We went on a trip to Indianapolis last month. We did more activities than we typically would have, so our spending was more than average.

The reason behind the trip was the Children’s Museum. We like visiting zoos around the country, so we used that to fill our other day there. The zoo was $91 for entry for 2 adults and 2 children, while our youngest was free. We had to pay for parking, bought lunch at the cafeteria, two kids rode the carousel, and we all rode the train; that came to $66.70 spent the day of our visit. The Children’s Museum was $90 for entry for the same group of us. It also had a carousel that we let the kids ride, I let them get a flattened penny (they used “their” $1 for it), and we bought lunch (parking in a parking garage was free); that came to an additional $35.88 spent on that day. The zoo’s meals were very reasonably priced, but the Children’s Museum’s meals were ridiculously expensive, so that free parking wasn’t exactly free.

We placed a grocery pick up order when we arrived, and that covered our breakfasts and dinners ($39.10, but we didn’t even use everything we purchased, so that’s inflated). We stopped at McDonald’s on the way there and as we left the city on the last day ($17.68). McDonald’s and Qdoba are sure fire ways to get our kids to eat and eat quickly, so they’re nice when we’re on the road.

On the first day, we went exploring the city. We had to pay to park in a parking garage, which was $5. On the last day, we did a Capitol tour and visited another museum (both of which were free), but we had to pay to park twice ($2.50).

We had booked an AirBnB for the trip. A series of events I won’t get into meant that we received a full refund from the originally booked location, had a coupon code for our inconvenience, and booked a new location right away. We ended up spending $574.32 for our lodging of 3 nights. We specifically didn’t book the cheapest place available because we wanted the comfort of multiple bedrooms for the kids. The two oldest can sleep together, but the youngest needs his own space so that it can be without a night light. We could have managed with two bedrooms because the youngest slept in the master closet, but I can never guarantee that there’s a closet big enough for a pack and play. This place had 4 bedrooms, but we didn’t use one of them. We also wanted a hot tub available, so Mr. ODA and I could hang out and watch tv after the kids went to bed. It’s an amenity we’ve grown fond of, and we even plan to purchase one for ourselves if our deck ever gets replaced.

In total, this trip cost us $922.18 (plus gas) for 3 nights away. This is a higher than normal 3-night trip for us, but we were ok with it since we hadn’t taken our usual amount of trips (newborn life). We could have planned ahead on our two big days to pack a lunch instead of buying there, but we chose the convenience of purchasing the meals over the potential savings, especially knowing that we weren’t spending anything outside the normal realm for our breakfasts (cereal) and dinners (easy, quick pasta meals). Although this wasn’t known at the time of booking, but it was once we started the activities, the concession from AirBnB more than covered our meals and extra activities on each day.

Our kids are 5, 3, and 10 months. The Children’s Museum was great for their ages. There were some exhibits for older kids that we bypassed. I thought the St Louis Science Museum was better at having interactive exhibits throughout (and is free!), but it didn’t mean that this place was bad. The zoo was nice too. There’s a lot of shade, which was appreciated on a very hot day, even in October. It felt smaller than the Cincinnati Zoo, which is where we usually go, but it was clean and the animal exhibits were nice. They had a lot of shows and “ranger talks” included with your admission too. There was a dolphin show that was included with admission that was significantly more than I would have ever expected as a free attraction!

The city of Indianapolis wasn’t great. We didn’t encounter a really nice area of the city; most of it is run down, and there was a lot of homeless downtown. It’s clear that there is a lot of updating underway, and that it’ll probably be a really cool place in a few years. I never felt unsafe, but it was noteworthy that we haven’t visited a city like this since Detroit (although we did find a nice place there, ironically).

All in all, we spent less than we originally projected. A 3 night trip where we were sufficiently entertained, but not overly exhausted (the kids got to bed on time!) for under $1000 was great.

You hear this term in real estate often. “What are the comps?” “Have you run the comps?” It’s short-hand for “comparables.” These are the houses that are similar to the house in question (whether you’re trying to list a house for sale or purchase a new house) can be used to determine the value of a property. It’s touted as if it’s difficult, and I’ve seen several comments in a “moms” group that told me more people need to know about appraisals.

An appraisal is an expert’s estimate in the value of something. It can be something small like a piece of jewelry or something big like a house. During a closing process that includes financing, the bank issuing the loan is going to request an appraiser evaluate the property being purchased. The bank is using this as a mechanism to verify that the property is worth the contract amount.

A recent appraisal we had done stated the following (for context). This report is based on a physical analysis of the site and improvements, a locational analysis of the neighborhood and city, and an economic analysis of the market for properties such as the subject. The appraisal was developed and the report was prepared in accordance with the Uniform Standards of Professional Appraisal Practice.

If your real estate purchase is through a loan, the bank is going to require an appraisal. Have you ever looked at the appraisal? The lender is required to give you a copy.

Let’s dig into one of mine.

THE APPRAISAL

This particular appraisal was completed for a refinance of a loan. It was done in December 2021 and is 37 pages long, granted a lot of that is teaching documentation.

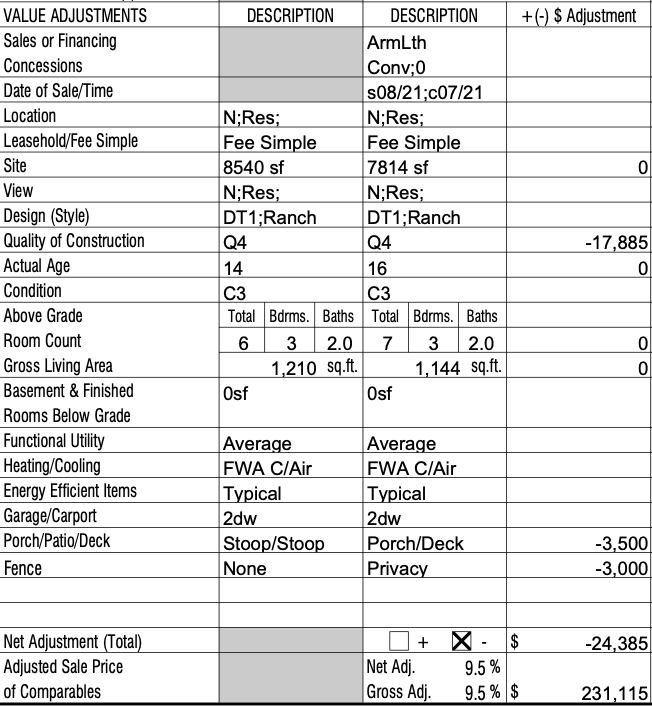

First, the appraiser identifies the property’s characteristics. Things like the address, plat number, taxes, house size and details, utility hookups, and neighborhood demographics are filled out. Here are a few snapshots with that information. All appraisal reports I’ve seen have looked like this (across multiple states).

Once the appraiser identifies the property’s details, he moves on to finding nearby homes that have sold recently. The comparable sales are of similar age, construction quality, and condition. There are formulas available to the appraiser to determine how differences between the property he’s appraising compares to the similar nearby homes. For instance, having another bedroom increases a property’s value by a certain amount, having a garage could increase the property value, having a fence affects the value, etc. Here’s a snapshot of one of the comparable sales for this appraisal. The first ‘description’ column contain the details of the house being appraised. The second ‘description’ column contains the details of the address he’s using as a comparable. Then there’s the adjustment column to identify how those differences affect the value of the home. This home being used had sold for $255,500. Each difference is calculated to account for a value of the home had it been even more similar to our house. So this house having a porch instead of a stoop is affecting the value at $3,500 (I don’t know how these values are determined, but I assume it’s all a software calculation that keeps it consistent).

This appraiser used 7 comparable sales. We’ve historically seen 3-5 houses used, but this market has created more options than usual. The appraisal was determined by removing the value of the land (since that’s calculated by the tax records regardless) and applying the average price per square foot amount to our house. The valuation came in at $230,000. We purchased the house for $117k 5 years ago, so that was a nice surprise. We were able to take out a loan for up to 60% of the appraisal’s value.

YOU CAN DO A RUDIMENTARY APPRAISAL YOURSELF

The point here is that an appraiser is using the specifications of nearby, similar real estate transactions to determine the value of the house in question. Since the concept of an appraisal is straightforward, you shouldn’t feel like you’re incapable of doing your due diligence on a purchase or determining the sale price.

It’s important to note that you’re focusing on houses that have SOLD. You’ll see houses nearby listed for sale at different prices, but that doesn’t mean that’s what the market deems a “fair market value.” You want to focus on the sold prices because that means someone was willing to pay that for that type of property, and a bank likely confirmed the value with an appraisal.

In this “moms” group I mentioned, several people told a person that she needed to hire an appraiser before listing her house. An appraiser is about $400-600. In a house sale, the buyer is responsible for the appraisal. Therefore, as the person listing the property, you’re not “ahead” in any way by paying for an appraisal up front because it wouldn’t have been your cost to bear anyway. Instead of paying someone to perform an appraisal, you look at houses nearby that sold recently.

Back in 2018, we were using sales for 6 months to a year prior to the date we were searching. The housing market hadn’t changed all that much year-to-year that you couldn’t use sales from a year ago. These days, you need to be looking at houses that have sold in the last 3 months, and maybe go back to 6 months if you don’t have any good options. If you need to use sales from a year ago these days, then assume a hefty inflation (in most areas) from the price it sold at, but it’ll at least give you a good starting point on the price.

For recent sales you dint, you’re looking for properties with the same number of bedrooms and bathrooms, approximately the same square footage, and approximately the same size yard. You’re hoping for pictures too so that you can evaluate if the condition of the property is objectively better or worse than the property you’re considering.

PERSONAL EVALUATION EXAMPLE

We’re currently on the hunt for another rental property to add to our portfolio. Things are moving fast, so we’re doing quick evaluations on the fly with best guesses of value. We have the benefit of doing several of our own real estate transactions, including plenty of searching for options outside of the ones we did purchase. Therefore, we have the knowledge to be able to eyeball the value. In the beginning, it would probably work best if you write down the details (similar to what’s found in the appraisal screenshots above) to identify the appreciable differences between your options.

We were looking at a property that was in poor condition. The listing even stated that they were offering a $3,000 flooring allowance as part of the sale, acknowledging that the condition was poor. The house is 3 bed/1 bath (colloquially referred to as ‘a 3/1,’ and was listed at 169,900. The listing photos showed a scratched up floor, but otherwise looked ok.

Not bad, right? Well, I don’t know what filter they used, but these colors are a lot more vibrant than the condition of those cabinets and appliances were in person. The photos didn’t capture the gouged walls or layers of paint that weren’t properly painted between coats. And, unlike popular HGTV shows would you have you believe, the paint color isn’t something we’re caring about. It’s a bonus if it doesn’t need a coat of paint before we rent it, but we’re generally expecting to paint a house after we buy it. The photos also don’t portray the filthy bathroom with the mismatched patchwork tiles in the shower. We stepped back and seriously considered flipping this or improving it and using it as a rental still.

I opened my Zillow app. When I’m looking for quick information, I’m focusing on price per square foot, rather than actual purchase price. This house came to $151/sqft. In the Zillow app, on the upper right corner, click ‘Filters.’ I always click ‘Reset’ before I start a new search because I never know what I last changed in the parameters. I chose the ‘Recently Sold’ toggle, left everything the same, and then at the bottom I changed ‘Sold in Last’ to ‘6 months.’ In this area, if I looked at a broader spectrum of recently sold houses, I’d have too many to look at, and the prices in 2019 would be drastically different than what’s currently happening in this market. If I still had too many results, I would have filtered down to 90 days. However, it’s January when I’m looking, so there hasn’t been too much activity in the last 3 months, and I want to capture more options that sold during the summer months.

Then I just started clicking the yellow bubbles of prices. I want to first focus on the ones closest to the house I’m looking to buy. As I get further away (or cross major roads), I’m probably looking at a different school district, or different crime levels, or different ‘feel’ of the neighborhood; be careful how far out you look.

Here are my thoughts on the first comp I found. The parentheses identify how it relates to the property I’m viewing: either it’s the same (=), my property is better (+), or my property is worse (-). It’s a 2 bed (+), 2 bath (+), with low curb appeal (+), smaller lot (+), nicer floors (-), covered deck (-), stainless appliances (-), kitchen cabinets were original and the stove’s vent hood was outdated (+), the master bathroom needs a facelift (+). This house sold in September 2021, so it’s a fairly similar market to what I’m looking in now. It sold for $117/sf. With the difference in the number of bathrooms and bedrooms, it’s hard to compare. Subjectively, the house I’m interested in is worse than this house, but it has another bedroom and a bigger lot. I decide that this comp doesn’t get me close to $151/sf for the house I’m looking at.

Comp 2 is around the block. It’s very close to the size of the house we’re evaluating (=) and is a 3/1 (=). It’s adorable, with great curb appeal, so it draws me in. Then I start noticing some things that are red flags. The roof doesn’t appear to be in bad shape, but my eyes are drawn to a water stain on the living room ceiling (+). It appears to have laminate flooring in the kitchen and carpet elsewhere, whereas the house we’re looking at has hardwood everywhere; our hardwood is beaten though, so this is hard to compare. I see that there’s old vinyl in the laundry closet that wasn’t addressed when new laminate appears to be laid, there’s some poorly laid wood flooring in just the entrance to the master bedroom, and there are several stains in the carpeted bedrooms. The backyard has power lines running through it (+); I see several issues with the vinyl siding on the house (+), but it has a covered deck (-). They had tried to sell this house from July to October, which tells me that plenty of people were drawn in, but those defects were clear (and probably more) in person. They started their listing at $166/sf and ended up selling at $146/sf. While this house looks to be in better condition than the one I’m evaluating, this tells me that I’m probably looking at the $140s/sf for the one I’m looking at.

There’s a 3rd ‘comp’ that caught my attention right behind the house I’m evaluating. Zillow claimed it was sold for $334/sf. Interesting anomaly. Our Realtor was able to pull the MLS and see it actually sold at $150k, so about $115/sf. So moving on.

I found a brick ranch around the block, so I’m excited that it’s very similar to the house I’m looking at. It’s a 3/1 (=). It sold in September 2021 for $149/sf after having first been listed at $163/sf in July. I dive into the pictures. The floor isn’t destroyed (-)! There are mismatched, yet updated, appliances in the kitchen. It’s frustrating, but they probably have a better lifespan that what’s in the house I’m looking at (-). The bathroom has been updated recently, but it’s small, and there’s no picture of the shower side of the bathroom (concern, but still better than the house I’m viewing) (-). There are minimal pictures, but at least one of every room. After comp 2 went for $146/sf, and this is better condition at $149/sf, I’m now putting the house I’m evaluating below $145/sf.

There’s a brick 3/1 next to Comp 4 that sold for $162/sf. But there are no pictures and it was for-sale-by-owner, which tells me someone probably overpaid for a higher list price because they were desperate. I’m throwing this out and not using it as a true comp.

At this point, I’m just standing there trying to evaluate whether this is worth pursuing or not. I can do detailed looks at comps later on a computer with a pad and pen. I decide that $145/sf is my highest value of this house and it’s horrible condition. However, even with that, I don’t want to go that high because of all the work that needs to be done right away on the house. The comps told me that’s the value of other homes that needed some work, but looked livable from day 1. I decided to sit on it. Well, the next day, it went under contract at a reduced price of $146/sf. I won’t know the actual price of the contract until it closes, but for now, it looks like someone bit on the $146/sf.

Now this is really important if you’re evaluating for a purchase. Do not overpay for a house. Do not feel pressured into needing it now. We’ve put in several offers on houses, but we’re not going to get into a bidding war. We also put in an offer on one house, and the seller said “raise it $5k and state the offer isn’t contingent on an appraisal, and you have a deal.” No. Requesting the appraisal clause to not be checked says we were probably overpaying even at the offer we made. So thank you to this man for letting me know that it was time to walk away.

SUMMARY

You can typically rely on your Realtor to provide you comps through the MLS. If you have questions about their valuation, ask for the details. I have an instance where I didn’t agree with my Realtor on a list price of our last personal residence. In this particular instance, I had better knowledge of the housing market where our house was than he did, because he focused on sales within the nearby city limits, and we were in the suburbs. He ran comps based on basic metrics (number of bedrooms, square footage). I had the benefit of knowing details behind some of the sales he was using or how some houses weren’t a good fit to use as a comp to the house we were selling. I was able to sway the list price to even higher than he suggested, and we were under contract that weekend.

I know how it works. I’ve taken the time to research and understand the process just enough that I can protect my finances and interests in these transactions. I’m not sharing this as an example to fight your Realtor on their suggested list price, but as a way to show you need to be an informed consumer.

There are a lot of factors that go into a home purchase. There are the simple ones, like the number of bedrooms and bathrooms your family desires. Then there are more complicated ones, like what compromises are you willing to make on your wish list to get to the price and location you want.

HOME CRITERIA

I started looking at real estate options in central KY just out of curiosity in June. I knew we wanted 4 bedrooms and at least 2 bathrooms, but it would probably be more like 2.5 bathrooms (master bathroom, kids’ bedroom bathroom, and a powder room on the first floor for guests). We knew we wanted a 2 car garage, which worked out well for us in our RVA house.

Then there’s more trivial things that I learned from experience. I preferred the master bedroom to be on the second floor with the kids bedrooms. When we built our RVA house, we didn’t think it would be too much to have the kids on a separate floor. Well, we made that decision before we had kids, and it turns out that having infants doesn’t make it easy to sleep on a separate floor. Yes, I had monitors. But kids are noisy. So once I ‘kicked’ them out of my bedroom, I didn’t want to have a monitor right next to my head to still be kept up by all their little squeaky noises through the night.

Our RVA house had a loft upstairs. It had a ‘wow’ factor to it, but it wasn’t practical. We used it as a den before we had kids, and then it was hard to keep it organized and clean once kids came around. Therefore, we put a basement on our must have list, and we weren’t going to compromise on that. We knew from our living style that a basement was going to be something we’d enjoy for a long time and didn’t want to take that off our list just yet.

We had a lot of criteria associated with the lot. We wanted about 0.25 acres. We felt that 0.5 an acre was more land than we really wanted, but anything less than 0.25 acres wasn’t going to leave enough room for multiple kids and a large dog to enjoy. We want to be in a neighborhood with several neighbors close, but we want more room than a garbage can width between the houses.

One of the sad parts of the house we were leaving behind was the backyard. We had a really nice natural area in the back half of our yard. We had put a firepit in and had a beautiful tree-scape back there, but still had a decent size grassy area for the kids and dog to play. Another downside for leaving was that the playground and pavilion (hang out space) for the HOA were two lots away.

FINANCIAL CRITERIA

When Mr. ODA and I got pre-approved for our first home back in 2012, we were approved for $750,000. Sure, we could afford that monthly payment, but then we couldn’t afford food or furniture or electricity. We had set our spending limit based on our down payment available at the time because we didn’t want to pay PMI. For this purchase, we could have afforded a monthly payment associated with a $500k house (or more), but that size house isn’t necessary for our life right now and we didn’t want to be saddled with that down payment.

I’ve already quit my job. Mr. ODA expects to quit his job in the near future. We don’t want to have him quit his job to hang out in an expensive house and never be able to do anything else because we need to pay $2,500 per month for a mortgage.

When looking at houses, we’re fluid in the cost. We preferred to stay below $400k, unless there was something we could get for more than that making it worth it (e.g., more land, more amenities). We found out that we could get everything we wanted for $350-400k, so it would have been hard for us to go higher than that.

When you’re pre-approved by a bank, they’re looking at your debt to income ratio. Your debt is categorized by your routine monthly payments (e.g., car loan). We don’t have any loans or debt payments in that sense, so they’ve set our pre-approval almost solely based on our income. This is a faulty expectation in a homeowner’s reality, since we all have fairly fixed monthly costs: cable, internet, cell phone, electricity, gas, water, etc. Then you have the cost of groceries and entertainment that may or may not be on a credit card and able to be tracked against your credit. Essentially, we don’t need a bank to tell us what we can afford, and we set our own expectations.

We know what we have for a down payment and closing costs, and we know that we’d prefer to pay $1200-1500 per month for our mortgage, which includes our escrowed real estate taxes and insurance.

OUR HOME

We got a 5 bedroom, 3 bathroom (with another bathroom roughed in for the basement), 2,750 square foot house with an unfinished basement, on about a 8,500 square foot lot. The basement is not a walk-out, which we were bummed about, but at least we have the space we wanted. The lot is slightly smaller than we set out looking for, but because our house is really wide and not deep, we actually ended up with a nice size back yard, which was really the intention of our lot size desire. Our house cost about $346k.

FINDING THE HOUSE

We looked in Lexington, KY first, and we explored resales and new construction. The neighborhood I was really interested in was sold out in one section or over $500k for a new-build in another section, so I started over. For resales in Lexington, we were looking at houses that were about 30 years old and needed updating. I really wish I had an eye for the potential in some homes. When I started investigating the new construction market, I realized that we could have a new build house for the same price as the resales that needed work. Most of the neighborhoods in Lexington have the houses on top of each other too, which we really didn’t want. We like neighbors, but we also want to be able to walk between the houses.

Through July, I tried to figure out the new construction market in the area. I thought I had a head start since we had built our house in Virginia a few years ago, but the process for these Central KY builders was much different. It was hard to stomach the fact that their build time was 11-12 months, and growing. We had built our house in Virginia in less than 4.5 months from contract signature to move in.

I looked up the different floor plans for as many builders as I could find. One builder had very large, but partitioned off, floor plans. Another builder had options available in Richmond, KY, and another builder had those options available for a year from now. I found a deal being offered by one of the builders in Richmond, KY that said “last basement lot of this section – free finished basement.”

I reached out to the listing agent. She took me on a virtual tour of the floor plan I liked, and it was by far my #1 contender. I asked her what “free finished basement” meant, and she said they’d cover the basement and finishing it. I verified several times – a $50k value??? Well, Richmond, KY wasn’t my preferred location, but hard to beat this deal. Plus, that neighborhood was just starting to be built, and we really liked being at the beginning of our last neighborhood’s build out. The listing agent put together a contract, but didn’t mention this deal. I said I wasn’t signing anything that didn’t have that in there. She added it, and then said she had to wait for her boss (the company owner) to come back to town in a couple of days to go over the details. Well, the deal was too good to be true. The deal was that we paid for the basement pour, but they paid to finish it. This deal was going on because the lot was less than favorable, so between the poor lot and less of an incentive, we walked away. That floor plan is still my favorite though, and if we ever move again, it’ll be hard not to go back to that builder. Also, they have the laundry room connected to the master closet or bathroom in their floor plans, and this is the most logical, amazing thing that I had even pointed out in our last house as something that should have been done.

Well, now I was getting desperate. How are we going to find something that we can move into? Maybe we’ll have to wait to list our house in Spring of 2021 because we’ll only find something to build that’s several months out. I’m very grateful that we found something when we did and didn’t have to wait until Spring of 2021 when housing prices have risen so much!

I had tried to get more information for a house that was under construction. We couldn’t change anything, but it was mostly ok. I didn’t love the tile in the bathrooms. The house layout was manageable, but it had a lot of wasted space (we don’t need a sitting room in the master bedroom or a formal living room). The house had a walk-out basement and was part of a neighborhood that had golf and a pool. It was also $393k. Affordable, but not what we were looking for. The lot was over 10k square feet, which is something we wanted. We asked Mr. ODA’s parents to go check it out. They went to see it and were quick to say no. I’m glad they did, and that I didn’t settle. We want our kids to ride their bikes in the driveway and street, and this house is on a greatly sloped hill (like recently rode our bikes down it, and I was scared).

I kept looking. We mostly were looking around Lexington, KY, but not within Lexington because of the lot spacing. We considered several re-sales in Winchester, Georgetown, and Richmond. They all were about $400k and not perfect, so it was hard to jump in.

At the end of July, a house popped up on my search. It was new construction and had been under contract, designed by someone that had to go with a different house because this one was significantly delayed. It was being built by the builder that had 11-12 month lead time on newly constructed homes, a builder without a good reputation, even to me, someone who didn’t grow up in the area. I requested the ‘spec list’ so I could see if there were any deal breakers in the design and selections.

I had hoped for white kitchen cabinets, and these were dark. I loved that there was a covered deck and that the already-selected upgrades to the floor plan were exactly what I would have selected (e.g., mudroom, guest suite, laundry room location, master bathroom layout). It had a pit basement. It was in the area we wanted; it was on a flat part of the road; and it could be ready before next year. The light fixtures were more eclectic than we would have chosen, but those weren’t a deal breaker.

We were told that it was probably going to be ready at the beginning of November. We figured a mid-August list on our home may take a week or 2 to get under contract, and then usually you see a 45 day close (versus our push for 25-30 days usually on rental purchases). We thought we may have a couple of weeks to bridge between selling our home and getting into the new house. Nope.

This was just as the bidding wars were really ramping up and people were losing out on 20-bid type offers on listings. Our house was under contract at the end of the first weekend. They wanted a 3 week close, and we pushed it to 4 weeks. That left 7 weeks of us being ‘homeless,’ which I covered in Part I.

SUMMARY

This is very specific to our needs and desires, but I hope that the thought process and ‘give and take’ in the decision making can be helpful to some. This information is also geared towards the Central KY market, and what you get for the price of a house in different areas of the country varies.

While we’ve had several issues with our home in the first six months, we’re happy to be in KY with family, the location of our house, and the general feel and functionality that it’s given us.