This is probably our easiest house to own; the closing process was the hardest part here. We closed on House 5 & 6 at the same time, so I’ll cover the closing story here because House 5 has a lot else to be said when I write out that whole saga.

TENANT

This property has a property manager on it (10% monthly rent). She processed a couple of applications at the onset, and it took 2 weeks to find the tenant. The lease started on August 18, 2017, and that’s been the same tenant in the house to date.

Rent is $850 per month. She pays on time, and it’s usually early. She just asked about her renewal, and we decided to keep her rent at the same price, even though it’s the start of her 5th lease term. Our cash-on-cash return was ahead for the last 4 years, so even though our taxes have increased by $400 since we purchased the property, we decided it was best to keep the tenant than to get a few more dollars per month.

She asked if she could paint the kitchen cabinets that were definitely old, and we figured they couldn’t be made any worse. When a tenant wants to make your house their home, it’s most often is a sign they make taking care of the property their priority, and that they want to stick around for a while.

We had to treat the house for ants over this last year, but the only real issue we’ve had on this house is that the main sewer line had to be replaced due to corrosion and tree stump intrusion into the pipe. The poor tenant had her toilets backing up into her house. It was $4,000 to replace the line from the street to the house. Honestly, I expected it to be more.

LOAN DECISION

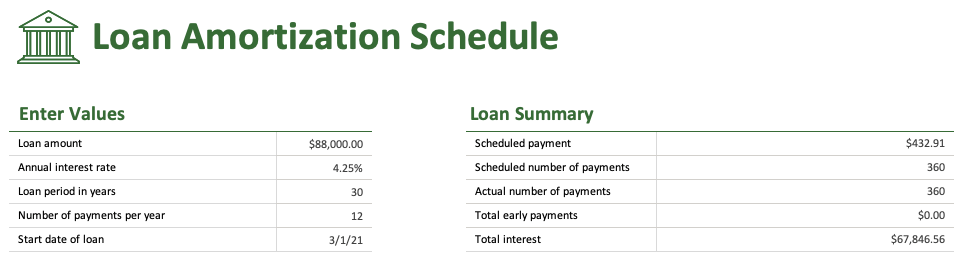

Option 1 – 20% down payment – conventional 30 year fixed at 4.95% with 0 points

Option 2 – 25% down payment – conventional 30 year fixed at 4.7% with 0 points

We weighed these two options for our loan (purchase price of $66,000). The difference is an increase of $3,300 in down payment to save $5,700 worth of interest over the life of the loan. Being that we closed on several houses in a short period of time, we chose Option 1. Having cash for the down payments and closing costs of the other houses was more important than the marginal savings in interest of putting 5% more down.

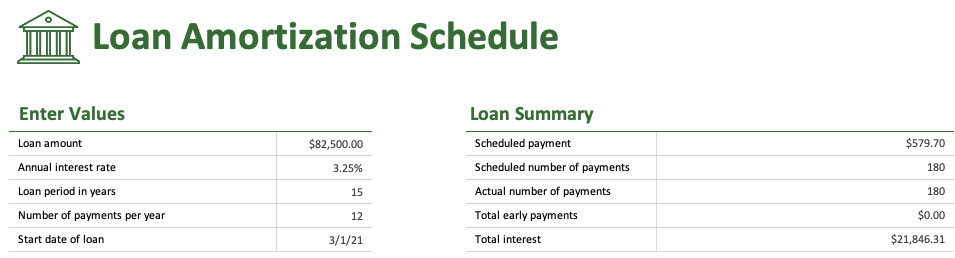

We’ve been paying down this mortgage. At the time of our decision on which house to pay extra principal towards, this was the smallest loan amount with a relatively high interest rate. We started paying extra towards this mortgage in October 2020. To date, we’ve paid an additional $35,500 towards principal, leaving a balance of just under $14k.

CLOSING

During the Spring and Summer of 2017, we saw a lot of houses. We also made offers on a lot of houses that didn’t end up going anywhere, either because there was no consensus on a purchase price or because the home inspection was unsavory. We closed on House 4 at the end of June, walked away from a deal on one house due to a home inspection issue, and then closings on House 5 & 6 got lost along the way by the attorney’s secretary. We worked with a specific attorney who we had a great relationship with, and who eventually helped us with a difficult purchase (see the story for House 8), but this was a hiccup.

The attorney’s office let us know they were unaware of these two closings around June 20th (in reality, they just missed the ‘all clear’ to move forward with a title search, but they were definitely made aware of them), which left us scrambling. Our rate lock expired July 7, and the secretary responsible for filing all the paperwork was taking her vacation the week of July 2. Since she was taking the week off, our attorney scheduled a surgery of his for the same time, so the office was closed. She said she would find a way to make it work, but then we didn’t hear from her and had to reach out to the attorney himself. Here’s that email, outlining all the details.

It wasn’t until June 30th that our attorney confirmed he was able to hand off our closing to another attorney’s office. We had a few questions about their fees, since we explicitly stated that we didn’t want it to cost us more because we had to change our closing location, and then the secretary there got defensive and gave us an attitude. I was quick to call her on it, explaining that we just wanted to better understand the break down of what they put on our closing disclosure. She backed down, and then we had an awkward interaction a few days later when we showed up in her office to sign the paperwork. It’s interesting how people don’t understand that writing in capital letters can come across as rude. Turns out this other firm was an old law school friend of the attorney we normally use, and they worked out a favor among themselves on the fees to ensure they didn’t lose any future business from us.

At the end of the day, we closed on the houses on time and without costing us anything extra, but it wasn’t a stress-free path to get there.

Luckily, this house has been easy to manage and the tenant has worked out perfectly. Our rent at $850 far exceeds the 1% Rule; with a purchase price of $66,000, our monthly rent goal would be $660. Tax assessments have recently risen given that the local market has appreciated substantially, so we will consider a rent increase in the future. However, at this time, having a long-term tenant on a house that has hardly any issues is more important than risking a rent increase and having her leave.