I have so much to say. January is a big time where people are willing to talk about finances, so many thoughts enter my mind that I want to squash some preconceived notions. Unfortunately, I just don’t have the time.

PERSONAL

At work, I’ve spent this year managing year end things and getting the 2026 processes stood up. I’m supposed to be part time, but I’ve been putting way more hours in because of that process. The guy who was helping me left for another position and was out of the country all last week, so I had to make sure I was extra on top of things. With all those actions going on, I also was pulled into hiring someone to be my assistant (for lack of better term… it’s not assistant as in answering the phone and getting the mail… it’s doing the daily bank reconciliations and those types of tasks so I can focus on policy development). This has taken a significant amount of my time, but hopefully this person will be on board to help in a week.

Our youngest started preschool last month. He only goes 2 days per week, and both are my work days. I’d really like to get to a point where I can actually take advantage of guilt-free, kid-free time.

I have a new years resolution that I’m keeping close to the vest, but one part of it is to walk 10,000 steps per day. I’m failing miserably, but it’s a work in progress. My 7 year old son asks me constantly if I’ve hit my step goal. So…. maybe I’m teaching him it’s ok to fail, but keep trying? His new years resolution is to get better at being his nicest, and that’s just adorable. He also says he wants to learn basketball, and I just can’t bring myself to do that. We are signed up for Spring baseball that should start in March. The youngest has to wait until next Spring, but I can’t wait to see what he can do. I’ll probably also be putting swim lessons back on the docket in the next couple of months. The youngest hasn’t had any lessons. The oldest passed the test for his yellow band, but he needs to have a free style stroke to get the green band. The middle needs confidence; she can absolutely swim, but she likes to pretend she can’t do things.

RENTALS

Last month I reported that at the end of the day on the 5th, I was still missing 25% of the month’s rent. As of 7 am on the 5th, I had only received 30% of rent. Many came through, but there were more than the usual amount that didn’t. For one, I had to manage a grant program from one of the places a tenant lives. The check finally arrived yesterday, but it’s dated December 12th. They mailed to my PO Box, in a town I left in 2020. I didn’t even know my lease had an address on it, but that’s how long these people have been there. The check was returned to them, so my tenant went down there to give them my new address. I don’t love these people having my address, or that they now officially know I don’t live in the same state as them, but I needed to get this check. I gave them the address over her phone and received confirmation she typed it in. Somehow the check was returned to them, so my tenant had to pick up the check and FedEx it to me (I told her she didn’t have to pay that kind of money for that!). I have a tenant that pays twice per month (and pays a premium for that); her second part of rent is due tomorrow, so we’ll see if I can finally be fully paid for this month by the 19th.

I have a tenant who fell into some unfortunate circumstances. Her current plan is to vacate her place by the end of March. She’s lived there since 2019 with a dog and 5 cats, so that place will need all new carpet and a new paint job, but hopefully will be ready for a May 1 rental. Because she’s always paid and I knew her financial circumstances, I’ve been slow to increase her rent. She’s paying $975, but the market rent should easily get at least $1200. The house is in really good shape and is newer. We had people fighting over the other house in that town at $1150, and it’s an older house with only one bathroom.

FINANCES

Well we traded in our van for a newer year, but that’s a story for another post. I also still haven’t fixed my retirement account access from when I got a new phone number, so that’s a made up number.

I’m going to be tracking our spending much closer this year. We’re generally on the same path with our spending, and I know we don’t do anything extravagant. With Mr. ODA’s lack of income, I just want to keep a closer eye on that and pivot if we need to.

Mr. ODA has a more exact approach to figuring out what we can spend per month without dipping into savings. I like my number better (and it’s lower). I took our rental income, deducted rental fixed expenses, deducted our typical bills, and was left with just over $1300 per month. That would go towards food, clothing, gas, etc. If I remove things that are offset by a shop (Mr. ODA is a secret shopper) and the long term investment purchases (i.e., car and windows), we’re at $987 as of the 18th.

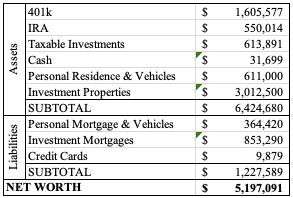

NET WORTH

We put $1500 on a credit card and finances $7500 to be able to save $1000. We also put $5500 on credit cards towards windows, which is also another post that’s coming. Our net worth took a hit for both these things. I also wasn’t able to update 3 accounts, so they’re just estimates, but at least our net worth still went up.

I had an “ah-ha” moment the other day about this word. There’s a difference between being able to afford something and wanting to afford it. So many times, we focus heavily on what people see on the outside. I hear it at work lately – I work with agents, and there are comments made about how people spend their money. Now, I agree with the “I just handed you a check for $20,000, what do you mean you have no money?” However, there’s a flip side. Just because someone pulls up in a Tesla doesn’t mean they want to throw money around.

TRADE OFFS

Mr. ODA and I have money. We can go out to dinner, go on a vacation and stay in a fancy hotel, pay for flights across the country for all 5 of us, buy another house, splurge on a vacation house and a boat. If we wanted to. We don’t.

Instead, we want to look into the future. We decided that the ability to spend time as a family, being there for the kids’ activities, and going on different kinds of trips throughout the year to give the kids experiences is more valuable.

I talk about this concept often in this blog. Every dollar spent has an opportunity cost. Every dollar spent should cause the question, “is this the best use of this dollar?” We joke about how we hesitate to buy a $30 pair of shorts, which you wear for years, yet we’ll spend $30 to eat one meal. Of course, we do have those instances where we go out to eat, but they’re not a constant staple of our household. We know that the instant gratification of that one meal isn’t going to get us to our long term goals. It’s the same concept with the $5/day coffee purchase. It’s not about the literal $5 that’s going to get you on your way to financial freedom; it’s the mentality that comes with making better financial decisions.

HOUSE POOR

When we were shopping for our first house in 2012, the bank pre-approved us for $750,000. We set our limit at $350,000. Why? Because we felt we could scrape together 20% down payment and closing costs for a $350,000 home. If we were under a $750,000 mortgage, we’d have to pay a higher monthly payment and private mortgage insurance (PMI) as a penalty for not having 20% down. At $350,000, our mortgage payment was about $2,000. At $750,000, the mortgage payment with PMI would have been about $3,500. That’s an extra $18,000 per year we would have been spending on a house instead of investments, trips, a new car, etc.

If I said to you, “pay $2000 to your mortgage, and at the very same time, put $1500 into a savings account that you can’t touch,” what would your reaction be? You’d find every excuse not to do that. You may do it for a month or two, but there would be an emergency or large purchase that comes up and you’d justify using that money for that instead.

CAR DECISIONS

While we can “afford” the Tesla, we didn’t buy it to be showy. We bought it to serve a purpose. Unfortunately, the concept of Tesla comes with pre-conceived notions for people. We didn’t pay for an extra color. We bought the base model because we weighed our expectations of using it versus the cost of extra charging needed and such. With the tax credit, our net was $38,000. I’d venture to say your car was about that price or more if you bought it new. So while we can afford the Tesla, that’s what we chose for our family because it met our needs. We didn’t buy an $80,000 BMW just for the name when a $40,000 car meets our needs.

GADGETS & TRINKETS

Maybe your spending is at the hundreds of thousands level. Maybe you’re buying the new Nintendo Switch that just came out. Maybe you’re buying each new game for your gaming system. Maybe you have bought into the influencers that are constantly jamming the latest mop and vacuum down your throat. Do you need 4 mops? Do you realize that you probably just need to actually use the one you already have and that this new gadget isn’t a miracle worker?

Everyone has their thing. There’s something that brings you joy and you’re going to be drawn to purchasing new iterations of it. I get that. But have you stopped and really considered the purchase?

This is where I don’t like the “envelope” method. People who use this concept, whether it’s literal envelopes or separate accounts, tend to overspend. They see there’s money left in an envelope and it goes into “extra” immediately in your head. “I saved this month, so I can buy myself something fun!”

This month, I replaced my favorite earrings because the originals were worn out ($12), bought a pair of black shorts because I had none ($14), bought a dress because Mr. ODA needed free shipping 😉 ($20), and two books I really want to read and aren’t available at the library ($20). Before this month’s Amazon order, my previous one was for kids summer pajamas in April. I buy filters for my vacuum instead of replacing it (although I’ll admit that I’ve had my eye on a new vacuum cleaner for about a year, but it’s been sitting at $80 and I know I’ve seen it for less than that). My mom bought me my steam cleaner mop several years ago, and I have a Bona that I bought for myself in 2016. The point here being that I’m stopping and thinking before making decisions, regardless of the amount of money I have available to me.

EDUCATION

It comes down to being an informed consumer. While you can rely on the experts, understand your own goals. When that relationship banker ran our numbers for a house purchase, all he did was ask us our fixed monthly expenses and income (debt to income ratio). Note that our approval was after the changes on how mortgages were approved from the 2008 crisis. It’s a flawed system. But we knew our limits and what our goals were. He didn’t ask us our goals outside of “so you want to buy a house.” At the same time, we were paying towards a wedding. So on top of needing to come to the table with about $80,000, we also needed $12,000 to go towards that wedding. We closed on our house on July 17th and were married on August 4.

We have money in many locations. Currently, in our main checking account, I’m projected to fall below $0 if I don’t have any income before the end of the week. I have a bank account with more than enough money in it, but it just pains me to move money out of that account. I don’t want to set the precedent. I bet if I had kept my business money separate from my personal money, it wouldn’t be as obvious. But we don’t keep things separate because the business income is our family income. So when I had to pay out over $3000 for a repair on a rental house, that ate into my personal checking account balance, so I’ll need to make that transfer.

I listened to the young receptionist at work bark about people spending their money and how someone showed up in a Tesla but can’t pay their $75 office bill. However, I’m observant. I saw that she complained to me that the money in her account showed up on the wrong day so her card was declined at Hobby Lobby. I saw that she regularly came in with a new outfit from TJ Maxx. I’m sure she got a deal, but is a new outfit twice a week a necessity? When she was let go from the job, she turned to “retail therapy.” It’s hard for me to help walk you through the loss of income while you are actively spending.

Personally, I worry, “what if the ability to transfer from our special savings account isn’t there one day?” That’s because I’m looking at the big, big, big picture of our lives, and not what happens today, this week, or this month when it comes to our finances. So that’s why I don’t buy the kids all the cute outfits I see and I don’t buy myself the latest gadget. I’d rather have the ability to go on a trip and do activities with the kids that build memories.

This was a good year. We took a lot of trips, made some good memories, and purchased some fun things. While day to day life has been hard with 3 little kids and managing some of my own interests, it really was a fun and rewarding year when I look at the big picture.

PERSONAL: MY YEAR

I went through a lot of growth in this year. I started the year with a girls trip, which was really healing in my mom-of-3 world. After that trip, I hunkered down on my diet and exercise. Over 10 months, I lost 22 pounds. Each kid added about 10 pounds to my body’s desired size (where I just plateau unless I put a lot of effort in). It’s not something that I regularly discussed with people or mentioned, but it is something that I’m pretty proud of and took effort. I ran a 5k in August, where I beat my time from the year before, and it didn’t feel like it took any effort to beat that, which was nice.

But then my oldest started kindergarten, which was a surprisingly hard adjustment in my schedule. He was completely ready for school, and him going wasn’t the hard part. I welcome new phases of life and mostly don’t dwell on the losses that those mean. However, the schedule of the year took me two or three months to get used to. He gets on the bus at 7, #2 gets dropped off at 9, she gets picked up at 12, baby takes a nap from 1:30-3:15, oldest gets off the bus at 2:45. It was just a lot of broken up time in my day, and it took so much out of me each day. I finally feel like I’m used to it and can be productive in those short periods in between.

We were told that our preschool will be changing ownership next school year, which threw a wrench in my plans. Sure, things will work out. But it doesn’t change that I had a plan that didn’t need to be thought about. I had a financial expectation that didn’t need to be budgeted for or considered any further. It was another thing that took mental energy from me. I had originally thought I’d not send the 3rd kid to a 2s year like the other two kids. I spent some days mourning that alone time I was giving up by keeping him home. But I toured a preschool, and that’s my wish list for next year. If we don’t get into that preschool, I’ll likely just keep him home with me and try for the 3s year there. It’s just a socializing desire. I don’t work and need child care, so it’s a privilege to send him if it works out.

On top of all the parenting jobs I have, my job managing our rental properties is another job that takes a ton of time and mental energy, but no one really sees the fruit of that labor. May was the only month this past year where everyone paid rent on time. While I’m pretty lenient on that, that’s still time that I’m taking to manage and keep up with. I have one tenant who hasn’t put the water bill in her name yet. Supposedly it’s a city issue, and she always pays when I send her a picture of the bill, but it’s still a time sucker that I have. Then add in that we have several maintenance requests that come up, and a few big projects that were needed.

Related to the rentals, I made 44 posts on this blog. I set a goal to post once per week, preferably on Thursdays, for the year. I fell short by 8 weeks, and I wasn’t consistent with the Thursday post each week. I did well when I had inspiration, and I always did the monthly updates, but I didn’t meet my goal. I’ll keep the same goal of once per week, preferably on Thursdays, for this year. While my reach isn’t far, I do hope that someone will find this little corner and gain a new perspective on their finances. Plus, I appreciate being able to go back to our monthly updates to see how things have changed. It’s hard to see it when you’re looking month-to-month, but to see a drastic jump in numbers from a year ago is nice.

PERSONAL: THE FAMILY

We made it to 12 states this year, and that’s pretty cool. The kids got to see a lot, and they’re really interested in different states and their stats. I appreciate that curiosity and the ability to learn while traveling. Only one trip was on a plane, which was to Colorado. We did a 2-week long trip to New York and Michigan, with a few stops in there. We went to Chicago for a wedding and explored the area, took the kids to Gatlinburg for Fall Break, went to Ohio to watch the eclipse in totality, and tagged along on Mr. ODA’s work trip to South Carolina.

Mr. ODA sold his 15 year old vehicle, and we purchased a Tesla. I didn’t have a great experience with one in Colorado, but I think that was more related to the circumstances than actual electric vehicle ownership. I had a great experience with the test drive, and we picked one up by the end of that week. We took advantage of their 0% interest and 3 months of free charging. We also referred a friend of ours, so we received $1000 in Tesla credits that we’ll use for charging after the free period.

We bought a hot tub. That was a purchase that was about a year in the making, so it wasn’t made lightly. There hasn’t been two days in a row where someone didn’t get in it, until we just left for a week (hoping that the water is in good shape when I get back!). Our deck was crushed by a tree in July 2023, and it wasn’t rebuilt until May 2024. Then we had to take the time to make the decisions on what we wanted, get it ordered, and wait for delivery. It was delivered in November, and it’s been a great purchase thus far. We haven’t done such a splurge before, and it’s nice to give ourselves something that we can enjoy.

The kids are doing their activities. We’ve been in a nice lull, but I recently saw our March calendar from this past year and was reminded of all those hours! Our oldest is doing t-ball for a second year. Our second is regularly doing gymnastics, but we’re also letting her do t-ball this spring. Our oldest is also doing an after school activity for checkers, but supposedly it’s in a fun way, so that’ll be interesting to see pan out. He was accepted into an advanced program for his 99th percentile state testing scores, which was a really exciting moment as parents. Our second will finish out her preschool year and go to kindergarten next year. And we hope to have another fun season over the next two months with everyone on skis!

RENTAL PROPERTIES

Besides the management of late rent payments, I had to put a lot of hours into these houses this year. We took a trip to Richmond, VA to work on quite a few of these houses. On top of that, there were several other activities that were needed, management of tenant turnover, and management of rental income, but I’ll save that for a future post so this doesn’t grow too long.

FINANCES

Our net worth increased by $745,000. We started the year with a goal of hitting $4 million net worth, and that was achieved in a short time. Month to month feels like we’re barely moving the needle, but it’s amazing to see that number over the course of a year.

We paid off one 0% interest credit card from our carpet replacement in our personal home, and then we opened a new 0% interest credit card to pay for the hot tub. That new card gets 2% cash back, so it’s being used more than we usually use a 0% interest card. Typically, we just pay for the major purchase and then pay it down over the 0% interest period. This time around, it’s being used for every day purchases so the monthly payment I’m making is more than I’d usually see.

I have a separate post that goes into our extra income that we brought in over the last year, which is related to earned credit card rewards and interest on savings accounts and bonds. That’s even cooler to see the total ($14k!) because that was actual cash that went into our account and was used.

In the last year, I only officially worked 11 days, which is crazy to think about. But I’ve been doing random other jobs to help others out. I’m on our homeowners association board of directors, and I’ve been helping a new school get their financials up and running. I’m ready to take a step back from the finance work because my commitment to the HOA feels more pressing, but we’ll see how the next couple of months progress. It’s just really hard to get things done when I’m rarely without a toddler who wants my attention (unless I get up at 4:30 or 5 am).

SUMMARY

This year has felt like it took a lot more hours from me for work and management of things. But I also feel like I have more energy now that I’m two years from having our last baby. We have lots of other things planned for this coming year, and I hope to take some even bigger trips to see more of the country now that we have a bit less baggage coming out of the baby years. We have no plans to make any big purchases at this time (although there are new windows needed on our house in the next couple of years), and I really hope this year is lots of fun with the family more than anything else.

We bought an electric vehicle. Honestly, I didn’t see this coming. Since our trip in July, Mr. ODA has been reading about them. He decided he wanted a Tesla for numerous reasons. We test drove one in mid-November, and we picked up our new car order by the end of that week. Tesla was offering 0% financing, if we put $3,999 down. The purchasing process was as easy as buying something off Amazon. I’m still in awe over it. We’ve now added a $589 payment into our monthly finances, but it was worth it for the trade off of interest earned by keeping the balance in our savings account. As part of this purchase, we sold Mr. ODA’s vehicle. It was 15 years old and in relatively great condition. We got much more out of that than we expected, and that check helped cover a gap I had in our checking account (yes, I could have transferred from savings).

I’ve continued to monitor the status of our insurance woes. Luckily everything is complete. I was able to get the new policy executed (after about a weeks worth of work) on the house with the roof that was too old, which meant I had to manage the cash flow between us and a partner. I had to answer a couple more questions on executing a new policy, and we received all the reimbursements from the old policy that was cancelled. I’m happy that’s behind us now.

We have a tenant who hasn’t paid anything towards December rent. Honestly, it’s expected each year. But they seem like good people, and they always work really hard to get things situated, so I’m always lenient with them.

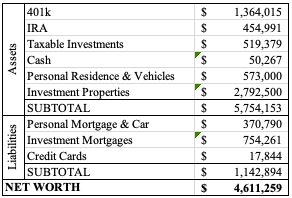

NET WORTH

Well, we bought a new car, paid off a credit card with a $6,500 balance since the 0% interest expired, and added a hot tub purchase to a different credit card, so there was some big swings in our net worth this month. With the hot tub added, our credit card balance went up $6k. Our cash only went down about $600, which was interesting to see. Our liabilities increased with the car purchase, but with our investments, our net worth increased by over $30k.

We bought a Tesla. In the process, they’re offering a 0% APR promotion. They let you see how your credit rating affects your monthly payment (through different APRs). The final column in the table below shows the increase each level adds from the previous level.

This is based on a 60 month term. So, ignoring the promotional option available, between the ‘>720’ and ‘680-720’ would cost you $39 per month. That’s a total of $2,340 over the loan term. By using the promotional rate, that’s $88 per month “saved,” which is $5,280. Don’t let it be lost that working on your credit history and credit worthiness is something that pays off into the future.

When we look into a large sum of money leaving our account, we consider the “net present value” of the dollars. The net present value is the difference between the present value of cash inflows and the present value of cash outflows over a period of time. Investopedia uses the following over-simplified example. “An investor could receive $100 today or a year from now. Most investors would not be willing to postpone receiving $100 today. However, what if an investor could choose to receive $100 today or $105 in one year? The 5% rate of return might be worthwhile if comparable investments of equal risk offered less over the same period.”

The 0% interest loan through Tesla is for about $40,000. Mr. ODA calculated that our net present value of money, based on our approximately 4% savings interest rate, is $36,017. Taking nearly $40k out of our savings account wouldn’t be a financial problem, but it’s not the smartest financial move in our portfolio. Instead, we’re going to pay about $580 per month, while the “balance” of that $40k earns interest. At 4% interest, the balance of $40k earns nearly $1,000 in a year. That balance will continue to dwindle, therefore lowering the interest earned each year, but it’s still a significant sum of money. In the first few years, the interest earned is essentially paying a couple of months worth of the car payment.

By being conscious of our financial standing in the world, we’ve set ourselves up for earning these promotions. Had our credit worthiness been below a score of 720, it would have cost us over $5k more over those 5 years of the loan. While I understand that purchasing a Tesla may be considered a luxury, this concept and awareness can be applied across all financial decisions, which is why I wanted to highlight it here.

Buying a new car is exciting! It’s shiny and clean, and it’s all yours. Well, after a couple of vehicle purchases, Mr. ODA and I learned a few things. And in the end, we’ve decided that buying a “pre-owned” (used…) vehicle is a more practical decision. So while I understand that this approach isn’t for everyone, maybe I can break this down in a way to get you on board.

Whether you’re buying the vehicle new, buying it used, or leasing it, you’re going to have basically the same costs of ownership after the initial purchase. You’ll need to pay for the registration, insurance, and taxes on any of these options. In all cases, you’re going to have to purchase fuel to make the car work. Unless you’re purposefully looking for a new vehicle after a short amount of time and ignoring maintenance, there will be maintenance costs (e.g., oil change, new tires, other fluids). However, the cost of those maintenance activities will depend on the vehicle.

In some states, you also have a personal property tax that may be an up-front tax on the vehicle, or could be an annual tax based on the vehicle’s value. Examples – In Georgia, there’s a one-time Title Ad Valorem Tax that is 6.6% of the fair market value of the vehicle at the time of purchase. In Virginia, there’s an annual personal property tax. Make note of this – the tax is directly related to the value of your vehicle. The more expensive and new the vehicle, the more you’re going to pay to Virginia in taxes – every year. At least each year that passes, the value of the car decreases, and therefore your tax owed decreases.

DEPRECIATION

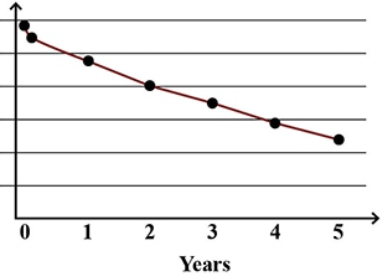

I’ve brushed on depreciation with the mention of a car’s value; that was the biggest determining factor for our move towards purchasing pre-owned vehicles. Depreciation is the loss of value over time. A very literal definition from dictionary.com says, “a reduction in the value of an asset with the passage of time, due in particular to wear and tear.”

While the value of a car decreases each year, it’s not a linear amount of value that’s lost each year. According to Edmunds, a car loses about 20% of its value in the first year. That means that if you spent $30,000 on the car, you probably can only sell if for about $24,000 after one year. Depreciation slows down after that first year, but the value continues to decline.

Source: Edmunds.com Depreciation Infographic

No matter the vehicle, you lose the most value as soon as you drive it off the lot. This is where purchasing a pre-owned vehicle is beneficial; someone else endured that largest loss of value.

You can look into Certified Pre-Owned (CPO) Vehicles, versus just a used vehicle, to give you peace of mind. According to cars.com, a car can only be labeled as CPO after a dealer has certified to the manufacturer that the car passed a multipoint inspection, which can encompass 150 or more items, and repairs have been completed as needed. A CPO vehicle comes with a free car history report, which will show you all the maintenance activities performed, as well as any accidents. A CPO vehicle may even come with a warranty and be in better condition than a non-CPO car. They are supposed to have been reconditioned to like-new condition, and they come with additional benefits that may not be provided on other used cars. But, CPO cars will cost you a bit more on average than a “regular” used car due to this due-diligence and other benefits.

RISKS OF PURCHASING A USED VEHICLE OVER A NEW

When buying a used vehicle, you have to weigh the cost against what you’re receiving (as you would with any purchase, really). Even when buying a new car, there’s no guarantee that it will work perfectly, but you’ll be covered by warranties and (hopefully) a reputable dealership. With a used car, you are taking on a risk that there are issues caused by the previous owner, including not knowing how the car was maintained. Was it owned by someone who followed the user manual, maintaining the right fluids and putting the right gasoline in it? What was their driving style – was it hard starts, stops, and turns with aggression, or was it a gentle, defensive driver that owned it? Was it owned by someone who knew they were getting rid of it in 1-3 years, so no maintenance was necessary in their mind and it wasn’t driven with care?

The question you ask yourself is whether you’re willing to take on this risk of how the car was treated for the cost you’re paying, and what that initial loss of value really means to you.

LUXURY VEHICLES

CPO vehicles began with luxury vehicle lines, but they’re more widely available now. If a luxury vehicle is something you’re interested in, there are some things to keep in mind. Not only does a luxury vehicle cost more up front, the maintenance, and possibly the fuel, will cost more as well. These are recurring costs that you should be considering when taking on the responsibility of a new vehicle.

An Audi was my dream car. I could not wait for it to be my time to make that purchase. Then I started hearing stories about how my friends’ Audis were in the shop. Not only were they costing them for having to be in the shop more than my car, but the maintenance itself was more expensive! I was used to paying $19.99 for an oil change on my Honda Civic in Albany, NY. The thought of paying $75 or more for an oil change because it’s an Audi was gut wrenching to me. Then there’s tires. I paid about $400 to put four new tires on my Chevy Equinox. Tires on an Audi? Double. I didn’t look into the cost of insurance, but usually it ends up being more to insure these sportier vehicles.

I had to truly take the time to consider how much I wanted this vehicle – was it something I needed and would accept the increased ownership costs, or was I ready to let go of this dream?

KEYS TO THE PURCHASING PROCESS

Don’t talk to the salesman in terms of monthly payment. I had quite the experience holding strong to my “what is the total cost of the vehicle” question and not talking about the cost in terms of monthly payment. I don’t want anything buried in my monthly payment. I repeated “don’t worry about what I want to pay month to month or how much I can afford in terms of a monthly payment.” I wanted to buy the car for $17,000. He wouldn’t say yes or no. He kept offering us a different monthly payment, and then we’d sit there, do the math, and say, “nope, that comes to $17,500.” You’d think after the first, or second, time we did this, he’d catch on that we’re not playing his antics and would be verifying the principal of the loan. We were there for hours. Hours. I got it though.

Know what price you want for any trade-in vehicles. When you trade in a vehicle to the dealership, you’re eliminating the hassle of selling it yourself (e.g., how do you market your car, how do you let someone test drive your car, how do you negotiate to get what you want?), but you’re probably not getting top dollar for it either. We’ve traded in two vehicles.The first was straight forward. The second had a fair market value of maybe $6,500 in fair/good condition (e.g., broken antennae, scuffs in the trunk from our travels and house work, a broken door arm rest from where the dog would stand on it to look out the window). Even though the car’s cosmetic issues were factored into the fair market value cost, it’s hard to say we would have been able to get $6,500 selling it personally. When the dealership offered me $5,000, I accepted it. The vehicle looked good, but it was those small details that would add up to any private buyer with a fine tooth comb, and I didn’t think I had a leg to stand on to negotiate over a few hundred dollars with the dealership.

OUR RECENT USED CAR PURCHASE EXPERIENCE

We found our used vehicle through cars.com. There are several online search tools you can use, as well as just showing up to a dealership. My search parameters were fluid: I’m willing to pay for the right value, versus “I have $20,000 to spend, what can I get?” I wanted a van, probably a Pacifica, with relatively low miles (I’m talking about averaging less than 12,000 miles per year), and somewhere around $20k. The Pacifica is set up where the base model has all the features I’d want, so I didn’t have to do a lot more manipulating of features (Chrysler has a lower tiered minivan with less features, versus 6 or more levels within the ‘Pacifica’ itself). The biggest deal breaker for me was leather seats – in that we did not want leather seats. I’d trade off the slightly more effort in cleaning the seats for not feeling extra cold or extra hot when we get in the car (and I have car seat mats under my kids’ car seats that protect the fabric anyway).

The dealership that had the van that best hit our search parameters was just over an hour away. We weren’t able to get there until near closing time, so I rushed through the review of the vehicle. In the future, I plan to do the following better:

Check all doors open and close correctly, without rattle, several times. Drive the car somewhere else, and open and close all the doors again.

If you have removable and/or movable seats, move them. Spend the time figuring it out. I couldn’t figure it out, so I just gave up and said “it’ll be fine.” They’re not fine. I didn’t know it because I didn’t know how it was supposed to work, but after using it a few times, I figured out that one works right, and the other gets the job done, but isn’t ‘right.’

Look for dirt. Don’t assume that a dealer’s deep clean is deep by any means. The car was dirty, but I put faith in their final ‘detailing’ process. They didn’t even wipe the dirt off the driver’s side arm rest or the back wall of the trunk. But they cleaned an obvious orange stain on the carpet.

Drive it on the highway. I get nervous about taking the car too far from its ‘home’ before it’s mine. Do it. See how the car operates at highway speed for more than a mile. Two kids at the dealership, COVID precautions, and it being near closing time meant I rushed myself. There’s a rattle that I should have noticed, but I didn’t drive the van more than a few miles up the road.

I negotiated a buff out of scrapes (maybe as far as gouges) on one of the panels of the van. They said they would ‘attempt’ it, but they weren’t making any promises because the paint was gone. But they did it! The panel looked brand new, and I’m so glad I got something right!

The average cost of a 2017 Pacifica was around $21,000 on these websites (the sites themselves give you a lot of data to see this type of information). The one we went to see was listed just below $18k, so I knew it wasn’t going to be in mint condition. The question is always: what is your tolerance and is the as-is product worth that value to you? It was to me.

We were about to trek all over for two months with a lot of our stuff (like an entire crib and mattress), two kids, and a dog. I wanted the van. During my test drive of the van, I noted quite a few scratches (possibly in the realm of gouges) on one of the door panels. I really didn’t know what I could or couldn’t ask for, so I countered their offer with $17,000, buffing the door panel, and detailing the vehicle. They accepted! I was happy with the imperfections against the price and was now the proud owner of a 3 year old van.

I’m 7 months in to owning the van, and I love it. I got its first oil change a couple of months ago, and the mechanic said the car is in excellent condition and then was surprised when I said I bought it used. We have put the van to the test with all our travel and house work. I hauled 12 sheets of drywall, a bath tub, a toilet, and a vanity with its counter.

STORIES WE’VE HEARD

“I’m looking for a new car because I just made my last payment on this car.” What? You WANT to always have a car payment? Is your car broken or not functioning well? Is it worth purchasing another brand new vehicle, paying the loan for 5 years, and then repeating the cycle? In my opinion, it is not. Try relishing in your newfound $300, $500, $700 each month that you don’t have to pay towards a car. Enjoy the car that you know you can rely on. You’re still paying all the maintenance costs on a vehicle, so you’re not really saving anything, unless you’ve planned it so that you drive so little that your tires last you those 5 years. Another variation: “We get a new car every three years, but it’s ok because we pay it off early so we own it outright.”

“I’m going to lease so I can get a new car every 3 years.” Why do you need a new car every three years? The dealer is loving the fact that they can count on you to rent the car from them for the car’s three most expensive years of ownership, only to give it back to them and do it all over again, and again. Is your goal to keep up with the Joneses or to make solid financial decisions?

LONG TERM COST OF OWNERSHIP

Manufacturers have reputations, based on years of empirical evidence, dictating how long their vehicles usually last and how well they hold their value in the resale market (e.g., Toyota is known for retaining value well). If you can avoid the early stages of a car’s life by buying something a few years old, keep it for many years, maintain it well, and choose a brand that has a strong track record for resale and “car life,” then you can hit the trifecta of a smart purchase.

Mr. ODA is still driving his first adult car. A Nissan. While it was bought new, he has kept it for 11 years thus far and it still runs strong. Each year he owns it, the original purchase price compared to the depreciation to date lowers the average annual cost of his ownership. Since 11 year old cars are depreciating at a very slow rate, if he keeps it maintained, he can save a lot of money compared to the other option of ‘upgrading’ to a newer car that would inherently cost him more money to own each year. Had he bought it 3 years later, it’s possible he could’ve purchased for half the price and still would have owned it for 8+ years while cutting 5 digits off the total cost of ownership. In hindsight, and with our view looking forward, that 3 years of owning it “new” isn’t worth $10,000+.

SUMMARY

The main point here is to be aware of the immediate depreciation of a brand new vehicle’s value. Allowing someone else to take that large value decrease by driving it off the lot can save you money, while still getting a fairly new vehicle. Through Certified Pre-Owned programs, you may even still be covered under vehicle warranties as if you purchased a new vehicle. Or, you can pay still a little less, accept a bit more risk, and get a used car that hasn’t gone through the CPO process. When making the decision on whether to lease, buy new, or buy CPO/used, be sure you’re well informed and weigh all the factors against how this purchase will affect your money, both in terms of cash flow and net worth.