This was a mess. I learned my lesson to research each property individually and not to make any assumptions. I also learned my lesson to hold true to our standards and expectations for a renter. We owned this house for a year and a half, but we learned a lot about tenants and the selling process. Hey, every struggle is a learning opportunity for next time, right!?

Mr. ODA showed me House 6 first (5 and 6 closed at the same time, and on my numbering list, this one came second… so try to overlook this awkward numbering!). I researched the area and the house’s history in detail, and I decided that it was worth pursuing. Very shortly after that, he approached me about House 5. The house was in better condition than House 6 and was literally only half a mile away. I assumed it was in the same neighborhood. I was wrong, and that’s where things went downhill fast.

LOAN

This house was so cheap that we needed an exception approved to get a loan. The purchase price was $60,000, which means a loan with 20% down is $48,000. The cutoff for even approving a loan with our regular lender is typically $50,000. Since we were below that threshold, we were ‘penalized’ by the rate.

I covered the closing snafu in the House 6 post, which also highlights the decision-making on the loan terms. Since this house was below that $50k threshold, our options were: 5.125% with a $200 credit or 5% with no credit. The higher interest rate would cost us an additional $1300 in interest, which isn’t offset by the $200 credit, so we chose the 5% rate. Hindsight: If we had known we would sell it just 18 months later, the credit would’ve been the better choice!

We purchased the house in July 2017. We immediately started aggressively paying towards the mortgage since it was the lowest balance and the highest interest rate.

We rented the house for $775, which far exceeded the 1% Rule.

WORK ON THE HOUSE

We did a lot of work in the yard. Here’s what the house looked like at some point before we owned it. It’s cute!

While it was under contract, the house sat vacant, so there were a lot of overgrown bushes, flowerbeds were filled with debris and no remnants of flowers having lived there, the lawn hadn’t been cut in a long time, and the tree in the front left had been removed at some point, leaving behind a mound of a stump and mulch that also collected debris. It’s a shame, and I kind of wish we had brought this little 2 bed/1 bath house back to life like it was in this picture. But I digress. Although this picture shows that the previous owner took care of the property, and that’s what attracted us to the purchase.

The floors were in immaculate shape, and the kitchen was quaint, but in decent shape. We purchased a new refrigerator before we could list for a tenant.

The bathroom needed a lot of help, but we didn’t want to overhaul it. The medicine cabinet wasn’t working anymore and the glass was cracked, so we wanted to replace it with just a mirror that covered the old medicine cabinet hole. Interestingly, we found a stash of 100s of razors behind it! (Apparently this is a thing from times gone by. You finish your blade and then you shove it behind the medicine cabinet for it to reside in the wall for all eternity.) We had several plumbing issues in the house. The drain pipe for the tub had multiple kinks in it, which caused the water to drain slowly and be more easily clogged. This would have been a major overhaul to get new plumbing installed in a way that was more direct.

The electric in the house was in need of work. We fixed quite a few electric-related-things while we owned it, but re-wiring the house was a major expense that would’ve come due in a few years.

TENANT ACQUISITION

The house was in great condition, had a big lot, was in a located close to the downtown area, and was on several bus routes (I even had a bus driver stop and ask me what the rent was on the house while I was working out front). It seemed like a great investment. We had several showings to qualified individuals….. who then went home, researched the house, and saw that it was in the highest crime area on Trulia’s crime map.

After sitting on the market for 5 weeks, we lowered our standards. There’s a reason you have standards as a landlord – it’s because if you select the right tenant, you’re saving yourself time, money, and headaches in the future. Here’s the email from our property manager. There are multiple red flags, and yet we gave her a chance.

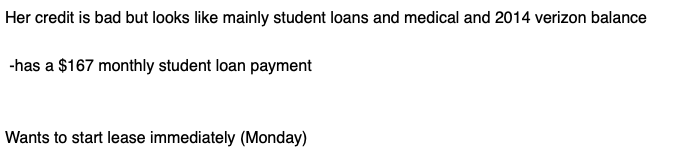

The prospective tenant provided us with an employment verification letter showing that she had just started a new job, her most recent pay stub corroborating the employment verification letter, and wrote a decent introduction in her application. Between it being 5 weeks with no tenant and it now being mid-August (with it harder to rent in the Fall), we overlooked her credit score of FOUR HUNDRED AND FORTY EIGHT (448) and SEVEN (7) accounts sent to collections. I don’t recommend you do this. Oops.

EVICTION

This is the fun part to recount. It’s detailed, but I think it’s interesting.

RENT COLLECTION

She moved in August 2017. By December 2017, we already had enough issues that she wasn’t going to be trusted going forward. We’re very flexible landlords, and we’re happy to work with you on any issues as long as they’re communicated up front and timely (meaning, if we have to continuously reach out to you for rent, you’re not in a position to ask for favors).

We had allowed PayPal to be used to pay rent, but every month there was an issue. She either sent it in a way that incurred fees (after being told that she would be responsible for such fees) or it was sent in a manner that caused PayPal to hold the funds and not immediately release them. After December’s rent was late, the late fee wasn’t paid in full, and there were fees taken out by PayPal, we cut her off from electronic payments. Our property manager informed her that going forward, all rent had to be received by her office (either by mail or drop off) before the 5th.

Speaking of flexibilities – we noticed that she needed to send us rent based on each pay check, versus having all the rent money at the beginning of the month. She was paying us a late fee every month. Her rent was $775, and her late fee was $77.50. That meant every month, we were collecting $852.50, which really wasn’t necessary. We offered a change to her lease terms – rent was due on the 1st and 15th. As compensation on our part, rent would be increased to $800, split into two $400 payments. However, if rent was late, the late fee was now 10% of the late payment ($40) or up to $80 if she was late on both installments. She agreed to this, as it saved her money each month and set her up for success by being able to set up a system with each of her paychecks. We didn’t like that our relationship with the tenant had come to us hounding her over money, so we thought this was the best path forward for both sides of the party. Here’s the addendum to her lease.

And yet this didn’t change anything!! The addendum was signed at the end of January 2018. She paid February’s 1st $400 late. Then she didn’t pay February’s 2nd $400, and we had to reach out to her several times before even getting a response… after she also didn’t pay March’s 1st $400.

Our property manager filed unlawful detainer (eviction) with the court, and that got the tenant’s attention. She then had to pay the balance due, as well as the court filing fee, before March 30th (court appearance date) to dismiss the court action. She showed up to court with the cash to pay and then everyone just went home. You can’t evict someone who has paid in full, even if the process of collecting rent was unnecessarily burdensome.

And then came April. There was another story about a medical emergency and a new job on the books. We had agreed to a new one-time schedule for April’s rent payment, and she missed those deadlines and was incommunicado. We sent her another default notice on April 25. Note that this medical emergency was for her “husband.” This is the first that she had implicated herself that someone may be living in the house other than her and her son. She paid her balance owed on May 4th.

On May 8, she was given another eviction warning notice for lack of May rent (the 1st $400) and gave no response to requests for information on when to expect rent. After continued lack of payment after that notice, she was served with another eviction notice. On May 17, she was given 30-days notice to vacate the premises by June 17, 2018 at 5:00 pm. But then she paid in full and on time. We then changed her lease terms to state she was on a month-to-month basis and she would be granted 30 days notice when we (or she) decided to terminate the lease agreement. It was signed on July 16.

Guess what? She didn’t pay September’s rent. At this time, we also addressed her husband.

She was married when she applied, but we didn’t know. Just now as I was looking back through our files to write this post, I saw that her pay stub she used for employment verification said that she was filing her taxes as married. I hadn’t seen that before. In all our visits to the house, there were always other people there. There was one man that seemed to be around 90% of the time. We overlooked it, but our lease did stipulate that anyone who stayed for more than 2 weeks was required to pass a background check and be on the lease. I strongly suspect that this individual was not going to pass a background check, which is why it was never disclosed to us that she was married and another adult was living there. Our property manager informed her that only she and her son were on the lease, and that if anyone else was living there, they had to be on the lease. She asked if we were referring to her mother-in-law visiting, our property manager said that it appeared to be her husband was living there, and then she ignored us.

We gave her our 30 days notice on October 5 to vacate, meaning she had to be out by November 5. Our property manager reached out to her on October 26 to see if she would be out earlier and set a time for key pick up. The tenant nonchalantly stated she wouldn’t be able to make it out by the 5th and she’ll be out by the 9th. Umm, excuse me, ma’am, but that’s not how this works. We held strong to the 5th and she lost it. Our property manager said that her lease is over on the 5th, and if she was not gone by then, the court fees would be her responsibility for us to get the court and local police department involved for her removal. She got angry and claimed that we didn’t handle the rental well at all, that we couldn’t charge her any court fees, and that she should charge us for not being able to use her tub because it was clogged (guess what on this one? The plumber removed things like a dental floss pick from the drain, immediately making it her fault (and at her cost) for said clog). She then said: “Lets just hope your (sic) as speedy with my deposit as you all were with terminating the lease.” I laughed out loud on this one just now. We should have terminated her lease an entire year before this discussion happened, but we kept working with her! Hysterical! Gosh, and to think this wasn’t our worst eviction process (more to come :)).

SELLING

A friend-of-a-friend was attempting to purchase a house in the same neighborhood as this house, and they ran into multiple issues causing them to walk away from other deals. Mr. ODA approached him with an opportunity to sell this house, which had similar specs to the one that they were pursuing. The buyer spoke to his wife and father about the deal and agreed to move forward. Of course, this deal was not easy.

The contract was ratified on October 31, 2018. We didn’t close until January 8, 2019. Our typical close time on our purchases is 4 weeks. We’ve done faster, and we may have done a bit longer if the time of month lined up better for our finances, but over 2 months was horrendous. Since our tenant was moving out on 11/5, and the closing was expected to be no later than November 30th, we didn’t pursue finding a tenant.

The appraisal was late being ordered, which was somehow allowable. Then it came in at the beginning of December at $65,000; our contract was for $68,000. We split the difference ($1000 from the buyer, $1000 from the seller, $1000 from the agent who was dual representing).

On December 18, our Realtor finally pushed back on the buyer’s side of the transaction to get things done. But it was Christmas time now. With so many offices closing for the end of the year, we weren’t able to get a closing date until the first week of January. The buyers were signing paperwork from Pennsylvania, which caused more delays because of having to send the paperwork back and forth for everyone’s signatures.

We sold in January 2019 for $67,000, after having purchased it for $60k just 18 months earlier. While this seems like a great deal, it’s not an automatic $7k in our pockets. You need to account for our closing costs from the purchase and sale (about $6,500), loss of rent for two months while trying to close the sale and the 6 weeks of no tenant when we purchased it, utility costs associated with vacant times, and costs to fix things around the house during our ownership. However, during that time, we had a tenant paying our mortgage (covering the loan interest and paying down the principal), and we were collecting more rent than projected because of her continued late payments.

1031 EXCHANGE

We made the decision not to pursue a 1031 exchange on this house. A 1031 continues to defer the depreciation to the next property, and it allows capital gains to be deferred. Based on current tax law, it can be done infinite times. However, there are extra lawyers and fees that come into play, so it becomes worth it when you have big dollars at stake, and that you have another property to purchase quite quickly after selling the first one.

The appreciation on the house was minimal given that it had only been 18 months since purchase, we had two sets of closing costs to add to the cost basis, and we hadn’t earmarked a place for that money to go upon selling. Plus, the cost of an intermediary would continue to eat into the “profit” versus tax paid, so we just went ahead and planned to pay capital gains taxes on it. Unfortunately, since we had depreciated the structure and the fridge over the prior 18 months, that paper money had to be brought back into the fold when calculating our taxes the following April. That’s several thousands of hidden money that is easy to forget about.

Depreciation is a great tax break when you own the property. The IRS assumes the value of your asset is being reduced by wear and tear and father time. This is true. It’s why if a landlord neglects the property and isn’t active with maintenance, renovations, and other replacements, the property will turn into a trash-heap in time. However, when you sell the property, you show the IRS that it in fact did not do that. If someone is willing to buy my property for more than I bought it for, then it obviously didn’t depreciate to a lesser value. I have to pay the IRS back for the depreciation assumptions that I was allowed to make over the time I owned it, plus pay the tax on the actual profits. Bummer, but logical.

In summary, we bought a cheap house and got a poor tenant. We had a TON of headaches with that tenant. We had to do a few house/yard projects over the ownership life of the property, but nothing worrisome and not already built into our numbers. Somehow, we made it work that eventually the tenant always paid up and then some (late fees). We made mistakes, we learned lessons. We figured out a set of streets to avoid for future purchases, learned how to sell an investment, and learned how to file taxes on an investment property sale. The story is fun to look back on. I’m glad we experienced what we did. But I don’t want to do it again.

One thought on “House 5: Bought and Sold”