An amortization schedule is a document that is a huge spreadsheet of numbers that tells banks and their software how to apply your monthly mortgage payment. It defines the amount of each payment going to principal to pay off the loan balance, and the amount going to interest for the bank allowing you to borrow their money.

Let’s rewind. How does the bank figure out how much your monthly principal and interest payment is going to be? This is a function of several things:

- Loan amount (purchase price minus down payment)

- Interest rate

- Loan term (length)

Want to see a formula for that?

- loan amount = x

- interest rate = y

- loan term (months) = z

Looks like a blast doesn’t it? I saved this formula into my spreadsheet for evaluating properties so that once I fill in the purchase price, expected down payment, loan length, and the predicted rate from my lender, it will auto-populate the monthly mortgage payment amount. I then take that number and can calculate predicted cash flow based on a rent estimate.

Back to the point of the post. Loans with long terms borrow the money for a long time. Loans with high rates borrow the money more expensively. In both cases, the early stages of the amortization schedule give much more money to the bank as your fee for borrowing (interest) than they do to pay down the loan. This is because every dollar of that loan principal is being borrowed and needs paid for.

In the first payment, the entire principal amount borrowed is in that formula above, so it’s expensive to the bank to give you that money. Fast forward 15 years of a 30 year loan and you have far less outstanding principal left, so the interest charge associated with that is less. Since your total monthly mortgage payment (principal and interest, ignoring escrows) total doesn’t change, the interest applied towards a smaller balance leaves more ‘room’ to pay toward more principal. Basically, the bank gets its money out of your monthly payment first, and what is left over can go to principal pay-down.

DAILY INTEREST

To better explain the cost of borrowing each dollar over time, it’s likely easier to break it down into daily interest. An amortization schedule calculates the cost to the borrower for giving you the bank’s money on a per day basis. So while I have access to $X for the whole month, I owe the bank for every day I’m carrying that principal. Multiply by 30 and that’s what the bank charges me for interest for the month. Then, remember that the leftover is what goes to the principal pay-down.

How to calculate. Divide your annual interest rate by 365 to get your daily interest rate. Multiply that rate by the outstanding principal to get your daily interest charge. Multiply that by the days in the month (or most banks use a standard month length = 365/12) and come up with the interest the amortization schedule charges you for that month’s payment.

We mentioned the different types of amortization we’ve seen in the House 1 post. This loan calculated your monthly principal part of the payment by the exact number of days in the month so each month’s proportion of principal to interest varied up and down. This is in contrast to what most banks do that I mention above.

THEORETICAL EXAMPLES

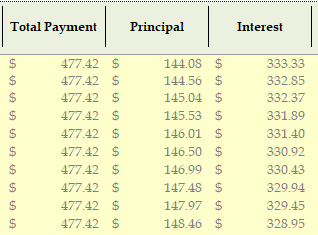

A pretty standard rate in the last decade is 4% on a 30 year fixed mortgage. Lets say the loan amount is $100k. Plugging that into my formula above, we get a monthly payment of $477.42. Above are the first 10 payments on that loan. Only about 30% of your monthly payment is actually paying down principal at the beginning. It takes 153 payments (i.e., months) before the amount of each payment going to principal is actually more than paying interest. Total interest on the full loan in this scenario is $71,869.

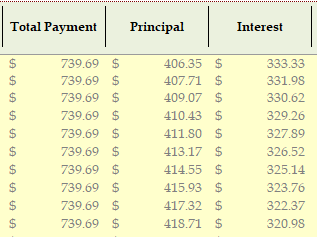

Now lets look what happens when we change it to a 15 year loan. The total payment jumps to $739.69 because you are paying the principal down twice as fast. But, the first payment you make is already $406.35 worth of principal pay down. Compare it to the first loan example in the terms of daily interest. The rate is the same. The amount is the same. So the interest due for the month is the same. But because your amortization schedule knows that you’re paying the loan off much earlier and requires a larger total payment, the leftover for principal pay-down is far more substantial.

Next, look how much quicker the interest charge drops after just 10 payments compared to the first example. $320.98 vs $328.95. This is because you are paying principal down more quickly, so the outstanding balance decreases and the daily interest is then lower too. Total interest in this scenario is $33,143.

In this example, we move back to a 30 year loan, still at $100,000, but we bumped the rate to 6%. The total payment rises to nearly $600, and the principal to interest ratio of the beginning payments is quite poor. Only 17% of the payment is going to principal pay down, which means that the daily interest is high, and stays high for many months. It’s not until month 223 (18 years later!) before the amount of principal in each payment is higher than the interest payment. Total interest in this scenario is $115,838.

Side story – Mr. ODA’s parents paid off their 30 year mortgage on their residence in 12 years. As a child, Dad would explain to me their process. They printed out the amortization schedule and put it on the fridge. Each month, based on their regular cash flow of life, they would choose ‘how many months’ they wanted to pay to the loan. So they’d make their regular payment, then they’d pay the principal portion of the next 2-3 months on the amortization schedule also. They’d make some really gnarly extra payments with weird dollars and cents, but it was a calculated decision. Then they’d cross those months off the schedule, knowing that with that extra payment, the interest that was tied to that principal portion on the schedule was simply avoided/canceled, by paying that principal early. This was a powerful tool to help me understand how the loan process worked, and one that help create the foundation for me to look at time value of money, opportunity cost, guaranteed return vs potential invested return, etc. Dad missed a lot of stock market gains by accelerating a 30 year mortgage to 12 years, but very few people ever regret owning the roof over their head free and clear – with a byproduct of NO MORTGAGE PAYMENTS for the 18 years that would’ve been remaining! Now he can make more investments with that leftover cash flow of life.

Amortization schedules are one of the largest “gaps” in understanding for the typical mortgage customer. They typically get told what to pay each month and ascribe to a “set it and forget” mantra that they know in 30 years, their house will be owned free and clear. Anytime before that, why bother understanding the background math?

As you can see in the examples, a shorter loan means faster pay down with less interest overall, and a lower interest rate means a smaller payment. When looking at loan options, understanding how the math operates to get to your options can help you determine what your priorities and goals are, and how to execute them.

In our recent refinancing post we talked about analyzing when was a good time to refinance our existing loans and which ones we’d target first. Simple advice you can find on the internet is that it’s a good idea to refinance if you plan to keep the property for longer than the result of closing costs divided by monthly payment. Most times this was about 2 years for us. You can see above that the 6% example had a $123 larger monthly payment than the 4% example (30 year term). So if closing costs are $2,000, it would only take 16 months (2000/123=16) to “break even” on a refi to go from a 6% loan to a 4% loan. No brainer!

There’s another hidden benefit there too, that gets missed to make it even shorter than 16 months. Look at the principal portion of the monthly payment. On the 6% example, it’s only $99 on payment 1, but on the 4% example it’s $144. That’s another $45 benefit! You’re paying down the principal at a faster rate. Add that extra principal portion embedded within the monthly payment to the $123 lower payment savings ($123+45=$168) and you get a “break even” point of only 12 months ($2000 closing costs/$168=11.9)!

Understand how your mortgage math works so that you can speak intelligently to a lender, ask good questions, and set yourself up with the best scenario for your finances and your future.

Hmm it appears like your blog ate my first comment (it was

extremely long) so I guess I’ll just sum it up what

I wrote and say, I’m thoroughly enjoying your blog.

I as well am an aspiring blog blogger but I’m still new to everything.

Do you have any recommendations for beginner blog writers?

I’d genuinely appreciate it.

LikeLike