Last month, I mentioned that there would be a lot of rental property expenses and bills being paid this month. Well, they will hit in November, but they don’t hit until the end of the month. I scheduled all the payments to be made right after our current credit card cycle closes, which is around the 20th of the month for most of our credit cards.

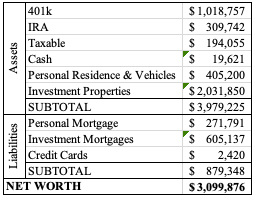

I had to update our 401k numbers with more recent data (usually the data I’m using is a couple of weeks old since updating those accounts involves an unnecessary amount verifications). I also updated one of the balances on our mortgages (one with a partner that I don’t have access to the account to see regular updates).

I’ve been working the second half of October and a few days in November, which has kept our spending low. This month I have the last of my Christmas shopping to do (hopeful for deals on Black Friday for items already in my cart!) and several insurance payments that will cause our credit cards to increase more than usual, but we’ll stay on top of paying them off.

We have yet to receive September, October, and November rent from one of our tenants (more information in the next post in a few days). Otherwise, everyone is paid up on rent, and we even had a tenant pay part of December’s rent!

We had several reimbursements come through this month that increased our cash on hand. Mr. ODA purchased things for our HOA on his credit card, so that was reimbursed. We had issues with our escrows and insurance payments, so the overages were reimbursed to us. I also worked, serving beer, in October, which increased our cash balance more than usual.

There are a few line items that were changed significantly because I wasn’t working with clear data the past few months. We may have hit $3 million net worth before this update, but I know that it’s official now! At 35 and 34, that’s a fun accomplishment. It doesn’t feel like we have money to throw around, and we certainly don’t live lavishly. You can see that $2 million of this is tied up in the appraisal value of homes we own, and most of the other parts of this is tied up in accounts that we can’t access until retirement. We still make decisions for the longevity of our net worth because, well let’s face it, we’re only in our mid-30s and there’s a lot of life to live.