We had two tenants move out at the end of July. We also had back to back trips scheduled for the end of July and beginning of August, with the kids starting school on the 13th. We also had the cruise planned for the end of September into October, so that was a decent push to get the rentals rented before we left. We put countless hours into those two houses and it definitely took its toll.

RENTALS

As of October 1st all our rentals are rented! That’s a good feeling after two months of vacancy. This is the month of taxes. We have several houses that are paid off, which means they aren’t escrowed, and I’m responsible for paying the taxes and insurance on them. The 4 houses we have in KY are owed this month, and it’s about $7k worth. We’ll owe 2 houses in VA that come to about $3k next month.

I have a couple of houses that are struggling to pay rent on time. Usually it happens for a couple of months and they get back on track, but that’s not happening quickly. I’m trying to remain optimistic, but there isn’t a track record of it getting easier if they have taken this long needing to catch up.

We closed on a new property near our house. It’s a townhouse that we hope to get rented later this month. We’ll see what it looks like once it’s empty, but it didn’t appear we’ll need to do anything to it to get it rented (which is how we buy our rentals). There will be separate posts going into the details of each rental turnover and the purchase of House15 using a commercial loan.

PERSONAL

This is the last month for the 0% interest credit card. When we have a major purchase on the horizon (it was house-wide carpet this time last year), we open a 0% interest credit card. We started this concept about 8 years ago. We look for a credit card that has 0% interest for at least 12 months and that gives us a bonus of some sort. We make more than the minimum payment each month and then pay it off before the deadline. A default payment can cause you to lose your 0%, so it’s important you’re making your payments. But we don’t pay a lot towards it because the money is doing more for us in our savings account (or the investments) than it would by paying down a 0% interest balance. This time around was a bit different. The carpet only cost us $10k, but the balance is over $14k. This credit card had the same incentive as our typically used card (2% cash back), so Mr. ODA used it a majority of the time. For a while, my goal was just to pay what gets our balance lower than the original balance from the carpet. But then we had some big rental purchases that we put on the card, and it just wasn’t worth paying $5k+ to the card. We will make a transfer from our big savings account to make that payment at the end of the month.

Mr. ODA’s last pay check arrived on October 11. He took the “deferred resignation program” as of April 30. The sunset date was September 30, so that covered the payout that we just received, including his balance of annual leave.

Outside of rentals, our spending has been minimal. With the cruise, we didn’t spend much since that was a week of almost everything paid for in advance. The dog had his annual check up, so he was the bulk of our costs. We have our routine costs we see, but happy to see lower balances after all the rental work costs.

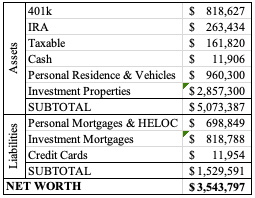

SUMMARY

I don’t even want to admit what is about to leave our account this month. I guess the positive is that it’s under $100k..? We have to pay the taxes on the houses that aren’t escrowed, pay off that credit card, and buy a house. At least the house purchase goes right towards equity. Since I didn’t get all the account numbers yesterday morning like I planned, here’s an update that captures our new purchase.