This house was purchased in 2018, and it was actually purchased by our Realtor and friend, under the plan that we would formalize the partnership after closing. Mr. ODA had been searching for another investment property, but we had 10 mortgages already (9 investment properties and our personal home), which is a Fannie Mae cap (see the Selling Guide, section B2-2-03). One of our loans was a commercial loan, and we had hoped that it didn’t count against the 10 mortgage limit, but it did. Fannie says that the cap is the number of properties being financed, regardless of type, when looking to originate a new loan. Our Realtor had one rental property on his own and had mentioned how he wanted to purchase more properties to create an income stream through that option.

Mr. ODA and our partner went to see the house without me in March 2018. After the initial visit to see the house, they requested the information for the tenant that was living there. We received their applications, current lease, move in check list, and rent roll. They had started living there October 1, 2015, and while they had been late, they had always eventually paid rent with the late fee. During some of our initial searches, we had someone tell us that rent on the 6th was more profitable because they’re pay with a late fee. While we don’t encourage late payments (and we’re actually really lenient with late fees in general), this eased our tension when we saw late payments.

The house is a 4 bedroom, 2 bath, with a fully finished basement. The condition of the house was probably slightly lower than what I would have accepted based on the pictures, but I hadn’t seen the house in person. I actually had only seen one room of this house before our walkthroughs this past July. Our partner and Mr. ODA said that the pictures didn’t do the house justice, and it was worth purchasing.

After our partner purchased the house in April 2018, we established a Limited Liability Corporation (LLC). My last post goes through the details of why we established an LLC for joint ownership, but we don’t use LLCs for our personally owned properties at this point.

LOAN TERMS

We requested three different options for the mortgage numbers: A) 20 year fixed with 20% down was 5.125%; B) 20 year fixed with 25% down was 4.75%; or C) 30 year fixed with 25% down was 4.875%.

All of the options included ‘points’ without us being told upfront or requesting it. We questioned the reason for the quotes having these points and were given a half-hearted response that sounded sketchy. We ended up with a 30 year fixed, no points, and a rate of 4.875%. There wasn’t an incentive to go with a shorter loan (and therefore a higher payment each month) at a higher rate just to put 20% down. We went for the 30 year instead of the 20 year to increase our cash flow opportunity since we have a partner on the house and are only getting 50% of the income and taxable expenses.

PARTNERSHIP

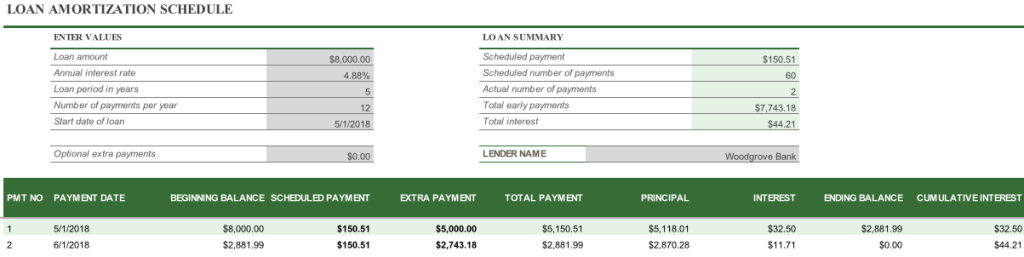

Our partnership actually started with a loan for the down payment of this house. Mr. ODA and our partner agreed to allow us to pay him back over time for our 50% of the closing costs. We didn’t have the amount needed liquid, but we knew we could make up the amount owed over a short period of time instead of liquidating money from our investment accounts. We were able to pay most of what was needed for his closing, but we “took” a loan from him for $8,000. I used a loan agreement template that I found online and manipulated it for our purposes.

We established the loan terms to be the same as the mortgage he was entering into (4.875%). Most personal loans are for five years, so we chose that timeframe, even though we knew we’d pay it off much earlier than that. We could have just agreed to the terms and not documented it based on our relationship, but I’ve always felt better having things overly documented. I was basically an auditor in my career, and I’ve seen how “gentlemen’s agreements” over rental-related things haven’t worked out. I formalized the process through this contract and had all of us sign it. While the contract was mostly for our partner’s benefit (to make sure we paid him and he received interest), this was the only documentation we had that once he closed on the house, he then had to give us 50% share of the property ownership.

I established a simple amortization schedule through Excel’s templates. We established the loan terms as 5 years (60 months) at 4.875% (same as the mortgage being executed). When I made extra payments to him, I logged them in the spreadsheet. We only made two payments to him, but he made $44 for not having to do anything except accept our money. 🙂

We had to establish an LLC to be able to claim the tax benefits on this house for our 50% share. The attorney required us to have the tenants acknowledge the transfer of ownership to the LLC since we hadn’t executed a new lease in our names. The attorney then took care of the establishment of the LLC with the State and transferring the deed of this house to the LLC.

RENT COLLECTION

We’ve had the same tenants since we purchased the house. We inherited the tenants, who had moved in 2.5 years before we purchased it, and had rent established at $1300.

As a reminder, we purchased the house in April 2018. They paid that July’s rent late, and despite reminders about the late fee, they didn’t pay it. And so began this constant story with them. The main frustration was that they wouldn’t tell us to expect rent to be late, so we kept having to follow up with them. After two months in a row of it being late at the beginning of 2019, Mr. ODA actually explicitly said: In the future, it’s better to communicate issues with rent payment up front to see if there’s an opportunity for us to work with you. We had been lenient and informally requesting the status of rent, but this was their warning that we’d be sending notices of default going forward.

In January 2021, we hit a wall with rent payment. I sent the notice of default on the 6th of the month like usual. However, because of the pandemic, I had to adjust my verbiage to highlight all the rent relief options available and remove the late fee requirement. My understanding is that a late fee can still be collected in Virginia, but I can’t proceed with eviction just because they don’t pay the late fee portion (which isn’t something we’ve ever held any tenant to regardless). While the rent payment is typically due within 5 days from notice, Virginia now required me to give them 14 days to request a payment plan or pay rent owed. We then had to text and email them several times and never got a response. I finally sent an email with the following at the beginning:

We are very flexible landlords and willing to work with all our tenants. However, we are unable to work with anyone who does not preemptively share possible rent payment delays nor respond to requests for information. Please respond to this email by noon Sunday January 24, 2021 or pay the rent owed by that deadline to prevent proceedings for eviction filing with the court.

Virginia was very lenient with rent payment throughout the pandemic, but they were also fair. The lack of response from a tenant or the tenant not working with the landlord didn’t protect them from eviction. I finally got a response that the rent would be paid that week.

Since then, we’ve been told that rent will be late. We’re simply sent an email that says “you’ll receive rent on 2/12. Sorry for the inconvenience.” It’s as if they feel they have the upper hand and control. We hadn’t received any late fees until I finally sent an email in response to their “you’ll receive rent when we get to it” email for August’s rent that there’s a late fee due.

In 3 years, they’ve been late 14 times. When I put it in that perspective, it doesn’t seem that bad. In the moment, it seems like it’s a constant battle with this house. That’s probably because a majority of our houses pay rent without making it a painful process!

RENT INCREASE

We hadn’t raised rent in the 3 years we owned the house, and they had been paying $1300 since they moved in on October 1, 2015. That’s a great deal for them! Depending on our ownership costs, we would typically look at raising rent every 2 years, and likely around $50. We’ve raised the rent on only 2 tenant-occupied houses we have (meaning, raised the rent on people who continued living there, versus raising it between tenants); both were rented under market value when we inherited the house, and both have received a $50 increase every two years. We typically raise the rent during vacancy times, which has worked out pretty well for most of our other properties.

For a 4 bedroom and 2 bath house, $1300 is low. We mulled over our options. The house is currently on an October 1st renewal, which is a poor time to be looking for new tenants. I wanted to get the house on a spring lease moving forward. My original proposal to our partner and Mr. ODA was to offer them a 6 month lease (ending 3/31/22) at $1400. Our partner said we should include our expectation that we’ll be raising the rent to $1500 for a year long renewal as of 4/1/22. I struggled for weeks on the verbiage for this double proposal. Eventually, Mr. ODA said we should just risk it. We should lay out an 18 month lease at $1450 to split the difference, and if they don’t want it, they can leave or attempt to negotiate.

We offered them just that, and they accepted. Of course, true to form, they were a week late in meeting the deadline to sign the selection that they want to continue living there at the increased amount. Now the rent will be $1450 as of October 1, 2021, and their lease will run through March 31, 2023.

MAINTENANCE

We started with a clogged drain right off the bat. We had our partner go over there and try to unclog it with store-bought items, but it didn’t work. We ended up hiring a plumber for $300 to work on it. We’ve had several plumbing issues in this house, including a clogged sink that backed up and flooded the kitchen and basement. We ended up needing to have the line jet blasted and a camera put through it for $550! This plumber’s quote for the ‘fix’ was $6k. Mr. ODA sent the video footage to another plumber, and that guy said he didn’t see that anything was needed, so we didn’t proceed with the ‘fix.’ The jet blasting appears to have worked, and we haven’t had any damage reported. The other plumbing issues included fixing leaks in the basement bathroom and replacing that toilet.

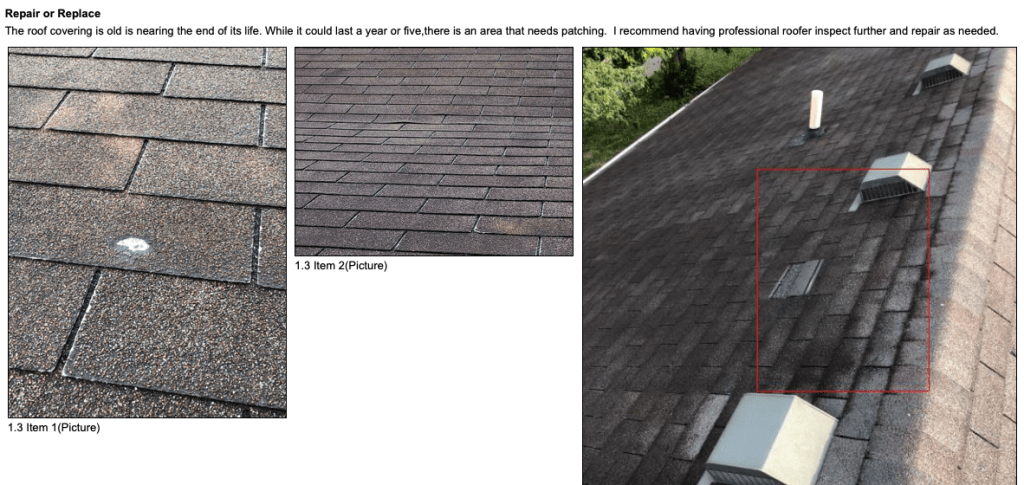

The inspection didn’t identify active leaking on the roof, but our insurance company was hounding us over the condition of it. We ended up sending our roofer out there to do the items that came up on the inspection report. This was $350.

We then had several more issues with the roof that cost us $125 before we just decided to replace it. The replacement was quoted at $5,500 and surprisingly that’s what we paid. We expected to have additional costs for plywood replacement due to all the damage we had seen.

Interestingly, while not communicating about rent nor paying rent, they felt the need to tell us the washing machine wasn’t working. We ended up replacing the washing machine for them. We try to not supply any non-required appliances because then it’s on us to fix them or replace them, but since the tenants already lived there when we bought the house, we inherited that the washer and dryer are our responsibility. More interestingly, as I was writing this post and going through my receipts, it dawned on me that the washing machine that was in the house when I did my walkthrough last month isn’t the one that we just sent them in February.

While collecting rent has been frustrating with this house, and we’ve had a lot of plumbing and roof expenses, the house is still profitable and worth our investment. The house is in an area of Richmond that’s being revitalized, yet at the same time it’s in its own pocket of the city that’s also protected from big changes and is mostly original owners. Appreciation has really taken off, so even though our maintenance issues have eaten big chunks out of our cash flow, this house will be well worth it when we eventually sell it and move on to a new investment.