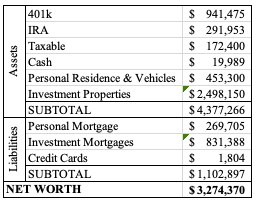

The market has recovered a good bit, so our net worth jumped. Our retirement accounts were at an intriguing low, but they’re back on track now. We also saw a few sales in the neighborhoods where our rentals are, so that increased our net worth based on the comps. We added a new property over the course of the last month as well.

NEW HOUSE IN OUR PORTFOLIO

We closed on a new house on March 24th. We worked on it for a few days, I held an open house, and we were able to get it rented as of April 8th. We had 16 days of vacancy. While showing it, most people were looking for a May or June start date, so we were lucky someone qualified for an April date. Back in 2016-2019, we were looking to follow the “1% Rule.” That means that if you buy a house for $100,000, your goal is to set rent at least $1,000 per month. This house isn’t even close. This market doesn’t allow for such a goal anymore because housing prices are soaring. The next goal would be to list for about $1/square foot. This house is 2100 square feet, but since the upstairs has smallish rooms and the basement is all open, we thought it wasn’t really worth pushing for $1/sf.

We bought it for $240k net, and ended up renting it at $1750. I wanted $1800, Mr. ODA wanted $1695, and when I went to list it, Zillow suggested $1750, so we went with that. Multiple people commented on how they appreciated the price, so we may have been able to get $1800 without an issue. I’m happy to have it rented, and I think these people are going to take good care of the house.

RENTALS

We put more money towards the house that we’ve been paying off, which is owned with a partner. We put our half towards it ($8,500), and it has a balance of about $600 now. The pay off quote required us to pay the anticipated taxes that will be paid out of escrow in May. We didn’t appreciate that, so we just went ahead and paid it down. We’ll let the May mortgage payment go through, wait for the taxes to get paid out of escrow in mid-May, and then pay it off. That’ll make 7 houses that are owned outright! But that also means I need to stay on top of insurance and tax payments.

We were just informed that one of our properties in Lexington that’s under a property manager hasn’t paid rent. She said it’s unlike them and that they aren’t even responding. She’s going to go to the house tomorrow to check on the situation. Since we’re paid a month after rent is received, this hasn’t affected us. A neighbor reported that they were moving out last month, but the tenant denied it. Perhaps they abandoned the property.

Once again, our two usual suspects didn’t pay rent on time. However, both of them actually made a better effort than they have been. One has paid this month’s rent in full, but has a balance of $286.31 (seriously…) to make up several late fees. I’m happy to waive late fees when it’s someone who communicates and isn’t always a fight to collect rent, but I’m holding this one to the balance owed. Another one told me that they wouldn’t pay until the last Friday of the month. I drafted an email to tell them that this is unacceptable because it’s been several months that they’re paying this late, and we need to work towards getting back to paying rent at the beginning of the month. Right after I drafted that, she sent half of this month’s rent. Better than nothing!

SPENDING CHANGES

Over the past month, we didn’t go out to restaurants very much. We haven’t been traveling because my family came into town for our daughter’s birthday party, and then I’ve been working on the weekend. Most of our spending went to gas (going back and forth to Lexington (half hour drive) multiple times per week!) and expenses to get the new house ready for a tenant.

I’m flying to my sister’s baby shower next month, so that another large and unusual expense on our credit cards ($250).

SUMMARY

We still have our state taxes to get paid. We went through the process of entering all our taxes, but we haven’t hit submit just yet. Surprisingly, we’re expecting a refund from the Federal side. The amount owed and the refund basically end up as a wash.

Our new property’s loan is a commercial loan, so it doesn’t get paid on the typical mortgage schedule, but on the 1 month anniversary of the opening. Therefore, the next payment is due on 4/24, and there’s no “1 month without a payment” type thing.

Clearly, our cash balance dropped significantly since last month because we had the closing. That was about $46k that we wired out, which was the expectation when we completed all the maneuvering with the cash out refinances in January. Our credit cards reflect our lower spending too, coming in about half what the balances were last month.