I have gone through all our expenses in 2021 and categorized them, which was very time consuming. I swore I’d do better this year, but it’s March, and I haven’t done anything.

In the past year, we hit a net worth of $3 million. That’s really exciting, but we have more goals. It’s important to note that the net worth is through our investment properties, retirement accounts, and other investment accounts, so it’s not liquid funds. The values on our properties have drastically increased, many of which we’ve recently refinanced and have an appraisal on file showing just how much equity we’ve gained on these. Except for the cash that we have in our savings account right now, as we prepare to purchase another property at the end of the month, we don’t typically carry a cash balance. Our philosophy is that, if there’s an emergency, there are very few things that can’t be put on a credit card, and we can liquidate investment funds within 24 hours. We don’t subscribe to “3 months worth of expenses in savings” type actions. We’ve had plenty of large expenses hit us with rental properties, fertility treatments, and other random health needs, but it hasn’t ever been something to drown us financially. So while it’s exciting to see that new net worth, it doesn’t change our spending philosophy.

DIVIDENDS, INTEREST, & REWARDS

Mr. ODA used to have our dividends get reinvested automatically, but now they are transferred into our checking account. That was over $6,500 that came in, mostly at the end of the year, but there was ~$30 per quarter deposited also. In a different time, interest earnings on accounts used to be something to be excited about. Our checking and savings account combined brought in $6.51 for the year.

Mr. ODA is set up with GetUpside. When I went to their site to get a better description, I learned that you can earn cash back through gas, grocery, and restaurant purchases; I thought it was just gas. It’s an app that allows you to earn cash back through your normal purchasing. However, it also gives you an incentive for referring people, and so when that person buys gas, you get some cash back. By checking the app for a participating gas station (and only using it if the incentive offered is a better price than surrounding gas stations), Mr. ODA deposited $32.45 for the year.

Between 5 credit cards, we brought in $4,232 worth of rewards. These are simply earned by either spending or paying the credit card, no further action. We preach and preach to have credit cards with rewards. Everything we purchase goes onto a credit card; at the end of every cycle, we pay that credit card off. We’ve developed a mindset for spending that means we’re not afraid of what we put on the credit card and whether we’ll be able to pay it off in full at the end of the month, because we’re not spending frivolously. I will caveat that this amount of rewards was possible due to sign-on bonuses that were earned in a previous year, and then the credit card changed their reward redemption options, allowing us to pay ourselves back for restaurant purchases. We had previously been using the rewards to purchase travel needs through their portal, but we were able to dwindle down our rewards with this reimbursement change.

INVESTMENTS

Every month, we each put $500 into our investment accounts as an automatic contribution to max out our Roth IRA contributions. Additionally, each kid gets $50 deposited into their investment accounts each month. We also received the child tax credit each month, so with that, we put $125 into each kids’ account. The thought process was that we received $600 for them, and so after investing in their accounts, we were left with $350 to go towards “raising” them, which was the intent of the money being sent out in advance.

EXPENSES

My categories were super broad. For instance, if we traveled, I included all the expenses (e.g., lodging, flight, activities, parking, dog-sitting) as “entertainment.” But “entertainment” also included watching horse racing, baseball game, zoo, babysitting, etc. “Home” includes any furniture purchased, decorations, cabinet knobs, pictures/frames, etc. Even with the broad categories, I still had too many.

There are 3 categories that we have more control over, so I took a closer look at them: groceries, gas, restaurants. These are the ones that we can control our actions to change if we wanted/needed.

GROCERIES

A shortfall on my tracking is that I don’t know if Walmart purchases were necessarily for groceries or for something else. I removed a $300 purchase from my list because we wouldn’t have spent that much in one transaction in groceries, but I can’t figure out what we did spend it on because it was too long ago.

I investigated the spike in June, and I didn’t come up with anything jarring. There’s a transaction for $165 on a day with another transaction, so that may not have been food. August had several trips to Kroger. Trips to Kroger mean that we’re buying in bulk, so things purchased there are typically several of a particular deal they’re running that week versus an actual grocery shopping trip. There are 19 grocery transactions in August, which is higher than usual. August also included an emergency “find this kid some medicine while we’re on the road” that cost us $8 worth of medicine.

Lesson learned: We can do better meal planning and making fewer trips to the grocery store. We can be more deliberate about what we’re purchasing instead of stocking the pantry without a plan. We have a Sam’s Club membership and sometimes we tag along to Costco to scope out deals, so those lead to more bulk purchases, which will fall by the wayside in 2022. The Kroger deals will continue to be on Mr. ODA’s radar though.

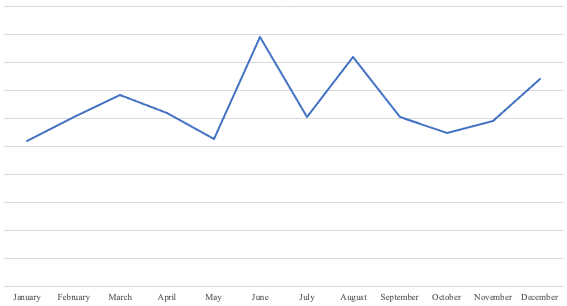

GAS

Interesting that January through April are so much lower because we didn’t necessarily stay home. We drove about an hour away for a trip in January and a trip about 90 minutes away in March, went from our house to Lexington (about a half hour) every weekend, and went to the zoo (about an hour or so away). I guess we stayed home during the week more, which kept our gas costs low. April was when we gave up on a lake house and decided to be deliberate about going on trips, so I expected to see an uptick in gas costs at that time. I described that whole thought process and what we did in this post. Some of the uptick in certain months can also be contributed to us trying to maximize gas prices (e.g., we fill up if we’re going to be near Costco, even if we don’t necessarily need the gas at that time). In October and half of November, I was working in Lexington on the weekends, so that was 3 days a week that I was driving 25 minutes each way. Then in December, we drove from KY to Long Island, which is a whole lot of gas.

Lesson learned: We like to be active, so I don’t foresee a change in our gas-purchasing patterns in this year. As I type this, gas prices are soaring all over the country. Since we like to travel, our trips are usually within driving distance versus flying with two kids, so spending the money in gas is cheaper than 3-4 plane tickets.

RESTAURANTS

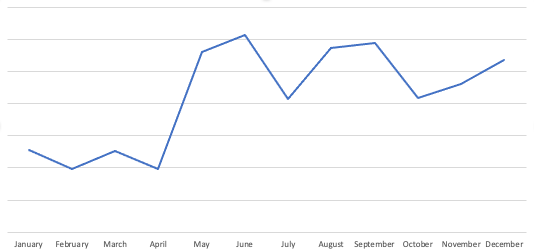

This is a funky one to track. While we’re traveling, we’re clearly eating at restaurants more often. That’s seen in the higher spending that happened over the spring and summer months. I don’t remember spending all of February in the house, but our credit card purchases seem to say that’s what we did – no gas and no restaurants. In March, we splurged on a birthday dinner ($77!), which is unusual for us. From April through August, we were traveling (and therefore eating fast food and at sit-down restaurants), Mr. ODA had work trips (so he’s going out to eat with coworkers for multiple nights), and there seems to be one or two transactions each month where we paid for a group dinner that was reciprocated (and not captured). Under the restaurants category is also when we went for drinks somewhere. We went to a winery and had a couple of drinks with friends, and that could probably be considered “entertainment” versus eating outside the home.

HOUSE WORK

We put a lot of money into our house this year, which is surprising since it’s new construction. We finished our basement, which was about $15k instead of the $75k-100k that other people have been quoted for the job. We bought a patio set, a grill, and an entryway table. Mr. ODA built a “shed” under our deck (we can’t have free-standing sheds per the HOA, so we enclosed under the deck .. not “free standing” 🙂 ). Most of our furniture moved with us from the last house without an issue, but there were a few purchases needed. Between our initial move in purchases (a kitchen table and chairs), purchases in 2021, and a few purchases that have already happened in 2022, we should be done with big house purchases.

INCOME

I quit my job in 2019. I manage our 12 rental properties as my “job” now, but I also am open to part time jobs as something to do. In April 2021, I was asked if I could help fill a position at the race track during their Spring meet. It wasn’t a job that I wanted to go back and do in future meets. I mentioned that I’d work the Fall meet if I could do something like pour beer, and Mr. ODA’s dad (who works there) made it happen. I also worked some of the days of their horse sales. I worked 22 days for the year and contributed $5k to our family’s spending for the year.

LOOKING AHEAD

I’ll try to track our expenses in real time this year, so that I can categorize them more accurately. Watching expenses month-to-month means you can also make adjustments if you see you’ve spent more than usual in one category.

Finishing our basement meant that we moved furniture around. A sections that was in our dining room moved to the basement, freeing up the dining room to actually be a dining room; I purchased a table and chairs. The “playroom” toys were moved down to the basement, and that room became the guest room. It’s nice that the guests can have their own space on the first floor and not share a bathroom with the kids. That freed up the previous guest room to be an actual office, so I purchased a desk (our old desk was in poor shape and it didn’t move to KY with us). Other than that, I don’t see any major expenses on our own house for this year.

We expect to travel a lot again this year. We already have six trips planned. They’re all driving trips, so that’ll increase our gas category. I have one trip expected to fly to my sister’s baby shower, but that hasn’t been scheduled yet. We’ll also have day trips that we’ll do around our house, which is usually an hour to an hour and a half worth of driving.

While we don’t “budget” or believe in the “envelope system,” we do watch our spending on a regular basis. We check our accounts every few days to ensure there are no surprises as well (i.e., don’t wait for your statement to come and find out there have been false charges). Keep paying attention to what’s being spent and where your money is going so that you can make informed financial decisions.