Our church had a series about “taking significant steps toward financial freedom.” In their terms, financial freedom doesn’t mean FIRE (Financial Independence, Retire Early), which is usually what we’re referring to here. They mean that they want people to be free of financial burdens and not “bound up” by finances. Mr. ODA and I have been in control of our finances for a long time now, so this isn’t teaching us much about what to do differently. However, I’ve enjoyed learning their perspective and have several take aways to share.

Many have heard of Dave Ramsey when it comes to christian-based financial teachings. Dave tells you to pay off all your debt and pay cash for everything. We disagree with that approach. Debt is not bad when it’s used responsibly and you’re being a good steward with your finances, and that’s what our church’s lesson is too.

People seem to think it’s ‘cool’ to talk about how ‘broke’ you are. And yet, it’s taboo to mention if you’re in a good position with your money. What if we made it so that you’re taught that when you find someone in a better financial position than you, you ask questions and learn what decisions got them to that position?

The lesson is how to manage your mentality with money. It’s not about restricting your spending or making you feel guilty for buying your coffee, but it is about how you make informed decisions day-to-day that grow you towards a position where money isn’t controlling every aspect and decision of your life in a stressful manner. If you take control of your money, instead of your money controlling you, you’ll work towards eliminating that stress.

THE WHY

The workbook starts by asking you to determine your net worth. Money-in minus money-out is your cash flow, while assets minus liabilities are your net worth. The goal here is the gauge the current status of your money and where you should probably plan to be. There’s also an exercise where you determine your motivation. Are you motivated by freedom from financial burden, having a feeling of security, having power, or through love and giving? When you determine your “why” behind making money, you know what direction to go.

Making more money isn’t always the right answer. To make more money, you may need to take on a second job or more hours at your current job. Is putting that time in worth the extra money that you’ll bring in? Will putting those extra hours in make you more happy? If not, perhaps decreasing expenses is that way to go to make ends meet. If you don’t have the ability to take time for yourself or do things that bring you joy or have “down time,” then it’s not worth taking more time from your week.

I quit working in May 2019. Since then, I’ve done odd jobs just out of excitement, not financial need. I learned different industries and only had to commit part time. I was recently feeling the pull to find another part time job. There’s a consignment sale that comes into town twice per year, and they were hiring. They said they pay $8 per hour with at least a 4 hour per shift commitment. The consignment sale is being held 30 minutes from my house. That means that a 4 hour shift requires me being out of the house for 5 hours. The gas to get there and back would cost me about $7 per day. That means I’m out of the house for 5 hours (away from nursing my baby and being with my kids) for $25 before taxes. That cost/benefit ratio was not worth it to me.

THE PLAN

My favorite analogy given was to a plumber. A plumber doesn’t just start laying pipes in walls and hope it works out. He will have a plan of how to get water from the source to the faucet. Without that plan, how would you know that the water will get to where you want it to go? Same with money. If you don’t have a plan for your money, how will you know that it’s going to the right places with minimal effort? Without a plan, that’s where the stress comes in.

If you’re worried that you’ll be able to pay your electricity bill, then money is controlling your life. Sit down and make the plan. Allocate funding to the necessities first. It’s ok to eat at a restaurant or buy a coffee, but is putting your money towards those expenses creating financial freedom or causing more stress?

Mr. ODA and I have a money-spending mentality, rather than a budget. In my opinion, when you create a budget, you’re either looking to spend everything you’ve set aside in that ‘envelope,’ you’re willing to move money around without discipline, or you think of left over money in that ‘envelope’ as a bonus and you spend frivolously. If you put $500 for the month’s groceries in an envelope, but you only spend $450, what are you doing with that $50? I’ve seen it happen plenty of times that someone splurges. Instead, Mr. ODA and I weigh every single purchase. Literally every purchase, I swear. I told the story about my weighted tape dispenser.

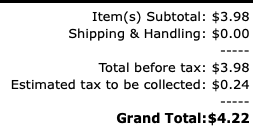

Every single year, I sit on the floor and wrap Christmas gifts. I don’t seem to notice during the year when I’m doing birthday gift wrapping (or perhaps I’m quick to grab a bag instead of wrapping paper for those instances), but at Christmas it’s apparent. I need a weighted tape dispenser. Having to find the tape on the floor in a mess, then having to use two hands to get a piece of tape off the little plastic dispenser, is just so much stress. It was YEARS of thinking “I need a weighted tape dispenser. Nah, I don’t need it for just this one week every year.” I finally bought one. It was $4.22. I agonized over this purchase because I didn’t feel it was truly a necessity and it turned out to be less than $5.

Grab your bank account statements and credit card statements. How much money did you spend? In what categories did you spend that money? Was it for necessities or was it spending that creates a strain on your ability to pay the necessities?

This is an exercise worth doing if you feel you’re drowning. I see posts daily in my mom groups that people say they make “good money,” but they can’t seem to pay the bills. I want to intervene. “Did you stop at the gas station on the way home from work to get a gatorade?” You could buy a 16 pack of gatorade, put it in your refrigerator, and have it waiting for you when you get home, which is probably about the same amount of time for not stopping at the gas station to make that inflated purchase.

So many people don’t seem to realize how fast those daily, small expenses add up. Ask yourself if there’s a better way to get such gratification, but in a way that furthers your dollar earned. Create the habit of weighing each purchase, determining if it brings you joy, and then either walking away or purchasing it. Know that if you purchase it, that will have ripple effects. So if you’re worried about paying that electric bill, then that instant joy gratification wasn’t a step towards financial freedom, where money isn’t controlling you.

I manage all our income and expenses (at a high level, like credit card payments, not individual line items). I have a spreadsheet that I set up in 2012 and have used religiously since then. I’ve shared how I set it up in the past, but we’ve entered a new phase that makes my spreadsheet even more important to me.

BACKGROUND

FIRE. Financial Independence, Retire Early. This isn’t a post about FIRE specifically, although it’s the movement that sparked Mr. ODA to go down our financial path.

The purpose of our rental portfolio was always for both Mr. ODA and I to quit working. We had covered my income before any kids were born, but I kept working because there was no reason to not be working. Once our son was born, I took 14 weeks maternity leave (not a separate bucket for Federal employees back in 2018; it came out of my own accumulated sick leave), then I worked about every other day for 8 months while Mr. ODA and I swapped child care roles, and I burned down my leave.

While we don’t plan to work full time, we do plan on keeping part time positions. We’ll work on things that bring us joy, rather than an office job with office politics. Since I stopped working, I’ve done odd jobs, part time. For example, I worked as a census taker and served beer at a local race track over the last 4 years. These were all seasonal, part time positions, with no long term commitment.

Now that I quit working, it’s Mr. ODA’s turn. We hardly skipped a beat when we left my six-figure salary behind (although a pandemic probably helped curtail spending on our behalf!). However, the thought of losing his salary as a safety net and losing insurance are two items that have caused some pause.

THE SPREADSHEET

For you to understand my panic that I’ll get into here, I thought a quick reminder was necessary. This is how I manage our money. It’s nothing fancy, but it works. I don’t miss payments. I can allocate expenses to a specific 2-week period against what income is brought in at that time.

There are two parts to the spreadsheet. Well, there are about 10 tabs, but this first tab, with two sections, is what’s pertinent.

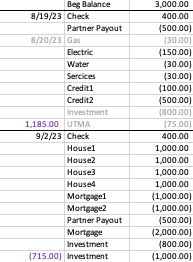

Part 1 is this section. This image is a very scaled down version of the section. We have 13 houses, 6 mortgages that get paid, 6 credit cards that get paid regularly, and a few other lines that I removed.

All numbers are made up place holders, except the investments. I deleted my IRA contribution line because it’s wonky (but I will max out IRA contributions), but I wanted to show how much we’re investing regularly. There’s $75, per kid, per month, going into their investment accounts. Then there’s general investing happening with one $1000 transaction and two $800 transactions per month. Mr. ODA is investing into his IRA to max it out ($6500/12=$541 per month..sort of).

You can see that I’ve listed Mr. ODA’s pay dates at the top, and then his salary income on the next line. The gray section accounts for all rental income. I’ve allocated the income into the salary two-week period that makes the most sense (about half pay me on the 1st or 2nd, and the rest pay on the 5th). The green section shows routine rental property expenses. The entire next section are our personal expenses. The blue is left over from when I was managing two personal homes last summer (but kept it to differentiate our house bills versus other bills). The next gray section (which I’m only just realizing is a second gray and should be a different color as to not conflate the two grays.. what a rookie mistake) accounts for expense that come out of Mr. ODA’s bank account. Finally, I have an “other” section. This is where I capture large expenses that don’t need their own line item because they only happen once or twice a year. Here I’ve put tax payouts that will be due in October (that’s 4 houses worth, and it’s last year’s numbers – because I want to know how this year’s amount owed, when it comes in, changed from last year’s to discern if it’s reasonable or if I need to dig into it).

This is part 2. Now, part 1 accounts for the general timing of income and expenses, but it doesn’t perfectly capture the due dates, scheduled payments, or whether I’ve paid it and it’s hit the account.

The top line is linked to the section that I update our checking and savings account balances. Then I transfer all the items per pay period into this list format. In this example, let’s say I’ve already scheduled the gas payment. So I mark it as gray and put the date in the left column. Similarly, our investments are automatic, so I mark them in gray as we get to that two-week period.

At each border lined, I put the total for that section. You can see that at the end of the 9/2/23 pay period, I project a negative balance. Truly, we seem to have more income than I project (rewards cashed out, someone paying partial rent a little early, etc.), so I don’t take any action until I need to. There are Federal regulations regarding savings accounts; so we can only make 6 withdrawals from the savings account before fees apply. I manage these projects to know whether I need to make a withdrawal. If I need to, then I project what other expenses I may have and transfer a little more than I deem necessary.

THE PLAN

So our first step to him leaving is to pretend we don’t have his salary. Mr. ODA set up a new bank account. The majority of his paycheck goes into that account. We still have $250 going into another account, and about $400 going into a third account because we need to meet the requirements of direct deposits to prevent any account maintenance fees.

Our general principals in account management was always to take money into our main checking account, pay out bills for that two week period, and put the balance into savings. However, that wasn’t creating any forced feeling of managing without Mr. ODA’s salary. I’m more of a visual learner, so I appreciated this concept of having the money automatically transferred to a completely separate account.

EXECUTION OF THE PLAN

The first month of this plan had me on edge. The accounting in the checking account meant I was constantly back down to a balance of about $500. When I worked in an office, I was at the computer everyday checking our money. Now that I’m responsible for 3 tiny humans, I’m rarely on the computer. I project out our routine expenses, but there have been plenty of times where a $100 or $500 charge goes through that I didn’t have listed in my expense column for that period. Therefore, I like to keep at least $1000 as a buffer in the checking account to cover those little expense that can add up. So keeping the projection to less than $500 in the checking account panicked me.

Now wait. It’s not that we only had $500. We have a savings account linked to that checking account. We have this online account that’s taking Mr. ODA’s salary and just building the balance because we don’t use that account for anything. We have Mr. ODA’s old personal checking account. And last but not least (as my adorable 3 year old says all day long), we have plenty of investments that can be liquidated within 24 hours. We have the money. It’s just the panic of having the money in the spot where the bills are being paid.

SUMMARY

I’m sure there are easier ways or “better” ways to account for this. I don’t like automatic payments for bills because I like scheduling them against our cash flow. I’ve used this exact set up since 2012, and it hasn’t failed me. Taking full responsibility to pay bills means I am very scared to miss a payment and cause a negative hit on either of our credit reports.

Now that we’ve eliminated about $5,000 per month of income, without changing our spending in any way, I’m interested to see how things go. We have a great spending mentality – we’re not spending on frivolous items and we weigh the cost benefit of a purchase to us. That’s not to say we can’t do better. I’m sure we can be more diligent about our grocery spending or at least cooking what we already have in the house (we don’t spend much at restaurants in a month). I’ve already started tracking our expenses month to be sure we can watch our trends and re-evaluate our spending if needed.

Now that we have this account growing with no need for it to pay the bills, we will use it for fun things. We’re not very good about doing fun things. Two summers ago, we wanted to buy a vacation home at a nearby lake. We decided that instead of spending $1200 per month on a mortgage to go to the same place all the time, we’d plan vacations each month and spend up to $1200 without “guilt.” It was great. We had so much fun. But it lasted 3 months. Having a newborn put a damper on activities, but we’re ready to do the same again.

The common goal in the FI/RE (Financial Independence, Retire Early) community is to reach a point where your net worth is 25x your annual spending, meaning your expenses are 4% of your net worth. This is an extreme oversimplification of things because of the number of variables associated with where your net worth might be, and how to access it. For example, retirement accounts have requirements to be met before drawing funds; while you may have hit the 4% expense to net worth ratio, it may not mean that you have that money liquid to cover your spending.

When the ODAs started down the path of FI/RE, we did it with a real estate rental portfolio. This path of net worth growth really doesn’t fit the traditional mold. It provides regular cash flow, rather than an account with a balance that’s drawn down.

As mentioned in previous posts, there are numerous ways to make money in real estate. The path we have taken is probably one of the simplest and most repeatable for anyone. We own a portfolio of single family rental houses, most of which were bought straight from the MLS. These basic properties are in basic neighborhoods with regular tenants. Nothing special. We acquired these properties by focusing on the 1% rule in real estate – try to secure 1% of the property’s purchase price in monthly rent. Another oversimplification of how things really go, but if we were able to find a $100k property that rents for $1,000 a month, we know we’re going to make money long term.

For these properties, we typically put 20%-25% down and finance the rest through a conventional mortgage. We find a tenant, and then the 4 ways to make money in real estate go to work for us: appreciation, tenant mortgage pay-down, tax advantages, and most importantly for our situation and FI/RE – cash flow.

I want to talk about how we can reach a FI/RE number through real estate cash flow differently and more quickly than using traditional stock market investing.

The $100k house had a 20% down payment and mortgage rate at 5% interest, which brings the monthly principal and interest payment to $429. Add another $121 for taxes and insurance (using round numbers here!), $100 for maintenance and capital expenditures savings, and $100 for a property manager; this comes to $750 worth of monthly expenses. At $1,000 per month of income, you have $250 per month of cash flow in your pocket. $250 per month equates to $3,000 per year of cash flow. With the $20,000 down payment and about $5K in closing costs, it means that our $25k investment nets us $3k per year in cash flow.

Circling back to the 4% rule for stock market investments, $3k in cash flow requires a savings of $75k. But we only had to invest $25k! We’re banking on the monthly cash flow, rather than a “stagnant” savings.

We took that math and ran with it. Our rental portfolio has 12 houses in it. While we’ve shown in prior posts that each house’s numbers aren’t as clean and simple as this example (some better, some worse), if we take that $3k annually and multiply by the 12 properties, we have $36k in annual cashflow for only $300k invested.

What would you rather need to produce $36k income – $300k or $900k?

Can you scale a rental portfolio to reach enough annual cashflow such that you can live off the cash flow?

Rental property investing is not completely passive. We have tenants to manage, properties to maintain, property managers to manage, income and expenses to track for taxes, lending efficiencies to explore, and the list goes on. But if you’re willing to put in a little work to reach financial independence (the FI part), you can do it substantially faster by finding strong properties to provide significant cash flow than if you were to take the totally passive route of simple stock market (index fund) investing.

Note, there’s nothing wrong with that – we have a substantial position in the stock market due to the tax free growth benefits of retirement accounts. The power of real estate investing saw our net worth grow faster than we’d have ever dreamed since we bought our first rental in 2016. The proof is in the pudding and we advocate to anyone to just get started!

I left my career exactly two years ago (on the 8th). My son was 8 months old. Honestly, I could have left my job years prior thanks to what my husband set up for us, but without kids, there was nothing to fill my time. I enjoyed my work a lot, so every day worked was another day of money ‘saved.’ I now have two kids and haven’t looked back. I’ve ‘retired,’ but I haven’t stopped producing some income in addition to managing our finances (although I managed the finances while employed full time also).

First, some background of my career.

When I first started working, I was very driven. My goal was CFO by my early 30s. That seemed crazy, until our CFO stepped in shortly after I started working there, and she was 32. Goal marked. I was on the General Schedule pay for the Federal government. I started as an intern in 2007 (GS-4) and joined the training program (GS-7) that gave you a salary increase every year (with acceptable performance) until your position’s max (GS-12 by 2011). I needed to devise a plan that got me to a GS-15 as fast as possible because in 2011 I was 25 years old, which meant I had 5-7 years to climb 3 grades (which takes at least one year in each grade). Not a lot of wiggle room. Well, I soon realized that there was more to life than climbing the ladder as quickly as possible.

I met my husband at work, and we ended up moving to DC for personal reasons and took a GS-12/13 (this means that I started the position as a GS-12, and after 52 weeks ‘in grade’ with acceptable performance, I was promoted to the GS-13 – in theory, not practice). I was warned that it would be an uphill battle to go from the 12 to the 13, and it wouldn’t be as easy and automatic as it had been to get to the GS-12. Commence years of frustration and extremely poor communication from my leadership on expectations. Without getting the promotion within my position, I applied for another position within the same office, and I got it. This was a GS-13/14. I never got the 14.

My experience within the CFO’s office was so hard on my psyche, and I felt that being a young female, rather than my excellent experience, production, and reputation, were playing into the decision making by my leadership to not promote me. I left and went “back into the field” instead. That position was a GS-13 with no promotion potential within that role. By that time, it didn’t matter to me. I didn’t want any more responsibility than what I had; I enjoyed the work I was doing.

My experience in the CFO’s office taught me that I preferred to be at home with my family and experiencing those things. Before my relationship with my husband, I didn’t realize how much I wanted to spend time outside of work traveling, playing sports, and being with my family.

MY LAST DAYS

When my son was born, I took 14 weeks off work (using my own built up leave since at the time the government didn’t provide maternity leave). The typical 12 weeks got me to just before Thanksgiving, and then I worked one or two days per week until after Thanksgiving. The goal was to work and burn my leave to zero before quitting instead of being paid out on it. If you’re paid out on it, then the tax bill hits hard and all at once. Plus, by burning the leave while still employed, I gained even more time off to burn during those pay periods, more 401k (TSP) matches, and added a few months to my back end pension calculation.

Based on my leave balance, being responsive at work, and managing child care, we first set a goal of January. Then, my husband pointed out that January and February had holidays, and I should try to work through those holidays to get those ‘free’ days off. The goal became March because March is long and without any holiday time off! Well, the Federal government shut down that winter for several weeks. My husband’s job was affected by the furlough, but my type of position was funded through a different mechanism that meant my agency still worked (and if you want a lot of detail on that, I’m always happy to talk about it, but I won’t bore the majority here 🙂 ). So I worked full-time while he stayed home with our son. This meant I wasn’t using my leave, so I could work the part-time schedule longer once he went back to work. We then set my goal for May. I probably could have made it longer, but I was afraid that if I got near Memorial Day, he’d say “work through that holiday,” and then 4th of July wasn’t too far away, so I forced my last day to fit.

I had a such a good reputation for the work that I did, that I still get asked questions by friends I made in the position. Plus, I help my husband get through some work things here and there since his position is similar to one I used to hold. I miss the work, but I don’t miss the office politics and red tape, so I’ll take these random questions from friends!

WHAT AM I DOING IN RETIREMENT

There are days that I miss the work I did. I certainly appreciate the flexibility we have now.

FLEXIBILITIES & MOBILITY

We had the opportunity for my husband to work in KY for the summer after I quit. We were able to capitalize on the per diem given for living away from your duty station, and my son was able to spend time with his cousins. I also learned to be extra grateful for our normal-sized house and that I wasn’t trying to live in a one-bedroom apartment for very long.

Since my husband’s job required fairly frequent travel, my son and I were able to join him for those work trips. We went to Orlando and Glacier National Park together! We also took several trips just for fun, like to the Braves Spring Training games.

Pandemic life made us realize that we wanted to be closer to family earlier than we had intended. We loved our neighborhood, and the schools were going to be great, but having to isolate from people for so long was hard. It was also a logistical nightmare to get things done sometimes without family to help watch the kid(s) in a pinch. Since I’m not working, we decided to move to KY to be near Mr. ODA’s family – a lot earlier in life than we had intended. We discussed the possibility in May, discussed it more seriously in June, had our house listed in August, and closed on it in September. Nothing like a hasty decision with a newborn and no house lined up to move into on the other end of this decision! But had we both been working and both needing to be employed once we moved, we wouldn’t have been able to make such a move as quickly as we did. You can read more about these decisions in my ‘Moving States’ series posted recently.

It’s been nice to be able to do activities with the kids during the week when things are less crowded. Sure, a pandemic limited our options for the last year, but we still have more freedom. I enjoy seeing all the things they learn in a day. There are hard days where I crave more adult conversation or the ability to sit quietly and get something done without being asked for the 90th snack of the day, but I still wouldn’t go back to work.

WORKING

I’m the type of person that wishes I knew the inner workings of so many things and have a strong desire for efficiency. When I took my first job in DC, I kept pushing that I wanted to bridge the ‘headquarters’ and ‘field’ communication gap. For instance, there was a process that the field would submit to headquarters for action. Headquarters had their own internal process of tracking and executing it, but the field didn’t know that process. Therefore, headquarters spent a lot of time answering “what’s the status of my request” type emails. I explained the process to the field, and then we were left to spend more time processing the actions than managing questions.

All this to say: I’m quick to jump at new opportunities where I’ll learn something. I like knowing the process for things and find these details help me better connect with other people. While not being employed full time, I’ve kept my eye open for short term and part time opportunities to do something different.

ENUMERATOR

In February 2020, before the pandemic started, I applied to work for the US Census. We don’t “need” the money, but it gave me something to do that’s different. The application said Census field work was expected to be conducted in April and May. This was going to be hard since my daughter was due at the beginning of April, but I figured I wanted to be in the mix for information instead of assuming I wouldn’t be physically able to do work. Well, the pandemic delayed everything. I didn’t get any information until June, went to training, and then started work in July.

I was able to set my schedule in advance, which was nice. I learned at the beginning that it was hard for me to manage pumping and for my husband getting our daughter down for naps. So I changed my future schedules to be in 2-3 hour segments so that I could go home to feed her and put her down for her next nap. I was given a cell phone that had my work assignments (addresses to collect census data) and my day’s hours. I went door to door trying to gather census data from addresses that hadn’t responded. Most people didn’t answer their door, which meant that I probably had to knock on neighbors’ doors until I could identify at least the number of people who lived at the address in question. That was probably the hardest part because I would introduce myself and immediately be met with “I filled mine out!”

The work was in my geographic area. The furthest I had to travel for my assignments was 25 minutes. We ended up moving out of the area in September, so I missed several opportunities to work more, but most of the work was dwindling by then (the work started to send us further and further from our ‘home base’… even an ability to go to other states).

Honestly, I wanted to be the number crunchers in the office, but that position wasn’t available. I thought if I started with the field work, I could get my foot in the door. Our move hindered that a bit, but I’m glad I did it. I learned how the Census gets tracked. I made some money. I have some good stories (encountered several types of animals, including being surrounded by two large dogs that got my adrenaline running; left a few houses because my gut said it wasn’t safe). The application used to track information needed help, as it assumed we were all working in cities, whereas I was usually out in the country (e.g., no close neighbors). I boosted my confidence with glowing remarks from my supervisor since I put more than bare minimum effort in and was efficient in getting the work done.

the giant dogs that circled me, but eventually let me back in my car

SEASONAL CHANGE RUNNER

A local race track had thought that a limited number of patrons would require less staff. Unfortunately, once the race meet started, they were surprised at where their deficiencies were. Less patrons doesn’t necessarily mean less activity at concessions and bars, for example. Mr. ODA and I were approached about an opportunity to fill this gap. We’d have to be ok being on our feet for 6-8 hours, pass a background check, and pass a COVID test (interest fact: this is my only COVID test I’ve taken).

The race meet is only 15 days. We were approached after the races had started. We needed a COVID test, but didn’t want to pay out of pocket for it, so we had to wait until the next Wednesday to get that. Between all these factors, we were left with only a few days that they needed help. One of those days, we already had plans to attend the meet as patrons, so we didn’t want to lose that ticket. Mr. ODA worked one day of the meet, while I worked 3. I then also picked up a shift for their Derby celebration (although it’s not where the Derby was held).

We had a security guard escort and walked between all the bars and concession stands making change. Patrons tend to start their day with large bills, so the cashiers need smaller bills changed out. That’s where we came in. On the first day, I walked over 26k steps – while wearing ballet flats. My feet and calves weren’t happy about it.

It was an interesting experience. I enjoyed watching the transactions that took place, and the time passed quickly. We didn’t even know what our hourly rate was until our first pay checks, but we thought it was something new and different, so we jumped at the opportunity.

BREASTMILK DONATION

I’ve breastfed both my children. For my first, I worked while he was 3-8 months old, so I needed to pump to leave him with someone else. I learned that I produced a healthy amount of milk and looked into donation methods. A friend of mine had donated milk to a milk bank that works with NICU babies, so I explored that option. I went through their rigorous approval process and took their oath on health standards. I donated over 1200 ounces to the bank that first time. They weigh the milk upon arrival, and I was paid $1 per ounce weighed.

It was a lot of work, don’t get me wrong. I agreed up front to provide 350 ounces per month for 4 months. I didn’t hit that mark. It was mostly to my lack of knowledge on how to freeze the milk so that it took up the least amount of space when packing a cooler. They also had a requirement that not more than 6 ounces gets put in a single milk bag, so that added up. I struggled with their packing mechanism; no matter how many of their videos and attempts I made, I couldn’t seem to get 350 ounces in one cooler. It’s nerve wracking when you’re trying to get frozen milk from a freezer to a cooler while it’s 80 degrees outside (garage freezer), and you feel like you only have one shot to do it right or you jeopardize your entire stash from arriving frozen and being worth all that time and effort. I digress.

My second child didn’t latch for the first 4 weeks of her life, so I was exclusively pumping. That meant that she wasn’t regulating how much I made, and so I was making a whole lot more milk than she needed. I knew the rules associated with this milk bank from last time, so I was on my A-game from the start. Lesson learned – double check their rules before any future donation attempts because they changed a couple of their rules. They now wanted 400 ounces per month for 4 months, and they allowed (and encouraged) as much milk in one bag as possible. I wish I had known that on the days where I was trying to figure out how to get 7 ounces into two bags and whether I wanted to hold off on mixing later pumping sessions. I did better with the packing this time around, but it still wasn’t great. I nailed it on my last cooler, but it was too little too late. After my last cooler went off, I only had about 150 ounces left over. We were about to be ‘homeless’ (remember when we sold our house but didn’t have a new one to go to yet!) for 7 weeks, and I couldn’t keep up with pumping and moving around to all different places, so again I didn’t meet their quota. They’re always so gracious for whatever they receive though. I ended up donating just over 1,100 ounces this time around at $1 per ounce.

Mr. ODA could retire today. But again: what would we do with all that free time, what would he do about his leave balances that we don’t want to cash out, what do we do about health care? Our monthly expenses are more than covered by our rental property cash flow, but we don’t want to be stuck at home not being able to spend any extra money because we don’t want to raise our expenses. Since Mr. ODA is going to keep his job for now, we’re planning a more extensive summer travel calendar and trying to shift the mindset away from super frugality since we’ve already met many of our financial independence goals. Our savings now will create lifestyle in the future once we’ve both taken the “retire early” plunge.

The biggest change since I was working is that the Federal government now pays paternity/maternity leave. As I shared, I had to use my own leave balance. The Family Medical Leave Act just holds your job – it allows you to use your own time off, but it doesn’t guarantee payment. So I was granted 12 weeks of unpaid leave that I was then “allowed” to substitute my own leave for. I had planned for babies, so I had a great leave balance to get me through my maternity leave. Now, my husband will get paid for 12 weeks without having to touch his leave balance! Since we’re talking about having another kid, he’s going to stick around to utilize that benefit.

I’ve done things here and there to keep me sane because talking to other adults is a big need for me. But I wouldn’t trade all the time I’ve had with my two kids thanks to Mr. ODA’s extensive research and aggressive saving/investing to get us set up for success and early retirement. I’ll continue to keep my eye out for these part time opportunities where I get to learn something new.