We bought a hot tub! It’s something that we’ve been talking about for almost a year, went looking at in May, and then finally ordered it last month. It was delivered and set up this week.

RENTALS

We replaced the roof on one of the houses. I go into that a little more in the ‘insurance’ section, but that was a $6,300 payment that was made.

INSURANCE

The fact that I have a separate category to cover my insurance efforts is just frustrating.

Last month, I complained that we were threatened with our liability policy being dropped because we didn’t provide the necessary documentation … that. we. were. never. asked. for. So I dropped everything and got the documentation as fast as I could, while being praised for my organization and response time as usual. Then a few weeks later, I was told that our policy has expired because they couldn’t get to our documentation review fast enough. Awesome. I love the one way street. We were finally informed that everything was reviewed and our policy was reinstated with no lapse in coverage. I paid that policy.

During that process, we were informed that one of our policy providers does not qualify to be covered under our liability policy because their company rating fell below A. Ironically, we had already pulled all but this one policy from this company. We requested a quote from another agent, but she said they couldn’t write a policy on the account at this time. It’s frustrating to me that once you file claims on your insurance (which it’s there for), you’re blacklisted. There were no claims for 8 years of rental properties and 12 years of homeownership, but that doesn’t matter. Since 3/4 of our claims in the last year are all in the same location … all those houses were hit by the same wind storms to cause damage. I certainly didn’t request trees to fall on two houses. Add in that the damage to our house was severe, making our policy pay out high for the last year, so getting new insurance policies where necessary (and on houses with no claims) has been difficult. There’s nothing to say we can’t keep this policy on this house even though the rating declined (which I would have never even known about), so we’re not stressing about it.

One of the wind damaged houses with a claim caused that company to drop us. That’s fine. I have been working on this replacement since September 23rd and finally got everything squared away on October 31st. One of the frustrations on that was that I’d ask multiple questions, and this guy would either not respond to an email or respond to half of it. One of my complaints was that my original request was for $500k of liability coverage (which is higher than offered on most policies I’ve had written, but is the minimum required for our liability policy), but he wrote it at $1 million. I asked for it to be lowered no less than 4 times. He finally responded when I got stern and called out the lack of action; he said that since it’s only about $25-30, they just go ahead and do it. I finally said (again) that I have liability policies that give me extra coverage, so I don’t want my individual ones to give extra coverage “just because,” and that it’s up to me to decide whether that $30 is worth it. He finally reduced it. The new policies are $510 more than the policy we were covered with that got dropped.

Oh – the original policy that we got dropped from included two houses. It wasn’t clear whether the company was dropping both houses, but I went ahead and switched both. I was hoping that the new policies would be written like all my other houses – individually. Unfortunately, it’s under one company and they handle things the same way, so both houses are tied together under one policy number again. I have multiple houses covered by Travelers, and they’re each on their own policy. I don’t understand why these houses get lumped together.

Another house of ours was given “high risk” insurance because of our roof condition. Our partner didn’t tell us about the transfer of insurance or the reason why. I discovered it when I received weird paperwork for our liability policy (which, ironically, now that I think of it, my liability coverage didn’t call out as odd, but they weren’t happy about that company getting downgraded…hmm). I discovered this on September 6th. I started getting quotes for roofers immediately, but that process took forever. I finally got the roof replaced on October 18th, and then I requested her to find us new insurance on October 31st. We have a new policy being issued effective November 15th, which will cancel the higher insurance. The total savings equates to about $450, but it’s still over $300 more expensive than the original one that we walked away from.

TAXES

Central KY taxes were due this past month. I paid 4 houses worth of taxes. 3 were cashed immediately. I pay via online bill pay, where they send the check on my behalf, instead of online because there are fees associated with that. Well, now one of them is floating out there without my knowing what to do next. There’s a 2% discount if you pay before 11/2, and that check didn’t get cashed by that deadline. So now I have to make phone calls to track down why the check I sent via bill pay didn’t arrive, even though another one arrived just fine. I also have a city that I have to pay a small amount of taxes to, and I’m waiting for those two checks to cash as well.

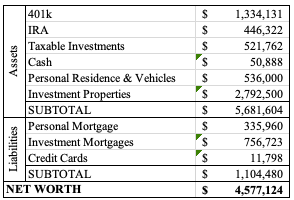

NET WORTH

Our net worth is almost $100k over last month’s. Not reflected in the credit card yet is the payment for the hot tub that just happened this week. By next month’s update, I’ll have to pay off the 0% interest credit card, so the total credit card number probably won’t change drastically.