The day that’s in the contract as the closing date.

I truly can’t believe how many people have asked some form of this question in my life recently. While I’ve had multiple in person conversations on this topic, this post really stemmed from a Facebook post. “Is it an expectation for people to be moved out of their home the day of closing when buying a home? We sold our house, and are moving into a new home that we’re supposed to close the same day. Is there not a grace period?” What would that grace period be? How would the timing be determined?

On one side, I see the “closing date” section of a Kentucky contract simply states, “The closing of this transaction shall occur on the ___ day of ________________, 20__.” That’s quite useless actually (as I consistently find in KY law and legal documents). There’s a lot to be inferred by that statement, versus it being explicitly and clearly stated. On the contrary (as this has gone many times over), Virginia wins out.

In the paragraph before this image, it states where closing shall occur and by what date. This excerpt clearly indicates the purpose of “closing,” leaving little room for interpretation.

However, if we take a step back from the legal jargon and contractual obligations, whether explicit or inferred, we can see the logic. If you’re the buyer, once you sign the paperwork to purchase the house, wouldn’t you expect the keys to be handed over to you right then so you can start moving in and living in this house you just paid for? Wouldn’t you want the sellers out of the house because they’re no longer financially responsible for the house, and you don’t want any liabilities of their damage (intentional or accidental) to fall on your hands? You’ve done a final walk through and signed off that the house was in the condition you expected it to be in at that point in time.

Now this isn’t to say that there aren’t other terms and conditions that can be agreed to between both parties. “Lease back” or “rent back” clauses are commonly used. Sometimes it’s beneficial for a buyer to process the transaction (e.g., a rate lock expiration), but they allow the seller to remain in the home for an agreed-upon period of time (e.g., to bridge a gap before their new house is ready/available). But all of these terms are to be agreed to, in writing, before the closing date.

When we just sold our last house, we allowed the buyers to store things in the garage. We entered into a contract separate from the house purchase contract, called a “Preclosing Occupancy Agreement.” I haven’t needed one of these in Virginia, so I don’t know their standard form, but KY’s form does well here. The document outlines the date the buyer can take occupancy and whether there’s a charge for it. There were other items that outlined incidentals, such as utilities. In our case, the buyers were simply asking for garage space to put some of their belongings (because they had a same-day-closing for their sale and purchase), so we didn’t require them to put any utilities in their name before the sale.

BRIDGE LOAN

I can understand the complaint. Financially, you likely need to sell your current home to afford a new home. The “cash” from your sale is what you’ll use as your downpayment, as most people don’t have 20% of $400k sitting in a savings account (nor should you!). That makes the option to buy the house, take a day or two or seven to empty out your old house, and then sell your house not feasible.

There’s such a thing called a bridge loan. It’s a short-term loan used to purchase assets until long-term financing can be secured. There are more fees and high interest rates associated with this. However, it could be worth it to save the hassle of Private Mortgage Insurance (PMI). PMI is required in many cases where you cannot provide 20% as a downpayment for a house purchase. It protects the lender in case you don’t make your mortgage payments. PMI is removed when your principal balance falls below 80% of the original value of your home, whether that’s through regular mortgage payments or you make additional principal only payments. You can request PMI be removed earlier than that if you provide proof that your home value has caused your principal balance to now be less than 80% of the value, which is typically proven through an appraisal at your cost. If you put 0% down on a $400,000 purchase, it would take almost 12 years of payments before your loan reached 80% of the original home value. That’s 12 years that you’re paying PMI on top of your mortgage payment, and those are funds that are doing nothing productive to your net worth. A bridge loan may be worth it if you already have a sale date on your current house and only need to cover a few days or weeks.

SUMMARY

Logistically, it would be great if you could buy your new home, move all your things, and then sell your current home. Financially, this isn’t normally feasible. A lot of the time, you’re needing the equity you have tied up in your current home to purchase your next home.

Our first purchase was made up of two 401k loans (that we maxed as residential loans, which are penalty free), a gift from parents because we were short just a few thousand dollars, and cash on hand. We needed about $80k. Our second transaction, we chose a new build house. We sold our house, went into a rental for 3 months, and then used the sale money to purchase. Our third transaction was also a new build. We hopped AirBnBs until that got old with a 6 month old and 2 year old, and then crashed in Mr. ODA’s parents’ basement. We had 7 weeks between selling our house and purchasing the new one, so the cash from the sale went into our account, and we let it sit there until we needed it to close. Then this current purchase was actually done before we sold our third house, but we had executed a Home Equity Line of Credit prior to the sale. We used the HELOC to put the down payment on the current house, and then the sale of our third house paid off the mortgage and HELOC before distributing the cash balance to us. In all of these transactions, we had the ability to float the funds. That allowed us the ability to house our belongings in “long term” storage (not a day or two) for those two times we had a gap between the sale and purchase. The HELOC allowed us to slowly move our belongings to the new house this last time, and then we did a final moving day of all our big items just before closing (our current house needed work when we bought it, so we didn’t move right away).

But in all cases, unless there’s a separate document indicating so, the closing date of a transaction is the date that you give or take possession of the property. If you were buying, you wouldn’t want to take the risk of the previous owners messing with something in a property you now own. If you were selling, the buyers would have the same expectation.

*This post was started in November 2022, but our son was born 3 weeks early (and on Thanksgiving), so it fell off my radar for a long time while I caught back up. Let’s dive in now.

We sold our primary home at the beginning of November to move a half hour away and closer to family. It was a new construction home, and we purposely sold when we did to avoid capital gains taxes. If you call it your primary residence for 2 of the last 5 years, you’re exempt from capital gains. Considering the market over the last two years (2020-2022), we were slated to owe a hefty penny if we sold before that 2 year mark.

Had we sold earlier or perhaps waited for the spring, we could have made more. Instead, we opted to be rid of the home, not try to rent, and be able to have that behind us. We were extremely fortunate that we were under contract by the end of the first weekend we listed. The market had cooled significantly from the multi-bid, exorbitant pricing, with appraisal waiving language days.

We only had 2 showings. The first politely let us know they wanted a walk-out basement. We had an amazing basement with 9′ ceilings and no soffits, but it didn’t have a door due to the floodplain. We don’t really understand why, but the backyard was definitely low enough for it to have been a walk out basement. It was one of the red flags that made me uncomfortable living there, along with a long delay for construction on our lot and a few around us due to extensive sink hole surveying. The second showing made us an offer 10k below asking. We sort of split the difference at $495k, and they accepted.

There were several houses listed in that neighborhood for weeks after we closed, that were listed the same weekend as us, so I am eternally grateful that the stars aligned for what we wanted/needed.

PROCEEDS CALCULATION

We purchased the home for $346,793 in November 2020. The contracted purchase price when we sold was $495,000, which was completed in November 2022. That’s a difference of $148,207, but that’s not “take away” money.

As the seller, you’re typically responsible for paying out the Realtor commissions. They’re typically 6%. We asked our Realtor if she would drop it to 5% (buyers agent gets 3%, sellers agent gets 2%) since we had drawn up our purchase contract sight unseen and this was the 4th commission based transaction she had from us in less than 2 years. She agreed. I truly don’t like asking someone to take a lower commission, but due to there being several transactions in a short period of time, many not even needing much effort (showings, phone calls, etc.), I accepted Mr. ODA’s plea to ask. That comes to $24,750 paid in Realtor commissions.

We then have to pay off any loans that used that property as collateral. We had a mortgage and a Home Equity Line of Credit (HELOC). We had put 20% down on the purchase, so the mortgage had about $266k left as the balance. The HELOC had been used for a couple of other things than just the down payment on a new home, and it didn’t require principal payments on it while we had it, so that balance was about $86k.

We walked away from the closing table with about $117,000 after tax offsets and such.

PAST DETERMINATIONS FOR WHAT TO DO WITH THE PROCEEDS

In July 2012, we purchased our first home for $380,000. We put 20% down; it was a foreclosure, but the only work we had to do was on the main floor bathroom. When we sold that home Fairfax, VA for $442,500 in October 2015, we paid off a car loan and bought our second two rental properties in Richmond, VA. The car loan was only at 0.9% interest, so it didn’t meet Mr. ODA’s requirements to pay down loans with higher interest rates, but it did alleviate one monthly payment I had to manage. The irony of that statement, now that I manage 14 houses worth of payments all year. We also used those proceeds to put 20% down on the purchase of a new primary home outside of Richmond, which had a purchase price of $359,743. We paid off House1’s mortgage because the loan had a balloon payment that we needed to be ahead of.

When we sold that Richmond home for $399,000 in September 2020, we took about $109k away. We used those proceeds to put 20% down on the purchase of our new home, at $346,793, outside of Lexington, KY. We paid off House4, House6, and House13. Since paying towards a mortgage and not paying it off doesn’t change your monthly cash flow, we focused on where we could eliminate a mortgage payment. We’ve since paid off House11 and House12. House12 had a high interest rate, so we were interested in eliminating that as fast as possible, even though we were paying for it with a partner.

WHERE DID THE MONEY GO THIS TIME

We purchased our current primary home last summer and put work into it. Since we purchased it before selling our house, we used a HELOC to pay for the down payment. That meant that when we walked away from the closing table, the money we were putting in our bank account had no distinct purpose (like in the previous cases where we had to use some of the sale proceeds to buy another primary house).

The first thing we did was open a high yield savings account. At the time, it was necessary because our savings account wasn’t paying market rate. I remember Mr. ODA complaining that interest rates on loans were increasing, but it wasn’t being shown on savings interest side. He found a high yield savings account that gave a sign on bonus (we like that ‘free’ money!). We put $50,000 into that account, earning over 4% interest. The money in that account was removed and put into our regular savings account, which is now earning over 4%.

Since the money didn’t have a purpose, we needed to get it into the market. If we put it all in the market at once, then we’re subject to a lot more fluctuation. To hedge our volatility, we planned to schedule regular investments. It seemed crazy to me, but our financial advisor and Mr. ODA decided on $5,000 per week. That would take 20 weeks to accomplish. To my chagrin, this was set up as an auto transfer. Even with a large balance sitting in the account, it didn’t hurt any less watching $5,000 every week be taken out. This plan didn’t last long though because Mr. ODA found Treasury accounts that act as short term certificates of deposit. My next post will go into this in more detail.

Not an immediate need, and we didn’t rush to buy something for the sake of buying it, but we earmarked about $20k for the purchase of a new van. I love the van we bought in 2019 (which was a used 2017), but it had a few kinks in it. I also felt pretty good about the deal I got on it. However, I didn’t put the time into test driving and looking at this van that I really should have because one of us had to stay in the show room with the kids while the other went for a drive. I also know what I’m looking for in a used car now (that was our first used car experience), versus buying a brand new car that hadn’t been driven by others. It helped that I was looking to buy the same exact van, just newer, so I know how it’s supposed to work and what to test. We ended up finding a van about 2 hours away from us in early 2023. We’re almost a year into this van, and I absolutely love it.

In the back of our minds, we’re still looking for another rental property. There’s an area in town near us that would work for short term rentals, which I’d like to dabble in. We have seriously considered a few, but interest rates have shot it down. A 1500 square foot house, with a $200,000 mortgage, comes to a monthly payment (of just principal and interest) of about $1,400. That’s just not good margins with such high interest on it. We’ll keep an open mind, but so far it isn’t panning out.

SUMMARY

Our savings account is currently earning 4.22%. Mr. ODA is also managing that balance by using the short-term Treasury bills. Since we started with the Treasury bills, we’ve made about $500, which is on top of the interest we’ve earned to date on the savings account, which is over $1600.

We started off with paying the mortgage that had a balloon payment. It was a commercial type loan, so it was amortized over 30 years, but was really only a 5 year loan. We decided to pay it off instead of re-mortgaging it at the end of the 5 years. After we took care of the balloon payment approaching, we started paying off mortgages where we could eliminate a payment (we had multiple houses with $30-60k worth of a balance), and then moved onto paying off high interest rate mortgages (for reference, a high interest rate was 5% … which is much different than today’s mortgage rates being “good” at 7.5%). We went through the process to refinance several mortgages, so we’re at a point where we’re happy with the mortgages that are left. If we wanted 100% cash flow, we’d start paying towards principal balances. However, we don’t feel that’s necessary for our current situation. We have 6 mortgages left (including our personal residence) out of 14 houses.

We definitely are more hands on with our money management than most people are going to be interested in. Now that we’re happy with our mortgage situation, we are focused on the interest side of our money working for us. With multiple Treasury bills that are reinvested for short periods of time (4 week and 8 week bills), then we’re able to earn quick interest while we don’t have a purpose for that money.

One of our houses has a balloon payment again (commercial loan). That will come due in about 3.5 years. Considering what current interest rates are, it doesn’t appear that refinancing is as enticing as just paying off the balance or selling the house. We’ll have to keep that in mind as we work on investments and having enough liquid cash over the coming years, because that loan’s balance is going to be about $173k at the end of the 5 year term.

For now, we’re in a good money management state with several short term bills and a savings account rate over 4%.

We have been surprisingly busy around here. I’ve been juggling a few rental issues, staying on top of some billing issues, and trying to make it through a commercial loan process.

At one point, most of our loans were held by one company. That was a more simple life. Even though we’re down to 6 mortgages under our name, it’s through 5 different companies. I’m really struggling keeping up with them and getting in a groove after our most recent refinance. I’ve mis-paid things 3 times now. I’m always on top of our payments, but something just isn’t clicking right now for me. I just paid one of our mortgages due April 1 instead of changing the date to be an April pay date. At the moment, we have a buffer in our account because we’re getting to this closing next week, but we usually don’t, so hopefully I have this figured out now that I’ve made so many mistakes.

RENTAL PROPERTIES

LEASE RENEWALS

We had 3 properties process their renewals this past month. Each of them had cost increases to their lease renewal (875 to 950 effective 5/1, 850 to 900 effective 8/1, and 1025 to 1100 effective 5/1). We have another property that will have a renewal offer go out this week. Then we have 3 that will need action by the end of April because the leases expire 6/30, and one that will need action by the end of May because it expires 7/31.

MAINTENANCE

We had a tenant reach out to us that they found bugs in their bathroom tub. She sent pictures and, sure enough, they were termite swarmers. I have way too much experience with termites. I called our pest company, and they sent someone out for an inspection to confirm they were termites. Then I got a call that because we didn’t pay the annual fee to keep our warranty current for the last 3 years (we had the house treated for termites in February 2019 when we bought it because there were active termites and extensive damage by the front door that needed repaired), they could charge us $650 again. However, since we’re considered a business account, she’d be happy to let us back pay the termite warranty and they’re treat it. So I paid $294 for the treatment instead (split with a partner on this house). She also informed me that they had cut off the hot water to the kitchen sink because there was a leak. I don’t know why tenants don’t tell us these things right away! I had my plumber out there the same day, and he replaced the whole faucet. That was $378. That’s one of those charges that’s frustrating because we could have replaced the faucet on our own, but we don’t live there anymore. Oh well; it’s also a cost split with our partner, so that helps.

We had another tenant reach out saying that her kitchen sink drained slowly. She’s been with us since we bought the house and never asks for anything. She’s on top of communication and was super appreciative each time we agreed to renew her lease. We had done a huge sewer line replacement project at this house, so I was skeptical of the issue. It turns out there was a plastic fork lodged down there, but I just let it go (meaning, she’s then technically responsible for the cost). Our property manager let her know that if it happens again, she’s financially responsible, but we’ll cover the cost ($200) this time.

RENT COLLECTION

We FINALLY got the check for one of our tenants that had an approved rent relief application. They submitted an application in November to cover December, January, and February rent. By mid-December, they ended up paying December rent because they hadn’t heard (and the application expires, meaning their protection from eviction expires (not that I would have pursued eviction for this group because they’ve been great tenants for several years)). They received approval for 3 months worth of rent and 2 late fees on January 11. We received the check on March 4th. So frustrating in that process, but still better than an October approval and us getting those 3 months paid at the end of January.

We had our usual suspects not pay rent. On the one house, they didn’t tell us they weren’t paying rent for the longest time. Now, they tell us they’ll pay us on a later date. I let it go this month, but with them paying on the 23rd, that means we’re in a perpetual cycle of not getting rent on the 1st. We have a partner on this house, so I plan to address it next month if they claim another 3+ week delay in getting us the rent. On the other house, she let us know in February that she’d struggle to pay rent and she gave us random amounts throughout the month. I let her know she was still $106 short from February and that she was now in default of March’s rent, and I got no response. Then Mr. ODA had $1000 show up in his account on Friday. She still owes $371 between the two months, but at least we have the mortgage payments covered. She’s also the tenant that we plan on not renewing her lease because she’s caused issues throughout her tenure.

BUYING A NEW PROPERTY

We’re still in the process of getting through closing on a new rental property. We’re expecting to close not he 24th, so we’ll see how that goes. It’s a commercial loan, and it operates different from residential mortgage underwriting, so we’re in the dark. Communication has been next-to-nothing. We’re currently waiting on the appraisal to come back. That was our one hurdle to getting into the house. I said once the appraisal clears, then we (as the buyer) shouldn’t have any risk in getting to closing. Therefore, we were hoping to have the house painted before we close (I would do the painting), then we could refinish the floor and get the rest of the cleaning done the weekend after closing, and get it listed for rent for April 1. I suppose I wouldn’t be trying to get to the house before Friday, so I guess I can be patient and wait to see what happens with the appraisal for a few more days (even though the appraiser was on site last Tuesday, and I’ve never had it take more than a day or two to get the paperwork).

REFINANCE FOLLOW UP, STILL

We still have an issue with the mortgage that I ended up paying 3 times for the 2/1 due date. Our refinance was difficult, and the communication continued to be difficult after closing. I asked on 2/1 whether our loans had been sold yet because I was surprised I hadn’t heard. Usually, I see a note saying to pay the new company before the first payment, thereby not paying the first payment to that “first payment notice” place that comes with the closing documents. The company’s contact said to keep paying them because they hadn’t sold the loans yet. I didn’t open the attachments in his email because I assumed he was reiterating what he said in the email. Turns out, one of the loans was already sold, and I should have paid the new company. Well, I processed a paper check to go to a completely different company (started with a C, and I didn’t catch that I selected the wrong one in bill pay). Luckily, that company sent us our check back, saying they think our loan is closed with them and they can’t process the payment (thank goodness we once had a loan with the address I put in the memo line so they could clearly make a connection and say “we don’t want this!”). When I noticed my mistake on the 14th, I sent a handwritten check that I rushed to the post office at 4:55 to get post marked. In the meantime, I found out that I was able to set up an online account with the new company even though I didn’t have the loan number yet (they gave it to me over the phone). I paid the new company online to make sure I didn’t have anything on my record claiming I didn’t pay by the 15th and it was late. I figured I’d rather manage 3 payments being made than fight the credit companies to change my credit report. Well, the initial company cashed my handwritten check, but they still haven’t sent the money to the new mortgage company. They just kept telling me they have 60 days to get it to them, and I said that’s unacceptable that they’re holding my money. That was a week ago that I was told I’d get a call back, and I haven’t heard from them.

PERSONAL EXPENSES

Now that the basement is done, I had a strong urge to finish projects. There were several things that were starting but not completed. Those final punch list items always seem to take forever. I was impressed that Mr. ODA pushed to get some of the things in the basement done right away, even though they weren’t on a critical path. However, I didn’t uphold my end of the project by painting those things, so I got back to that. I mentioned several of the projects in a recent post, and I’ve done a whole lot more since that post. But all that to say, I’ve spent a lot of money in the last month. I bought a lot of supplies to finish off these open projects. I also had big purchases of cabinet hardware, a dining room table, a desk, and a wood. We haven’t done very much out of the house, so we don’t have a lot of other expenses than these projects, which means our credit cards are actually have the usual balances. We did book an AirBnB for a trip at the end of the summer with friends of ours. That was a big hit on the credit card for a week at the beach, but they reimbursed us for their half.

SUMMARY

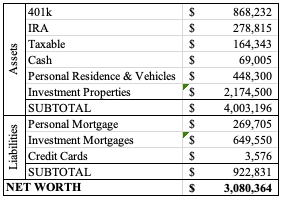

It feels like I just keep lowering the balance in our investment accounts each month, but I went to look at February 2021 to see the total. Even though some balances have decreased, we’ve still contributed to the accounts, so overall they’re $21k higher than last year, which is encouraging. I guess I should also focus on the property values raising significantly. We’re over $500k higher than last year in our assets, and our liabilities (i.e., mortgages) are about 13k less than February 2021. We’re also still over $3M on net worth, even if we’re hovering right around that. We’ll add about $50k to our net worth by the end of the month, as long as we close on the new property on time.

You hear this term in real estate often. “What are the comps?” “Have you run the comps?” It’s short-hand for “comparables.” These are the houses that are similar to the house in question (whether you’re trying to list a house for sale or purchase a new house) can be used to determine the value of a property. It’s touted as if it’s difficult, and I’ve seen several comments in a “moms” group that told me more people need to know about appraisals.

An appraisal is an expert’s estimate in the value of something. It can be something small like a piece of jewelry or something big like a house. During a closing process that includes financing, the bank issuing the loan is going to request an appraiser evaluate the property being purchased. The bank is using this as a mechanism to verify that the property is worth the contract amount.

A recent appraisal we had done stated the following (for context). This report is based on a physical analysis of the site and improvements, a locational analysis of the neighborhood and city, and an economic analysis of the market for properties such as the subject. The appraisal was developed and the report was prepared in accordance with the Uniform Standards of Professional Appraisal Practice.

If your real estate purchase is through a loan, the bank is going to require an appraisal. Have you ever looked at the appraisal? The lender is required to give you a copy.

Let’s dig into one of mine.

THE APPRAISAL

This particular appraisal was completed for a refinance of a loan. It was done in December 2021 and is 37 pages long, granted a lot of that is teaching documentation.

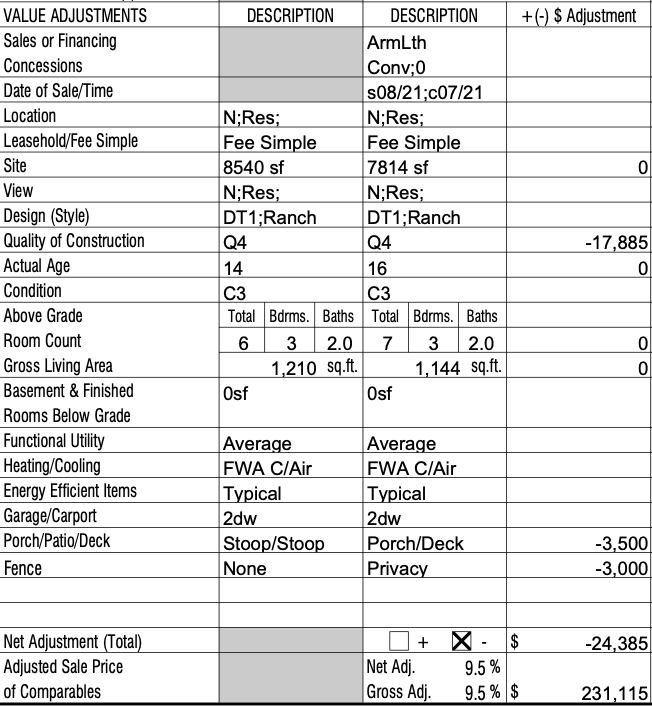

First, the appraiser identifies the property’s characteristics. Things like the address, plat number, taxes, house size and details, utility hookups, and neighborhood demographics are filled out. Here are a few snapshots with that information. All appraisal reports I’ve seen have looked like this (across multiple states).

Once the appraiser identifies the property’s details, he moves on to finding nearby homes that have sold recently. The comparable sales are of similar age, construction quality, and condition. There are formulas available to the appraiser to determine how differences between the property he’s appraising compares to the similar nearby homes. For instance, having another bedroom increases a property’s value by a certain amount, having a garage could increase the property value, having a fence affects the value, etc. Here’s a snapshot of one of the comparable sales for this appraisal. The first ‘description’ column contain the details of the house being appraised. The second ‘description’ column contains the details of the address he’s using as a comparable. Then there’s the adjustment column to identify how those differences affect the value of the home. This home being used had sold for $255,500. Each difference is calculated to account for a value of the home had it been even more similar to our house. So this house having a porch instead of a stoop is affecting the value at $3,500 (I don’t know how these values are determined, but I assume it’s all a software calculation that keeps it consistent).

This appraiser used 7 comparable sales. We’ve historically seen 3-5 houses used, but this market has created more options than usual. The appraisal was determined by removing the value of the land (since that’s calculated by the tax records regardless) and applying the average price per square foot amount to our house. The valuation came in at $230,000. We purchased the house for $117k 5 years ago, so that was a nice surprise. We were able to take out a loan for up to 60% of the appraisal’s value.

YOU CAN DO A RUDIMENTARY APPRAISAL YOURSELF

The point here is that an appraiser is using the specifications of nearby, similar real estate transactions to determine the value of the house in question. Since the concept of an appraisal is straightforward, you shouldn’t feel like you’re incapable of doing your due diligence on a purchase or determining the sale price.

It’s important to note that you’re focusing on houses that have SOLD. You’ll see houses nearby listed for sale at different prices, but that doesn’t mean that’s what the market deems a “fair market value.” You want to focus on the sold prices because that means someone was willing to pay that for that type of property, and a bank likely confirmed the value with an appraisal.

In this “moms” group I mentioned, several people told a person that she needed to hire an appraiser before listing her house. An appraiser is about $400-600. In a house sale, the buyer is responsible for the appraisal. Therefore, as the person listing the property, you’re not “ahead” in any way by paying for an appraisal up front because it wouldn’t have been your cost to bear anyway. Instead of paying someone to perform an appraisal, you look at houses nearby that sold recently.

Back in 2018, we were using sales for 6 months to a year prior to the date we were searching. The housing market hadn’t changed all that much year-to-year that you couldn’t use sales from a year ago. These days, you need to be looking at houses that have sold in the last 3 months, and maybe go back to 6 months if you don’t have any good options. If you need to use sales from a year ago these days, then assume a hefty inflation (in most areas) from the price it sold at, but it’ll at least give you a good starting point on the price.

For recent sales you dint, you’re looking for properties with the same number of bedrooms and bathrooms, approximately the same square footage, and approximately the same size yard. You’re hoping for pictures too so that you can evaluate if the condition of the property is objectively better or worse than the property you’re considering.

PERSONAL EVALUATION EXAMPLE

We’re currently on the hunt for another rental property to add to our portfolio. Things are moving fast, so we’re doing quick evaluations on the fly with best guesses of value. We have the benefit of doing several of our own real estate transactions, including plenty of searching for options outside of the ones we did purchase. Therefore, we have the knowledge to be able to eyeball the value. In the beginning, it would probably work best if you write down the details (similar to what’s found in the appraisal screenshots above) to identify the appreciable differences between your options.

We were looking at a property that was in poor condition. The listing even stated that they were offering a $3,000 flooring allowance as part of the sale, acknowledging that the condition was poor. The house is 3 bed/1 bath (colloquially referred to as ‘a 3/1,’ and was listed at 169,900. The listing photos showed a scratched up floor, but otherwise looked ok.

Not bad, right? Well, I don’t know what filter they used, but these colors are a lot more vibrant than the condition of those cabinets and appliances were in person. The photos didn’t capture the gouged walls or layers of paint that weren’t properly painted between coats. And, unlike popular HGTV shows would you have you believe, the paint color isn’t something we’re caring about. It’s a bonus if it doesn’t need a coat of paint before we rent it, but we’re generally expecting to paint a house after we buy it. The photos also don’t portray the filthy bathroom with the mismatched patchwork tiles in the shower. We stepped back and seriously considered flipping this or improving it and using it as a rental still.

I opened my Zillow app. When I’m looking for quick information, I’m focusing on price per square foot, rather than actual purchase price. This house came to $151/sqft. In the Zillow app, on the upper right corner, click ‘Filters.’ I always click ‘Reset’ before I start a new search because I never know what I last changed in the parameters. I chose the ‘Recently Sold’ toggle, left everything the same, and then at the bottom I changed ‘Sold in Last’ to ‘6 months.’ In this area, if I looked at a broader spectrum of recently sold houses, I’d have too many to look at, and the prices in 2019 would be drastically different than what’s currently happening in this market. If I still had too many results, I would have filtered down to 90 days. However, it’s January when I’m looking, so there hasn’t been too much activity in the last 3 months, and I want to capture more options that sold during the summer months.

Then I just started clicking the yellow bubbles of prices. I want to first focus on the ones closest to the house I’m looking to buy. As I get further away (or cross major roads), I’m probably looking at a different school district, or different crime levels, or different ‘feel’ of the neighborhood; be careful how far out you look.

Here are my thoughts on the first comp I found. The parentheses identify how it relates to the property I’m viewing: either it’s the same (=), my property is better (+), or my property is worse (-). It’s a 2 bed (+), 2 bath (+), with low curb appeal (+), smaller lot (+), nicer floors (-), covered deck (-), stainless appliances (-), kitchen cabinets were original and the stove’s vent hood was outdated (+), the master bathroom needs a facelift (+). This house sold in September 2021, so it’s a fairly similar market to what I’m looking in now. It sold for $117/sf. With the difference in the number of bathrooms and bedrooms, it’s hard to compare. Subjectively, the house I’m interested in is worse than this house, but it has another bedroom and a bigger lot. I decide that this comp doesn’t get me close to $151/sf for the house I’m looking at.

Comp 2 is around the block. It’s very close to the size of the house we’re evaluating (=) and is a 3/1 (=). It’s adorable, with great curb appeal, so it draws me in. Then I start noticing some things that are red flags. The roof doesn’t appear to be in bad shape, but my eyes are drawn to a water stain on the living room ceiling (+). It appears to have laminate flooring in the kitchen and carpet elsewhere, whereas the house we’re looking at has hardwood everywhere; our hardwood is beaten though, so this is hard to compare. I see that there’s old vinyl in the laundry closet that wasn’t addressed when new laminate appears to be laid, there’s some poorly laid wood flooring in just the entrance to the master bedroom, and there are several stains in the carpeted bedrooms. The backyard has power lines running through it (+); I see several issues with the vinyl siding on the house (+), but it has a covered deck (-). They had tried to sell this house from July to October, which tells me that plenty of people were drawn in, but those defects were clear (and probably more) in person. They started their listing at $166/sf and ended up selling at $146/sf. While this house looks to be in better condition than the one I’m evaluating, this tells me that I’m probably looking at the $140s/sf for the one I’m looking at.

There’s a 3rd ‘comp’ that caught my attention right behind the house I’m evaluating. Zillow claimed it was sold for $334/sf. Interesting anomaly. Our Realtor was able to pull the MLS and see it actually sold at $150k, so about $115/sf. So moving on.

I found a brick ranch around the block, so I’m excited that it’s very similar to the house I’m looking at. It’s a 3/1 (=). It sold in September 2021 for $149/sf after having first been listed at $163/sf in July. I dive into the pictures. The floor isn’t destroyed (-)! There are mismatched, yet updated, appliances in the kitchen. It’s frustrating, but they probably have a better lifespan that what’s in the house I’m looking at (-). The bathroom has been updated recently, but it’s small, and there’s no picture of the shower side of the bathroom (concern, but still better than the house I’m viewing) (-). There are minimal pictures, but at least one of every room. After comp 2 went for $146/sf, and this is better condition at $149/sf, I’m now putting the house I’m evaluating below $145/sf.

There’s a brick 3/1 next to Comp 4 that sold for $162/sf. But there are no pictures and it was for-sale-by-owner, which tells me someone probably overpaid for a higher list price because they were desperate. I’m throwing this out and not using it as a true comp.

At this point, I’m just standing there trying to evaluate whether this is worth pursuing or not. I can do detailed looks at comps later on a computer with a pad and pen. I decide that $145/sf is my highest value of this house and it’s horrible condition. However, even with that, I don’t want to go that high because of all the work that needs to be done right away on the house. The comps told me that’s the value of other homes that needed some work, but looked livable from day 1. I decided to sit on it. Well, the next day, it went under contract at a reduced price of $146/sf. I won’t know the actual price of the contract until it closes, but for now, it looks like someone bit on the $146/sf.

Now this is really important if you’re evaluating for a purchase. Do not overpay for a house. Do not feel pressured into needing it now. We’ve put in several offers on houses, but we’re not going to get into a bidding war. We also put in an offer on one house, and the seller said “raise it $5k and state the offer isn’t contingent on an appraisal, and you have a deal.” No. Requesting the appraisal clause to not be checked says we were probably overpaying even at the offer we made. So thank you to this man for letting me know that it was time to walk away.

SUMMARY

You can typically rely on your Realtor to provide you comps through the MLS. If you have questions about their valuation, ask for the details. I have an instance where I didn’t agree with my Realtor on a list price of our last personal residence. In this particular instance, I had better knowledge of the housing market where our house was than he did, because he focused on sales within the nearby city limits, and we were in the suburbs. He ran comps based on basic metrics (number of bedrooms, square footage). I had the benefit of knowing details behind some of the sales he was using or how some houses weren’t a good fit to use as a comp to the house we were selling. I was able to sway the list price to even higher than he suggested, and we were under contract that weekend.

I know how it works. I’ve taken the time to research and understand the process just enough that I can protect my finances and interests in these transactions. I’m not sharing this as an example to fight your Realtor on their suggested list price, but as a way to show you need to be an informed consumer.