We had two tenants move out at the end of July. We also had back to back trips scheduled for the end of July and beginning of August, with the kids starting school on the 13th. We also had the cruise planned for the end of September into October, so that was a decent push to get the rentals rented before we left. We put countless hours into those two houses and it definitely took its toll.

RENTALS

As of October 1st all our rentals are rented! That’s a good feeling after two months of vacancy. This is the month of taxes. We have several houses that are paid off, which means they aren’t escrowed, and I’m responsible for paying the taxes and insurance on them. The 4 houses we have in KY are owed this month, and it’s about $7k worth. We’ll owe 2 houses in VA that come to about $3k next month.

I have a couple of houses that are struggling to pay rent on time. Usually it happens for a couple of months and they get back on track, but that’s not happening quickly. I’m trying to remain optimistic, but there isn’t a track record of it getting easier if they have taken this long needing to catch up.

We closed on a new property near our house. It’s a townhouse that we hope to get rented later this month. We’ll see what it looks like once it’s empty, but it didn’t appear we’ll need to do anything to it to get it rented (which is how we buy our rentals). There will be separate posts going into the details of each rental turnover and the purchase of House15 using a commercial loan.

PERSONAL

This is the last month for the 0% interest credit card. When we have a major purchase on the horizon (it was house-wide carpet this time last year), we open a 0% interest credit card. We started this concept about 8 years ago. We look for a credit card that has 0% interest for at least 12 months and that gives us a bonus of some sort. We make more than the minimum payment each month and then pay it off before the deadline. A default payment can cause you to lose your 0%, so it’s important you’re making your payments. But we don’t pay a lot towards it because the money is doing more for us in our savings account (or the investments) than it would by paying down a 0% interest balance. This time around was a bit different. The carpet only cost us $10k, but the balance is over $14k. This credit card had the same incentive as our typically used card (2% cash back), so Mr. ODA used it a majority of the time. For a while, my goal was just to pay what gets our balance lower than the original balance from the carpet. But then we had some big rental purchases that we put on the card, and it just wasn’t worth paying $5k+ to the card. We will make a transfer from our big savings account to make that payment at the end of the month.

Mr. ODA’s last pay check arrived on October 11. He took the “deferred resignation program” as of April 30. The sunset date was September 30, so that covered the payout that we just received, including his balance of annual leave.

Outside of rentals, our spending has been minimal. With the cruise, we didn’t spend much since that was a week of almost everything paid for in advance. The dog had his annual check up, so he was the bulk of our costs. We have our routine costs we see, but happy to see lower balances after all the rental work costs.

SUMMARY

I don’t even want to admit what is about to leave our account this month. I guess the positive is that it’s under $100k..? We have to pay the taxes on the houses that aren’t escrowed, pay off that credit card, and buy a house. At least the house purchase goes right towards equity. Since I didn’t get all the account numbers yesterday morning like I planned, here’s an update that captures our new purchase.

You hear this term in real estate often. “What are the comps?” “Have you run the comps?” It’s short-hand for “comparables.” These are the houses that are similar to the house in question (whether you’re trying to list a house for sale or purchase a new house) can be used to determine the value of a property. It’s touted as if it’s difficult, and I’ve seen several comments in a “moms” group that told me more people need to know about appraisals.

An appraisal is an expert’s estimate in the value of something. It can be something small like a piece of jewelry or something big like a house. During a closing process that includes financing, the bank issuing the loan is going to request an appraiser evaluate the property being purchased. The bank is using this as a mechanism to verify that the property is worth the contract amount.

A recent appraisal we had done stated the following (for context). This report is based on a physical analysis of the site and improvements, a locational analysis of the neighborhood and city, and an economic analysis of the market for properties such as the subject. The appraisal was developed and the report was prepared in accordance with the Uniform Standards of Professional Appraisal Practice.

If your real estate purchase is through a loan, the bank is going to require an appraisal. Have you ever looked at the appraisal? The lender is required to give you a copy.

Let’s dig into one of mine.

THE APPRAISAL

This particular appraisal was completed for a refinance of a loan. It was done in December 2021 and is 37 pages long, granted a lot of that is teaching documentation.

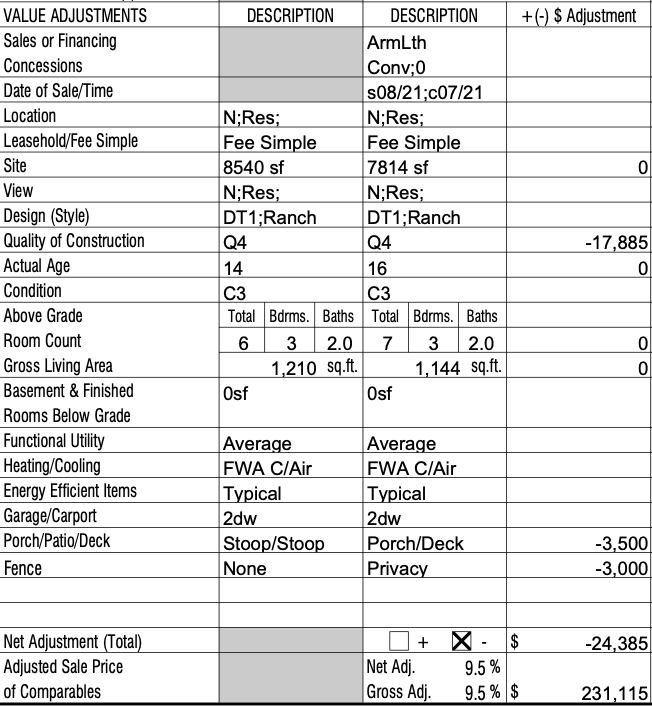

First, the appraiser identifies the property’s characteristics. Things like the address, plat number, taxes, house size and details, utility hookups, and neighborhood demographics are filled out. Here are a few snapshots with that information. All appraisal reports I’ve seen have looked like this (across multiple states).

Once the appraiser identifies the property’s details, he moves on to finding nearby homes that have sold recently. The comparable sales are of similar age, construction quality, and condition. There are formulas available to the appraiser to determine how differences between the property he’s appraising compares to the similar nearby homes. For instance, having another bedroom increases a property’s value by a certain amount, having a garage could increase the property value, having a fence affects the value, etc. Here’s a snapshot of one of the comparable sales for this appraisal. The first ‘description’ column contain the details of the house being appraised. The second ‘description’ column contains the details of the address he’s using as a comparable. Then there’s the adjustment column to identify how those differences affect the value of the home. This home being used had sold for $255,500. Each difference is calculated to account for a value of the home had it been even more similar to our house. So this house having a porch instead of a stoop is affecting the value at $3,500 (I don’t know how these values are determined, but I assume it’s all a software calculation that keeps it consistent).

This appraiser used 7 comparable sales. We’ve historically seen 3-5 houses used, but this market has created more options than usual. The appraisal was determined by removing the value of the land (since that’s calculated by the tax records regardless) and applying the average price per square foot amount to our house. The valuation came in at $230,000. We purchased the house for $117k 5 years ago, so that was a nice surprise. We were able to take out a loan for up to 60% of the appraisal’s value.

YOU CAN DO A RUDIMENTARY APPRAISAL YOURSELF

The point here is that an appraiser is using the specifications of nearby, similar real estate transactions to determine the value of the house in question. Since the concept of an appraisal is straightforward, you shouldn’t feel like you’re incapable of doing your due diligence on a purchase or determining the sale price.

It’s important to note that you’re focusing on houses that have SOLD. You’ll see houses nearby listed for sale at different prices, but that doesn’t mean that’s what the market deems a “fair market value.” You want to focus on the sold prices because that means someone was willing to pay that for that type of property, and a bank likely confirmed the value with an appraisal.

In this “moms” group I mentioned, several people told a person that she needed to hire an appraiser before listing her house. An appraiser is about $400-600. In a house sale, the buyer is responsible for the appraisal. Therefore, as the person listing the property, you’re not “ahead” in any way by paying for an appraisal up front because it wouldn’t have been your cost to bear anyway. Instead of paying someone to perform an appraisal, you look at houses nearby that sold recently.

Back in 2018, we were using sales for 6 months to a year prior to the date we were searching. The housing market hadn’t changed all that much year-to-year that you couldn’t use sales from a year ago. These days, you need to be looking at houses that have sold in the last 3 months, and maybe go back to 6 months if you don’t have any good options. If you need to use sales from a year ago these days, then assume a hefty inflation (in most areas) from the price it sold at, but it’ll at least give you a good starting point on the price.

For recent sales you dint, you’re looking for properties with the same number of bedrooms and bathrooms, approximately the same square footage, and approximately the same size yard. You’re hoping for pictures too so that you can evaluate if the condition of the property is objectively better or worse than the property you’re considering.

PERSONAL EVALUATION EXAMPLE

We’re currently on the hunt for another rental property to add to our portfolio. Things are moving fast, so we’re doing quick evaluations on the fly with best guesses of value. We have the benefit of doing several of our own real estate transactions, including plenty of searching for options outside of the ones we did purchase. Therefore, we have the knowledge to be able to eyeball the value. In the beginning, it would probably work best if you write down the details (similar to what’s found in the appraisal screenshots above) to identify the appreciable differences between your options.

We were looking at a property that was in poor condition. The listing even stated that they were offering a $3,000 flooring allowance as part of the sale, acknowledging that the condition was poor. The house is 3 bed/1 bath (colloquially referred to as ‘a 3/1,’ and was listed at 169,900. The listing photos showed a scratched up floor, but otherwise looked ok.

Not bad, right? Well, I don’t know what filter they used, but these colors are a lot more vibrant than the condition of those cabinets and appliances were in person. The photos didn’t capture the gouged walls or layers of paint that weren’t properly painted between coats. And, unlike popular HGTV shows would you have you believe, the paint color isn’t something we’re caring about. It’s a bonus if it doesn’t need a coat of paint before we rent it, but we’re generally expecting to paint a house after we buy it. The photos also don’t portray the filthy bathroom with the mismatched patchwork tiles in the shower. We stepped back and seriously considered flipping this or improving it and using it as a rental still.

I opened my Zillow app. When I’m looking for quick information, I’m focusing on price per square foot, rather than actual purchase price. This house came to $151/sqft. In the Zillow app, on the upper right corner, click ‘Filters.’ I always click ‘Reset’ before I start a new search because I never know what I last changed in the parameters. I chose the ‘Recently Sold’ toggle, left everything the same, and then at the bottom I changed ‘Sold in Last’ to ‘6 months.’ In this area, if I looked at a broader spectrum of recently sold houses, I’d have too many to look at, and the prices in 2019 would be drastically different than what’s currently happening in this market. If I still had too many results, I would have filtered down to 90 days. However, it’s January when I’m looking, so there hasn’t been too much activity in the last 3 months, and I want to capture more options that sold during the summer months.

Then I just started clicking the yellow bubbles of prices. I want to first focus on the ones closest to the house I’m looking to buy. As I get further away (or cross major roads), I’m probably looking at a different school district, or different crime levels, or different ‘feel’ of the neighborhood; be careful how far out you look.

Here are my thoughts on the first comp I found. The parentheses identify how it relates to the property I’m viewing: either it’s the same (=), my property is better (+), or my property is worse (-). It’s a 2 bed (+), 2 bath (+), with low curb appeal (+), smaller lot (+), nicer floors (-), covered deck (-), stainless appliances (-), kitchen cabinets were original and the stove’s vent hood was outdated (+), the master bathroom needs a facelift (+). This house sold in September 2021, so it’s a fairly similar market to what I’m looking in now. It sold for $117/sf. With the difference in the number of bathrooms and bedrooms, it’s hard to compare. Subjectively, the house I’m interested in is worse than this house, but it has another bedroom and a bigger lot. I decide that this comp doesn’t get me close to $151/sf for the house I’m looking at.

Comp 2 is around the block. It’s very close to the size of the house we’re evaluating (=) and is a 3/1 (=). It’s adorable, with great curb appeal, so it draws me in. Then I start noticing some things that are red flags. The roof doesn’t appear to be in bad shape, but my eyes are drawn to a water stain on the living room ceiling (+). It appears to have laminate flooring in the kitchen and carpet elsewhere, whereas the house we’re looking at has hardwood everywhere; our hardwood is beaten though, so this is hard to compare. I see that there’s old vinyl in the laundry closet that wasn’t addressed when new laminate appears to be laid, there’s some poorly laid wood flooring in just the entrance to the master bedroom, and there are several stains in the carpeted bedrooms. The backyard has power lines running through it (+); I see several issues with the vinyl siding on the house (+), but it has a covered deck (-). They had tried to sell this house from July to October, which tells me that plenty of people were drawn in, but those defects were clear (and probably more) in person. They started their listing at $166/sf and ended up selling at $146/sf. While this house looks to be in better condition than the one I’m evaluating, this tells me that I’m probably looking at the $140s/sf for the one I’m looking at.

There’s a 3rd ‘comp’ that caught my attention right behind the house I’m evaluating. Zillow claimed it was sold for $334/sf. Interesting anomaly. Our Realtor was able to pull the MLS and see it actually sold at $150k, so about $115/sf. So moving on.

I found a brick ranch around the block, so I’m excited that it’s very similar to the house I’m looking at. It’s a 3/1 (=). It sold in September 2021 for $149/sf after having first been listed at $163/sf in July. I dive into the pictures. The floor isn’t destroyed (-)! There are mismatched, yet updated, appliances in the kitchen. It’s frustrating, but they probably have a better lifespan that what’s in the house I’m looking at (-). The bathroom has been updated recently, but it’s small, and there’s no picture of the shower side of the bathroom (concern, but still better than the house I’m viewing) (-). There are minimal pictures, but at least one of every room. After comp 2 went for $146/sf, and this is better condition at $149/sf, I’m now putting the house I’m evaluating below $145/sf.

There’s a brick 3/1 next to Comp 4 that sold for $162/sf. But there are no pictures and it was for-sale-by-owner, which tells me someone probably overpaid for a higher list price because they were desperate. I’m throwing this out and not using it as a true comp.

At this point, I’m just standing there trying to evaluate whether this is worth pursuing or not. I can do detailed looks at comps later on a computer with a pad and pen. I decide that $145/sf is my highest value of this house and it’s horrible condition. However, even with that, I don’t want to go that high because of all the work that needs to be done right away on the house. The comps told me that’s the value of other homes that needed some work, but looked livable from day 1. I decided to sit on it. Well, the next day, it went under contract at a reduced price of $146/sf. I won’t know the actual price of the contract until it closes, but for now, it looks like someone bit on the $146/sf.

Now this is really important if you’re evaluating for a purchase. Do not overpay for a house. Do not feel pressured into needing it now. We’ve put in several offers on houses, but we’re not going to get into a bidding war. We also put in an offer on one house, and the seller said “raise it $5k and state the offer isn’t contingent on an appraisal, and you have a deal.” No. Requesting the appraisal clause to not be checked says we were probably overpaying even at the offer we made. So thank you to this man for letting me know that it was time to walk away.

SUMMARY

You can typically rely on your Realtor to provide you comps through the MLS. If you have questions about their valuation, ask for the details. I have an instance where I didn’t agree with my Realtor on a list price of our last personal residence. In this particular instance, I had better knowledge of the housing market where our house was than he did, because he focused on sales within the nearby city limits, and we were in the suburbs. He ran comps based on basic metrics (number of bedrooms, square footage). I had the benefit of knowing details behind some of the sales he was using or how some houses weren’t a good fit to use as a comp to the house we were selling. I was able to sway the list price to even higher than he suggested, and we were under contract that weekend.

I know how it works. I’ve taken the time to research and understand the process just enough that I can protect my finances and interests in these transactions. I’m not sharing this as an example to fight your Realtor on their suggested list price, but as a way to show you need to be an informed consumer.

I shared that I would tell the stories of our home purchases. Instead of starting with #1, I decided to start with the most interesting. This property was being sold by a licensed Realtor, so we had a false sense of security. It ended up being the sketchiest (technical term) deal we’ve done. This is in Virginia.

We started with a home inspection, which revealed several issues. We requested the HVAC condensate line be cleared and the water in the backup pan removed. We also agreed to have our attorney withhold $1,300 at closing, to be paid to a contractor of our choice after closing, to repair other items found during the inspection. I can’t remember why we were handling the home inspection items, but that should have been the first red flag.

Our closing was scheduled for 8/18.

We were told that the HVAC repairs agreed upon were completed. We went to check on the progress of cleaning out the house and the HVAC repairs on August 10th. The HVAC’s backup pan still had water in it, and the house was filthy (after being told it was ‘vacant’ and ‘cleaned’). Plus, the electric was turned off. We had our Realtor reach out to the seller to cover our bases. Here’s his email:

While waiting for a response on this email, we checked with our closing attorney to ensure everything else was ready for closing; it wasn’t. We fully expected a “we’re clear” response, but instead we were told they were having trouble clearing the title. We weren’t given the specifics, but that’s not what you want to hear a week before closing. It ended up being cleared, but that was one more thing to worry about!

As typical, we had to do a final walk-through of the house to ensure it’s in the same condition (or better) as it was when we went under contract. Knowing how poorly the seller communicated over the previous month, we wanted to see the house the day before closing, rather than right before we head to the closing table. The electric was still not turned on, and it wasn’t cleaned. Our Realtor contacted the seller again. We were assured it would be addressed, and the electric would be on. We made plans to walk through the house in the morning.

Our Realtor was unavailable that morning, since this wasn’t supposed to be part of the schedule, so he sent a team-member to let us in. As luck would have it, she dropped the lockbox key below the front porch, so we couldn’t get in. We called our attorney and postponed the closing to later in the day. The Realtor was able to obtain a copy of the key to let us in, where we learned the electric was still off.

I contacted the electric company. I explained that I was the buyer, and the seller kept saying the electric would get turned on, but here we are at the 11th hour with nothing. The woman on the other end couldn’t tell me what she was seeing since it wasn’t my account, but she carefully played with words to let me know: sorry, hunny, but there’s no way this electric is getting turned on while under this person’s name because there is a high outstanding balance. She assured me that if I put it in my name, there wouldn’t be any issues. However, I wasn’t about to pay fees and put it in my name before the house was legally mine.

This is where we learned that a good attorney is worth his weight in gold. We never really understood the role of a closing attorney, since all our closings had gone smoothly (I mean, we could sign all the closing documents in about 20 minutes at this point). Since the electric wasn’t on, and we couldn’t verify the condition of the home, as required by the contract, our attorney withheld $5,000 of the settlement proceeds. The seller’s attorney was NOT happy, but it was entertaining to watch from our standpoint.

We had been provided a ‘receipt,’ dated 8/17 (the day before closing), that indicated an HVAC repair man had been out to do the work required. We are pretty sure that this was falsified. There was no electricity in the house that day, and there was still water in the pan on 8/18. Here’s the email I sent to our attorney releasing the $5,000 withheld, less the cost of my HVAC technician performing the repairs.

It cost me $125 for the HVAC technician’s trip. Our attorney told the seller’s attorney that he would release the $5000 less the $125. The seller’s attorney said he didn’t have any authority to allow that; so our attorney said he didn’t have any authority to release the $5000. Well, the seller’s attorney decided $4875 was better than nothing, and I got my $125 back.

All in all, everything fell into place, but there were many days and hours that felt like we were about to fall into a pit.

We purchased the house for $89,000, plus the $1,300 for contractor repairs, and the seller paid $2,000 of our closing costs (this minimizes the amount we have to bring to closing and allows us to leverage every last dollar we can for maximum efficiency). Our first lease was for $995/month, exceeding the 1% Rule. We closing in mid-August, and the first lease didn’t execute until October 1, which was one of our longer vacancies. That tenant renewed her lease once. Currently, the rent is $1,025/month. We sought $1,050 for a 12 month lease, and the prospective tenant negotiated an 18-month lease at $1,025. We accepted this because it was rented in October, and an 18-month lease brought as back to spring-time turnover. Even though taxes have risen since the purchase, we still maintain the substantial cash-on-cash return that is provided for in trying to obtain the 1% rule on investment real estate purchases.

After closing, I painted nearly the entire house (including the trim) over the course of a week; the house looked significantly better with just a fresh coat of paint. We also had to do a more thorough cleaning job than we’ve typically had to do on houses we purchase, including caulking the tub and cleaning the carpet.

We replaced the dishwasher with the first tenant, and then replaced the refrigerator after the second tenant kept complaining about the seal not working well. Most costly, the house has had several roof and siding issues. The kitchen was an addition with a flat roof, which typically causes problems. We replaced the gutters, fixed the flashing, repaired some siding, and then eventually replaced that part of the roof altogether. We also had to replace a cracked window, which was surprisingly under warranty. It took a lot of work to find the window manufacturer and a local distributor, but it surprisingly all worked out because it was a stress fracture and covered under a lifetime warranty.