We’re continuing our spring/summer of travel and activity, which is why there are fewer posts and lots more spending.

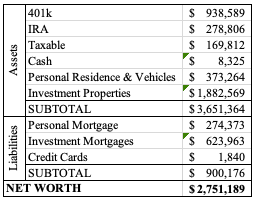

The stock market has increased, which has been the main factor in our net worth change. We paid $2,000 towards the mortgage we’re paying down, leaving a balance of $3,300. This mortgage will be paid off once all our rent is collected for July; it was pushed back a little bit because of the flooring replacement that occurred in one of our rentals, which is why our credit card balance is much lower than last month. We’re also still waiting for half of one property’s rent, which is the norm these days.

- Utilities: $250. This includes internet, cell phones, water, sewer, trash, electric, and investment property sewer charges that are billed to the owner and not the tenant.

- Groceries: $518

- Gas: $268

- Restaurants: $165. Our credit card reimburses for many of these expenses; we received credits totaling $120.13 in the last month.

- Entertainment/Medical: $1,093

- Investment: $1,100

- Insurance Costs (personal and rentals): $845

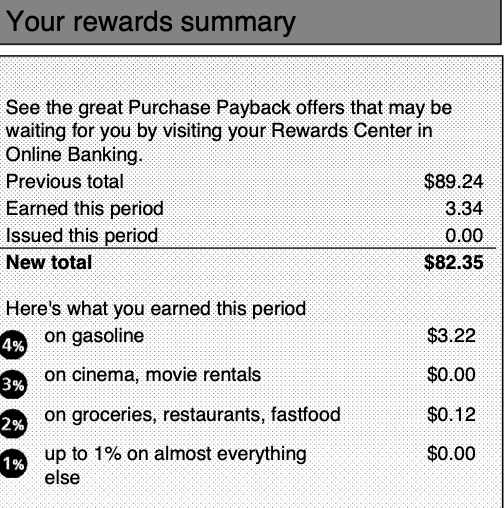

VIGILANCE ON CREDIT CARD REWARDS

Mr. ODA discovered that our PNC credit card rewards balance was decreasing, despite earning new rewards this cycle. He investigated further and noticed that we had been losing rewards for a few months now. PNC has a policy that they don’t issue their rewards until you hit $100 worth of rewards. Once we hit $100, PNC sends us a check in the mail. Since they send a check, we still receive paper statements, even though we regularly check our financial accounts online. Over the past few months, both of us checked the balance to see “ok, we’re nearing $100,” but didn’t put any more effort into knowing the details of the balance. Mr. ODA happened to notice that the statement didn’t make sense.

$89+3 somehow equals $82. There isn’t a single section on our statement or via our online account that identifies the loss of rewards Mr. ODA called PNC to ask for more details and learned that our rewards expire after 2 years, despite their policy of not issuing a check until you hit $100. They basically said, it doesn’t matter that your account is over 10 years old, or that credit has been used less in the last year due to the pandemic, or that they don’t clearly identify the expiration of rewards and just identify a lower balance. As a comparison, and I keep going back to Chase, but Chase changed up their reward categories to allow the consumer to earn more rewards during the pandemic (e.g., in addition to giving rewards in the travel category, since consumers weren’t traveling, they added grocery and home improvement stores as major reward categories).

The PNC customer service representative reinstated 60 days worth of lost rewards and issued a statement credit. We don’t want a statement credit because we no longer want to use this credit card, earning rewards that we’ll never be able to capture. If we use this credit card to use up the statement credit, that’s rewards that could be earned on a different credit card. Now Mr. ODA is fighting for the credit to be applied to our checking account or to have a check sent to us (which is the preference on our profile) and fighting for the reinstatement of the rest of the rewards lost.

Without PNC, we’re down to 4 credit cards in our regular rotation. We have 3 cards that we use for categories (gas, grocery, restaurants, travel, home improvement stores), and then we have the Citi Double Cash card that is for “everyday purchases.”