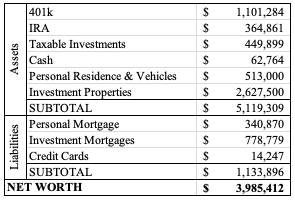

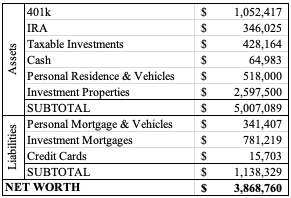

We’re just going to cut to the chase – $4 million net worth! I mentioned that this was a goal for this year. Unlike other years worth of large jumps because of purchasing houses, this was less in our control (granted, our market allocation decisions are what’s driving it…. and by “our,” I absolutely mean only Mr. ODA’s because I don’t do anything in that realm).

RENTALS

Well, we’ve had a quiet month. What’s going to be funny is, I’m going to list the things that we did. Quiet doesn’t mean silent or without effort, but we’ve had a rough go of it over the last year, so this was a welcomed break.

We had termites at a property. We pay $98 annually for their termite warranty program, since we found extensive termite damage and live termites when we bought the house. We’ve had to treat the house several times, so this $98 is a steal. However, I’m wondering why we keep needing to treat the house.

We paid $125 for a plumber to go out to a clogged sink. When we received the invoice, it was for 2 plumbers to go. Between the phone call that they were on their way and the tenant saying they were great, only 35 minutes had elapsed. The company charged us almost $300. Mr. ODA called to ask why they choose to send two plumbers to do a one-man job, while also charging us for it. The owner said it was for liability purposes, which Mr. ODA fought back on. They agreed to a reduced rate, but we were only charged $125, which was less than agreed upon.

We had our third tenant move in, after we unexpectedly had to turnover three houses in the middle of winter. We also were given notice by another tenant that she’s vacating by the end of March. We handled increases for two houses (one handled by a property manager to increase $50/month, and one handled by me to increase by $25/month).

We had one tenant pay on the morning of the 6th with no communication, so I did have our property manager let them know that’s not going to be ok. We also had a usual suspect pay late, with the late fee. However, their communication was frustrating. They said they’d pay on the 6th. At the end of the 6th, they said the money hadn’t cleared like they expected. No communication on the 7th. I asked for an updated on the morning of the 8th, and they said it would be that day. At 11 pm, I hadn’t received anything and reached out. I was then told that money was going into the ATM right then so that she could pay. Sometimes I wish I could do a deep dive into tenant finances so that I could help them out.

PERSONAL

Mr. ODA has a trip in July where a group of guys will hike in the Rockies. Our family is going out before that trip is scheduled to do our own exploring. We booked 4 round trip plane tickets, and Mr. ODA handled the lodging booking for the guys’ portion. That’s almost $3,000 worth of purchases, so our credit cards are higher than usual.

Speaking of the plane tickets. We purchased gift cards from Costco for Southwest. The gift cards are essentially $450 for $500 worth of purchasing power at Southwest. We bought two, therefore saving $100 on the tickets. For an extra few clicks on the computer, and the 15 minutes waiting time before the e-gift cards were delivered to my email, that’s $100 that can be used somewhere else.

We bought a new vanity for our bathroom. That was about $700 for the vanity, faucet, toilet flusher, and mirror. I sold the old vanity (in rough shape) for $30. And because I’m proud that I did most of it on my own, here’s a picture. I needed Mr. ODA’s help with the supply lines because I lost patience with how tightly they were screwed on and my lack of progress. I cut the baseboards down to size, except I somehow measured wrong on one quarter round cut (I was cutting while it was on the wall). Mr. ODA cut and installed the replacement piece for me.

We finished up the ski season. The kids did great. I was really proud of them for sticking with it. We used our season pass well (i.e., exceeding the cost had we bought individual tickets for each visit). I took two of the three kids to the aquarium, and we took the baby for a procedure at a local children’s hospital. We’ve started tee ball for our oldest. Our March is very full and busy, so we’re getting into the swing of things and keeping track of the schedule.

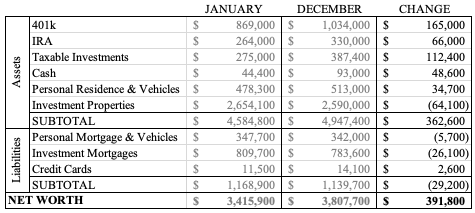

NET WORTH

Well, we far exceeded that $4 million goal. The market went up big, with our biggest changes being in our retirement account, IRAs, and cash. Our cash increase is offset by the lower amount in our Treasury account. Some of the short term bonds were transferred back into our savings account, and we’ve kept that money in savings since our deck replacement is slated to begin.