increased by $52, and then our last 3 mortgages were all refinanced in January and this ‘first payment’ has been a bear. The information out of the refinancing company has been contradictory, they requested a bunch of information weeks after closing to support all the money they already gave us, and it’s just been rough. Rough enough that I ran to the post office to get a check in the mail at 4:48 pm today, only to get home to an email saying that I had to send that check (due tomorrow) to a different address. Ugh.

I was excited to share some positive news this month, but that got overshadowed by these mortgage payments! Anyway, we came home to some surprises after our vacation.

First, I had a medical procedure done in January. It was originally scheduled for November, but the week of the procedure, I had my heart go crazy on me. That cancelled my procedure because I couldn’t go under anesthesia until they knew my heart would be OK. We got my heart sorted out enough that I was cleared for the procedure, but once I was able to reschedule it, it went into 2022 ….. a new deductible year. They said that I needed to pay half the cost of the procedure before they’d schedule it. Since I had been waiting since September for this, I wasn’t going to question anything, and I gave my credit card number for $1200. Well, my insurance hasn’t processed the procedure yet, but I guess since I paid in advance, some sort of system review showed I had overpaid, and they refunded me $1196. I don’t know how they decided to keep $4, but I’ll cross that bridge when I see my claim is processed on my insurance website.

Second, I’ve mentioned before that you need to stay on top of insurance! I received a bill for my heart-related-ambulance-ride for over $900. The last time I was in an ambulance, I ended up owing the full bill, which was $500 at that time. When I saw $900, I figured, gosh 10 years later and a new jurisdiction, and THAT is what I owe. It said “we billed your insurance, and this is your balance.” Hmmm. Log into my insurance website and see there’s no claim history for an ambulance ride. I then learned, for the first time ever, how to submit my own insurance claim. I let the fire department know I submitted the claim, and then they said they’d do it for me! Why did your paper say you already did?! Well, the surprise I got was that my insurance covered all but $46 for the ride!!! I couldn’t believe it. That’s the happiest I’ve ever been to spend $46.

The most random thing that happened was a check from our electric company from our Virginia house. We sold that house in September 2020. Our mail forwarding isn’t active anymore and it was sent to our old address, so I really have no idea how we got it. It was $31.09 due to a required review of all accounts every 3 years. It’s not anything crazy or life changing, but that was truly a surprise!

RENTAL UPDATES

We had our usual suspects not pay rent earlier this month. One flat out said they won’t pay until the 23rd. I’m not even sure how to handle them anymore. I keep reminding myself that we raised their rent $150/month to get them to leave, but they accepted. So at least we’re in a good position there? The other paid us $700/$1150 on Friday (late). She at least emailed us with the awareness that we shouldn’t have to hunt her down for rent payments, so she got a pass because I was about to send the default notice at 12:01 am on the 6th. I’m also once again in a position of tracking down a rent relief payment on another house that’s supposed to cover December, January, and February. While the tenant ended up paying December rent, we’ve still been floating the January and February finances. The approval of their application (that was submitted in November) was January 10. As of today, no information from the State and no check in the mail.

I got a tenant renewal processed this morning. We increased their rent by $50/month (starting 5/1 when their current term ends), after it having been steady for 2 years. Our usual baseline to keep a good tenant is a $50 increase every 2 years.

We gave two property managers notice to increase rents on 2 properties that are up for renewal on 4/30. We do 60-day notices. It’s not entirely necessary, but I look at it as a way to negotiate with the tenant for a month, and then if they don’t agree to new terms, we have a month to get it rented. One ‘cried COVID’ last year, and we let her by. She’s been there 2.5 years at the same rate, and she even got the house under market value originally because it was November (bad timing). She’s at $875 and we said we’d go to $950. That’s a larger increase than we usually do, but the market rate for the house is $950-1000. If she balks, we’ll manage the turnover and get a new tenant in there. For another house, they’re at 1025 and have been since October 2019. They even negotiated a discount back then for an 18 month lease, so they’ve been under market. Despite our efforts to grieve our taxes, the City thinks this house is in an affluent neighborhood and has charged as such. We’re offering them a bump to $1100. Again, more than our usual $50 increase, but it’s been more than 2 years and $1100 is under market value. Then we had a 3rd person say she wants to stay in the house, but her lease isn’t up until August. She’s been there since August 2017 and has been at $850 rent since then. We’re looking to increase her rent to $900. She’s an awesome tenant that never needs anything, and I know she’s in grad school without much money. We’ve made her so happy for the last several years by renewing her without an increase, so I hope she understands the need to increase it now.

I paid the insurance on our townhome, which is a property we own outright, so I need to manage the escrow-type transactions. That was $210.

After our cash-out-refis in January, we have been looking for a new property to purchase. We’ve made 4 offers that have been out-bid. Mr. ODA has been trying to work the off-market angle. We made a full price offer for one of the houses contingent on seeing it, and the guy said that he’d now prefer to sell off his portfolio as one instead of each individual house. He declined our full-price-off-market offer. Sketchy. Then another guy said he wanted to wait until the new flooring was installed in his house before letting us see it, and then he won’t respond to messages now a week or so later. Interesting. We’re now trying to work another off-market deal through our Realtor, but the seller and our Realtor are out of town. I ran the comps on it and come to $235ish, while they were expecting $250k. I don’t deny that they’d get an offer in this market at $250, but I don’t know that it’s worth it to us. Then again, to be done with this driving around, seeing houses, making offers, and losing out, may all be worth an extra $15k.

PERSONAL TIDBITS

This month, we went on a trip for just about a week. The flight was paid for in a previous month, so that’s not captured in our spending. We stayed with a friend, and she made us nearly all of our food. We paid for our brewery visits with her. It was a great trip, and I definitely recommend Bend, OR! We did a last minute change from Touro for our rental car to a ‘regular’ car rental place at the airport, so that charge shows up in this month’s finances. We also booked 2 last minute hotel rooms, once for the night of our arrival and one for the night of our departure (we flew in/out of Portland, which is about 2.5 hours from Bend, so it was easier with the kids sleep schedules to be near the airport those two nights instead of arriving really late or leaving really early).

We bought Hamilton tickets. We were late on that band wagon until we finally found a friend with Disney+ who wanted to watch it with us even though they had seen it 257 times. Since December 2020, we’ve watched Hamilton a whole lot. We got on right when tickets were being sold and were about to accept the $200+ ticket price until Mr. ODA found the ticket sales through the actual venue were only $130! It’s not until June, but that’s something to look forward to!

We finished our basement over the last year and have been using for the last month now. We had a projector on hand that we used as our TV down there, but it started to die shortly after we hooked it up. We bought a new projector and have been really happy with it, and I was happy with it only being $270.

While our electric bill was surprisingly low last month, it was surprisingly high this month. They did an estimated meter reading, putting the estimated kWh usage at the highest it’s ever been. When I questioned their estimation process and shared the current meter read, they said that next month will probably be an actual reading and since it’s not more than 1000 kWh difference, they’re not going to change anything. Sure, I can afford this $414 bill that may be offset next month, but many people can’t. Their estimation process shouldn’t put the projected energy usage at an all-time-high, thereby dumping surprisingly large bills on people. Regardless, it’s something that works itself out, and isn’t something I’m going to fight any harder on right now. It’s just annoying knowing that our energy usage was high last year because we had a broken unit without our knowledge, and then with a working unit, they’re estimating that we’ve used more than ever.

Mr. ODA changed one of our credit cards, so I’ve been all out of sorts here now. The credit card was a travel-related card, and they increased their annual fee by $100. He ran the numbers and determined the benefits didn’t outweigh the cost increase. Instead of closing the card, they agreed to change the type of card. However, all the things we used that card for are now on different cards, and this change “activated” an old card of mine. Our credit card usage is convoluted; perhaps I’ll do a new explanation and update my last post on it (and then maybe that’ll get me to remember all the changes!).

NET WORTH

Our net worth dropped about $15k from last month, but that was due to the market. While not fun to see those numbers go down, it doesn’t affect our day-to-day. Our cash balance is really high right now while we keep cash liquid for a downpayment while finding another investment property.