RENTAL PROPERTIES

We paid $2,850 in extra principal towards the main mortgage we’re paying down, leaving that mortgage with a balance of $5,500. We had a $4k flooring purchase on another house that has set our pay off timeline a few weeks back, but we’ll still have that mortgage paid off in the next couple of months. We have a rental property that we purchased in 2016 that has flooring that’s at least that old. The carpet has long passed its useful life, and the linoleum in the kitchen and laundry room has started to peel up at the seam. Typically, we wouldn’t want to replace flooring while a tenant still lives there, but they’ve lived with this for almost a year, and they’ve been our tenants since we purchased the house. As a means of keeping the tenant happy, we agreed to replace the flooring in all the rooms except the bathrooms.

We had two of our tenants not pay rent by the 5th, as required by the lease. They’re the two that are typically late, and they’re typically not up front with telling us about it. We’ve said several times that we’re really flexible landlords, but we can’t be flexible if we’re not told what is happening. With one tenant, who had just recently irked us with a plumbing issue and being incommunicado, we didn’t even reach out for information. We’ve had enough of their antics and having to chase them for rent. So I simply sent them their notice of default letter, outlining all their rights as tenants as now required under COVID-related procedures. I received an email letting me know that they’d pay on the 7th. I love their nonchalant response, like they hold the power and will pay whenever they feel like it (hmm). For the other tenant that was late, she texted to say she’d be late with the payment on the 7th, and then on the 7th only paid part of the rent due. She said she was in a car accident and there was an issue with her sick leave pay out, but she’d get it to us when it got fixed. She resolved it on the 12th, although still without the late fee.

We were able to get the invoice on the HVAC replacement for one property, which meant we paid our partner the $3,288 we owed him, on top of his usual $2,167 that we pay out for him to pay the mortgages and then his share of the profits (since I manage all the rent collections).

OUR SPENDING

Our credit card balances are high for several reasons. The $4k flooring purchase; as well as the insurance for one of our properties that isn’t escrowed because we paid off that mortgage, which was $436; an expensive gift purchase that isn’t transparent in the cash and credit line items because that cost was split 3 ways (i.e., we received 2/3 of that cost back in cash, but it’s still reflect in the credit line); and our travel.

We booked a camp site for the end of the month that required payment up front. We just got back from a trip, which increased our spending. But I’ll note that when we travel, we’re not eating expensive meals. Our interest is in the experiences and activities, rather than exploring sit down local restaurants. Our food for 5 days cost us $161 as a family of 4. We also ended up only paying for 2 of the 4 nights in the hotel because the air conditioning was broken, even after they came to ‘fix’ it, and then, when I was checking under the bed to see if any toys or socks got left behind as we were leaving, I found a large, dead roach. We didn’t ask for any comps; one was automatically reflected in my final invoice without my prompting, and then when the manager was speaking to Mr. ODA about his stay, he volunteered removing another night.

We opened a new credit card to take advantage of the bonuses since we knew we’d have this travel and the flooring cost to meet the $4,000 spending threshold for their bonus. This credit card has an annual fee of $95 and no 0% interest period, which goes against our norm when looking to open a new credit card. However, the bonus can be transferred to our Chase Rewards Portal, where we can use it to book travel at 50% the cost. We also received a $50 grocery credit.

ROUTINE UPDATES

- My husband and I cashed in the last of his savings bonds that we got as children, so that was an extra $735 that we brought it that wasn’t planned.

- We paid about $6,074 for our regular mortgage payments. Several of our properties had mortgage increases due to escrow shortages. I haven’t figured out which I dislike more: planning for tax and insurance payments, or the large escrow increases that seem to happen year after year. I think it’s the escrow though.

- Every month, $1100 is automatically invested between each of our Roth IRAs and each child’s investment accounts. I should also note that I don’t speak to other investments because they happen before take-home pay, but my husband maxes out his TSP (401k) each year as well, which I had also done when I was employed.

- Our grocery shopping cost us $700. Honestly, I don’t even know how to explain that cost jump. I think it’s because my husband shopped some deals at Kroger and Costco, so we stocked up on some things that aren’t part of our routine purchasing.

- We spent $200 on gas. Two trips to Cincinnati, our trip to Atlanta, and then more-than-usual trips around town.

- $400 went towards utilities. It’s higher than last month because we paid 3 months of our cell phones, which gets us back on quarterly billing as a family. Utilities include internet, cell phones, water, sewer, trash, electric, and investment property sewer charges that are billed to the owner and not the tenant. We still haven’t sought reimbursement from the builder on our electric bill, but this month’s bill was even less than the last month’s.

- Our entertainment costs included baseball game tickets for our trip as well as two games later this summer, parking for the games this past weekend, a new shirt for our son, activities for the kids, and the hotel. This past month, we spent $650 on things I’d classify as entertainment related. I also included boarding for our dog ($100) in this total.

- Speaking of our dog, he had his annual appointment (shots and the year’s worth of preventative medicines), and that cost us $500.

- We spent $292 eating at restaurants and ordering take out. We utilized a Door Dash credit on one of our Chase credit cards, which was about $30.

- But! I killed it with running errands this month and actually returning things that needed to be returned. I returned $150 worth of items one day!

- We paid our State taxes during this period too. Between two states, that was $954. Also, anecdotally, I’ll share that we spent $6.40 to mail our Virginia tax return. We processed our taxes through Credit Karma, as we had done last year. We got through the federal e-file and moved onto the state filing, only to find out that if you’re filing partial states, Credit Karma doesn’t support it. I had to print 70 pages of our federal return, sign it, and ship it off to Virginia.

SUMMARY

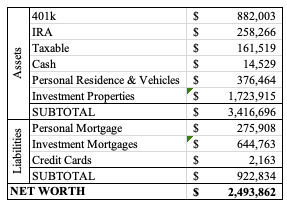

Our net worth actually dipped this month. The stock market is the main factor in that, but the house valuation estimates are starting to level off and look more realistic as well.

Between our personal lives and our business life with these rental properties, we were sure kept busy. We expect the Spring months to be a busy time of year, and honestly it feels good to be active again. While we’ve loosened the purse strings for the summer months, especially after having done hardly anything for the last year, it was still a shock to see just how much we spent in these categories. But that’s the benefit of looking at your finances regularly. We can either choose to remain on course with our summer plans, or we can dial it back if we feel this was more than we expected.

Since we know we’re on top of our finances and have set up a healthy mentality when it comes to spending, we’re comfortable looking at this information once a month. If you’re currently developing these money habits, you may want to do these types of check-ins more frequently.