In January, I shared why we chose to finance our new (used) car. To those who know us, they would think paying interest would be an immediate no, but there are reasons that it may work in our favor. We also have a mentality that the best decision is the one that makes our money work the hardest, not an overarching thought that debt is bad.

The dealership was offering $1000 off the purchase if we financed. Mr. ODA ran the numbers, and we decided that was worth paying the minimum 4 months of interest. I paid off the loan, so now we have the actual numbers.

Here’s what I had said back in January: The financing was 6.99% and we chose the option that allowed pay off after 4 payments. There was an origination fee of $175, which is rolled into the principle. Our payment is $151.94. The first 4 payments hold $175.07 worth of interest. So we will pay $175.07 of interest and the $175 origination fee as a means of taking $1,000 off the list price. That nets us, including the $30 of credit card rewards, $679.96 less on the list price. After the 4th payment is made in May, we’ll make a lump sum payment of about $7,134 to pay off the loan.

I did not read any prepayment penalty data, but Mr. ODA wasn’t so sure. We made a lump sum payment to bring the balance down to about $2500 in February. What I wasn’t prepared for was that the loan system decided that I didn’t owe any monthly payments for several years at that point. I decided to just go ahead and make my monthly payment a couple more times after that even though it was being applied as principle only and not a monthly payment.

We paid $175 origination fee and $112.49 in interest. So our net save on the final purchase was $712.51. I also included the fact that we made $30 by only financing the bare minimum and putting the rest on a credit card that got us 2% (there was no fee from the dealership to put this on the credit card, which was also a factor in the decision), bringing the net to $742.51 worth of the $1000 off the purchase price. This was better than projection because of the way their loan system applied our lump sum payment.

We bought a Tesla. In the process, they’re offering a 0% APR promotion. They let you see how your credit rating affects your monthly payment (through different APRs). The final column in the table below shows the increase each level adds from the previous level.

This is based on a 60 month term. So, ignoring the promotional option available, between the ‘>720’ and ‘680-720’ would cost you $39 per month. That’s a total of $2,340 over the loan term. By using the promotional rate, that’s $88 per month “saved,” which is $5,280. Don’t let it be lost that working on your credit history and credit worthiness is something that pays off into the future.

When we look into a large sum of money leaving our account, we consider the “net present value” of the dollars. The net present value is the difference between the present value of cash inflows and the present value of cash outflows over a period of time. Investopedia uses the following over-simplified example. “An investor could receive $100 today or a year from now. Most investors would not be willing to postpone receiving $100 today. However, what if an investor could choose to receive $100 today or $105 in one year? The 5% rate of return might be worthwhile if comparable investments of equal risk offered less over the same period.”

The 0% interest loan through Tesla is for about $40,000. Mr. ODA calculated that our net present value of money, based on our approximately 4% savings interest rate, is $36,017. Taking nearly $40k out of our savings account wouldn’t be a financial problem, but it’s not the smartest financial move in our portfolio. Instead, we’re going to pay about $580 per month, while the “balance” of that $40k earns interest. At 4% interest, the balance of $40k earns nearly $1,000 in a year. That balance will continue to dwindle, therefore lowering the interest earned each year, but it’s still a significant sum of money. In the first few years, the interest earned is essentially paying a couple of months worth of the car payment.

By being conscious of our financial standing in the world, we’ve set ourselves up for earning these promotions. Had our credit worthiness been below a score of 720, it would have cost us over $5k more over those 5 years of the loan. While I understand that purchasing a Tesla may be considered a luxury, this concept and awareness can be applied across all financial decisions, which is why I wanted to highlight it here.

We’ve hit some pretty big milestones financially. Mr. ODA casually mentioned a certain number by a certain age, but our goals were more associated with quitting our full time jobs. I quit my job in May 2019. We’re in a situation for a couple of years where we’ve been ready for Mr. ODA to quit, but we keep pushing the date back because his job isn’t preventing us from doing the things we want to do.

How did we get to the point where we replaced my income and I could quit working without scaling back anything financially? We took risks. Some of them were big ones. Some of them weren’t so big, but they felt big at the time. Most risks worked in our favor, but some did not.

RETIREMENT ACCOUNT LOAN

Mr. ODA and I both worked for the Federal government. Their version of a ‘401k’ is the Thrift Savings Plan (TSP). There were two loan options that were available: a primary residence loan or a general purpose loan. You then repay the loan back to your account with interest (the interest is paid into your account as well). When we took our loans, the rate was just over 2%. According to tsp.gov, the rate is currently 4.75%. There’s a fee of $50 to take a primary residence loan and a fee of $100 to take a general purpose loan.

While you’re missing out on the compound interest of your account when you take the loan, the ability to buy our own house, create that equity, and be at the beginning of our careers made the decision easy for us. We made extra payments during the repayment period, and we were able to adjust the regular payments up and down based on our financial needs each month. We have no regrets in our decision.

ADJUSTABLE RATE MORTGAGE

An adjustable rate mortgage (ARM) sounds scary. A variable rate. Most people are used to locking in a 30-year mortgage. I’d venture to say that most people also think they know what an ARM entails, so they don’t even consider it. We considered it. We looked into it in great detail. We couldn’t see why more people didn’t use it. We actually were very hesitant over this decision the first time because an ARM’s reputation is very negative. However, we took our time to lay out the numbers and see what would work best for us.

The first time we used an ARM, we knew we had no intention of being in the DC area for more than 5 years. By using an ARM, we saved thousands worth of interest in our mortgage payments over the three years we owned it.

There are several “fail safe” parameters in an ARM. For one, you do lock in a rate for some period of time. We considered 5 year, 7 year, and 15 year options. Then after that period of time, your rate can only adjust within the contractual terms. For example, we have one rate that can adjust 2% in either direction at the 5 year mark, and then 1% for each of the following 4 years after that, with a cap of paying a maximum interest rate of 7% (this is an old loan, clearly). The rate adjustments aren’t a given, and they’re adjusted based on the prime rate at that time, not based on the whim of the bank or the maximum it could increase.

We also ran the numbers based on the interest rates. An ARM’s incentive was that the interest rate is lower than the 30-year conventional loan rate. I don’t have the details since this post is more of an overview, but the ARM saved us money we paid towards interest. Interest is a higher percentage of those earlier payments in an amortization schedule. We either sold the house or paid the loan off early, so the ARM adjustment never came into play, and we saved all that interest cost.

BUSINESS/COMMERCIAL LOAN

A series of events had us asking a local credit union about loan options. They offered us a commercial loan. This one has a big catch though: there’s a balloon payment. Our loan is amortized over 30 years, which is how our payments are calculated. However, the balance of the loan is due at the 5 year mark. That balance is going to be about $175k. We have no plans to pay that off by that time (we aren’t even making extra payments towards it). We will refinance it. The pro here was that our interest rate for a loan closed on in 2022 was 3.625% (when mortgage rates were in the 5% range). Hopefully by 2027, interest rates are lower than they are today; this is a gamble at the moment.

PARTNER

There’s a cap in the “Fannie/Freddie” world of the number of mortgages a person can hold. That cap is 10. There was a point where we had completely leveraged ourselves and ran out of room. We had a Realtor friend interested in more rental properties, and he agreed to front our down payments, which we’d pay back with interest, and have a 50% share in the houses.

We signed an agreement with him that outlined our payments to him for the down payment he covered (which we paid off in about 3 months), and it established our 50% shares in the two houses purchased via this method. We purchased the houses in April 2018 and February 2019, and put them in a limited liability corporation (LLC). Each month, I collect rent from the houses and pay out our partner’s share. These houses don’t ask for much (one has been rented since before we owned the house and one has a tenant that has been there a few years), but if they need something, I handle coordinating the maintenance request. We should have set up a schedule where I’m paid for my time since Mr. ODA and our partner really don’t do anything for these houses, but luckily the requests are few and far between. We split all costs 50/50.

RENTERS WITH COMPENSATING FACTORS

I have several examples of entering into lease agreements with tenants that don’t have a perfect record. In these instances, we typically request some sort of compensating factor (e.g., a cosigner, an additional security deposit). We give everyone the chance to tell us about their financial and rental history before we run a background check on them (telling us doesn’t cost anything, but a background check does).

We had a prospective tenant not disclose a bankruptcy on her record. I could have immediately disqualified her and her husband, but I gave them a chance. They lived in that house for a year. They only moved because his job after grad school took them out of the area, but they set us up with a new tenant at their departure, and she stayed there for several years. Then they moved back to the area, and they requested a house of ours. We had one available, so we happily had them move into it. There’s one success story from giving someone a second chance.

I also have a couple that doesn’t have a happy ending. We had purchased a house without vetting the area. I had fully vetted a house two blocks away, but I learned my lesson that the crime of an area doesn’t need more than one block to change its ways. This house was in a bad area. The house itself was adorable. It attracted wonderful people to come see it, but they’d check the crime history of the area and decline applying (understandably). Someone came forward with a 448 credit score. That’s pretty bad. She wrote a really nice letter though. She disclosed everything up front and said she just wanted a roof over her and her son’s heads. I believed it. We then spent months and months struggling to get her to pay her rent, even offering her a payment plan several times and changing her lease structure to allow her to pay twice per month (hopefully eliminating the constant late fees she was accruing). We eventually gave her 30 days notice to vacate the premises due to lack of payment. She didn’t even make it a year. Instead of listing the property for rent, we ended up selling it. That was a whole other debacle where we entered into a contract to close by September of that year, but we didn’t close until the following January due to the lack of financial qualifications on the buyer’s end.

PAID OFF LOANS/MORTGAGES

This doesn’t appear to be a big risk. What could go wrong with paying off your mortgages? Well, if we didn’t have a cash reserve, and there was an emergency, then we paid off these loans with the cash on hand, leaving nothing to cover that emergency. However, those dooms-day concerns rarely come to life, and we had continued cash flow that replenished our accounts.

The positive here is that we freed up cash flow. Instead of having mortgage payments to make every month, we now have the cash to go into savings or towards any higher-than-expected bills. Besides the house we sold, we’ve also paid off 6 mortgages. That means that we’ve paid less interest to the banks, and that’s more money in our pockets.

We haven’t paid off any other loans because they’re all below 5% interest (they’re actually all below 4% except for 1 with our partner, and we would need his buy in the pay that off, which he hasn’t wanted to do). After payments to mortgages, our property manager, our partner, and utility payments, we have over $8,000 in cash flow per month. I will note that this doesn’t include things that I need to save up for each year to be able to afford (e.g., taxes and insurance), and it doesn’t include maintenance needs that crop up. Cash flow is important for us because if Mr. ODA quits his job, that’s less income to offset our regular personal expenses.

FINANCIAL AWARENESS

On any given day, we’re weighing several financial decisions fluidly. There are the givens that we have to pay the bills that are out there. I have to pay all the mortgages and utility bills. I weigh the best time of the month to pay each bill, which means that I may not pay them as soon as the statement arrives, but may wait until closer to the statement due date (but never carrying a balance unless it’s 0% interest). Then there are the options such as paying additional payments towards a credit card with a 0% interest rate, additional principal payments to a mortgage, or additional investment plans. We’re not looking to apply for any loans, so the $9k balance on a 0% interest credit card doesn’t have any attention of mine except the $500 I pay each month. I have it marked on my calendar when that 0% introductory rate expires, and I’ll have to pay the balance in full.

Our money is handled by a full, big picture, approach. Each day, there’s a chance that we come to a fork in the road and make a different decision because the variables changed slightly. We don’t put our money into “buckets” or “envelopes.” In my experience, people who handle their money like this end up overspending.

We hit our goal to replace my income well before our son was born, but then I kept working until he was 9 months old. While I was still working, we could have easily said, “we hit our goal, but since you’re still working, let’s put all that money into a slush fund of some kind.” When people see any “extra” money, they then look for their next splurge. They feel they deserve something for saving money instead of putting that extra money to work for you and your future.

There are those “autopilot” moments in our finances, but when it comes to making a big change, we put pen to paper and check the details. We aren’t going to take $100,000 out of our investment accounts to pay off a 2.5% mortgage. But one day, we will have to consider what to do with our loan that has a balloon payment, which shows it’s not a hard and fast rule that we won’t pay off anymore loans early (because if interest rates are still at 7.5% in 2027, it may not be worth refinancing that balance).

LIVE SMART WITH INFORMED DECISIONS

Take the time to make informed decisions and research the data for yourself. Run models with the projection of money to see for yourself if it works in your situation. Don’t spend your days listening to other people’s opinions on actions. If we had listened to opinions, we wouldn’t have taken a TSP loan or taken out ARMs.

We’re at over $4 million net worth, have a solid cash flow (which is important because if our net worth of $4 million was tied up in a retirement account, that wouldn’t give us the ability to live comfortably now), and have plenty of money going into accounts for the future (for both us and the kids). Our spending is managed regularly with an ingrained thought process. Take the small, first step for yourself without other people’s opinions weighing you down.

If you want to live differently from everyone else, you have to take action and think for yourself.

We turned over a rental in April, bought a new house that requires work in June, and turned over another rental in July. Those activities have a lot of expenses associated with it. While we could have strategically spent the money and paid off credit cards, it’s nice to have a cushion. When we’re faced with a lot of large expenses, Mr. ODA searches for a new credit card.

Why do we open a new credit card for big expenses? Because it’s a free short term loan for us. We’re looking for a card that provides an introductory 0% interest period, as well as some other bonus(es). Carrying a balance on a credit card and paying up to 25% interest is a non-starter in our financial portfolio.

Mr. ODA had searched for a new credit card back in the April timeframe, but we had multiple credit hits around that time, and I didn’t want to risk it. We paid off the expenses for the first rental turnover through our regular credit cards. Once we bought our new house and we knew that turning over another rental was looming (with big expenses like carpet replacement), Mr. ODA found a credit card he wanted.

At the last second, Mr. ODA switched which card he wanted. The card gave an introductory offer of $200 back after you spent $1000 within 120 days, up to 5% cash back on two categories you choose, 2% cash back on one everyday category, and 1% on all other purchases. It had 15 months of 0% APR and no annual fee. He received a credit limit of $500. Seriously. He called to get a credit increase and find out why it was so low, but they said they required another credit report pull to talk to him about anything. Nope. So we have this random $500 limit credit card in our portfolio. We’ve spent our $1000 and will get our $200 cash back (unless they find a loophole, which I would expect based on how this company’s relationship has been so far), and then this card will just sit unused until they close it years from now due to inactivity.

Since that was a bust, Mr. ODA opened a different credit card in my name (spread the wealth on credit inquiries). I was granted a $9,000 credit limit, and we got straight to work spending that. There’s no annual fee; it has a 15 month 0% introductory period; and earn 5% cash back on purchases in your top spending category (automatically, without choosing a category) up to the first $500 spent and 1% cash back after that. It gave us $200 cash back after we spent $750 in the first 3 months.

Two of our first few expenses were a vanity for our new master bathroom and 1,000 sf worth of vinyl plank flooring for a rental. Our balance within the first week was over $5,000. As much as I can’t stand to see that balance sitting there, it has helped us move money around. Usually we focus our spending in the categories that each credit card offers with higher rewards, but for these bigger expenses, we’re focused on being able to float them for several months.

We used a Home Equity Line of Credit (HELOC) for the down payment on the new house. Originally, we had been paying down the principal on that, and put $14k towards that over the last month. We then decided we should focus more into buying the dip of the stock the market instead of paying down that account with 4% interest rate (although that’s variable). That’s what we’re currently focusing on, knowing that when we sell our current house, proceeds will pay off the HELOC in a short few months. We currently have about a $1500 cash cushion because we know that we have the HELOC to fall back on. For instance, we’re replacing the driveway and walkways at our new house, and we’ll pull cash out of the HELOC to pay for that (they don’t take credit).

If your credit is in favorable standing and you have large expenses looming (without a need for a new loan/mortgage in the near future), then look for a new credit card. Don’t open any random one. You’re looking for 0% interest for 12-15 months, no annual fee, and the possibility of a reward system (whether it’s an introductory offer related to spending, a cash back incentive for spending, or some form of both).

A HELOC is a line of credit secured by the equity in your home. This is different from a loan or mortgage.

What is equity? It’s the appraised value of your home that is not mortgaged. You may have put 20% down when you bought the house, and now you’re looking to tap into that equity along with the principal of the mortgage you’ve paid down. Or perhaps your home value has increased drastically, and you want to utilize the equity.

What is a line of credit? It is a revolving account of credit. This means that when you close on a HELOC, you don’t get a check cut for that amount right then. You need to “draw” on the account, as needed, which is essentially writing checks from that account to either yourself or another entity. As you make principal payments, the amount of principal becomes available again for a future draw, as long as you’re within the draw period of the line of credit.

Do you have to disclose the purpose of the HELOC? There are no parameters on what you can use the money for when you draw it from the HELOC. You may want to pay off a credit card that has a higher interest rate, do home improvements, do other construction projects, medical bills, etc. While you’d want to utilize this for larger purchases, you can draw smaller amounts as long as you draw the minimum required by your terms (e.g., no less than $100). You earn interest from day 1, so this isn’t more beneficial than a credit card that gives you a short-term “loan” for your statement period (you don’t pay interest on a credit card balance that is paid off by the due date).

TYPICAL TERMS

The application process is similar to applying for a mortgage. A bank wants to see your credit report, along with some backup documentation (e.g., tax returns, account statements). We also had to update our homeowners insurance to show the HELOC as a mortgagee.

A HELOC will typically only cover a portion of the equity in your home, depending on the bank’s terms. If your appraisal value is $400,000, and your mortgage balance is $250,000, then the equity in your home is $150,000. While there may be instances where a bank would approve a HELOC for the full amount of $150,000, most are going to approve 80% or 85% of that amount.

There are no closing costs associated with the HELOC. Typically, the bank processing the HELOC will cover the costs associated with the line of credit initiation up front. However, they will require those fees to be paid back to them if the HELOC is closed within a certain period of time (usually 36 months). For our first HELOC, when we closed it within the 36 months, we paid back a prorated amount of the fees (e.g., if the fees were $300, and we closed it after a year, we owed $200). For our current HELOC, if we close it within the 36 months, we’re required to pay back 100% of the fees they covered, not the prorated amount.

A HELOC has a variable interest rate, which may adjust monthly or quarterly based on the lender’s terms. A variable interest rate can adjust up or down. But this is something to be aware of because it’s not like a loan or mortgage that has a fixed rate made known up front. The rate, in our case, is set at the index rate with a margin. However, there’s a floor to the bank’s rate. What does this look like? The index rate is 3.50%. The margin is -1.00%. However, the bank’s floor is 3.00%. Therefore, even though 3.5-1=2.5, the minimum interest rate they’ll lend at is 3.00%. Therefore, our current rate is 3.00%.

There is a “draw period,” which means you can only take funds from the line of credit for a certain period of time (e.g., 10 years). When you do draw from the line of credit, you’re charged interest on the principal balance. During the draw period, you must make the minimum required monthly payments on the account, which is typically the monthly accumulated interest owed, but some banks may require principal payments during this period also. When the draw period is over, it enacts the principal repayment period, meaning you have a certain amount of time (e.g., 10 more years) to repay the principal balance of the HELOC. There is no charge for the HELOC existing though; it can be there and never drawn on.

OUR PROCESS

The most recent HELOC we closed on had a different process than the first. We expressed our interest, and since they already had our documentation on hand from a commercial loan, they didn’t ask for supporting documentation (e.g., account statements). However, for some strange reason, she said she couldn’t use the credit report from our commercial loan, and she had to pull our credit again. At the time we were applying for another mortgage, so the hit on our credit counted as “mortgage shopping,” so we gave up the fight and let it happen.

This company would have given us 100% of the equity available in our home. However, two weeks after initiating the HELOC process, we told them we needed a pre qualification letter for an offer we made on another personal residence. They then told us that since we’re on record as wanting to sell our home, they would only approve 80% of the equity.

The loan officer asked for two references for each of us. There was no information given on what this personal reference had to know about us. We both handed over our people, but they were never contacted, so we won’t know the purpose.

Finally, they asked for our homeowners insurance to show them as a mortgagee on our policy, which I was able to do with one quick phone call to that office.

Typically, the process will include an appraisal. This bank had a valuation system that they used. Based on this woman’s inputs into the system (which were all wrong), she said that she could approve us for $100,000 without paying for a full appraisal. We don’t need more than that, so that was sufficient to us.

We closed the HELOC a month after expressing interest. Our process may have been slower than the typical period it would take because we were fighting the credit pull for a while (not to mention the company we were working with is notoriously slow at responding to inquiries). Mr. ODA expressed our interest in pursuing the HELOC on April 12th. We were cleared to close as of May 11th, but we chose to close on that following Friday. We went to a local bank branch, and a relationship banker went through the documents with us as we signed them.

WHY THE HELOC FOR US?

My general plan was that we’d have a HELOC initiated, so that when we found a new personal residence, we could use the HELOC for the down payment of that house without having to sell our current house first. In the past, we’ve sold our home, went into temporary housing, and then moved into a new home. Granted, all our past home purchases were in a completely different locale than where we were living, but I really didn’t want to manage storage of goods or go into temporary housing with two kids and a dog again.

We initiated the conversation on the HELOC without having any intent to move yet. Not to go into too much detail on this topic, but we need to be residents of this house for two years to avoid paying capital gains. Our 2-year mark isn’t until November, so we weren’t in a rush to move before then. A home with the same floor plan around the block from us sold for $190k more than what we bought this house for less than two years ago, so we expect there to be a hefty chunk going to capital gains if we don’t meet the two year requirement.

I was keeping an eye on the market, but clearly had no plans to move. To me, a regular check on Zillow lets me know what I can get for my money. However, there are some things related to our current personal residence that are concerning, and we had decided that this wouldn’t be a long term location for us. With the market right now, I knew we’d either be paying a higher mortgage than I ever anticipated in life, or I’d be compromising on my wish list. Well, a house that met a lot of our wish list popped up in the area we liked for less than $500k, so we jumped on it. The house needs work, so even though we’ll close on it over the summer, we aren’t in a rush to move into a construction zone.

Once we close on the new house with funds from the HELOC, we’ll start accruing and paying interest on the balance. We’re not required to make principal payments until after the draw period, which is 10 years. When we eventually sell our current home, the proceeds from the sale will pay off the HELOC seamlessly through the closing process.

We have been surprisingly busy around here. I’ve been juggling a few rental issues, staying on top of some billing issues, and trying to make it through a commercial loan process.

At one point, most of our loans were held by one company. That was a more simple life. Even though we’re down to 6 mortgages under our name, it’s through 5 different companies. I’m really struggling keeping up with them and getting in a groove after our most recent refinance. I’ve mis-paid things 3 times now. I’m always on top of our payments, but something just isn’t clicking right now for me. I just paid one of our mortgages due April 1 instead of changing the date to be an April pay date. At the moment, we have a buffer in our account because we’re getting to this closing next week, but we usually don’t, so hopefully I have this figured out now that I’ve made so many mistakes.

RENTAL PROPERTIES

LEASE RENEWALS

We had 3 properties process their renewals this past month. Each of them had cost increases to their lease renewal (875 to 950 effective 5/1, 850 to 900 effective 8/1, and 1025 to 1100 effective 5/1). We have another property that will have a renewal offer go out this week. Then we have 3 that will need action by the end of April because the leases expire 6/30, and one that will need action by the end of May because it expires 7/31.

MAINTENANCE

We had a tenant reach out to us that they found bugs in their bathroom tub. She sent pictures and, sure enough, they were termite swarmers. I have way too much experience with termites. I called our pest company, and they sent someone out for an inspection to confirm they were termites. Then I got a call that because we didn’t pay the annual fee to keep our warranty current for the last 3 years (we had the house treated for termites in February 2019 when we bought it because there were active termites and extensive damage by the front door that needed repaired), they could charge us $650 again. However, since we’re considered a business account, she’d be happy to let us back pay the termite warranty and they’re treat it. So I paid $294 for the treatment instead (split with a partner on this house). She also informed me that they had cut off the hot water to the kitchen sink because there was a leak. I don’t know why tenants don’t tell us these things right away! I had my plumber out there the same day, and he replaced the whole faucet. That was $378. That’s one of those charges that’s frustrating because we could have replaced the faucet on our own, but we don’t live there anymore. Oh well; it’s also a cost split with our partner, so that helps.

We had another tenant reach out saying that her kitchen sink drained slowly. She’s been with us since we bought the house and never asks for anything. She’s on top of communication and was super appreciative each time we agreed to renew her lease. We had done a huge sewer line replacement project at this house, so I was skeptical of the issue. It turns out there was a plastic fork lodged down there, but I just let it go (meaning, she’s then technically responsible for the cost). Our property manager let her know that if it happens again, she’s financially responsible, but we’ll cover the cost ($200) this time.

RENT COLLECTION

We FINALLY got the check for one of our tenants that had an approved rent relief application. They submitted an application in November to cover December, January, and February rent. By mid-December, they ended up paying December rent because they hadn’t heard (and the application expires, meaning their protection from eviction expires (not that I would have pursued eviction for this group because they’ve been great tenants for several years)). They received approval for 3 months worth of rent and 2 late fees on January 11. We received the check on March 4th. So frustrating in that process, but still better than an October approval and us getting those 3 months paid at the end of January.

We had our usual suspects not pay rent. On the one house, they didn’t tell us they weren’t paying rent for the longest time. Now, they tell us they’ll pay us on a later date. I let it go this month, but with them paying on the 23rd, that means we’re in a perpetual cycle of not getting rent on the 1st. We have a partner on this house, so I plan to address it next month if they claim another 3+ week delay in getting us the rent. On the other house, she let us know in February that she’d struggle to pay rent and she gave us random amounts throughout the month. I let her know she was still $106 short from February and that she was now in default of March’s rent, and I got no response. Then Mr. ODA had $1000 show up in his account on Friday. She still owes $371 between the two months, but at least we have the mortgage payments covered. She’s also the tenant that we plan on not renewing her lease because she’s caused issues throughout her tenure.

BUYING A NEW PROPERTY

We’re still in the process of getting through closing on a new rental property. We’re expecting to close not he 24th, so we’ll see how that goes. It’s a commercial loan, and it operates different from residential mortgage underwriting, so we’re in the dark. Communication has been next-to-nothing. We’re currently waiting on the appraisal to come back. That was our one hurdle to getting into the house. I said once the appraisal clears, then we (as the buyer) shouldn’t have any risk in getting to closing. Therefore, we were hoping to have the house painted before we close (I would do the painting), then we could refinish the floor and get the rest of the cleaning done the weekend after closing, and get it listed for rent for April 1. I suppose I wouldn’t be trying to get to the house before Friday, so I guess I can be patient and wait to see what happens with the appraisal for a few more days (even though the appraiser was on site last Tuesday, and I’ve never had it take more than a day or two to get the paperwork).

REFINANCE FOLLOW UP, STILL

We still have an issue with the mortgage that I ended up paying 3 times for the 2/1 due date. Our refinance was difficult, and the communication continued to be difficult after closing. I asked on 2/1 whether our loans had been sold yet because I was surprised I hadn’t heard. Usually, I see a note saying to pay the new company before the first payment, thereby not paying the first payment to that “first payment notice” place that comes with the closing documents. The company’s contact said to keep paying them because they hadn’t sold the loans yet. I didn’t open the attachments in his email because I assumed he was reiterating what he said in the email. Turns out, one of the loans was already sold, and I should have paid the new company. Well, I processed a paper check to go to a completely different company (started with a C, and I didn’t catch that I selected the wrong one in bill pay). Luckily, that company sent us our check back, saying they think our loan is closed with them and they can’t process the payment (thank goodness we once had a loan with the address I put in the memo line so they could clearly make a connection and say “we don’t want this!”). When I noticed my mistake on the 14th, I sent a handwritten check that I rushed to the post office at 4:55 to get post marked. In the meantime, I found out that I was able to set up an online account with the new company even though I didn’t have the loan number yet (they gave it to me over the phone). I paid the new company online to make sure I didn’t have anything on my record claiming I didn’t pay by the 15th and it was late. I figured I’d rather manage 3 payments being made than fight the credit companies to change my credit report. Well, the initial company cashed my handwritten check, but they still haven’t sent the money to the new mortgage company. They just kept telling me they have 60 days to get it to them, and I said that’s unacceptable that they’re holding my money. That was a week ago that I was told I’d get a call back, and I haven’t heard from them.

PERSONAL EXPENSES

Now that the basement is done, I had a strong urge to finish projects. There were several things that were starting but not completed. Those final punch list items always seem to take forever. I was impressed that Mr. ODA pushed to get some of the things in the basement done right away, even though they weren’t on a critical path. However, I didn’t uphold my end of the project by painting those things, so I got back to that. I mentioned several of the projects in a recent post, and I’ve done a whole lot more since that post. But all that to say, I’ve spent a lot of money in the last month. I bought a lot of supplies to finish off these open projects. I also had big purchases of cabinet hardware, a dining room table, a desk, and a wood. We haven’t done very much out of the house, so we don’t have a lot of other expenses than these projects, which means our credit cards are actually have the usual balances. We did book an AirBnB for a trip at the end of the summer with friends of ours. That was a big hit on the credit card for a week at the beach, but they reimbursed us for their half.

SUMMARY

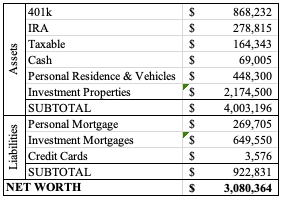

It feels like I just keep lowering the balance in our investment accounts each month, but I went to look at February 2021 to see the total. Even though some balances have decreased, we’ve still contributed to the accounts, so overall they’re $21k higher than last year, which is encouraging. I guess I should also focus on the property values raising significantly. We’re over $500k higher than last year in our assets, and our liabilities (i.e., mortgages) are about 13k less than February 2021. We’re also still over $3M on net worth, even if we’re hovering right around that. We’ll add about $50k to our net worth by the end of the month, as long as we close on the new property on time.

You hear this term in real estate often. “What are the comps?” “Have you run the comps?” It’s short-hand for “comparables.” These are the houses that are similar to the house in question (whether you’re trying to list a house for sale or purchase a new house) can be used to determine the value of a property. It’s touted as if it’s difficult, and I’ve seen several comments in a “moms” group that told me more people need to know about appraisals.

An appraisal is an expert’s estimate in the value of something. It can be something small like a piece of jewelry or something big like a house. During a closing process that includes financing, the bank issuing the loan is going to request an appraiser evaluate the property being purchased. The bank is using this as a mechanism to verify that the property is worth the contract amount.

A recent appraisal we had done stated the following (for context). This report is based on a physical analysis of the site and improvements, a locational analysis of the neighborhood and city, and an economic analysis of the market for properties such as the subject. The appraisal was developed and the report was prepared in accordance with the Uniform Standards of Professional Appraisal Practice.

If your real estate purchase is through a loan, the bank is going to require an appraisal. Have you ever looked at the appraisal? The lender is required to give you a copy.

Let’s dig into one of mine.

THE APPRAISAL

This particular appraisal was completed for a refinance of a loan. It was done in December 2021 and is 37 pages long, granted a lot of that is teaching documentation.

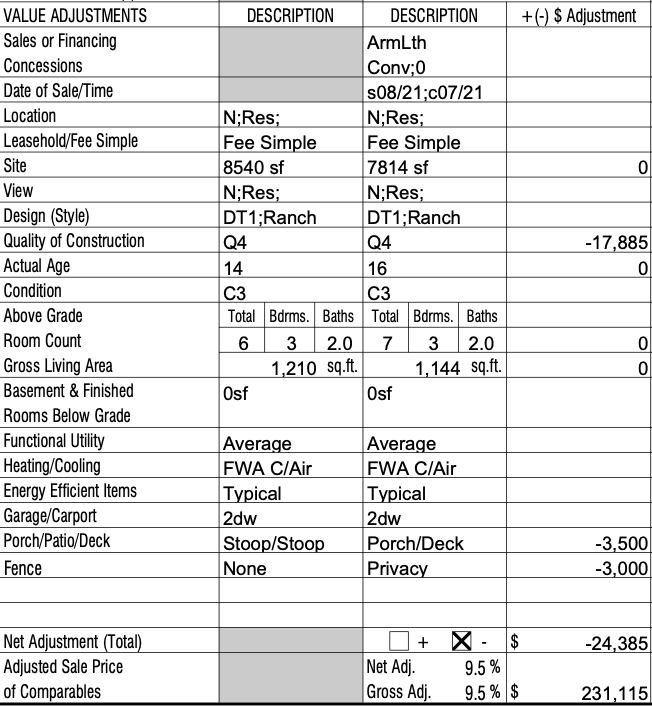

First, the appraiser identifies the property’s characteristics. Things like the address, plat number, taxes, house size and details, utility hookups, and neighborhood demographics are filled out. Here are a few snapshots with that information. All appraisal reports I’ve seen have looked like this (across multiple states).

Once the appraiser identifies the property’s details, he moves on to finding nearby homes that have sold recently. The comparable sales are of similar age, construction quality, and condition. There are formulas available to the appraiser to determine how differences between the property he’s appraising compares to the similar nearby homes. For instance, having another bedroom increases a property’s value by a certain amount, having a garage could increase the property value, having a fence affects the value, etc. Here’s a snapshot of one of the comparable sales for this appraisal. The first ‘description’ column contain the details of the house being appraised. The second ‘description’ column contains the details of the address he’s using as a comparable. Then there’s the adjustment column to identify how those differences affect the value of the home. This home being used had sold for $255,500. Each difference is calculated to account for a value of the home had it been even more similar to our house. So this house having a porch instead of a stoop is affecting the value at $3,500 (I don’t know how these values are determined, but I assume it’s all a software calculation that keeps it consistent).

This appraiser used 7 comparable sales. We’ve historically seen 3-5 houses used, but this market has created more options than usual. The appraisal was determined by removing the value of the land (since that’s calculated by the tax records regardless) and applying the average price per square foot amount to our house. The valuation came in at $230,000. We purchased the house for $117k 5 years ago, so that was a nice surprise. We were able to take out a loan for up to 60% of the appraisal’s value.

YOU CAN DO A RUDIMENTARY APPRAISAL YOURSELF

The point here is that an appraiser is using the specifications of nearby, similar real estate transactions to determine the value of the house in question. Since the concept of an appraisal is straightforward, you shouldn’t feel like you’re incapable of doing your due diligence on a purchase or determining the sale price.

It’s important to note that you’re focusing on houses that have SOLD. You’ll see houses nearby listed for sale at different prices, but that doesn’t mean that’s what the market deems a “fair market value.” You want to focus on the sold prices because that means someone was willing to pay that for that type of property, and a bank likely confirmed the value with an appraisal.

In this “moms” group I mentioned, several people told a person that she needed to hire an appraiser before listing her house. An appraiser is about $400-600. In a house sale, the buyer is responsible for the appraisal. Therefore, as the person listing the property, you’re not “ahead” in any way by paying for an appraisal up front because it wouldn’t have been your cost to bear anyway. Instead of paying someone to perform an appraisal, you look at houses nearby that sold recently.

Back in 2018, we were using sales for 6 months to a year prior to the date we were searching. The housing market hadn’t changed all that much year-to-year that you couldn’t use sales from a year ago. These days, you need to be looking at houses that have sold in the last 3 months, and maybe go back to 6 months if you don’t have any good options. If you need to use sales from a year ago these days, then assume a hefty inflation (in most areas) from the price it sold at, but it’ll at least give you a good starting point on the price.

For recent sales you dint, you’re looking for properties with the same number of bedrooms and bathrooms, approximately the same square footage, and approximately the same size yard. You’re hoping for pictures too so that you can evaluate if the condition of the property is objectively better or worse than the property you’re considering.

PERSONAL EVALUATION EXAMPLE

We’re currently on the hunt for another rental property to add to our portfolio. Things are moving fast, so we’re doing quick evaluations on the fly with best guesses of value. We have the benefit of doing several of our own real estate transactions, including plenty of searching for options outside of the ones we did purchase. Therefore, we have the knowledge to be able to eyeball the value. In the beginning, it would probably work best if you write down the details (similar to what’s found in the appraisal screenshots above) to identify the appreciable differences between your options.

We were looking at a property that was in poor condition. The listing even stated that they were offering a $3,000 flooring allowance as part of the sale, acknowledging that the condition was poor. The house is 3 bed/1 bath (colloquially referred to as ‘a 3/1,’ and was listed at 169,900. The listing photos showed a scratched up floor, but otherwise looked ok.

Not bad, right? Well, I don’t know what filter they used, but these colors are a lot more vibrant than the condition of those cabinets and appliances were in person. The photos didn’t capture the gouged walls or layers of paint that weren’t properly painted between coats. And, unlike popular HGTV shows would you have you believe, the paint color isn’t something we’re caring about. It’s a bonus if it doesn’t need a coat of paint before we rent it, but we’re generally expecting to paint a house after we buy it. The photos also don’t portray the filthy bathroom with the mismatched patchwork tiles in the shower. We stepped back and seriously considered flipping this or improving it and using it as a rental still.

I opened my Zillow app. When I’m looking for quick information, I’m focusing on price per square foot, rather than actual purchase price. This house came to $151/sqft. In the Zillow app, on the upper right corner, click ‘Filters.’ I always click ‘Reset’ before I start a new search because I never know what I last changed in the parameters. I chose the ‘Recently Sold’ toggle, left everything the same, and then at the bottom I changed ‘Sold in Last’ to ‘6 months.’ In this area, if I looked at a broader spectrum of recently sold houses, I’d have too many to look at, and the prices in 2019 would be drastically different than what’s currently happening in this market. If I still had too many results, I would have filtered down to 90 days. However, it’s January when I’m looking, so there hasn’t been too much activity in the last 3 months, and I want to capture more options that sold during the summer months.

Then I just started clicking the yellow bubbles of prices. I want to first focus on the ones closest to the house I’m looking to buy. As I get further away (or cross major roads), I’m probably looking at a different school district, or different crime levels, or different ‘feel’ of the neighborhood; be careful how far out you look.

Here are my thoughts on the first comp I found. The parentheses identify how it relates to the property I’m viewing: either it’s the same (=), my property is better (+), or my property is worse (-). It’s a 2 bed (+), 2 bath (+), with low curb appeal (+), smaller lot (+), nicer floors (-), covered deck (-), stainless appliances (-), kitchen cabinets were original and the stove’s vent hood was outdated (+), the master bathroom needs a facelift (+). This house sold in September 2021, so it’s a fairly similar market to what I’m looking in now. It sold for $117/sf. With the difference in the number of bathrooms and bedrooms, it’s hard to compare. Subjectively, the house I’m interested in is worse than this house, but it has another bedroom and a bigger lot. I decide that this comp doesn’t get me close to $151/sf for the house I’m looking at.

Comp 2 is around the block. It’s very close to the size of the house we’re evaluating (=) and is a 3/1 (=). It’s adorable, with great curb appeal, so it draws me in. Then I start noticing some things that are red flags. The roof doesn’t appear to be in bad shape, but my eyes are drawn to a water stain on the living room ceiling (+). It appears to have laminate flooring in the kitchen and carpet elsewhere, whereas the house we’re looking at has hardwood everywhere; our hardwood is beaten though, so this is hard to compare. I see that there’s old vinyl in the laundry closet that wasn’t addressed when new laminate appears to be laid, there’s some poorly laid wood flooring in just the entrance to the master bedroom, and there are several stains in the carpeted bedrooms. The backyard has power lines running through it (+); I see several issues with the vinyl siding on the house (+), but it has a covered deck (-). They had tried to sell this house from July to October, which tells me that plenty of people were drawn in, but those defects were clear (and probably more) in person. They started their listing at $166/sf and ended up selling at $146/sf. While this house looks to be in better condition than the one I’m evaluating, this tells me that I’m probably looking at the $140s/sf for the one I’m looking at.

There’s a 3rd ‘comp’ that caught my attention right behind the house I’m evaluating. Zillow claimed it was sold for $334/sf. Interesting anomaly. Our Realtor was able to pull the MLS and see it actually sold at $150k, so about $115/sf. So moving on.

I found a brick ranch around the block, so I’m excited that it’s very similar to the house I’m looking at. It’s a 3/1 (=). It sold in September 2021 for $149/sf after having first been listed at $163/sf in July. I dive into the pictures. The floor isn’t destroyed (-)! There are mismatched, yet updated, appliances in the kitchen. It’s frustrating, but they probably have a better lifespan that what’s in the house I’m looking at (-). The bathroom has been updated recently, but it’s small, and there’s no picture of the shower side of the bathroom (concern, but still better than the house I’m viewing) (-). There are minimal pictures, but at least one of every room. After comp 2 went for $146/sf, and this is better condition at $149/sf, I’m now putting the house I’m evaluating below $145/sf.

There’s a brick 3/1 next to Comp 4 that sold for $162/sf. But there are no pictures and it was for-sale-by-owner, which tells me someone probably overpaid for a higher list price because they were desperate. I’m throwing this out and not using it as a true comp.

At this point, I’m just standing there trying to evaluate whether this is worth pursuing or not. I can do detailed looks at comps later on a computer with a pad and pen. I decide that $145/sf is my highest value of this house and it’s horrible condition. However, even with that, I don’t want to go that high because of all the work that needs to be done right away on the house. The comps told me that’s the value of other homes that needed some work, but looked livable from day 1. I decided to sit on it. Well, the next day, it went under contract at a reduced price of $146/sf. I won’t know the actual price of the contract until it closes, but for now, it looks like someone bit on the $146/sf.

Now this is really important if you’re evaluating for a purchase. Do not overpay for a house. Do not feel pressured into needing it now. We’ve put in several offers on houses, but we’re not going to get into a bidding war. We also put in an offer on one house, and the seller said “raise it $5k and state the offer isn’t contingent on an appraisal, and you have a deal.” No. Requesting the appraisal clause to not be checked says we were probably overpaying even at the offer we made. So thank you to this man for letting me know that it was time to walk away.

SUMMARY

You can typically rely on your Realtor to provide you comps through the MLS. If you have questions about their valuation, ask for the details. I have an instance where I didn’t agree with my Realtor on a list price of our last personal residence. In this particular instance, I had better knowledge of the housing market where our house was than he did, because he focused on sales within the nearby city limits, and we were in the suburbs. He ran comps based on basic metrics (number of bedrooms, square footage). I had the benefit of knowing details behind some of the sales he was using or how some houses weren’t a good fit to use as a comp to the house we were selling. I was able to sway the list price to even higher than he suggested, and we were under contract that weekend.

I know how it works. I’ve taken the time to research and understand the process just enough that I can protect my finances and interests in these transactions. I’m not sharing this as an example to fight your Realtor on their suggested list price, but as a way to show you need to be an informed consumer.

Our 11th purchase was a 4 bedroom and 2 bathroom house, which we were excited about. We only had one other 4 bedroom, and it only had 1.5 baths, so this was a new demographic we could meet. We again needed a mortgage, but we were tapped out (max of 10 mortgages allowed per Fannie Mae), so we went to our partner. I went through the process of establishing the partnership in the House 10 post.

The house had been listed for sale in July 2018, dropped the price in October 2018, and we went under contract on it on December 1, 2018. We went under contract at $129,000, which meant, according to the 1% Rule, we would look to rent it for at least $1290.

The house required a lot of cosmetic work (relative to our usual purchases) before we could rent it. The biggest hold up was the carpet replacement, but we had to do a lot of cleaning and painting also. We closed on February 4, 2019; got to work on the house on the 6th; and then had it rented on March 3, 2019. That’s a longer turnaround time than we’d like, but we thought the long-term benefits of a 4/2 house would be worth it. Plus, with our goal being $1290 based on the 1% Rule, we were happy that we rented it at $1300 and through March 31, 2020.

LOAN TERMS

We were given two options from the loan officer. Both options required 25% down. We could do a 15 year mortgage at 5.05% or a 30 year mortgage at 5.375%. The 15 year mortgage payment was $865, while the 30 year was $640. Since both options required 25% down and we aren’t concerned with our monthly cash flow (as in, we’re not living off of every dollar that comes out of these houses right now), we chose the 15 year. Escrow changes over the last few years have increased the mortgage to $941, unfortunately. However, we’ve been paying off this loan with pretty substantial chunks of money thrown at it. The loan started at $96,750, and the current balance is $21,350. We would have liked to have this paid off a few months ago, but we need to time our payments with our partner, who recently paid for a wedding, renovations to a new house, and a new tear-down property adjacent to his personal residence that he’s going to build a garage-type thing (city living = street parking for him).

We went under contract at $129,000, and the house appraised at $140,000, so that was a nice surprise. The current city assessment is at $148k, but it would likely sell for more than that.

PARTNERSHIP

Since the LLC was already under way when we purchased House 10, we needed to add this one to the LLC. We contacted our attorney. He processed all the paperwork, and we showed up just to sign everything in a quick meeting. At this time, we also requested an EIN be established for the LLC. To process adding this to an established LLC, it cost us $168 (which we paid half of since we’re split 50/50 with our partner).

PREPARING TO RENT

This house was probably the second most effort we had to put in to prepare it for renting. We had to replace quite a few blinds that were broken, do a deep clean of everything, install smoke alarms, paint, replace the carpet, and do some subfloor work.

We had to paint nearly every room (one room we even painted the ceiling the same color as the walls because the ceiling was in rough shape, and it wasn’t worth the time for precision of the edges).

The floor at the front door was rotted by termites. The guys had to cut out the floor and replace the wood before the new carpet could be ordered. We needed the house treated for termites at that point since there was an active infestation that we found. Depending on time and price, I’d rather replace carpeted areas with hard surface flooring for easier maintenance. Since we were already losing time with all the maintenance on this house to get it ready to rent and it was a small area, we just went the easy way out and put new carpet in. The carpet was only in the living room and hallway; all the bedrooms have hardwood flooring.

FIRST TENANTS

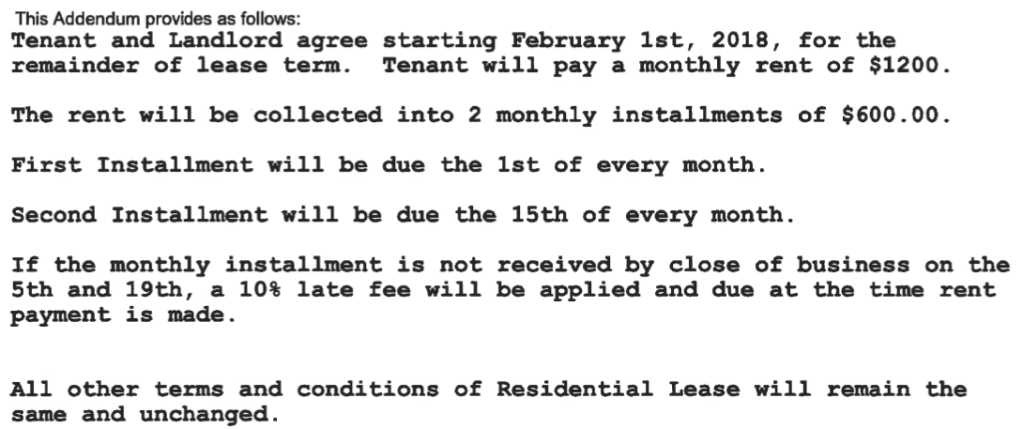

We were able to get a family in the house fairly quickly after we finished our work. We rented it at $1300. They signed it on March 3rd, and I had set the terms until March 31, 2020 (this comes into play later). The family had been renting with a roommate (and the husband’s boss!), and that guy had wanted to leave the house. In January 2020, the tenant said, “we signed the lease on March 3rd, so we want to be out at the end of February.” That’s not how leases work. The lease signed said until March 31, 2020. Some time between us telling him that he was in our lease until the end of March, not February, and the end of February actually coming, they decided they wanted to renew their lease. They signed a new lease with us on March 11 to cover 4/1/2020 through 3/31/2021.

In April 2020, the tenant received a job offer in Texas. He asked about a lease break, and we offered an option. All the communication was done via text message, so it was technically in writing, but there was never a “wrap up” text that identified all the agreed upon terms to allow for the lease break. I used this as a teaching opportunity for the 3 of us in the LLC that clearly documenting agreements in writing (preferably with signatures) is important.

The tenant offered to pay May rent without prompting, so we thought that was covered. The part that needed to be detailed was what was considered a “lease break” fee. We had agreed to 60 days worth of rent, and the security deposit couldn’t be used to pay that. Mr. ODA tried to contact the husband on multiple occasions to get rent paid at the beginning of May, but there was no response. I finally sent an email, detailing that they agreed to pay May’s rent, and that technically, they were on the hook for the entire year’s worth of the lease (quick aside: while that’s what the lease says, I think a caveat in the law actually means they’re not really liable for the whole amount because once the house is vacant for 7 days, it defaults back to our ownership, and then we have to show due diligence to re-rent it, leaving them liable for only the gap period). Well, as usual, the landlord gives us a guilt trip (their daughter was in the hospital in TX) instead of separating that from the concept of “pay your debts owed.” As a person, I feel for you on this; as a business owner, it’s not my responsibility to manage your finances and personal life.

The tenant called Mr. ODA and yelled at him. A few hours later, presumably with a more clear head, we received a fair response via text. He even apologized for yelling on the phone. He paid the last few hundreds that were owed, and we all moved on.

SECOND TENANTS

After our first tenants vacated the house, we had to get the house turned over. There was a good bit of work that needed to be done for just a year of someone living there. They had also left stuff behind that became our responsibility to get out of the house. We listed the house for rent. Our partner showed it to 3 younger people who would rent it together. They seemed great until we ran their background and credit check. They had evictions they didn’t disclose (claimed they didn’t know), so we shared the report with them and continued showing it.

We ended up showing it to a couple, and they liked it. After we accepted their application, we were able to get the lease signed on May 7, 2020. Since this was at the very beginning of the pandemic, we had to get creative. I signed this lease on a street corner (hadn’t realized that the place I had selected with outdoor seating was closed!), and they paid their first month’s rent, security deposit, and pet fee in cash that he handed to me in a sock (with a warning that told me this wasn’t the first time he handed someone cash like this haha). They’ve been great tenants, and they renewed their lease.

MAINTENANCE

The new carpeting when we first bought the house cost us $700. Between the termite treatments and other general pest control, we’ve spent $950.

Once the first tenant moved in, we learned of some other issues that weren’t apparent by us just working there and not living there. We had the plumber come out to fix several issues with the hot water that cost us $1450! Then we found out that the master bathroom shower wasn’t installed properly, and it was missing a p-trap; that cost us $325.

Our insurance carrier didn’t like that there wasn’t a handrail for the front steps of the property, so in March 2020, we had to have one installed at $190.

We had to replace the washing machine in April 2020 for about $500. As I’ve shared, we try to not include any ‘extra’ appliances because then maintenance and replacement are our responsibility. This was a fun one – we replaced it just to make the tenants happy and not deal with maintaining it, and then those tenants left right after that, and our new tenants brought their own appliances (so they just have two washers and two dryers in their kitchen).

We had an electrical issue with the master bathroom that cost us $150.

Luckily, I did the inspection over the summer, and nothing came of that initially. We did end up replacing a fan in the master bedroom because the light part of it stopped working with the switch. Since we don’t live near the house anymore, and our partner was in the middle of getting married, we went through Home Depot to have it installed, so all together (fan/light and install) it was about $175.

SUMMARY

This has been a good house. We didn’t realize that the house is located outside the city limits, so we needed to figure out trash pick up in the county (not included in the taxes). Other than a few maintenance hiccups, things have been smooth sailing. We’re happy with the tenants who are there, that they’re maintaining and cleaning the house, and we’re getting our desired rent amount (that they pay on time every month). The street is in a decently nice neighborhood with a lot of original owners, which helps it keep (and increase) its value.

There are a lot of factors that go into a home purchase. There are the simple ones, like the number of bedrooms and bathrooms your family desires. Then there are more complicated ones, like what compromises are you willing to make on your wish list to get to the price and location you want.

HOME CRITERIA

I started looking at real estate options in central KY just out of curiosity in June. I knew we wanted 4 bedrooms and at least 2 bathrooms, but it would probably be more like 2.5 bathrooms (master bathroom, kids’ bedroom bathroom, and a powder room on the first floor for guests). We knew we wanted a 2 car garage, which worked out well for us in our RVA house.

Then there’s more trivial things that I learned from experience. I preferred the master bedroom to be on the second floor with the kids bedrooms. When we built our RVA house, we didn’t think it would be too much to have the kids on a separate floor. Well, we made that decision before we had kids, and it turns out that having infants doesn’t make it easy to sleep on a separate floor. Yes, I had monitors. But kids are noisy. So once I ‘kicked’ them out of my bedroom, I didn’t want to have a monitor right next to my head to still be kept up by all their little squeaky noises through the night.

Our RVA house had a loft upstairs. It had a ‘wow’ factor to it, but it wasn’t practical. We used it as a den before we had kids, and then it was hard to keep it organized and clean once kids came around. Therefore, we put a basement on our must have list, and we weren’t going to compromise on that. We knew from our living style that a basement was going to be something we’d enjoy for a long time and didn’t want to take that off our list just yet.

We had a lot of criteria associated with the lot. We wanted about 0.25 acres. We felt that 0.5 an acre was more land than we really wanted, but anything less than 0.25 acres wasn’t going to leave enough room for multiple kids and a large dog to enjoy. We want to be in a neighborhood with several neighbors close, but we want more room than a garbage can width between the houses.

One of the sad parts of the house we were leaving behind was the backyard. We had a really nice natural area in the back half of our yard. We had put a firepit in and had a beautiful tree-scape back there, but still had a decent size grassy area for the kids and dog to play. Another downside for leaving was that the playground and pavilion (hang out space) for the HOA were two lots away.

FINANCIAL CRITERIA

When Mr. ODA and I got pre-approved for our first home back in 2012, we were approved for $750,000. Sure, we could afford that monthly payment, but then we couldn’t afford food or furniture or electricity. We had set our spending limit based on our down payment available at the time because we didn’t want to pay PMI. For this purchase, we could have afforded a monthly payment associated with a $500k house (or more), but that size house isn’t necessary for our life right now and we didn’t want to be saddled with that down payment.

I’ve already quit my job. Mr. ODA expects to quit his job in the near future. We don’t want to have him quit his job to hang out in an expensive house and never be able to do anything else because we need to pay $2,500 per month for a mortgage.

When looking at houses, we’re fluid in the cost. We preferred to stay below $400k, unless there was something we could get for more than that making it worth it (e.g., more land, more amenities). We found out that we could get everything we wanted for $350-400k, so it would have been hard for us to go higher than that.

When you’re pre-approved by a bank, they’re looking at your debt to income ratio. Your debt is categorized by your routine monthly payments (e.g., car loan). We don’t have any loans or debt payments in that sense, so they’ve set our pre-approval almost solely based on our income. This is a faulty expectation in a homeowner’s reality, since we all have fairly fixed monthly costs: cable, internet, cell phone, electricity, gas, water, etc. Then you have the cost of groceries and entertainment that may or may not be on a credit card and able to be tracked against your credit. Essentially, we don’t need a bank to tell us what we can afford, and we set our own expectations.

We know what we have for a down payment and closing costs, and we know that we’d prefer to pay $1200-1500 per month for our mortgage, which includes our escrowed real estate taxes and insurance.

OUR HOME

We got a 5 bedroom, 3 bathroom (with another bathroom roughed in for the basement), 2,750 square foot house with an unfinished basement, on about a 8,500 square foot lot. The basement is not a walk-out, which we were bummed about, but at least we have the space we wanted. The lot is slightly smaller than we set out looking for, but because our house is really wide and not deep, we actually ended up with a nice size back yard, which was really the intention of our lot size desire. Our house cost about $346k.

FINDING THE HOUSE

We looked in Lexington, KY first, and we explored resales and new construction. The neighborhood I was really interested in was sold out in one section or over $500k for a new-build in another section, so I started over. For resales in Lexington, we were looking at houses that were about 30 years old and needed updating. I really wish I had an eye for the potential in some homes. When I started investigating the new construction market, I realized that we could have a new build house for the same price as the resales that needed work. Most of the neighborhoods in Lexington have the houses on top of each other too, which we really didn’t want. We like neighbors, but we also want to be able to walk between the houses.

Through July, I tried to figure out the new construction market in the area. I thought I had a head start since we had built our house in Virginia a few years ago, but the process for these Central KY builders was much different. It was hard to stomach the fact that their build time was 11-12 months, and growing. We had built our house in Virginia in less than 4.5 months from contract signature to move in.

I looked up the different floor plans for as many builders as I could find. One builder had very large, but partitioned off, floor plans. Another builder had options available in Richmond, KY, and another builder had those options available for a year from now. I found a deal being offered by one of the builders in Richmond, KY that said “last basement lot of this section – free finished basement.”

I reached out to the listing agent. She took me on a virtual tour of the floor plan I liked, and it was by far my #1 contender. I asked her what “free finished basement” meant, and she said they’d cover the basement and finishing it. I verified several times – a $50k value??? Well, Richmond, KY wasn’t my preferred location, but hard to beat this deal. Plus, that neighborhood was just starting to be built, and we really liked being at the beginning of our last neighborhood’s build out. The listing agent put together a contract, but didn’t mention this deal. I said I wasn’t signing anything that didn’t have that in there. She added it, and then said she had to wait for her boss (the company owner) to come back to town in a couple of days to go over the details. Well, the deal was too good to be true. The deal was that we paid for the basement pour, but they paid to finish it. This deal was going on because the lot was less than favorable, so between the poor lot and less of an incentive, we walked away. That floor plan is still my favorite though, and if we ever move again, it’ll be hard not to go back to that builder. Also, they have the laundry room connected to the master closet or bathroom in their floor plans, and this is the most logical, amazing thing that I had even pointed out in our last house as something that should have been done.

Well, now I was getting desperate. How are we going to find something that we can move into? Maybe we’ll have to wait to list our house in Spring of 2021 because we’ll only find something to build that’s several months out. I’m very grateful that we found something when we did and didn’t have to wait until Spring of 2021 when housing prices have risen so much!

I had tried to get more information for a house that was under construction. We couldn’t change anything, but it was mostly ok. I didn’t love the tile in the bathrooms. The house layout was manageable, but it had a lot of wasted space (we don’t need a sitting room in the master bedroom or a formal living room). The house had a walk-out basement and was part of a neighborhood that had golf and a pool. It was also $393k. Affordable, but not what we were looking for. The lot was over 10k square feet, which is something we wanted. We asked Mr. ODA’s parents to go check it out. They went to see it and were quick to say no. I’m glad they did, and that I didn’t settle. We want our kids to ride their bikes in the driveway and street, and this house is on a greatly sloped hill (like recently rode our bikes down it, and I was scared).

I kept looking. We mostly were looking around Lexington, KY, but not within Lexington because of the lot spacing. We considered several re-sales in Winchester, Georgetown, and Richmond. They all were about $400k and not perfect, so it was hard to jump in.

At the end of July, a house popped up on my search. It was new construction and had been under contract, designed by someone that had to go with a different house because this one was significantly delayed. It was being built by the builder that had 11-12 month lead time on newly constructed homes, a builder without a good reputation, even to me, someone who didn’t grow up in the area. I requested the ‘spec list’ so I could see if there were any deal breakers in the design and selections.

I had hoped for white kitchen cabinets, and these were dark. I loved that there was a covered deck and that the already-selected upgrades to the floor plan were exactly what I would have selected (e.g., mudroom, guest suite, laundry room location, master bathroom layout). It had a pit basement. It was in the area we wanted; it was on a flat part of the road; and it could be ready before next year. The light fixtures were more eclectic than we would have chosen, but those weren’t a deal breaker.

We were told that it was probably going to be ready at the beginning of November. We figured a mid-August list on our home may take a week or 2 to get under contract, and then usually you see a 45 day close (versus our push for 25-30 days usually on rental purchases). We thought we may have a couple of weeks to bridge between selling our home and getting into the new house. Nope.

This was just as the bidding wars were really ramping up and people were losing out on 20-bid type offers on listings. Our house was under contract at the end of the first weekend. They wanted a 3 week close, and we pushed it to 4 weeks. That left 7 weeks of us being ‘homeless,’ which I covered in Part I.

SUMMARY

This is very specific to our needs and desires, but I hope that the thought process and ‘give and take’ in the decision making can be helpful to some. This information is also geared towards the Central KY market, and what you get for the price of a house in different areas of the country varies.

While we’ve had several issues with our home in the first six months, we’re happy to be in KY with family, the location of our house, and the general feel and functionality that it’s given us.

This one has been pretty easy, but we did have an interesting issue arise with the first tenant.

This is our largest house at 4 bedrooms and 1.5 bathrooms, and 1281 square feet. It’s a cape cod style house, so the upstairs has slanted ceilings, the half bath is not anything to write home about, and the HVAC struggles to work up there. The carpet on the stairs could really be replaced (but it hurts me to spend money on stairs because they’re soooo expensive compared to carpeting a room!). But the house has a huge fenced-in yard with a nice deck that’s a great selling point.

The kitchen was renovated at some point, so that’s held up well – and lets face it, who doesn’t choose baby pink knobs for their new kitchen cabinetry? But the plumbing and roof have been painful.

I’ve already told many of the stories about this house through other teaching posts, so bear with me if things sound familiar.

LOAN

The house is in Richmond, VA, and the purchase was very simple. We offered $109,000, and the seller countered with 112,500 and 2,000 in seller subsidy (i.e., closing costs), which we accepted. It was listed on June 22 at $119k, and we offered on June 25, so I’m actually surprised we got the contract agreed to so quickly.

Quick note here: after reviewing real estate contracts in NY, KY, and VA, Virginia wins. Sure there are several states that I haven’t ventured into, and this is an extremely small sample size. The paperwork is simple yet thorough, all while being in plain language. So if you’re needing a template to work off of, look up Virginia’s purchase agreement.

We settled on a 30 year conventional loan at 5.05%. We received a $200 lender credit since we closed on several properties in a short period of time. This is the house that we refinanced and received an appraisal of $168,000! We had already started with equity in the house because it appraised at $114,000 at closing.

INSURANCE

Interestingly, we couldn’t insure the house through the company that we had gone with because they have a 5 rental limit. Our agent was able to quote us through another company though, so our process appeared seamless. However, the quote was much higher than we anticipated. We went through a friend to insure it, but shortly after closing (literally a week), we were able to find an even cheaper option – that was awkward.

THE NEIGHBORHOOD

Not a category that usually gets mentioned. I discussed the neighborhood of the one house we sold already, which was because I didn’t realize it was in a higher-than-average crime area that tenants honed in on. But this neighborhood is worth mentioning.

Rentals aren’t prevalent here. In fact, many of the homes are the original owners. While working on the house when we first purchased it, the neighbor across the street approached me. He as-politely-as-possible threatened me that this is a nice neighborhood, that everyone keeps up their property, and that they don’t want any trouble. I assured him we have good standards as landlords, and we haven’t had any neighbor complaints for any of the tenants we had in our houses.

The location also comes into play for our first tenant.

TENANT #1

This house is under a property manager for 10% monthly rent.