It’s been a while since I’ve talked about the credit cards we have and how we manage using them. I seem to be caught in multiple conversations around me lately about how people feel credit cards are bad, so they use debit cards. I understand that some people have a bad history where they weren’t disciplined enough, but don’t you think after several years, you’re older and wiser and could likely teach yourself discipline? My last post was about how you could make $500 in a year just by putting an expense on a credit card and paying it off each month if you have 2% cash back. So let’s dive in to what we made in 2025. There is one caveat: we have a lot of credit cards and we put a lot of effort into using the categories; I fully understand this is more effort than nearly anyone else is willing to put in. But hopefully you can take just one thing away from this teaching and information.

You need to find your why. Your why is your driving factor on everything. Put things in perspective of “if I hadn’t spent $10 on that coffee, what could that have gone towards to provide me with longer term satisfaction?” I admit that I’ll go to Starbucks for a drink, but I buy about 5 of those $6 drinks (I get a very basic thing) in a year.

INTEREST EARNED: $1,191.42

The easiest way to make your money work for you is through interest on a bank balance. Currently, savings rates are hovering around 3.25%. I’ll just jump right into it: compound interest. Even if you have $500 extra, put this money in a savings account. At this interest rate, you’re earning $16 in a year, but that’s $16 more than you had at the beginning of the year. The mentality that $16 isn’t “worth it” is the type of thought process you need to move away from. If that balance was $5000 instead of $500, then that’s $162 in passive income.

TREASURY DIRECT: $2,098.14

This is more advanced interest income. You can create an account here and invest your money in short term securities (think CD type things at a bank). The rate is currently about 6.25%. You’re tying your money up for a period of time (4 weeks through 30 years), and the rate is tied to the term of investment, but we are actively managing our investments in 4-8 weeks segments, earning about $50 at a time.

CREDIT CARD REWARDS: $1,947.75

We have several credit cards. Some are a flat percentage for all purchases, and some have categories that earn an additional percentage back. The amount that I have here is only related to what we cashed out. More was earned, but we keep some in our Chase account balance so that we can get a bonus if we book travel through their portal.

If you don’t want to manage categories, go for the Citi Double Cash card. It gives you 1% on a purchase and 1% on a payment. The key here is that you can’t claim a statement credit because that doesn’t count as a payment, meaning you don’t get your 1% on that amount.

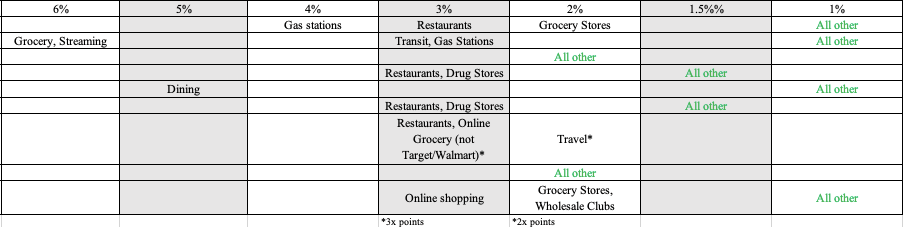

Without giving too much away on the cards we have, here’s a snapshot that I keep in my phone to remind myself what card to use for each purchase. The 5% category there changes quarterly. Usually, if I can’t use my Citi card, then I’m checking this graphic to see what the next best percent back for “everyday purchases” would be.

SUMMARY

This is “passive” income we’ve made. We had other avenues that brought in other income, but this is where we basically just spent money or kept money in certain accounts and brought in an extra $5,237.31. That’s a big number, and I’m sure that type of money can make a difference in your life or pay for a trip you want to go on.