I have a tenant who, in the same day, told me that she couldn’t pay rent on time and asked whether she could buy the house. She said she paid $60,000 to me and that could have gone towards owning a house. While I understand the lump sum of what you paid being a pain point, owning a house isn’t that simple. I thought I’d break down a comparison of what she would have done to own this house versus her renting it over the last several years.

RENT HISTORY

Based on the proximity to Main St and the comps in the area, we went into the purchase expecting about $1,000 per month in rent. At the 1% Rule (where you set monthly rent at 1% of your purchase price), we should have been at $1,020. Knowing that it was October/November by the time we would get it rented (there aren’t as many people looking for a new rental in the Fall, after school has started and holiday activities are ramping up) we chose to list it at $975 and keep it below that 4 digit threshold. It sat for 3.5 weeks with hardly any activity, and we dropped it to $875. We found a tenant in under 2 weeks then, but we weren’t thrilled amount our cash flow on it.

The tenant’s lease started on November 1, 2019. Her rent was $875. My property manager incorrectly established a one-year term lease instead of an 18-month lease like she was supposed to, so we had to do a 6-month extension after the first year. Then in March 2021, we tried to increase the rent to $900, and she complained that due to the pandemic, she couldn’t afford that. We let it go and she renewed a year lease at $875.

Come February 2022, we were significantly under market value for rent and she hadn’t been a friendly tenant, so we were content pushing a raise to $950. If she didn’t want to pay that, she was free to leave and we would take the vacancy hit to fix it up and get it re-rented. She complained about the increase, and our property manager told her to take a few days to look around to see if she could find somewhere to rent that was at a price she would feel more comfortable with. She came back and said she couldn’t find anything and accepted the increase to $950.

Not including a few late fees she has owed over the last nearly-five-years, she’s paid us $52,850. While in total that appears to be a significant number, that number does not mean that you’d have $52k in equity in a home had you paid towards a mortgage.

OUR PURCHASE INFORMATION

We paid $102,000 for the house in 2019. We asked for several options for the loan structure. We asked about putting 20% versus 25% down, and whether the rate for a 15 year, 20 year, or 30 year loan would have the best rate. Going through those details is something I’ve done in the past, so for this purpose I’ll just note that we chose to put 25% down because then we didn’t need to “buy down” the rate. The rate for each loan length was 4.55%. With no incentive to do a shorter loan term (and therefore increase our monthly payment), we chose the 30 year term. I do want to note that our interest rate is higher than the average for 2019 (3.9%) because it was an investment property and not a loan for a primary residence.

Based on the 25% down and the closing costs, we had to come to the table with $26,589.12.

Our mortgage was $538.46, which includes escrow. We paid off this loan fairly soon after we closed on it, so we don’t have a monthly mortgage payment. However, I do need to plan for our current mortgage and insurance payments each year, which is currently over $2,000.

FACTORS TO CONSIDER

To keep this more consistent in the message, note that the loan discussed will be based on the purchase price of $102,000.

First, you need to have favorable credit to qualify for the mortgage. In an example, the lowest credit score I could plug in was 620. However, in much of what I’ve read, anything below 680 is questionable on qualification. Our requirement to rent a property is to have a credit score of 600. Perhaps there are lenders that will process a mortgage if your credit score is below 620, but you’re going to pay a premium via the interest rate.

With a credit score of 780, say you’ll have a rate of 6%. But then with a score of 680, you’re looking at 6.5%. At 6%, your principal and interest payment (doesn’t include the escrow required) would be $599.19. At 6.5%, it goes to $631.69. That’s only $32.50 per month extra; over 30 years, that’s an extra $11,700 paid to the bank. I have some tenants where an extra $32 per month is a big deal.

Without at least 20% down on a loan, you’ll likely have to pay private mortgage insurance (PMI). This amount could add a monthly premium to your mortgage payment anywhere from 0.2% to 6%. I did a quick calculator with the example of $102,000 purchase price, $3,060 down (typically the lowest available without any special loan structures is 3%), and a credit score of 620 (lowest it allowed). The PMI was calculated as $187 each month.

I mentioned that our final closing costs were over $26k. If I remove our down payment, that leaves $1,089 in closing costs. I will note though, that our contract had $2,000 in seller subsidy (a credit). Without that purchase agreement structure, that means your closing costs are actually $3,089. This means that you need to come to the table with $6,149. Buying a house is not like buying a car where you can roll all the costs into the loan, and I feel like people don’t realize this.

Your debt to income ratio also plays a factor in whether you can qualify and what your interest rate would be. So even with a decent credit score, you need to show a low debt-to-income ratio, meaning you can’t have your credit cards maxed out. The lender wants to see that you don’t have high monthly costs that would prevent you from paying your mortgage.

That brings me to the flexibility of paying rent. She paid $475 worth of August rent (due August 1st, with a grace period to August 5th before a late fee is owed) on August 20th. If you pay your mortgage late, there’s a late fee and it gets reported to the credit bureaus. Your late payment of rent doesn’t get reported to anyone. She also has the extra advantage that I’m willing to work with her on late payments. An apartment complex type owner is going to immediately file for eviction on the 6th without full rent payment, regardless of your story.

SUMMARY

While a mortgage payment of $538.46 looks favorable against a rent payment of $950, it’s not that simple. I was able to qualify for the mortgage, qualify for a favorable interest rate, and put significant money down.

If I add a premium to the rate we were able to get, assuming my tenant’s credit score is similar to what it was when she rented our house, and then add the PMI that would be applied by not having 20% down, then the mortgage payment (including escrow) would have been $903.02. PMI stays on the mortgage until you reach 78% loan to value ratio (unless you pay for an appraisal and can prove 80% earlier than that). That threshold in this example is $79,560. That principal balance would be achieved in over 11 years, which means you’ve paid $25,058 for essentially nothing.

Then on top of paying these premiums for the mortgage, she would need to pay for the maintenance of the property herself, which is included in my rent factors. I’ve paid over $3,000 for repairs and maintenance on the house over the last 5 years (which is fairly low). However, that includes a deck replacement that we did ourselves and probably would have cost $4,000 instead of the $400 we paid in materials.

So the next time you think that you could be paying half of your rent with a loan, know that you’re not looking at the whole story. There are many factors that go into a mortgage, especially the initial ability to qualify for such loan.

Surprisingly, I didn’t cover all our houses in posts last year. I was going to say, “let’s finish this up,” but we’ve since purchased #14! This is a long post. I tried to separate the stories, but since they were part of the same purchase, it was too convoluted to decide which story went with which house.

We spent the summer of 2019 living in Lexington, KY. Mr. ODA took a temporary job for 3 months, and we spent our summer looking for more rental properties to try another market. The housing costs in central Kentucky were less than central Virginia, but the rental rates were also lower.

We drove around with our Realtor for quite some time. We were hoping to find a multi-door complex. However, 4-8 door units have just not been well taken care of. We take care of our houses, and I didn’t want to inherit all the deferred maintenance of a poor landlord. Many of the places had long-term tenants, so there wouldn’t be a vacancy to ease getting work done either. Additionally, there were several that we saw where the tenant was home, smoking and telling us all that was wrong with the property. It was abysmal.

So after searching through many other options, we settled on two houses at the same time.

FIRST OFFER

Mr. ODA actually made an offer on a house in Winchester that I hadn’t seen. It was a large house that had been converted into 2 units. Mr. ODA and our Realtor went after work one day, and it wasn’t worth me packing up the baby and driving a half hour to meet them for one house. However, I did get to see some of it because I took on the home inspection appointment. Since I had never walked through the house, it was easy for me to objectively see the information on the inspection and convince Mr. ODA to walk away. There was just too many big-ticket items (e.g., not enough head room for stairs, water damage not properly cleaned up in multiple rooms, several code violations) and deferred maintenance that it wasn’t worth us putting the money into it. The tenants were sitting on the porch smoking during the inspection, and I didn’t love the idea of inherited tenants that were allowed to smoke in the house.

SECOND OFFER

I can’t tell the history of these purchases without this gem of a story. Mr. ODA found a house that was in a decent shape in Winchester.

Aside: We focused on Winchester because while the rent income was low, the housing cost was also low. Whereas in Lexington, the rent was low, but the housing prices were higher.

We made an offer on the house. In the offer, it lists the seller’s name. It was a State Senator! When we sent over the offer, the seller’s agent agreed to our details, but asked for a pre-approval letter before he’d sign. The amount of weight the people in Kentucky put on a pre-approval letter is absurd, in my opinion. We went through the effort to get the letter and send it over. About that same time, the seller’s agent said someone else came in with a better offer, so we could either submit our highest and best offer, or lose the deal. The sketchiness of the action floored us.

The house had been on the market for a month. We had a verbal agreement (that had even been put in writing, but not yet signed). What are the odds that someone came in at the same time as us with an offer over asking for a house on the market a month? We called his bluff, and we were wrong.

THIRD AND FORTH OFFERS – UNDER CONTRACT

In August 2019, we went under contract on two houses in Winchester, KY.

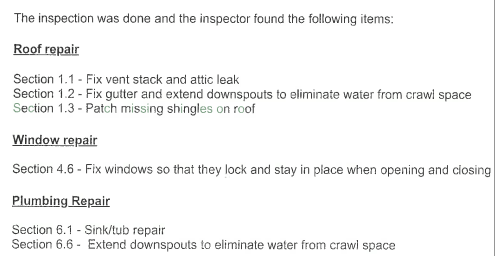

Property12 had been owner occupied and flipped to sell. The owner had lived there long enough that she wouldn’t Docusign the contract, and we had to wait for her to initial, sign, and date all the pages by hand. The house had been listed for 36 days when we made the offer. It was listed at $115,000, and we went under contract at $112,000 with $2,000 in seller subsidy (closing costs) on 8/7. It’s a 3 bed, 2 bath ranch at 1120 sf.

We received the home inspection on 8/14. We asked for the items below to be addressed, or to take $1000 off the purchase price. They agreed to fix the issues.

Property13 had been listed for nearly 3 months before we made an offer. It had been most recently listed at $105,500. Our offer was for $102,000 with $2,000 seller subsidy. We also included the following requirement in the contract: Seller agrees to remediate the water and mold in the crawl space, fix the down spout next to the crawl space door so that it channels the water away from the home, replace the missing gutter on the front of the house, and repair the rotted facia and sheathing on the front of the house.

Additionally, we had a home inspection on the house and identified the following items for them to repair.

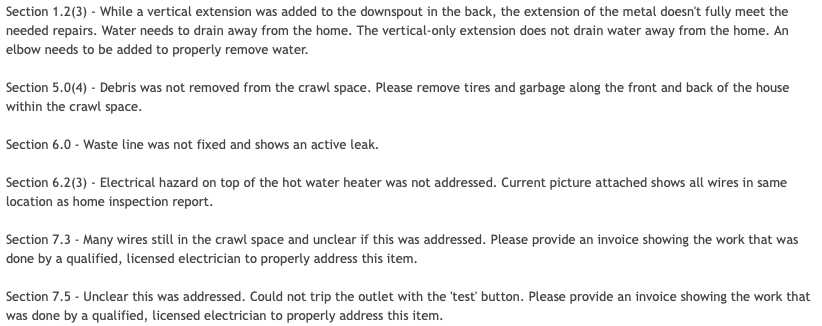

Getting the sellers to identify that these items were done before closing was not an easy task. We checked the day that closing was originally schedule for and noted that several things were not complete.

Then, at 7:30 pm the night before closing (which had already been delayed a week), we received one receipt identifying a couple of things were done. Eventually we received documentation that it was taken care of.

LOAN DETAILS

The options we typically ask for when considering the direction of our loan are as follows.

We chose the 25% down – 30 yr fixed option for both properties. Our goal is to not pay points, so that led us to the 25% down options. Since there was no incentive to take a shorter term (thereby increasing your monthly mortgage payments and decreasing your cash flow), we chose the 30 year option.

These loans were originated in September 2019. We processed multiple cash-out-refinances on some of our properties in December 2021; we used it to pay off about $66k on Property12 and about $74k on Property13.

LOAN PROCESSING & DELAYED CLOSING

We had a lender that we loved in Virginia. She couldn’t cover loans in Kentucky, but the company itself had a branch that could do it. She referred us to someone in Kentucky. It was the worst experience I’ve had in closings. Our closings are always annoyingly stressful in that last week, but this was bad throughout the month and then bad enough that our closing was delayed a week – completely due to the loan officer’s inability to manage the loan.

We had multiple issues over the course of the week we initiated our relationship just accessing the disclosures. They kept telling us to sign things we didn’t receive, or they’d tell us our access code and then when I say it doesn’t work, act like they never told us different information and give new information.

On August 16, I had to tell the loan officer that one of the addresses was wrong. THE ADDRESS. On August 26, we received conditional approval of our loan from underwriting. On August 27, we received our appraisal with no issues noted. But at that point, our August 30 closing was delayed a week already.

That’s where the problem was – our appraisal was ordered late, had to be rushed, and still didn’t make it in time for them to develop the Closing Disclosure (CD) and get us to a closing on August 30. The loan officer never once acknowledged that he ordered the appraisals late, causing this delay. It took asking for timelines from his supervisor, and piecing together emails we had on hand, to show that it was his fault.

On August 29, I finally made contact with the loan officer’s supervisor and was rerouted to someone else to get the job done. I had to repeat all of our issues and the errors that were found on the CDs.

On September 3, I was given disclosures that were still wrong. The new loan officer claimed that what she put in the system was correct, so she wasn’t sure what was wrong, causing me to once again outline all the errors.

On September 4, I was asked for more documentation that wasn’t caught during underwriting. I was furious.

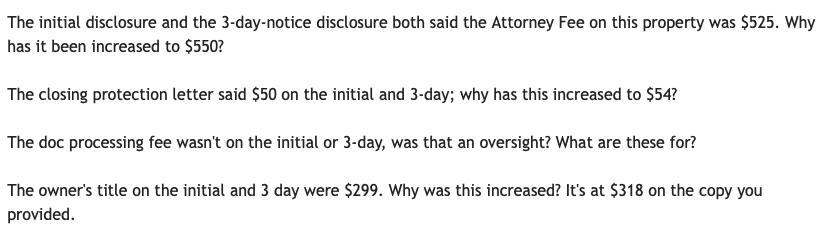

On September 5, I gave up talking to our lender about issues on the CD and spoke directly to the Title Attorney’s office, who was much more knowledgable and responsive. Here’s an example of what I’m questioning when I look over a CD. Some of these seem small (e.g., $4 difference, $25 difference), but you can see how these add up, both on a single transaction and when we’re processing several homes in one year. Not to mention – why pay more for something than you were quoted or you’re supposed to?

Another surprise that came our way was a “Seller Agent Fee” for $149 per transaction. At no point in time was an additional fee disclosed to us by our Realtor. A typical transaction has 6% commission paid by the seller, which is traditionally split 3% and 3% for the buyer and seller representation. Being that these were Rentals #12 and 13, in addition to 2 personal residences we had purchased, imagine the surprise when we, as buyers, were being charged for representation. We questioned why this wasn’t disclosed to us up front as a Re/Max requirement, and it was taken off our CD.

CLOSING DAY

I had planned to leave town the Friday after the original closing date because that was the last date that we had our apartment. I didn’t want to move me and the baby into my in-laws house and continue the poor sleep we had been dealing with by not being at home. So even though closing was delayed, I left. Mr. ODA had to be my power of attorney. He had to sign his name, write a blurb, and then sign my name on ALL those papers that are part of a closing….. times two. Eek. I didn’t know that at the time (but baby went back to sleeping perfectly once we were home, so it was worth my sanity 🙂 ).

At 11:30 am on closing day, the lender claimed that the power of attorney documents (from the lawyer…) were not complete enough to be counted as filed on their end. I appreciated the snip from the attorney when questioned.

I always wondered why tv shows always showed both at the closing table with a ceremonious passing of the key. We’ve had our share of weird closings (in a closet, in a parking lot, at our dining room table), but we never sat at the table with the seller in Virginia. We were so confused about how specific the closing attorney was being about the closing time options, and then we found out that the seller and buyer are at the table together in Kentucky. The seller for Property12 was so rude to Mr. ODA through the transaction! She kept grilling him on whether he addressed the utilities. The seller shouldn’t be allowed to talk to the buyer! We’ve since been able to process 3 transactions in Kentucky and avoid the seller at the table, but I’d like to advocate that Kentucky move away from this buyer/seller meeting process!

RENTAL HISTORIES

Property12 was listed at $895 on 10/2. Based on my birds-eye-view of the area, I thought $1000 was going to be easy to rent it at. Based on the 1% Rule that we had followed in Virginia, we should have a goal of $1,100 per month. However, we were trying for a Fall lease, which is more difficult than a Spring lease, so I thought listing at $995 would get quick movement instead of letting it sit for too long. Our property manager disagreed. She also said we were limited our pool of candidates by not allowing smokers; but, the whole house is carpeted and I was not budging on that.

We found a tenant on October 16 and allowed her to move in right away, but not start paying rent until November 1 if she agreed to an 18 month lease (we really wanted to be on a Spring renewal going forward). That was an unfortunate blow to our expectations – nearly two whole months without rental income on a house we didn’t need to do any work to.

We increased rent to $950 as of 6/1/2022 after no previous increases.

Property13 was listed for rent at $995 with no movement. We dropped to $875 and offered free October rent for however long was remaining in the month. A lease was established on 10/18/2019. Our property manager was supposed to establish an 18 month lease and didn’t. Luckily, the tenant agreed to a 6 month extension.

Property13 renewal came in April 2022. She had balked about the state of our economy in 2021, and we backed off the proposed increase at that time. Well, all the jurisdictions finally jumped on the increased assessments, and we saw a drastic increase in our costs. We told her that the new offer for a year lease is $950, which is higher than we’d typically increase in one year ($75 instead of $50). But we told her that we were willing to let her walk if she didn’t agree to it since she originally negotiated a lower cost and argued an increase at the 18 month mark, which we let go. She tried to fight it, but our property manager told her to check the rental options in the area to see that she’s still getting a deal. She agreed to the increase.

MAINTENANCE HISTORIES

Property12 requires a new heat pump in June 2021. We paid $3900 for a whole new system, which is a funnily low number just a year later.

The tenant there complained of high water bills. I asked to see a history of the water bills to know how much was considered higher than their average usage. The property manager agreed that the toilet was running and causing higher bills, but also admitted that they attempted to fix the toilet twice over a 3 week period, with multiple days between receiving a maintenance request and taking action. While I agreed that we could compensate her for the issue, I couldn’t quite pinpoint why this was my financial burden and neither the tenant’s nor the property manager’s. I followed up with more information from the property manager with questions like: Why did it take the tenant from 9/20 until 10/11 to identify the issue still remained and that there was a waste of water? They indicated that they believe they made a good faith effort to address the issues as reported. I eventually settled on a $25 concession on one month’s rent.

Property13 had several issues with the hot water installation that were eventually resolved, which was frustrating after we tried to manage issues with the hot water heater through the home inspection process and received documentation as if it was complete. The tenant requested pest control in July 2020 claiming that a vacant house next door caused an increase in pests. I was frustrated because that’s not how it works. I approved treatment at that time, and then she came back with another request in October. Luckily, I haven’t heard about pests since then. In my Virginia leases, we’ll handle some pest control requests, but if there are roach issues once a tenant has been there for some time, we don’t typically pay for that type of treatment.

SUMMARY

All in all, these tenants have been pretty quiet. They ask for random maintenance things here and there, but they’re not usually big-ticket items (except that HVAC replacement!). Our property manager has been more difficult than the tenants.

Being that we were used to the 1% Rule when we purchased these houses, it’s unfortunate that even at 3 years in, we’re not renting it at 1% of our purchase prices. Our cash-on-cash isn’t completely accurate right now because I won’t see our taxes for this year for another month or two. Being that jurisdictions kept the tax amount steady through the pandemic, I’m expecting to see an increase in assessments for this year. I’ve also seen big increases in our home insurance policies, so that will probably eat into our cash flow as well. Our cash-on-cash analysis on Property12 is about 6.5%, and it’s about 7.5% on Property13. These numbers are only slightly lower than our expectation/desire, with our average being about 8%.

In the upcoming year, we’re going to look to get rid of our property manager, so these houses may begin needing more attention from us. It’s been hard to take on more when paying a property manager has been a sunk cost at this point. However, the frustration of managing their management (e.g., making sure charges are correct, not getting a full picture of what work is being done, and then paying them a significant amount of management money and leasing money only for them to claim that checking on the property requires additional fees) has led to us wanting to take it on since we’re in town now. The current lease terms are up in April and May, so if we’re going to take on management, it should be before the possibility of paying them half a month’s rent for leasing it (not to mention they’re notoriously 4-6 weeks out in every leasing attempt they’ve done for us, whereas I’ve never had an issue getting a property leased within a week).

Our 11th purchase was a 4 bedroom and 2 bathroom house, which we were excited about. We only had one other 4 bedroom, and it only had 1.5 baths, so this was a new demographic we could meet. We again needed a mortgage, but we were tapped out (max of 10 mortgages allowed per Fannie Mae), so we went to our partner. I went through the process of establishing the partnership in the House 10 post.

The house had been listed for sale in July 2018, dropped the price in October 2018, and we went under contract on it on December 1, 2018. We went under contract at $129,000, which meant, according to the 1% Rule, we would look to rent it for at least $1290.

The house required a lot of cosmetic work (relative to our usual purchases) before we could rent it. The biggest hold up was the carpet replacement, but we had to do a lot of cleaning and painting also. We closed on February 4, 2019; got to work on the house on the 6th; and then had it rented on March 3, 2019. That’s a longer turnaround time than we’d like, but we thought the long-term benefits of a 4/2 house would be worth it. Plus, with our goal being $1290 based on the 1% Rule, we were happy that we rented it at $1300 and through March 31, 2020.

LOAN TERMS

We were given two options from the loan officer. Both options required 25% down. We could do a 15 year mortgage at 5.05% or a 30 year mortgage at 5.375%. The 15 year mortgage payment was $865, while the 30 year was $640. Since both options required 25% down and we aren’t concerned with our monthly cash flow (as in, we’re not living off of every dollar that comes out of these houses right now), we chose the 15 year. Escrow changes over the last few years have increased the mortgage to $941, unfortunately. However, we’ve been paying off this loan with pretty substantial chunks of money thrown at it. The loan started at $96,750, and the current balance is $21,350. We would have liked to have this paid off a few months ago, but we need to time our payments with our partner, who recently paid for a wedding, renovations to a new house, and a new tear-down property adjacent to his personal residence that he’s going to build a garage-type thing (city living = street parking for him).

We went under contract at $129,000, and the house appraised at $140,000, so that was a nice surprise. The current city assessment is at $148k, but it would likely sell for more than that.

PARTNERSHIP

Since the LLC was already under way when we purchased House 10, we needed to add this one to the LLC. We contacted our attorney. He processed all the paperwork, and we showed up just to sign everything in a quick meeting. At this time, we also requested an EIN be established for the LLC. To process adding this to an established LLC, it cost us $168 (which we paid half of since we’re split 50/50 with our partner).

PREPARING TO RENT

This house was probably the second most effort we had to put in to prepare it for renting. We had to replace quite a few blinds that were broken, do a deep clean of everything, install smoke alarms, paint, replace the carpet, and do some subfloor work.

We had to paint nearly every room (one room we even painted the ceiling the same color as the walls because the ceiling was in rough shape, and it wasn’t worth the time for precision of the edges).

The floor at the front door was rotted by termites. The guys had to cut out the floor and replace the wood before the new carpet could be ordered. We needed the house treated for termites at that point since there was an active infestation that we found. Depending on time and price, I’d rather replace carpeted areas with hard surface flooring for easier maintenance. Since we were already losing time with all the maintenance on this house to get it ready to rent and it was a small area, we just went the easy way out and put new carpet in. The carpet was only in the living room and hallway; all the bedrooms have hardwood flooring.

FIRST TENANTS

We were able to get a family in the house fairly quickly after we finished our work. We rented it at $1300. They signed it on March 3rd, and I had set the terms until March 31, 2020 (this comes into play later). The family had been renting with a roommate (and the husband’s boss!), and that guy had wanted to leave the house. In January 2020, the tenant said, “we signed the lease on March 3rd, so we want to be out at the end of February.” That’s not how leases work. The lease signed said until March 31, 2020. Some time between us telling him that he was in our lease until the end of March, not February, and the end of February actually coming, they decided they wanted to renew their lease. They signed a new lease with us on March 11 to cover 4/1/2020 through 3/31/2021.

In April 2020, the tenant received a job offer in Texas. He asked about a lease break, and we offered an option. All the communication was done via text message, so it was technically in writing, but there was never a “wrap up” text that identified all the agreed upon terms to allow for the lease break. I used this as a teaching opportunity for the 3 of us in the LLC that clearly documenting agreements in writing (preferably with signatures) is important.

The tenant offered to pay May rent without prompting, so we thought that was covered. The part that needed to be detailed was what was considered a “lease break” fee. We had agreed to 60 days worth of rent, and the security deposit couldn’t be used to pay that. Mr. ODA tried to contact the husband on multiple occasions to get rent paid at the beginning of May, but there was no response. I finally sent an email, detailing that they agreed to pay May’s rent, and that technically, they were on the hook for the entire year’s worth of the lease (quick aside: while that’s what the lease says, I think a caveat in the law actually means they’re not really liable for the whole amount because once the house is vacant for 7 days, it defaults back to our ownership, and then we have to show due diligence to re-rent it, leaving them liable for only the gap period). Well, as usual, the landlord gives us a guilt trip (their daughter was in the hospital in TX) instead of separating that from the concept of “pay your debts owed.” As a person, I feel for you on this; as a business owner, it’s not my responsibility to manage your finances and personal life.

The tenant called Mr. ODA and yelled at him. A few hours later, presumably with a more clear head, we received a fair response via text. He even apologized for yelling on the phone. He paid the last few hundreds that were owed, and we all moved on.

SECOND TENANTS

After our first tenants vacated the house, we had to get the house turned over. There was a good bit of work that needed to be done for just a year of someone living there. They had also left stuff behind that became our responsibility to get out of the house. We listed the house for rent. Our partner showed it to 3 younger people who would rent it together. They seemed great until we ran their background and credit check. They had evictions they didn’t disclose (claimed they didn’t know), so we shared the report with them and continued showing it.

We ended up showing it to a couple, and they liked it. After we accepted their application, we were able to get the lease signed on May 7, 2020. Since this was at the very beginning of the pandemic, we had to get creative. I signed this lease on a street corner (hadn’t realized that the place I had selected with outdoor seating was closed!), and they paid their first month’s rent, security deposit, and pet fee in cash that he handed to me in a sock (with a warning that told me this wasn’t the first time he handed someone cash like this haha). They’ve been great tenants, and they renewed their lease.

MAINTENANCE

The new carpeting when we first bought the house cost us $700. Between the termite treatments and other general pest control, we’ve spent $950.

Once the first tenant moved in, we learned of some other issues that weren’t apparent by us just working there and not living there. We had the plumber come out to fix several issues with the hot water that cost us $1450! Then we found out that the master bathroom shower wasn’t installed properly, and it was missing a p-trap; that cost us $325.

Our insurance carrier didn’t like that there wasn’t a handrail for the front steps of the property, so in March 2020, we had to have one installed at $190.

We had to replace the washing machine in April 2020 for about $500. As I’ve shared, we try to not include any ‘extra’ appliances because then maintenance and replacement are our responsibility. This was a fun one – we replaced it just to make the tenants happy and not deal with maintaining it, and then those tenants left right after that, and our new tenants brought their own appliances (so they just have two washers and two dryers in their kitchen).

We had an electrical issue with the master bathroom that cost us $150.

Luckily, I did the inspection over the summer, and nothing came of that initially. We did end up replacing a fan in the master bedroom because the light part of it stopped working with the switch. Since we don’t live near the house anymore, and our partner was in the middle of getting married, we went through Home Depot to have it installed, so all together (fan/light and install) it was about $175.

SUMMARY

This has been a good house. We didn’t realize that the house is located outside the city limits, so we needed to figure out trash pick up in the county (not included in the taxes). Other than a few maintenance hiccups, things have been smooth sailing. We’re happy with the tenants who are there, that they’re maintaining and cleaning the house, and we’re getting our desired rent amount (that they pay on time every month). The street is in a decently nice neighborhood with a lot of original owners, which helps it keep (and increase) its value.

There’s a company in Virginia that advertises no-closing-cost-refinances. If it’s your personal residence, then this holds true. For investment properties, there are some closing costs, but it’s cheaper than the usual refinance. We used them for two other loans – one at the beginning of the pandemic when we signed the paperwork in a tent in the parking lot, and another where we signed the paperwork at our kitchen table in Kentucky with a traveling notary (that’s a thing!).

There was a threshold requirement in order to qualify for this refinance, and that was the new loan had to be at least $100,000. Only 2 of our houses had a loan originated for over $100k originally, so that limited our abilities.

Mr. ODA came to me and said he wanted to do a cash-out-refinance. This company had changed their policy, and they’d allow a cash-out-refinance to get us to the 100k threshold. The first two Virginia houses we purchased (2016) had balances of about 70k and 60k. We had enough equity in these houses that we could take a substantial amount out in the refinance, but Mr. ODA chose $50k each.

Here’s a run through of the thought process on how to do this and why it’s a benefit. I personally like seeing the details behind other’s decisions, so hopefully this will help someone or help make the concept click and open up an opportunity. This process was only just initiated, so I’ll do an update after we execute the plan to see how it changed.

The original goal was to use that money to pay off another loan. We’ve made our decision on which loan to pay off based on the highest interest rate. Right now, our highest interest rate is a loan with our partner at 5.1%, but this is also the loan that we’re actively paying off (leaving a balance right now of 26k, which we’re responsible for half). Since we need to time our principal payments to be matched with our partner, we can’t just dump money into this loan without really complicating things. So our second-highest interest rate is 4.625%. This loan originally was $89k in 2017 and has a balance of $62k. If we paid this off, that would leave about $35k in cash (based on the other two loan refinances that we’d take $50k out of each) that we could use to pay towards another loan or earmark for another purchase. As this discussion happened, Mr. ODA pivoted.

This company is only available to refinance loans in Virginia. Instead of paying off that $62k loan for a Virginia property, what if we also refinanced that loan and paid off one of two loans remaining on our Kentucky houses? I’m a visual person and needed to see how this would actually play out.

The terms were that if we picked a 15 year loan, that brings the interest rate down to 2.5%. With a 30 year loan, it’s 3.125%. I compared the current amortization schedule to the proposed amortization schedule, and here they are. Note that the interest isn’t a one-to-one comparison because we’ve already paid 4-5 years of interest on these loans.

HOUSE 2

The original loan terms were a 20 year at 3.875%.

The new terms would create a new 15 year loan, reduce the rate to 2.5%, and increase the loan to about $123k (pay off old loan, fees for closing, and $50k cashed out). This decreases our monthly cash flow, on this property, by $294.38.

HOUSE 3

The original loan terms were a 15 year at 3.25%.

The new terms would create a new 15 year loan, reduce the rate to 2.5%, and increase the loan to about $113k (pay off old loan, fees for closing, and $50k cashed out). This decreases our monthly cash flow, on this property, by $155.89.

HOUSE 8

The original loan terms were a 30 year at 4.625%.

The new terms would create a new 30 year loan, reduce the rate to 3.125%, and increase the loan to about $ (pay off old loan, fees for closing, and $35k cashed out). This is slightly off because the new loan isn’t showing at exactly $100k, but for all these the final numbers will be slightly different. This decreases our monthly cash flow, on this property, by $84.87.

In these projections, we’ll receive $135,000 cash in hand. With that, we’ll pay off the higher loan in Kentucky, which has a balance of about $81k. That mortgage has a monthly payment of $615.34. These three loans have increased their monthly mortgage payments by $535.14 in total. Since we’ve eliminated a monthly mortgage with the cash from these new loans, our total monthly cash flow actually has a net increase of $80.20. In addition to this net positive cash flow, we also have over $53k in cash in our account.

Now, if you know us, cash in our account isn’t a preference by any means. In my last monthly update, you can see that we have almost 20k in cash and that’s abnormal. Add $53 to that, and that’s just too much money sitting in a checking account. At this point, the goal is to buy another house. With the way the market is, we’re probably not going to hit the 1% Rule we strive for (the expected monthly rent will be at least 1% of the purchase price – $1000 rent for $100,000 purchase), and we’re not going to see the margins that we’re used to. It’s going to take a lot of effort to get our psychology right for this next purchase. We’ll have to hold strong in knowing that our other houses have great margins, and at least it won’t be negative cash flow.

At this point, we’ve started the refinance process by signing our initial disclosures and providing all the many, many documents needed to originate a loan.

The common goal in the FI/RE (Financial Independence, Retire Early) community is to reach a point where your net worth is 25x your annual spending, meaning your expenses are 4% of your net worth. This is an extreme oversimplification of things because of the number of variables associated with where your net worth might be, and how to access it. For example, retirement accounts have requirements to be met before drawing funds; while you may have hit the 4% expense to net worth ratio, it may not mean that you have that money liquid to cover your spending.

When the ODAs started down the path of FI/RE, we did it with a real estate rental portfolio. This path of net worth growth really doesn’t fit the traditional mold. It provides regular cash flow, rather than an account with a balance that’s drawn down.

As mentioned in previous posts, there are numerous ways to make money in real estate. The path we have taken is probably one of the simplest and most repeatable for anyone. We own a portfolio of single family rental houses, most of which were bought straight from the MLS. These basic properties are in basic neighborhoods with regular tenants. Nothing special. We acquired these properties by focusing on the 1% rule in real estate – try to secure 1% of the property’s purchase price in monthly rent. Another oversimplification of how things really go, but if we were able to find a $100k property that rents for $1,000 a month, we know we’re going to make money long term.

For these properties, we typically put 20%-25% down and finance the rest through a conventional mortgage. We find a tenant, and then the 4 ways to make money in real estate go to work for us: appreciation, tenant mortgage pay-down, tax advantages, and most importantly for our situation and FI/RE – cash flow.

I want to talk about how we can reach a FI/RE number through real estate cash flow differently and more quickly than using traditional stock market investing.

The $100k house had a 20% down payment and mortgage rate at 5% interest, which brings the monthly principal and interest payment to $429. Add another $121 for taxes and insurance (using round numbers here!), $100 for maintenance and capital expenditures savings, and $100 for a property manager; this comes to $750 worth of monthly expenses. At $1,000 per month of income, you have $250 per month of cash flow in your pocket. $250 per month equates to $3,000 per year of cash flow. With the $20,000 down payment and about $5K in closing costs, it means that our $25k investment nets us $3k per year in cash flow.

Circling back to the 4% rule for stock market investments, $3k in cash flow requires a savings of $75k. But we only had to invest $25k! We’re banking on the monthly cash flow, rather than a “stagnant” savings.

We took that math and ran with it. Our rental portfolio has 12 houses in it. While we’ve shown in prior posts that each house’s numbers aren’t as clean and simple as this example (some better, some worse), if we take that $3k annually and multiply by the 12 properties, we have $36k in annual cashflow for only $300k invested.

What would you rather need to produce $36k income – $300k or $900k?

Can you scale a rental portfolio to reach enough annual cashflow such that you can live off the cash flow?

Rental property investing is not completely passive. We have tenants to manage, properties to maintain, property managers to manage, income and expenses to track for taxes, lending efficiencies to explore, and the list goes on. But if you’re willing to put in a little work to reach financial independence (the FI part), you can do it substantially faster by finding strong properties to provide significant cash flow than if you were to take the totally passive route of simple stock market (index fund) investing.

Note, there’s nothing wrong with that – we have a substantial position in the stock market due to the tax free growth benefits of retirement accounts. The power of real estate investing saw our net worth grow faster than we’d have ever dreamed since we bought our first rental in 2016. The proof is in the pudding and we advocate to anyone to just get started!

Spring is a time for lease renewals or preparing to re-rent a house.

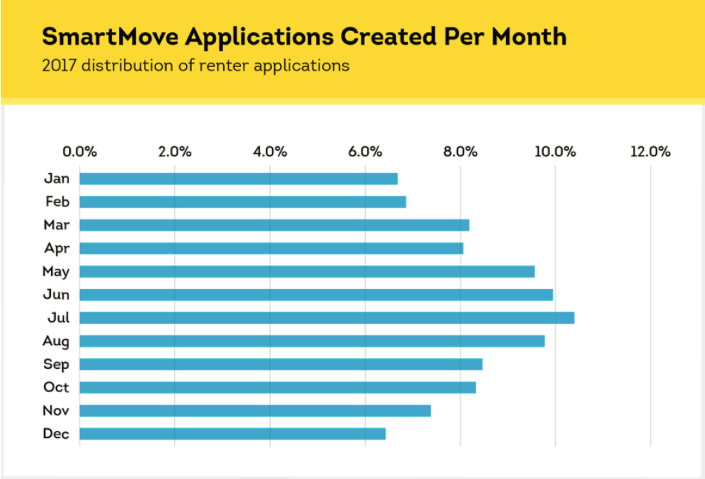

Spring and Summer are times when people are most active in the real estate market. It’s the best time to be listing your house for sale and for rent, which may yield you a better sale/rent amount because of greater competition. This timeframe is likely most active because of the better weather for moving and the school year – if a family is looking to move, they’re more likely to do it when they don’t have to transfer their kids to a different school district mid-school-year. Personally, when I was in college, nearly all the rentals were available in May or June. I remember being frustrated that I couldn’t get an August lease and had to pay for the summer months even though I’d be back living at my parents’ house. Now that I’m older and have more experience, it all makes sense. Below, you can see the increase in applications processed by SmartMove (the way we process tenant applications) that occur during the summer months, which indicates the most active time in the market.

We have seen this reflected in our days-on-the-market and rent prices. When we can list a house in the Spring months, we’re able to get it rented with very few days vacant. Houses that we’ve closed on at the end of the Summer (when school starts) and in the Fall have taken us more time to find a tenant, and we’ve had to reduce our asking monthly rent amount.

For those houses that we had purchased in a less-opportune time of year, we’ve worked to get them back to a Spring-time market for renewal.

We purchased two in September 2019 that we weren’t able to get rented until November 1st that year; we offered those tenants an 18 month lease so that their lease expiration would become May 31st.

We did similar with a house that we purchased in August. After that first year, a prospective tenant tried negotiating the list price for rent, and we said we were willing to reduce the rent a bit for an 18 month lease; they agreed, and we got our rental on a Spring renewal.

We recently had a tenant break their lease (with our concurrence), so that house has a lease expiration of October 31st now. We intend to offer a 6 month lease term to that tenant when the time comes.

With that said, we have lots of activity at this time of year.

We have 9 houses in Virginia and 3 in Kentucky. These markets are so different for us. We do our best to work with our tenants to encourage them to continue renting with us. I wrote about this in detail in my Tenant Satisfaction post.

Here’s a break down of how we handled all the leases that are expiring at this time of year.

In Kentucky, one lease was set to expire at the end of April and another at the end of May. These two properties are under a property manager. She attempted to increase the rent for a new lease term, but the tenants pushed back. Landlords don’t have a lot of leverage in a pandemic. Since the property manager is the one who handled the communication, I don’ t know what the details were. We believe both these houses are rented for less than market value, so that’s unfortunate. But, we’re grateful that both tenants renewed their lease for a year, so we don’t have to work to turnover the houses. Within reason, we’d always rather rent for a few bucks under market value than to handle turnover and lost rent (vacancy) by trying to maximize monthly cash flow.

In Virginia, we have an array of situations. Richmond was quick to acknowledge the property value increases that have occurred over the last year or so. This means that they increased our assessments, which effectively increases our property taxes.

We have the first two properties that we bought in that market, which are next door to each other and both have long term tenants (one since we before we purchased it, and the other is the second tenant who moved in a year after we purchased). We inherited their rent at $1,050, and then we increased it to $1,100 two years ago. With the property assessment increases, it was time to raise their rent again for this July. I initiated a letter to each of them stating the rent will increase as of July 1, which gave two options: they could leave the property by June 30th in accordance with their lease, or they could sign on for another year at the increased rent rate. Both chose to stay in the property, and they signed another year at $1,150. This is still below market value for the houses, but we’re happy with the lack of maintenance needs in these houses over the last 5 years. We’re in the middle of replacing the flooring in one of the houses. That house has a family of 5 and a dog living in it, so it’s not surprising that it’s worn out faster than the identical one next door with one person in it.

We have a 2 bed, 1 bath house that rents at $795. She’s been in the house since July 2018, which means that her lease ends June 30th of this year. Based on the 1% Rule (i.e., we’re looking for the monthly rent to be 1% of the original purchase price) for this house, our rent goal is $635. Since we’ve exceeded that goal for the life of our ownership, and the house hasn’t cost us much in maintenance, we chose to not increase her rent if she wanted to renew for another year, which she did. She has also spent some of her own money to spruce up the house and make it her home, and we recognize the value to us that her efforts also bring.

Another house reached out to us and asked if we were willing to renew her lease for another year. She’s been there since we purchased the house in 2017, and we’ve never increased her rent. She usually pays rent early and doesn’t ask for anything. The 1% Rule puts us at $660, and we’ve been collecting $850. Since we’ve been lenient on rent increases, I thought it a good idea to re-evaluate her terms. I plugged all the numbers into Mr. ODA’s calculation sheet to see how we were doing since the taxes increased so much on this house. Our cash-on-cash return (which we aim to be at 8-10%) came back at 19.8%. A rent increase for the sake of increasing rent isn’t worth it for such a good tenant, so we agreed to renew her lease for another year at the same rent. She wrote back: “omg thanks so much for the good news!” Happy tenants = good tenants, remember?

As for the others that I haven’t mentioned:

Two of our houses were put under a two year lease last year, so they didn’t require any action from us this year.

We have another house in KY that has a lease ending 7/31 and is under a property manager. We’ll offer a renewal option for them (i.e., we’re not interested in asking them to leave), but we haven’t worked out those details yet. Since we’re very hands off for our KY houses, we don’t know the satisfaction level of those tenants to gauge. Historically, we’ve had trouble renting this unit, costing us long vacancy times, so if we can renew their lease for even the same rent, we’re happy. Plus, having a 7/31 end date starts pushing us closer to the Fall for any future year-long rental agreements.

One of the houses that we have with a partner has a difficult tenant. I mention the tenants almost every month in the financial updates because they don’t pay their rent on time, and getting information out of them is like pulling teeth. They’ve rented there long before we owned the property, and their rent has always been $1,300, which is well below market value. We plan on offering them a drastic rent increase and a new lease term (we’re still managing under the previous owner’s lease agreement) in July for their September 30th expiration term.

While we don’t have any houses to turn over, we’re going to get into each house this summer. Since so many of our houses don’t typically have turnover, we don’t get into them as often as we should to make sure things are running correctly (i.e., don’t want small issues to go unnoticed and cost us in the long run). Specifically, we need to make sure that the HVAC filters have all been changed and verify there aren’t any red flags. I plan to give the tenants at least a month’s notice before we enter, so that if there are any maintenance activities they should have been performing, they have time to get it situated. I’ll walk through with our typical move in/out inspection form and note any concerns or areas of interest. I also understand that by being visible, I’m opening myself up to being asked for things that a tenant may not necessarily ask for via email or text, but I’ll cross that bridge when I come to it. For now, we’re just grateful that we have no houses to turn over and no expected loss of rental income for the year thus far!

I shared that I would tell the stories of our home purchases. Instead of starting with #1, I decided to start with the most interesting. This property was being sold by a licensed Realtor, so we had a false sense of security. It ended up being the sketchiest (technical term) deal we’ve done. This is in Virginia.

We started with a home inspection, which revealed several issues. We requested the HVAC condensate line be cleared and the water in the backup pan removed. We also agreed to have our attorney withhold $1,300 at closing, to be paid to a contractor of our choice after closing, to repair other items found during the inspection. I can’t remember why we were handling the home inspection items, but that should have been the first red flag.

Our closing was scheduled for 8/18.

We were told that the HVAC repairs agreed upon were completed. We went to check on the progress of cleaning out the house and the HVAC repairs on August 10th. The HVAC’s backup pan still had water in it, and the house was filthy (after being told it was ‘vacant’ and ‘cleaned’). Plus, the electric was turned off. We had our Realtor reach out to the seller to cover our bases. Here’s his email:

While waiting for a response on this email, we checked with our closing attorney to ensure everything else was ready for closing; it wasn’t. We fully expected a “we’re clear” response, but instead we were told they were having trouble clearing the title. We weren’t given the specifics, but that’s not what you want to hear a week before closing. It ended up being cleared, but that was one more thing to worry about!

As typical, we had to do a final walk-through of the house to ensure it’s in the same condition (or better) as it was when we went under contract. Knowing how poorly the seller communicated over the previous month, we wanted to see the house the day before closing, rather than right before we head to the closing table. The electric was still not turned on, and it wasn’t cleaned. Our Realtor contacted the seller again. We were assured it would be addressed, and the electric would be on. We made plans to walk through the house in the morning.

Our Realtor was unavailable that morning, since this wasn’t supposed to be part of the schedule, so he sent a team-member to let us in. As luck would have it, she dropped the lockbox key below the front porch, so we couldn’t get in. We called our attorney and postponed the closing to later in the day. The Realtor was able to obtain a copy of the key to let us in, where we learned the electric was still off.

I contacted the electric company. I explained that I was the buyer, and the seller kept saying the electric would get turned on, but here we are at the 11th hour with nothing. The woman on the other end couldn’t tell me what she was seeing since it wasn’t my account, but she carefully played with words to let me know: sorry, hunny, but there’s no way this electric is getting turned on while under this person’s name because there is a high outstanding balance. She assured me that if I put it in my name, there wouldn’t be any issues. However, I wasn’t about to pay fees and put it in my name before the house was legally mine.

This is where we learned that a good attorney is worth his weight in gold. We never really understood the role of a closing attorney, since all our closings had gone smoothly (I mean, we could sign all the closing documents in about 20 minutes at this point). Since the electric wasn’t on, and we couldn’t verify the condition of the home, as required by the contract, our attorney withheld $5,000 of the settlement proceeds. The seller’s attorney was NOT happy, but it was entertaining to watch from our standpoint.

We had been provided a ‘receipt,’ dated 8/17 (the day before closing), that indicated an HVAC repair man had been out to do the work required. We are pretty sure that this was falsified. There was no electricity in the house that day, and there was still water in the pan on 8/18. Here’s the email I sent to our attorney releasing the $5,000 withheld, less the cost of my HVAC technician performing the repairs.

It cost me $125 for the HVAC technician’s trip. Our attorney told the seller’s attorney that he would release the $5000 less the $125. The seller’s attorney said he didn’t have any authority to allow that; so our attorney said he didn’t have any authority to release the $5000. Well, the seller’s attorney decided $4875 was better than nothing, and I got my $125 back.

All in all, everything fell into place, but there were many days and hours that felt like we were about to fall into a pit.

We purchased the house for $89,000, plus the $1,300 for contractor repairs, and the seller paid $2,000 of our closing costs (this minimizes the amount we have to bring to closing and allows us to leverage every last dollar we can for maximum efficiency). Our first lease was for $995/month, exceeding the 1% Rule. We closing in mid-August, and the first lease didn’t execute until October 1, which was one of our longer vacancies. That tenant renewed her lease once. Currently, the rent is $1,025/month. We sought $1,050 for a 12 month lease, and the prospective tenant negotiated an 18-month lease at $1,025. We accepted this because it was rented in October, and an 18-month lease brought as back to spring-time turnover. Even though taxes have risen since the purchase, we still maintain the substantial cash-on-cash return that is provided for in trying to obtain the 1% rule on investment real estate purchases.

After closing, I painted nearly the entire house (including the trim) over the course of a week; the house looked significantly better with just a fresh coat of paint. We also had to do a more thorough cleaning job than we’ve typically had to do on houses we purchase, including caulking the tub and cleaning the carpet.

We replaced the dishwasher with the first tenant, and then replaced the refrigerator after the second tenant kept complaining about the seal not working well. Most costly, the house has had several roof and siding issues. The kitchen was an addition with a flat roof, which typically causes problems. We replaced the gutters, fixed the flashing, repaired some siding, and then eventually replaced that part of the roof altogether. We also had to replace a cracked window, which was surprisingly under warranty. It took a lot of work to find the window manufacturer and a local distributor, but it surprisingly all worked out because it was a stress fracture and covered under a lifetime warranty.