In January, I mentioned how I have a very detailed spreadsheet to track my expenses. I started this spreadsheet concept in 2012 when my husband and I started combining living expenses. We also moved from NY to PA to a VA apartment to a VA house in a matter of 22 months. I needed to have a way to make sure I didn’t miss any bills. I didn’t want to rely on receiving the bill itself in the mail or in my email before paying it. I chose to develop the spreadsheet based on our pay check dates, which were every 2 weeks.

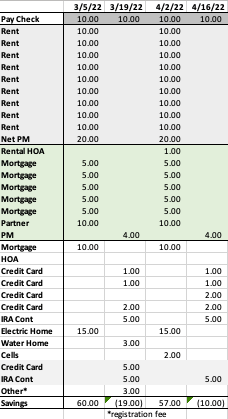

Here’s my sheet, in essence. Pay no attention to the actual numbers in this screenshot, as I didn’t take the time to make sure they were made up but still proportioned to each other. The format is exactly as I use it though. I set it up at the beginning of each year.

For the entire year, I record the pay check receipt across the top of the sheet. The dates are based on the day the money hits our account. This has changed over the years, as we used to get paid on Tuesdays, but now Mr. ODA’s pay check shows up in our account on a Saturday.

The first section, which is all gray, is the rental income. I then record all the rental income near the 1st of the month. If a pay check isn’t near the first of the month, I record it for any pay check date that shows up in the first 10 days of the month. Realistically, I receive the majority of our rent on the 5th of each month, so it doesn’t make sense to record it as a projection any earlier than the 1st, and as near the 5th as I can. The ‘Net PM’ is because I don’t collect rent on our KY houses; the property manager collects rent, removes their expenses, and then we receive the net by the 10th of the following month.

The next section is the light green, which captures routine expenses on the rental properties. I record the HOA due date every 3 months, each month’s mortgage payment, the payout to our partner (I take in all the rent each month and then pay him out his half plus our half of the mortgage payment), and then the VA property manager’s expenses.

The white section covers all our personal expenses.

– The bottom two gray lines are simply an indication to me that those affect Mr. ODA’s account and not our main checking account.

– I pay our personal mortgage near the 1st of the month (some time between the 1st and the 10th, but I typically prioritize this getting paid as close to the 1st as possible).

– Our personal residence’s HOA is only due one per year, which is why there’s nothing on that line for this particular snapshot.

– Then I have all our credit card payments. For the year, I project based on the previous year’s average bill. As I get closer to the statement end period, I update the projection. If I project that a credit card bill is going to be $1000, but as we spend through the month, we had more expenses than I thought, I update the projection on the spreadsheet to reflect that. So where it said $1000, I may put $1700 to cover my savings projection.

– I project our my utilities too. I know that I have an electric and water bill each month, and I have a cell phone bill that I pay in 3-month increments to my sister-in-law for a family plan. When setting up the sheet for the year, I simply keep the same numbers from last year for the utility lines. While I can log into my account and see the details, it’s easier if I already have it laid out like this. Then I can see, “last year, for this month, my bill was only $40; why is it $70 now?” One caveat here is that I usually keep the lines on this sheet to those items that are going in or coming out of our checking accounts. The water bill can now be paid by credit card (since we moved to KY last year). Technically, I should remove that from the sheet because I track bill due dates separately from this part of the sheet, but since I’m used to tracking the water bill’s due date like this, and I like seeing how the bill changes from last year’s amount due, I’ve kept it on the list.

– I have our IRA contributions listed as well, since that’s a big chunk that comes out each month. The maximum contribution into a Roth IRA is $6,000. We have automatic contributions twice per month, so that’s actually $500 out of each ‘pay check’ grouping.

– The “other” line is for expenses that happen every year, but they aren’t worth having individual lines because there’s only one or two payments per year. As I type that, perhaps my own HOA payment could be added to the other line since it’s only paid once per year. In Virginia, we had personal property tax that would be due each year. We also have our taxes that we owe (because we purposely plan our taxes so that we don’t get a refund because that means you’ve given Uncle Sam an interest free loan). We have vehicle registration fees due. All these ‘one off’ payments are recorded on the “other” line and then I describe the expense two lines below with the asterisk.

As for the savings projection, this is probably mislabeled. It has always said ‘savings,’ but it’s really just the net of that two-week period’s income and expenses. To know if I’m in good shape (if perhaps I’m in a position where my account balance is being kept really low), I net the two ‘savings’ next to each other (so I would add the $60 and the -$19 to know that my income from that first two-week period will cover my expenses for the second two-week period also).

In practice, as I receive the income or I pay a bill, I change the text from black to gray. This tells me that it’s paid and accounted for. I also update to actuals as I go. So if I projected a credit card payment to be $150, but the actual payment was $147.34, that’s what gets put in the sheet when I make the payment. This helps me track actual amounts through the year, as well as sets myself up to create projections for the next year.

I have a separate tab in my workbook that tracks additional income for the year. For example, when I was working part time, I recorded that income on that other spreadsheet. Each time we get money from our credit card rewards, it gets recorded on my income spreadsheet. By keeping track of our additional, unplanned, income, I have the ability to identify our actual savings net for the year. I take the ‘savings’ bottom line from this spreadsheet and add all the additional income we’ve brought in from the other sheet.

While I’m not budgeting the details of our expense categories (e.g., $300 per month for groceries), I’m tracking my income and overall expenses based on bill payments. Last year, I had tracked my expenses by category to see if overspend in one area in particular. I didn’t keep up with it though because the billing cycles didn’t line up with when I’d be running my financial update, but I hope to get in a better grove this year. This set up makes me feel comfortable that I’m not missing a bill. If I get to the end of a 2-week period, and I haven’t grayed out an amount, then I know it’s time to investigate why I didn’t receive mail or an email prompting me to pay a bill. Usually what happens is I’m tracking Mr. ODA’s credit card payment and wondering how much longer he’s going to wait to pay it until the due date. 😛

I hope that was easy to follow. I don’t want to put all our exact numbers in there, but I wanted to share how I “budget.” If you have any questions, don’t hesitate to reach out!