Another month, and another delayed post while I juggle life. These numbers are mostly based on last Wednesday’s market close. I had big intentions of writing this on Thursday last week.

RENTALS

Our rental that we purchased a month ago is still vacant. It’s a commercial loan, so the first payment was just made on it yesterday. It always hurts to pay those bills without income. I’ve spent some time cleaning it. It looked fine if you just did a quick glance. But the details were terrible. I wiped down all the walls in the house and all the outlets and switch plates, which were extremely necessary. I wiped the baseboards with their first clean using the mop, but I’ll need to go back and do a wipe with something that gets directly on it. We were excited that the house didn’t need painted, but the closets are a bit of a mess. If I decide to make the time, I’ll throw some fresh paint on some parts. The bathrooms were pretty bad, and they’re about 70% done being cleaned. Maintenance wise, we just needed to replace a missing cabinet door pull, clean out the air return vent, and do a few random small fixes with caulk and screws. I’ve shown in several times. I even had a lease drawn up for one person, but it fell through.

We’ve had issues with our two new tenants getting their utilities in their name. We had one in Virginia who claimed she tried to get the water bill in her name and it just wasn’t happening. She always paid the day I sent the bill to her, so I just let it go. This past month was terrible. It took her over a month to get it paid, and I threatened to turn it off so that it would force her to get it in her name and keep me (and my property manager) out of it. One in Lexington was annoying that she didn’t get it done, and she’s not very communicative. Then the other in Winchester had to go in person to get the water in her name, so that wasn’t surprising that it took a while.

PERSONAL

Our 3rd kid got off the waitlist for preschool! Our beloved preschool closed down last year. Everyone flocked to this other preschool. I followed the “rules” and did things “ethically,” but we got waitlisted. Long story. I wasn’t pushing for him to be in preschool in the 2s year (he’ll be 3 next week, but our age cut off here is August 1st). I figured I’d push really hard in the next couple of months to make sure he got a spot for next year. This place I want him to go to has a lot more spots for 3 year olds than 2 year olds, so I had high expectations we’d get a spot next year. Well, we got the email a couple of weeks ago that there was room available for him! It’s a longer day than we’re used to, but he’s so excited to go to school. He asks to go to the playground daily, so that’s going to be nice that he’ll have TWO playground times twice a week. I can’t wait to hear all his stories.

My work schedule has me in the office for half a day on Monday, Tuesday, and Thursday. We’re going to look into adjusting that in January to account for the days he’s in school so that I can actually enjoy some kid free (guilt free…no strict schedules and babysitter availability) time since 2018.

We paid off the 0% interest card that was sitting at $14,000. It didn’t bother me to have that balance sitting there because it was for a good reason, but it sure does feel good to have that off our plate. Our spending has been relatively low the last few months. This month will see a small spike because I have’t preemptively bought any Christmas gifts, so that will likely be a large purchase amount later this week. We’re also in the market for camping gear since we took the kids camping this past weekend and noted a few gaps in our equipment.

SUMMARY

We’re up $1.5 million from 2 years ago, which is a cool number to see. Considering we paid off large credit card balances, I’m surprised our net worth only went up about $5k since last month. I updated the value of the houses in the past few weeks, so that’s where the hit is. Home values are expected to go down in the Fall, so I like to capture that adjustment from the higher values that appear in the Spring. Our cash value obviously went down since it went towards credit card payments and a down payment on a house (except it only decreased by $11k).

*I’ve been working on this post for a week, so my numbers are a week old, but I don’t want to re-update them. I’m also posting on a Tuesday just to get this ‘out the door.’*

I’m starting to pull myself out of the overwhelmed hole I felt I was in. There’s still a lot going on, but I feel better equipped to stay on top of things. I had just been so exhausted, that I didn’t have the energy to do anything extra each day, and I was just getting by. Last weekend, I was able to work on pressure washing our patio and deck furniture (which was long overdue), and then I stained our deck. That’s been a pretty good springboard to me getting a fire lit under myself to get other things done, so that’s felt really good.

Our middle child graduated pre-k on Thursday. That was a big milestone, and my poor girl is so sad that she’s going to miss her teachers. She’s really struggled with my going to work and not being home all the time (although my time not home, while she would be home, averaged about 10 hours per week). I have things better organized at work, and I’m feeling good about my tasks and role in the office, so the hours I’m spending there are dwindling. I had agreed to about 20 hours per week, but I was closer to 26/28 each week. The biggest issue was waiting for someone to be available to help me, and then that everyone else is full time, so they don’t realize I’m trying to get out of here by 2 pm each day. This week our oldest graduates kindergarten and has many events around end of school.

RENTALS

One of the mortgages has been paid enough that the balance dropped from 6 digits to 5 digits. It’s still a lot of money owed there, but that felt like a nice accomplishment when I went in to capture the balance!

June is Richmond tax season for these houses. That means I’ll be paying out large chunks of money for the houses we have no escrow on.

We had a few maintenance needs come up. One house had the water heater flood the basement. Luckily, I think we’re OK on that front. We replaced the water heater. The gas wasn’t hooked up right, so the tenant called the plumber to get that squared away. This happened while I was in a different state, and I’m so grateful it happened in a house with a handy tenant.

We had some flashing fall off a roof line. This wasn’t a priority to address at the time, but the tenant started claiming allergies were flaring up because birds were getting in the attic. Sometimes you just need to accept that’s the story you’re hearing. We had a handyman go over there and verify there are no birds anywhere. The “hole” she thought she saw was just where the soffit was hanging a bit, but there were no gaps in the wood structure itself. He tacked up the soffit, and I contracted with another company to repair the one piece of flashing.

That handyman also went out and handled a wasp nest. At that house, the tenant says a window won’t stay open when she opens it, and we let her know it’s on our radar now, but it won’t be fixed just yet as our people are spread thin and that’s not an emergency. That house had a temporary tenant in it (housing with our current tenant). To cover the tenant and us, I asked for a $500 deposit. When they moved out, I had our tenant sign that there was no damage, and I returned the deposit.

We’re still working on the major termite damage that occurred at another house. There was quite the domino effect. Leaks from bathrooms and the laundry room created a very wet environment, which created a breeding ground for termites, which feasted on our wood all over that place. The crawl space got cleaned up, but we’ve been waiting over a month for the bathrooms to get replaced and fixed. I’m hopeful that it’ll start next week, but frustrated nonetheless.

I had a leak from a toilet bolt at another house. I was frustrated because we had just been called out for water on the floor at this house recently, but it turns out this was necessary. When the house is a certain age, things just wear away and need replaced.

We also had a limb fall from a tree at another rental. The tenant explained how much of a liability it was for me. I love when tenants instruct me on my level of liability (that’s sarcasm). We have a tree guy that’s been super useful for many things and he handled it the next day with no problem.

PERSONAL

We haven’t been spending much money. Most of our money these days goes to grocery shopping. On our current statement for our main credit card, we only have 11 transactions recorded for over 3 weeks.

We paid our last month of pre-school for our second. They are closing the school and they didn’t want to add on days for the snow days that occurred, so they gave us $50 off the last month of tuition to cover the 2 days we were owed for make-ups. Since the school is closing, everyone scattered, and we ended up not getting into another preschool next year for our youngest. So at this point, that’s an extra $375 per month in our pockets next year – unless a spot opens up for the littlest.

Mr. ODA took the buy out, which I think I mentioned last month. His last day of work was April 30th. He said he’s settling into the not working concept and starting to get over the desire to know what’s happening at work and with his programs he worked so hard on. He’s done a lot of work around the house here, including treating for termites in a very intense fashion, but that was cool to see.

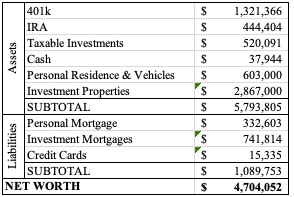

NET WORTH

Two months ago, my job asked for my goals. It’s a specific document that I was to fill out. Someone else had mentioned their net worth goal, and our next big step would be $5 million net worth. Well, the market has been in shambles, and our net worth plummeted from where it was. I thought it prudent to not make such a goal when our net worth is completely reliant on the market actions right now (i.e., we’re not selling/purchasing or making any big moves that would drastically change our net worth outside of the market actions). We’re finally on the upswing and now at the highest net worth we’ve been, so that’s encouraging after those big dips recently.

I grew up in a private school setting, and we didn’t have a cafeteria that made us food to purchase. Everyone once in a while, we’d have “pizza day,” where we could bring in a dollar or two and buy pizza that they had delivered from somewhere. My high school had a full cafeteria that prepared breakfast and lunch to purchase. It was a private school, so there weren’t any state subsidies. All that to say, bringing my lunch to school wasn’t even a thought. I packed a lunch and a snack every morning. In 2nd grade, I started doing that for myself and my sisters because my mom was really sick, and it just stuck as a chore I did.

I have a child who just started Kindergarten last month. Since my background was bringing my lunch to school, I expected to pack his lunch too. He’s bought school lunch just once so far, and it was for his birthday. I figure there will be a few days throughout the year that he’ll want to buy lunch, but so far he’s content with my packing it.

Last week, I was volunteering at the school, and another mom said “I don’t bother packing anything. For $2 they get breakfast and $2.75 they get lunch; I can’t make meals for that little.” And so, this post was born. Now, I don’t know the outcome, but my hypothesis is that what I pack for his meal is less than that. So let’s dive in.

BREAKFAST

First, breakfast for my kids nearly every day is cereal. That’s their preference. For all the things we don’t buy name brand, cereal is one we keep name brand. We buy it on sale on Kroger. Mr. ODA likes to stock up, even though he admits that the sales are every other week and we may not need 5 boxes of Honey Nut Cheerios in our pantry at any given time. 🙂

We paid $2 per regular-sized box. The box says a kids serving size will get 12 servings per box. That would come to $0.17 per bowl. Regardless, I do know that $2 per box is less than $2 for one breakfast though.

My kids don’t eat much for breakfast. At home, they have a snack around 10, a hearty lunch, another snack, and then dinner. They’re really good about eating when they’re hungry and not eating when they’re not. Even when my son got free breakfast at the orientation events, he ate a partial bowl of cereal and some fruit. We go through a lot of fruit in this house. But mornings before school don’t have the time to get fruit and cereal into him. I forced it on testing mornings, but he still wanted to eat just the fruit and nothing of more substance, so I had to bribe him.

LUNCH

This is where fruit comes in. We also have fruit as part of the after school snack.

Here are some options that I mix and match throughout the week (though not exhaustive). I’m also taking suggestions!

Yogurt Covered Raisins: $2.97/pack, 6 in a pack = $0.50 each.

Clementines: $3.50 per bag. I’m estimating there’s about 20 in a 3 lb bag. $0.18 each.

Grapes: We purchase these at $0.98-1.98 per pound. At the high end, for what I pack, I’m going to assume $0.20 per serving I give.

Oreos: Family size is $5.28 with maybe 48 cookies (that was a quick google). I put two in his lunch box if I put any at all, so that’s $0.22.

Fruit snacks: Honestly, we have a gigantic box that was given to us at some event, and that’s lasted us since the end of last year’s school year. But I’ll include this cost anyway because eventually I’ll buy more. $15.99 at Costco for 90 = $0.18.

Applesauce pouches: I buy Walmart’s version of this. $5.68 for 12 pouches = $0.47 each.

Peanut butter and jelly sandwich: A jar of peanut butter is $1.94, jelly is $2.74, and bread is $1.42 for 20 slices. The bread is $0.14 per sandwich clearly. The other two are harder to quantify, but both are minimally used per sandwich I make, so let’s say $0.15 total for those, bringing a sandwich to $0.19.

Chicken nuggets: $5.97 for a 32 ounce bag. I have no idea how many are in there. The package says 4 nuggets are a serving and there are 12 servings in the bag, so let’s say there are 48 nuggets. That seems low though. That means each nugget is $0.12.

Pizza: We seem to have pizza once per week, and there always seems to be 1 or 2 slices left over. $4.97 for the pizza, where we get 8 slices, so $0.62.

If I pack a peanut butter and jelly sandwich, grapes, clementine, and oreos, that’s a total of $0.79. Today I put a PBJ, raisins, grapes, and oreos. He actually got 3 oreos because there were only 3 left in the package; that total came to $1.22. Yesterday’s lunch was 7 nuggets, an applesauce pouch, grapes, and a clementine; that came to $1.69 (actually, that doesn’t include the bit of ranch I put in there, so perhaps add a few cents).

The first few weeks of school, I had been putting more food than this in his lunch box. He had told me he was eating everything, but grandparents day had grandma eating with him so she saw he was throwing some things away. I had asked him repeatedly to tell me what he likes or doesn’t, or if there’s not enough or too much food so that we can make adjustments.

There are other things like puffed corn, chips, and cheez-its that I buy for his snack. He eats lunch at 10:30, so they give him a snack in the classroom at 1:30. There’s no option to buy a snack at the school at this time, so everyone needs to pack their own snack.

SUMMARY

By the time my child gets home from school, I’ve spent approximately $1.80 to feed him for breakfast, lunch, and snack. On the high end, it may be about $2.25. This also assumes that the child is happy to eat all the options presented for the meal. When my son bought his lunch, he ate the orange slices, bread, and half the spaghetti. He didn’t touch the broccoli (that I put on his tray for myself), and he didn’t even pick from all the options presented in the cafeteria line. Whereas I know what I’m packing includes things that he eats regularly at home.

While I agree that $2.75 for a meal is cheap relative to buying at a restaurant or fast food, the assumption that it’s cheaper than what you could pack a lunch for doesn’t appear accurate.

Back when I spent my days working in front of a computer, it was easy for me to analyze our spending. These days, with 3 kids in tow, I’m lucky to record our finances timely. There’s no time for analyzing. But over the past two years, I haven’t been happy with our spending total for the year, so it was time to look into it a bit more. It’s hard to know what has changed since I don’t have month over month, or year over year, trends to compare this data to, but it’s a start.

There are some caveats.

I don’t include any spending that isn’t on a credit card here. That means some of our rental property bills aren’t captured (they’re paid via Venmo or check), but I decided that’s ok because I can see that in a different way (a separate spreadsheet). Those expenses are reactive and a necessity to running the business, so it’s not like I can change a spending trend there. I’m more curious about our actual expenses and where our money is going for personal decisions. There will be some rental expenses captured here though.

I’m doing this analysis for the first half of the year. If this was for a month at a time (which is a goal), then I’d be able to dive deeper into spending at each place. For instance, at Walmart, those expenses aren’t always ‘grocery.’ However, I don’t have the time to go through all the purchases and siphon out non-food purchases. I did go through most of the Amazon purchases and categorize them.

If a purchase was made at Lowe’s or Home Depot, it’s classified as home improvement. It may have been rental property work, but generally it’s related to something we’re doing at our house.

If a purchase was made while on vacation (such as amusement park, tolls, hotels, dog sitting) , it’s categorized as ‘vacation.’ If we were on vacation and purchased food, it wasn’t labeled as vacation. All fast food or restaurant purchases for the first half of the year are categorized as ‘restaurant.’

If we did an activity from home, it’s labeled as ‘entertainment.’ If we did something related to sports (this includes swim lessons, ticket purchases for performances, etc.), then it’s labeled as ‘sports.’ The entertainment versus sports delineation is because something like a single tournament could be considered entertainment, but I kept all sports items as ‘sports.’

None of this includes whether we were reimbursed by someone else for a purchase. For example, we purchased tickets for 15 of us to go to an amusement park on vacation, but we only paid for 4 tickets of that personally. Mr. ODA is a personal shopper for restaurants, so much of our restaurant shopping around town is actually later reimbursed in that process (but not captured here because it’s not a credit card line item).

In the process of going line-by-line on my expenses, I discovered that I never received a refund for something. I placed an order on Etsy for a personalized gift for my niece’s birthday. A few days later, I went to check the status of the order, and I discovered that the shop I ordered from was no longer selling on Etsy. I was frustrated that I received no email that told me my order wouldn’t be fulfilled. I contacted Etsy customer service. At the time, I misunderstood Etsy’s billing process. I assumed it was charged when the item shipped. As I was just going through charges, I realized that the amount was charged on the date of purchase (e.g., not when shipped), and I had never received a response from Etsy. After another frustrating round of attempting to contact customer service this morning, I finally received a resolution. Now my ‘to do list’ has to keep track of this refund appearing. It’s $10.01, so it’s not the end of the world. However, it would be nice if Etsy shuts down a seller (their words), that they manage the outstanding orders without me having to take my time to get it corrected. Plus, if I let every “it’s just $10” go, it could add up quickly.

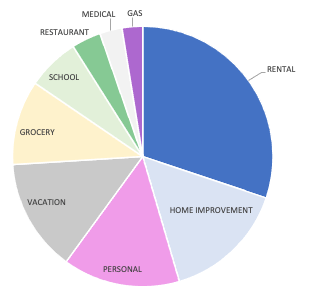

FIRST HALF OF THE YEAR SPENDING

By far, our largest slice of the pie up there is for rental expenses. Honestly, I’m happy to see that so much of our credit card expenses are taken up by rental expenses we had. I pay our insurance premiums (where they aren’t escrowed) via credit card, and I can pay our county taxes for one house with a credit card, which I do for the cash back rewards. There was flooring replaced at one house, which was a significant amount of that slice.

The ‘home improvement’ category includes new patio furniture we purchased, but were reimbursed by insurance (a tree fell on our deck). It also includes the electrician work and dirt fill purchases that we needed for the deck rebuild. Our house has a few more fairly large projects we want to complete, so I expect that to continue being a larger chunk.

I know that our “grocery” expense isn’t completely groceries. I’d like to focus on this category of spending more in the second half of the year. I want to quantify what’s purchased at Walmart that is actually grocery versus personal shopping type purchases. I think that our grocery purchases are higher than they should be, but I can’t put my finger on exactly why. Historically, I’ve blamed it on ‘bulk’ shopping; Mr. ODA will go to Kroger for the “buy 5” type sales. I’m not sure that’s it though.

We don’t eat at restaurants very often. We usually eat at fast food places while we travel or are away from home at an inopportune time. When we’re at home, we’re usually eating at a “personal shopper” experience where our food cost is mostly reimbursed (although that’s not captured in the chart).

Our health insurance deductible is $3,200 per year, so we expect slightly more than that each year in the medical expense category (and based on how deductibles work, that expense is front loaded in the year). I actually pre-paid a bill at a child’s urgent care visit. I paid them $50, but that visit, along with two more visits since then, came to a total of $12. I’m waiting for their reimbursement of that difference.

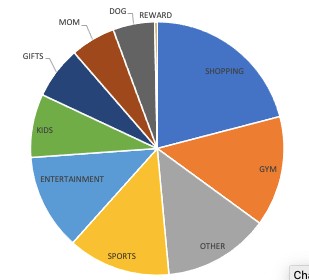

PERSONAL SPENDING

I’m going to dig deeper into the ‘personal’ category. I labeled a bunch of things as ‘personal’ as a means of not having too many small slivers of the overall spending pie. This includes all gifts, needs for kids (new shoes), clothing for kids, gym membership, sports, etc. It includes a ‘shopping’ category. I spent some time going through my Amazon orders and categorizing them, but the ‘shopping’ category was too daunting and difficult to parse out further. About a third of the ‘shopping’ category is Amazon orders through Mr. ODA’s account that I didn’t pull up to categorize. The rest is random purchases that were probably related to gifts or kids clothing.

For entertainment, this is small things like going to the movies (which we go for $2 per ticket), bowling, and aquarium. The largest chunk of this pie part here is actually 4 season pass lift tickets for our family’s future winter season. I put the ‘mom’ category to see what I’ve purchased for myself that wasn’t a necessity (e.g., a travel cosmetic bag, baseball shirts to wear to my son’s games), as well as my one hair cut and one pedicure that I’ve gotten this year so far. The ‘other’ category is boring stuff – utilities, car maintenance, professional fees, etc.

Had I gone through my Walmart orders in detail, I would have been able to identify some more purchases that could be removed from ‘shopping’ and put into other categories. For instance, the ‘dog’ category is actually higher because I order his glucosamine and tooth cleaning treats from Walmart most of the time, and that’s a monthly expense. His annual vet appointment is in the Fall, so this will be a larger slice of the pie for the end of the year.

SUMMARY

Our annual credit card payment total for the last three years have been about the same. While it’s a ‘win,’ that it isn’t increasing, it’s still at a number that I don’t like. Mr. ODA has been working towards a ‘retirement’ date. We’ve pushed it back just because his job hasn’t significantly impeded our lifestyle, but the day will eventually come. If it’s next year, I’d feel better if our credit card payments weren’t as high.

I went into this expecting my grocery category to be higher than I’d prefer. I didn’t identify much of what is causing that, so I’ll try to focus heavily on watching that expense each time it hits the credit card, rather than trying to remember what each purchase entailed six months later.

I was surprised to see the gas category such a small sliver of the pie. We’ve done a lot of trips (although, I suppose a majority were in July, which isn’t captured in this data). It appears living in a smaller city and doing things mostly on this side of town means we’re not having to fill up our tanks too often.

Overall, I didn’t notice any egregious spending. We don’t spend for the sake of spending. This year we traveled more than we had the previous two years, but mostly our spending is the same. Now that we’re two years into our house, there are less projects that we’re putting money towards. I’m encouraged that now that I’m looking at this, I’ll be able to identify areas to scale back.