Quick post about our 3rd investment property purchase. After we closed on House #2, the seller said he was interested in liquidating the house next door, which was a mirror image of the house we just purchased. The story here is how the offer was made.

We agreed to purchase for the same bottom line as House 2. There was some confusion about what “bottom line” actually meant, where we meant it should account for our side of the transaction not using a Realtor. It took us over a month to go through the financials and have an agreed upon purchase price.

We purchased House 2 for $117k with $2000 back in closing costs. Our first offer on House 3 was $113,400. The selling agent countered that he came up with 117,000-2,000-1,170 (commission to our agent on that house) = $113,830, but he had to forward the offer to the seller. Then we received this from the seller:

The selling agent agreed that Mr. ODA’s math was closer to accurate than the sellers, and that if it came down to a few hundred dollars difference, he was willing to eat that from his commission since he didn’t have to pay to take pictures and list the house.

And so here’s the final response from Mr. ODA, and a view into how his brain works. He never fails when it’s math.

He paid 4% commissions to agents on the last purchase. That 4% was derived from a $117k sales price, which equals $4680. That $4680 gets subtracted from my funds at sale, or $115k. $115,000-$4,680 = $110,320. Thus his “net” that he “walked away with.” If that “net” were to be matched on this price, you would take $110,320 and divide it by 0.97 which would equal $113731. As a check, if you take 3% of $113731 it is $3,411. Subtract $113,731 from $3,411 and you get $110,320 – the same ‘take’ as he got from 1718. An arbitrary reduction in price of just Krissy’s portion of the commission is incomplete, as your 3% is no longer equal in each transaction. The way your math works, his walk away is $113830 less the 3% = $110,415. That is more than he took from 1718. Since I know that Mike is willing to “walk away with” $110k, I offered a purchase price that, when reduced by your 3% commission, comes to $2 shy of $110,000, his stated in writing goal for this transaction.

We paid $113,732 for the house. 🙂

TENANTS

This house has had the same tenants since we purchased it in 2016. We raised their rent by $50 in 2019, and we expect another $50 increase upon their renewal in a few months. The house has appreciated greatly since we purchased it, which has caused our taxes to increase from $750 twice a year to now $870 twice a year), which we need to account for in the rental income of the property.

They take good care of the house, and they actually border on being too cautious about maintenance needs. We’ve had several issues with the plumbing, which has culminated in it being their children putting things where they shouldn’t be, which means the cost is on the tenant because it’s not routine maintenance.

The tenant replaced a stove and refrigerator, at their expense and with the understanding that either they leave those behind or replace them with reasonable, working appliance. For the stove, they sought approval from us to upgrade their stove to something that’s more conducive to his culinary expertise. We told them that they could replace the stove there, but that a working stove must be there upon their vacating the unit. About a year ago, we were there for a maintenance call and noticed an upgraded refrigerator, which they didn’t tell us about. We again told them that since we provided a refrigerator with the unit that a working one must be put in its place when they vacate.

This is the house that we installed a backsplash in the kitchen. The tenant said that he cooks a lot and there’s been grease splatter that’s been hard to keep off the flat-painted wall. We agreed that a backsplash is better for the longevity of the house. There were several options available, so we even let the tenant pick from a few samples. We did the peel and stick style, so we saved on cost and labor, but accomplished the goal of an easy-to-clean surface.

Twice, they’ve reached out to us about a rent-to-own offer. We aren’t interested in selling because our financial goals require a month-to-month cash flow, this house is newer and still in good condition, and we have a low rate mortgage on it; but knowing how much the house has appreciated, we may be interested in a 1031 exchange option if the offer is right.

House 1 was purchased from a family member because we saw an opportunity when they were getting ready to sell their townhome. House 2 was purchased because we were looking for a way to make our profit from the sale of our first home to get to work for us. While in the process of purchasing House 2, the seller said he was interested in liquidating the house next door, which was a mirror image of House 2, and so that became House 3. Both House 2 and House 3 came with tenants, which was a big advantage, but delayed a few lessons in rentals for us.

After we sold our house outside of DC, we moved just outside of Richmond, VA. We spent a few months looking at the neighborhoods and analyzed the markets available in Richmond. I was more interested in the college area, where it’s a market I knew well, having been a college kid who rented in an old house that was sectioned into apartments. Mr. ODA was more ambitious (in my opinion), looking into neighborhoods that families would rent in. Many investors are looking to rent in areas of Richmond that fit the quintessential Richmond mold (e.g., walkability to restaurants and shops, bike routes). However, these houses don’t come close to hitting the 1% Rule.

We’ve purchased several houses on the east side of town, and they’ve worked out very well and most don’t have turnover. The value of House 2 since we purchased it has increased by about $70k as the neighborhoods in the area continue to decrease crime and increase value. Both houses are about 13 years old, 1200 square feet, and have 3 bedrooms and 2 baths. All of the rooms except bathrooms and kitchen are carpeted, which is something we’ve since tried to stay away from.

THE EXCLUSIVITY AGREEMENT

After we saw House 2 and wanted to make an offer, our Realtor relationship went downhill. We had a Realtor for our home purchase when we moved to the area, and we continued the relationship to have access to the MLS. After we purchased our home and started looking for rentals, we soon learned that our Realtor 1) had an agenda to get the most commission, regardless of the best deal or our interests, and 2) kept pushing areas she knew versus areas we were interested in. We had made it known that we wanted to buy several properties, and I believe by the time we wanted to make an offer on a house, she realized we weren’t looking to further this relationship after this deal. Since she had shown us a few houses, we expected to see this deal through with her. That’s when the straw broke the camel’s back. We received the offer to review, and it came with an exclusivity agreement.

An exclusivity agreement is a contract established by the Realtor to protect their interests. If the client signs it, then it means that the client is committed to that agent for the terms in the agreement (e.g., a single purchase, a period of time). We hadn’t needed one in Fairfax, and the one we had for our personal home contract covered a month’s time. When we received the contract for House 2, the exclusivity terms were until October 4, 2016, from the date of the contract, which was May 4, 2016. We requested the date be changed to match the “close no later than” terms in the contract, which was June 17. That’s when the bs-ing commenced. I’m sure the average buyer wouldn’t have noticed nor cared. We saw right through it, and she kept digging in deeper with holes in her story and guilt.

First, she claimed that she made it 6 months (although it was 5 months) so that it gets through closing and we didn’t have to sign again. We countered with three pieces of logic: 1) the field can accept an address, so change it to the house’s address to cover us for the entire time it took us to get to closing, whenever that may be; 2) the exclusivity period on our personal residence’s contract expired long before we actually closed (because it was a new build, and the contract was signed before construction began), but we never had to re-sign an agreement; and 3) we never experienced a 6-month closing on a routine purchase.

Instead of addressing that the field could accept the house’s details rather than a period of time, she said: I’m committed to helping you guys look for houses and make offers, are you committed to working with me? Red flag. When we said we wanted it changed to the house address, and that we didn’t mind signing on for each property we made an offer on, she furthered the guilt with: We have know each other for almost a year and I honestly didn’t think it would be such an issue. If you are not willing to sign it I am not going to be able to work with you. If it’s not supposed to be a big deal for us, why is it a big deal for you/your broker?

One of the first things we learned in the real estate market was to not sign an exclusivity agreement. It eliminates your rights as a buyer and ties you unnecessarily to an agent. On the Realtor’s side, I understand that a lot of time and effort goes into working with clients, and there is a possibility that one Realtor shows a client a house, but that client uses a different Realtor to sign the contract, which causes the agent who showed the property to lose the commission. However, I believe that if there’s a good relationship with the Realtor and client, it shouldn’t need to be in writing that they’re committed to each other. I also don’t believe that it’s routine that a Realtor shows several houses to a client, and then that client finds someone else to make an offer. I was also surprised that it’s at the contract stage in the process, and not at the showings stage.

When she wouldn’t write the offer without us signing an unnecessarily long exclusivity agreement (again, we were willing to sign it as associated with this offer/property), we called our old Realtor and asked if she could write the offer for us even though she didn’t cover that area. (An Agent’s license covers the whole state, but typically their access to the MLS is confined to local metro areas unless they want to pay for other regions.) She wrote the offer for us. She also introduced us to a loan officer who we have used for every property purchase since then, and recommended to others.

EXPENSES

This house is relatively new, so we haven’t had any major expenses. We had a couple of HVAC service calls, one was a legitimate concern and one was a misunderstanding by the tenant on how it works in extreme temperatures. What we haven’t paid for in physical house repairs, we’ve made up with in learning new things about tenants.

TENANTS

We had a tenant move in right before we closed on the house. She had gone through a divorce and was living on her own. At the end of the year, she got back together with her ex-husband and moved out. We touched up the paint, cleaned the carpet, cleaned the kitchen and bathrooms, and then listed the house for rent. We chose two ladies, one of which had a criminal record for forgery a few years prior. Other than that, they were the best qualified financially.

Our only issue in the first year was that they had a ‘friend’ look at our HVAC unit. We told them that it’s not their property, and had anything been wrong, it would have been on them to fix because we didn’t authorize tinkering with our very-expensive property. The issue was that it was 100 degrees outside, they had the thermostat set at 60, and it wasn’t getting to that temperature. That’s not surprising. Our technician went out, checked the unit, and explained to them that when it’s that hot, you can’t expect it to get to such a different temperature in the house. He suggested using fans.

They moved in June 1, 2017 and one of the ladies is still there.

At the end of their second year, we increased their rent by $50/month to $1100. This is still under market value for the house, but not having to turnover the unit was more important than a drastic increase in rental income.

In February 2020, we learned a new aspect of the law – domestic disputes. One of the ladies reached out to us and requested to be released from the lease because she had a restraining order filed on her roommate. We researched the requirements associated with restraining orders (because the two she gave us were expired) and then her rights as it related to being a tenant. She had paid her portion of the rent each month, so we weren’t aware of issues. We released her from any responsibility immediately and notified the roommate. Per Virginia Code, the remaining tenant is responsible for the entirety of the lease from then-on. We gave her the opportunity to vacate the property within 30 days if she could not pay the full lease amount going forward, but she chose to stay on the property.

The world shut down a month later. Other than an issue here and there with our other properties, this one has been the most affected. She doesn’t communicate up front anymore when she won’t be able to have rent on time. We received a letter from her stating that she had been furloughed, but things in the letter didn’t look professional and piqued my interest (recall the forgery charge). I called her employer who informed me that her hours were cut, but she was not furloughed; the woman who answered the phone sounded exasperated and indicated she had explained this to our tenant several times. I informed the tenant that I had done an employment verification and that we could be flexible, but rent was still expected. Then a few months later, after she didn’t pay rent or tell us what was happening, she claimed she couldn’t pay rent because of an issue with a check showing up. We requested her employment information again, and I verified she was fully employed. When I asked her what was going on, she stated that she wasn’t required to tell me where her rent was coming from and whether she was employed didn’t mean she could pay rent. Fun.

Then, a few months later again, I received an email from the Commonwealth of Virginia asking me for my tax identification number and other information because our tenant had applied for rent assistance. I was confused because the rent assistance program was for unpaid rent balances, and she was fully paid. I watched the rent assistance program training and attempted an application myself so that I could see how the process works before I questioned anything more. I verified that the program was indeed for past due rents and couldn’t be requested for future rent. I contacted the State office to gather more information, and the tenant had submitted that she didn’t pay January 2021’s rent, which she had. The State made a note in her file. I informed the tenant that the program was for past due rents, which she had none, and that she was not qualified for such a program, but we were willing to work with her if she had any problems paying rent timely in the future.

Each time she’s not paid full rent by the 5th of the month, she has paid rent in full before the end of the month. After she took full responsibility of the property’s rent and lease, we had her sign a new lease with just her name. That lease ends on June 30 this year, and we’re currently decided whether we’ll offer her another year at an increased rate (last increase was 2 years ago) or we’ll request her to vacate the property.

I manage all the financials for my family. Mr. ODA makes the maneuvers, and I record them. Excel is where our organization lives and dies. Sure, I have a degree in Finance and Information Technology Management (i.e., Excel), but it doesn’t need to be complicated or difficult to make tax prep easy for you.

This level of organization allows us to do our own taxes. After the first year of purchasing rental properties, we thought we’d have to hire someone to do our taxes because it would be complicated. It’s not any different than filing your own personal taxes. The software systems available online walk you through the entire process. Each property’s income and expenses have to be entered separately, which is time consuming if you have several properties, but it isn’t difficult.

The most important thing to be ready for your taxes is to make it a whole year activity. If you record income and expenses as they occur, it’s less of a hurdle when the year is over. By recording the activity all year, it then becomes a verification process when the year is over, thereby reducing the possibility of missing something or recording something wrong.

At the beginning of each year, I create a projection of income and expenses, which helps Mr. ODA adjust his W2 tax bracket throughout the year so that we break as close to even or owe very little when it comes to tax filing. Let me dive into that aside quickly.

Taxes Part 2 is what I’m particularly referring to, but you may need the lesson in Part 1 to know what that means. There are IRS penalties if you fail to pay your proper estimated tax (when you don’t pay enough taxes due for the year with your quarterly estimated tax payments, or through withholding, when required). Title 26 of the United States Code covers the penalties. Essentially, the IRS is saying, “You have to estimate your annual taxes owed, and you’re not allowed to only pay us taxes on April 15th every year, but you have to pay the taxes over the course of the year.” People get excited to receive a refund from their taxes, but really that’s just an interest-free loan you’ve given the government. Perhaps some people do need that forced savings, but wouldn’t it be nicer to have that extra money in your pocket throughout the year?

Back to the point…

I create a new workbook every year with each house having its own spreadsheet. Schedule E is going to require you to put your income and expenses, per property, not as a whole, so it’s important to have expenses assigned to a particular house. I set up each spreadsheet in an Excel workbook to identify all known costs for the coming year. Not all of these apply, but these are typically the categories of my known costs for each year: property management, HOA, utilities (City of Richmond bills the owner (not tenant) for sewer fees), property taxes, insurance, annual mortgage interest, cost basis depreciation, and prepaid points depreciation. There’s also a chance that you’re carrying appliance depreciation costs (meaning, the purchase of a washer, dryer, refrigerator, etc. aren’t recorded as an actual expense in the year purchased, but are required to be depreciated over its useful life).

As the year goes on, I record any mileage (record the actual miles along with the mileage cost) and maintenance costs. The IRS posts the standard mileage rate for each year here. If a roundtrip to a rental property is 40 miles, then the expense is calculated as 40 miles multiplied by the standard mileage rate, which is $0.56 for 2021. I’ve learned over the years that the software systems just request your miles and do the calculation for you (which is smart and safer on the calculation side), but we want to know what the calculation is going to be, so I enter it as $22.40 in my spreadsheet.

You’ll be expected to input the days your property was vacant, so record that once it’s known.

Each spreadsheet is linked to a master sheet at the beginning of the workbook that shows the net income and expenses for each property. The difference of these amounts are what Mr. ODA uses to adjust his W4 deductions.

I personally assign costs month by month so I can keep track of them, but it doesn’t even need to be that fancy. A running list of these expenses are enough.

The categories are based on what’s going to be requested through Schedule E.

Then in January/February of the following year, I go through my filing cabinet and my email to ensure I’ve captured all of the expenses that I have receipts for, and vice versa to ensure that if I’ve recorded an expense, I have a receipt for it. Having already captured the expenses throughout the year serves as ‘checks and balances’ and doesn’t make the task feel too overwhelming.

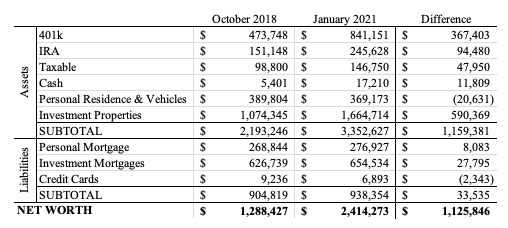

On the surface, a jump of $1.1 million in just over 2 years seems impossible, but here’s the break down of how things changed in our finances during our child-rearing hiatus.

The highlights: – Mrs. ODA left her job; – We purchased three new properties; – We sold one property; – We paid off two mortgages and significantly paid down two others; – Our investments grew based on market fluctuation, as well as our continued investment; and – The value of the properties we own appreciated.

401K

Since I met Mr. ODA, I maxed out my Thrift Savings Plan (TSP, the Federal government’s 401k) contributions each year. Before that, I had been putting money into the TSP, but hadn’t maxed it out. I left my career position in May 2019, at which point I stopped contributions to my TSP. However, we put in as much as we could for the year before I quit (if Mr. ODA has his way, we’d have maxed out my contributions); I contributed $13,070 over the first 4 months of 2019. My balance on June 30, 2019 (it’s a quarterly report) was $300k. I have gained $127k over 19.5 months based on my investment strategy for the account with no new contributions. Mr. ODA continues to max out his contributions of $19,500 per year. His account balance has increased due to annual contributions, a loan repayment, and market fluctuations.

IRA AND TAXABLE

A Roth IRA has maximum contribution limitations per year. For 2019, 2020, and 2021, that amount is $6000. We each put $500 per month into the Roth IRA to max out the contributions. We have maxed out the contribution limitation every year we’ve known each other (10 years), and Mr. ODA had done so before Mrs. ODA knew such a thing. We don’t time our contributions throughout the year because we don’t want to stress about when the perfect time is and then possibly end up throwing five grand in when December rolls around. We have taken the ‘set it and forget it’ (essentially dollar cost averaging) approach to the Roth IRA investment.

Dollar Cost Averaging – Since we know we want to put $6,000 in for the year, we break it down into $500 a month and contribute on the 30th of every month regardless of individual pricing. This eliminates the need to pay attention to, and the effect of, volatility in the market. Some may say that dollar cost averaging is not a prudent idea because the market always goes up over time (essentially you’re setting yourself to pay higher and higher per share as the year progresses, on average), but I just can’t handle the psychology of dropping $6k on January 1 and not having anxiety for the rest of the year that it was the right decision.

As for the taxable accounts, this includes accounts we have set up for our children – UTMAs (however, the growth of these funds are not taxable to us because they are taxed at the minor’s rate – 0% for us). An UTMA is the Uniform Transfers to Minors Act. It allows an account to be set up in the child’s name without the child carrying the tax burden of the money. The IRS allows an exclusion from the gift tax up to $15,000. We put $50 per month, per child, into the account. This is also ‘set it and forget it’ with automatic deductions from our checking account.

CASH

Our cash balance really has no meaning. We bring in income and we pay our bills. We don’t purposely keep a savings account balance (as I shared in the Leveraging Money post, we’re not interested in maintaining 3x our monthly income in a savings account at 0.01% interest rate). We don’t purposely project how much to put towards mortgage principal.

We currently have a larger-than-normal cash balance, which is left over from selling our primary residence in September. It hasn’t been dwindled lower yet because we have a fence install that needs cash and we were paying down the last of our large credit card. Now that most of these things have happened, we’ll put more of our cash balance towards the investment property mortgage we’re currently paying down.

PERSONAL MORTGAGE

In October 2018, we had been living in our previous house for just under 3 years. In January 2021, we had only made 1 mortgage payment on our new home. While our current home cost slightly less than our last home and we put 20% down for each house, we had more years of principal pay down in October 2018 than we currently have.

PERSONAL RESIDENCE AND VEHICLES

We sold our Virginia home for $400k in September 2020. The valuation of that home rose significantly over the 2019-2020 years due to lower inventory with high demand in the Central Virginia area (probably all over the country, but I don’t know those details).

Also in September 2020, I traded my vehicle in for a van (and I couldn’t be happier :)!). That increased our vehicle valuation since the van is 3 years newer and a higher cost than my previous vehicle.

Even though my vehicle value rose slightly, Mr. ODA’s vehicle’s value continued to decline, and we purchased a home in a lower cost of living area, therefore having a lower value.

INVESTMENT PROPERTY VALUES

Since October 2018, we’ve purchased 3 properties, increasing the total property value of our portfolio. Additionally, all of our properties continue to increase in value. The Virginia homes have increased significantly over the last two years. In the table below, I’ve provided each property’s change in value from January 2020 (oldest snapshot per property I have) to February 2021.

Note that this is a projection based on the internet’s valuation and not an exact science. The only house that we have a recent appraisal on is the one that we refinanced in January 2020. That house’s appraisal was $168,000; we paid $112,500 in July 2017.

INVESTMENT MORTGAGES

Of the three most recent purchases, one was purchased with a partner, split 50/50, and the other two were the last two KY houses purchased. These three added $215k of new debt. However, you see that our mortgages on investment properties have only increased by $27k, which doesn’t exactly say “we bought 3 new houses.” That’s because we’ve paid down (and sold) about $150k of mortgages in addition to 2+ years worth of mortgage payments going towards these loans.

In May 2020 and January 2021, we refinanced two properties. Quick tidbit – we signed the refinance papers in May under a tent in a parking lot, and we signed the January refinance at our kitchen table with a traveling notary. While the interest rate and monthly payment decreased, the loan balances increased because we rolled closing costs into the principal and took $2,000 cash out (the maximum allowed) in each case.

We sold one property that we had been paying down the mortgage on; in October 2018 it had a balance of $11,142, and we sold it in January 2019. We had been paying down the mortgage because it was our lowest balance. When we made that decision, selling the house wasn’t in the immediate future. An opportunity presented itself, and we sold it.

We’ve paid off two mortgages during this period. One was in January 2019 with a balance of about $44k, and another was in April 2020, which also had a balance of about $44k in the October 2018 calculation. Our intent to paying off mortgages was two-fold. It increases our monthly cash flow that helps Mrs. ODA stay home with the kids, and it gets Mr. ODA closer to being able to leave his job. Plus, due to Fannie/Freddie requirements of having no more than 10 conventional loans, it creates the opening for us to get a new mortgage if the opportunity arose. The downside is that it de-leverages the house’s financials and creates a smaller cash-on-cash return for the property.

We have also paid down 2 mortgages over the last two years that aren’t completely paid off. – One of those properties is the one that we purchased after October 2018 with a partner. It has our highest mortgage rate. The affect on the numbers here just shows that the principal balance of that mortgage is smaller than it was originally, thereby not increasing the mortgage total ‘fully,’ if you will. The principal pay down on that mortgage has been $44k total, but we’re only responsible for half of that. – On the other mortgage, we’ve paid almost $28k towards principal between October 2018 and now.

CREDIT CARDS

We open new credit cards with 0% interest for an introductory period when we have large purchases looming. Not only is the 0% interest beneficial to us for an introductory period of 12-15 months, but we strategically choose new cards that come with a welcome bonus (points or cash) when you reach a moderate spend level in the first several months. Given the strategic timing of a new card before a large purchase, this bonus is easy to achieve. When we have large balances on credit cards, it’s because we’re purposely carrying a balance month-to-month at 0% interest. We have never paid interest on a credit card balance.

LIFESTYLE

Despite Mrs. ODA leaving the workforce, our net worth increased for all the reasons listed above. The one unmentioned piece, because its not directly tied to any accounts, is lifestyle. While our net worth, rents, and investments have increased, our lifestyle has not creeped. We still make strategic decisions, spend money mainly on needs, look for wants that provide our happiness without breaking the bank, and generally keep our financial future at the forefront of our daily lives. We live like no one else does so eventually we can live like no one else can.

Living intentionally allows us to get to where we want to be.

A tenant moves out. Days without a tenant in the house equate to less income. On top of that, you probably have to touch up paint or repaint. You have to clean the carpet. You have to clean all the appliances and bathrooms. You may have to replace an appliance. Then there’s the extreme, that you may have to hire a junk removal company to get rid of the debris left behind and then hire a cleaner that charges a hazmat fee on top of the cleaning fee (does it sound like I’m speaking from personal experience?).

Turnover is when one tenant moves out and another moves in. The goal is to make that period of time as short as possible, or even non-existent. There aren’t always scenarios that you, as the landlord, have control over, but making a tenant feel appreciated and heard can keep them living under your roof for more than the initial lease term.

When a tenant leaves, in the best case scenario, you’re losing 1 or 2 days of income ($80). However, it’s also taken us up to 2 months to get a unit rented. That means you’re making 2 mortgage payments without income to offset them. When calculating your cash-on-cash return, the assumption is typically 5% vacancy rate, or about 18 days per year without rental income.

Then there’s the work you need to do to get the unit ‘rent ready’ again. Again, the best case scenario is cleaning the house and paint touch up. We now pay someone to come in and clean the house between tenants; it became worth the $100 to have someone come in, with the right tools, and be done a lot faster and better than I could do. The preference is to not have any carpet in a house, but we do have a few that have carpet that will need cleaned between tenants ($125). We do our own paint touch ups, so it’s typically no cost except my time because we have a standard paint color, and therefore left over paint. Quick tip: if you’re not painting the whole wall, use a paint brush to touch up the areas that need it, and then go over it with a roller to help blend it together, then you won’t see those touched up spots.

However, there may be more work to do than those quick, simple tasks that you can have lined up for 1 or 2 days. Even if the tenant treats the house great, appliances and carpeting have a useful life and may need to be replaced, which involves ordering and scheduling installation.

The end goal: keep tenants happy and not wanting to move means more money in your pocket. Find compromise and don’t always focus on your bottom line – and your bottom line will likely end up thanking you.

In 5 of our properties, we haven’t had any turnover (owned anywhere from 1.5-4.5 years). In 3 cases of turnover, the tenant left due to a job relocation. We’ve had 2 evictions. Our turnover rate for the average years we’ve owned the properties is 1.75, so the majority of the time the tenants renew their lease.

How do we do it? We create a relationship that says we’ll be responsive and listen to issues, we’re reasonable and fairly lenient with paying rent on time with sufficient notice and justification, and we provide houses that are in good condition.

We had a tenant vacate a house due to a job relocation. She had such a good experience with us, that she set us up with a new tenant for their house. Then a year later, she moved back into town and reached out to me. She said they had such a terrible experience with a landlord that if they were to rent again, it would only be from us. We just happened to have a tenant moving out because that tenant was buying her own house, and our newly vacated house fit all the parameters she wanted. That meant we had 2 days of turnover and didn’t have to list the property.

That house really needed a new paint job. We hadn’t painted it when we purchased it, and now it’s 3 tenants in. We didn’t know that until the tenant moved out and didn’t have time to paint the whole house before the new tenants were moving in. To show that we knew the house wasn’t perfect, we offered the new tenant $50 per room and $25 per paint can if she wanted to paint on her own. She was thrilled because she planned to paint some rooms to begin with, but now there was a financial incentive for her.

As for rent payments, if the tenant usually pays rent without issue and they preemptively reach out to tell us that they’ll need more time to pay rent, we’ll usually waive the late fee. Our calculations for the year don’t anticipate collecting late fees, so it’s not a loss of ours to waive the fee, but it makes them feel like we care about them as people. If you’re a tenant: communicate regularly with your landlord. Your landlord doesn’t want to evict you, doesn’t want to tarnish your record, and doesn’t want to put you in a position of financial hardship, but we can’t work with you if you don’t communicate with us.

We had a tenant ask us to put in a backsplash in the kitchen. He explained that he cooks regularly, and food is splattering on the wall, which was painted in a flat paint and didn’t wipe well (painted before we owned it). This is unconventional because it’s more than a request to fix a leaking sink or an inoperable appliance. However, we saw the benefit to install a backsplash in the longevity of the kitchen’s life and the tenant feeling like they got a ‘win.’ We agreed to do a peel’n’stick backsplash, which met the goal of a wipeable surface without being labor intensive. We even gave them options to choose from that matched the house’s color scheme. It cost us $68 and about 90 minutes of our time to install it. This tenant still lives in the home, which we’ve owned for nearly 5 years now.

We allow pets in the properties. Back when we were trying to rent an apartment for ourselves to live, few allowed pets; if they allowed pets, there was an astronomic fee associated with it. We decided to not eliminate the average 50% of pet owners by mandating a pet-free property, and we wouldn’t charge monthly pet fees or high initial fees (though we still charge some) associated with having a pet. Honestly, I have kids and a dog; my dog has never done anything wrong in our home, but my kids sure do make a mess and spill things. We have had issues with pets in our properties, but the owners have done other things wrong, so it was a poor tenant issue, not necessarily a pet issue.

I also feel that if we provide a house that looks clean and well-kept, then the tenant is more likely to keep it in that condition. We’re setting the expectation that this is the type of house that we’re renting, and we expect it to be in similar condition when we get it back. We understand paint scuffs happen, pictures get hung, and there may be a couple new stains on carpet, but the house is to be returned to us clean and put together, which is even stated in the lease. If we handed over a house that was dirty or had dingy paint and carpet, the tenant is likely to not put as much effort into keeping it in pristine condition. This isn’t foolproof. But we charge the security deposit for anything outside of normal wear and tear, and they understand this will happen from the lease signing, as well as the unspoken expectation made by the condition we hand the house over in. People are more likely to take care of properties when its condition is good enough to feel pride in, and will typically not respect it if it’s apparent the landlord isn’t taking care of it either.

Our first investment purchase was a townhome in central Kentucky (while living in Virginia) in February 2016.

At this point, we had purchased and sold our first primary residence, and had purchased a new construction home. Our first home sold for $62,500 more than what we purchased it for and we walked away from the sale with over $130,000. Our new home needed about $70k for closing, leaving $60k that we wanted to use for investment properties.

PURCHASING FROM FAMILY

Mr. ODA’s brother-in-law had purchased a foreclosed townhome while he was in college and rented a room out to his friend – excellent forethought and financial decision making there! When him and his wife got married, they were ready to look into a home with more space and less stairs, so we offered to purchase the house. About 2.5 years after he had purchased it, we set him up to make $16,500.

Their Realtor suggested listing at $90-95k. The comparable sales in the area were suggesting 95-100k, but the townhouse in question had a lower PVA than the others recently sold. There was another townhome in the community listed for sale at $100k, but it had been on the market for 4 months at that time, meaning the market wasn’t interested in it at that price. Additionally, this deal was being done off market, which automatically yields a higher net for the seller because there were no Realtor commissions and minimizes the risk of a listing. They didn’t need to get it ‘show ready’ or have to leave the house for an indefinite number of showings. We removed the uncertainty of how long the house would be listed and therefore how many mortgage payments they’d still be paying before it sold. We also eliminated the possibility of an appraisal and home inspection negotiation during the contract period. For all those reasons, we offered $85,000. We settled on $87,000 with $2,000 in seller-paid-closing-costs. A family member, who’s a lawyer, sent us a template for a contract, so we used that as a starting point, and I wrote up our own contract.

We first looked into a loan assumption. We started with several questions regarding how he was paying PMI (whether we’d have to assume the PMI, whether the PMI would be recalculated for the new appraised value based on our purchase, and whether there would be a penalty if we paid down the balance faster to eliminate the PMI), how the loan balance would transfer cleanly, and whether they needed to cash out escrow. After asking all these types of questions, we learned that PNC wouldn’t allow a loan assumption of an FHA loan since our intent was to use it as an investment property.

We did not do our own home inspection. We figured the HOA would cover the exterior, and we reviewed the home inspection he had completed two years prior. There had been a few upgrades since the initial home inspection, and there wasn’t anything that needed our immediate attention. We bought a new washer and dryer since the unit didn’t have any, and I painted most of it before it was listed for rent.

THE LOAN PROCESSING

Both sides of the transaction were able to sign the purchase contract electronically. We went through the whole loan processing without having to visit Kentucky. The attorney shipped the loan documents to us, we invited a notary over to watch us sign the papers, and then we FedEx’d the papers back to the loan officer for the sellers to sign.

While the closing itself went smoothly, we had several issues with our loan provider.

Our loan was a portfolio loan, which means that it’s a loan on the primary market and not backed by Fannie/Freddie. The interest rate was 4.5%; it was amortized over 30 years, but it had a balloon payment after 10 years. We paid careful attention to this loan (e.g., made many, frequent principal payments) because that meant we’d owe over $59k in 10 years.

It was amortized by 365/360 Rule (i.e., by the day) rather than the way it works in a traditional mortgage (annual rate divided by 12). In a traditional mortgage, the principal and interest difference is based on an annual APR, which creates a consistent amortization that gradually reduces the amount of interest in each month’s payment compared to the principal that will be paid. In the 365/360 Rule, each month’s principal and interest applied to the loan is different because it’s based on the number of days in the individual month. For example, in March, we paid February’s 28 days of interest, and in April, we paid March’s 31 days of interest; therefore, more of our March payment was applied to principal.

Here’s a snapshot of the amortization schedule, reflecting the changes of interest and principal by month.

The bank’s system was antiquated in that we could not make online payments unless we had a bank account with their bank. Being that this bank was in Kentucky while we lived in Virginia, we weren’t interested in opening a bank account and funding it just to pay this loan. This meant that all of our payments had to be sent by check to their location for keyed entry. The people responsible for entering these payments were not aware of the principal-only concept, and we spent almost the entire first year of the loan having to call every single time we sent a principal payment to have them reverse it, apply it as principal-only, and credit us the days worth of interest it cost us. After several months of this occurring and the response being that the teller doesn’t know how to enter it (then teach them…), we filed a complaint with the Better Business Bureau. We received all the interest owed to us as a result and all future payments were applied correctly.

Due to the poor relationship with the bank and the impending balloon payment, we paid off the loan faster than the 10 years. The loan was issued February 2016, and we made our final payment in April 2020.

PROPERTY MANAGEMENT

We hired a property manager since we were not local and didn’t want to manage showings or maintenance issues in an unknown market. The property management fee is 10% of the monthly income. We actually had several issues with the first property management company, but ‘managing the property manager’ is another post. We released ourselves from that first contract and negotiated with another company, who has been managing the property for the last 4 years.

We have also had to manage the HOA company to address water leaks that stemmed from the brick facade. Both times, the issue presented was eventually resolved, but never in a timely manner. Unfortunately, we are responsible for interior fixes (e.g., drywall) caused by the exterior cracks, which are covered by the HOA since it’s a townhome.

One final interesting story about this house. In November 2016, just a few months after we purchased the house, an intoxicated driver crossed the center line, hopped the curb, drove through the fence, and drove into the back of our townhome, destroying our HVAC unit and taking out a post of the 2nd story deck. It was a Sunday morning. We didn’t pay anything for this incident. The HVAC and a broken light were covered by the insurance company; the deck was repaired by the HOA’s management company. It was an incredible incident.

The townhouse hasn’t been easy to rent. We actually looked into selling it, but our property manager, who is also a Realtor, thought we could only list it at $90,000, which was not something we were interested in, having purchased it at $85k. Once the place is rented, we don’t have issues with maintenance, rent payment, or tenant-related issues. It just takes a month or two of vacancy before we find a qualified applicant. We have offered incentives for leases longer than 12 months to help eliminate our turnover rate and number of days vacant.

I shared that I would tell the stories of our home purchases. Instead of starting with #1, I decided to start with the most interesting. This property was being sold by a licensed Realtor, so we had a false sense of security. It ended up being the sketchiest (technical term) deal we’ve done. This is in Virginia.

We started with a home inspection, which revealed several issues. We requested the HVAC condensate line be cleared and the water in the backup pan removed. We also agreed to have our attorney withhold $1,300 at closing, to be paid to a contractor of our choice after closing, to repair other items found during the inspection. I can’t remember why we were handling the home inspection items, but that should have been the first red flag.

Our closing was scheduled for 8/18.

We were told that the HVAC repairs agreed upon were completed. We went to check on the progress of cleaning out the house and the HVAC repairs on August 10th. The HVAC’s backup pan still had water in it, and the house was filthy (after being told it was ‘vacant’ and ‘cleaned’). Plus, the electric was turned off. We had our Realtor reach out to the seller to cover our bases. Here’s his email:

While waiting for a response on this email, we checked with our closing attorney to ensure everything else was ready for closing; it wasn’t. We fully expected a “we’re clear” response, but instead we were told they were having trouble clearing the title. We weren’t given the specifics, but that’s not what you want to hear a week before closing. It ended up being cleared, but that was one more thing to worry about!

As typical, we had to do a final walk-through of the house to ensure it’s in the same condition (or better) as it was when we went under contract. Knowing how poorly the seller communicated over the previous month, we wanted to see the house the day before closing, rather than right before we head to the closing table. The electric was still not turned on, and it wasn’t cleaned. Our Realtor contacted the seller again. We were assured it would be addressed, and the electric would be on. We made plans to walk through the house in the morning.

Our Realtor was unavailable that morning, since this wasn’t supposed to be part of the schedule, so he sent a team-member to let us in. As luck would have it, she dropped the lockbox key below the front porch, so we couldn’t get in. We called our attorney and postponed the closing to later in the day. The Realtor was able to obtain a copy of the key to let us in, where we learned the electric was still off.

I contacted the electric company. I explained that I was the buyer, and the seller kept saying the electric would get turned on, but here we are at the 11th hour with nothing. The woman on the other end couldn’t tell me what she was seeing since it wasn’t my account, but she carefully played with words to let me know: sorry, hunny, but there’s no way this electric is getting turned on while under this person’s name because there is a high outstanding balance. She assured me that if I put it in my name, there wouldn’t be any issues. However, I wasn’t about to pay fees and put it in my name before the house was legally mine.

This is where we learned that a good attorney is worth his weight in gold. We never really understood the role of a closing attorney, since all our closings had gone smoothly (I mean, we could sign all the closing documents in about 20 minutes at this point). Since the electric wasn’t on, and we couldn’t verify the condition of the home, as required by the contract, our attorney withheld $5,000 of the settlement proceeds. The seller’s attorney was NOT happy, but it was entertaining to watch from our standpoint.

We had been provided a ‘receipt,’ dated 8/17 (the day before closing), that indicated an HVAC repair man had been out to do the work required. We are pretty sure that this was falsified. There was no electricity in the house that day, and there was still water in the pan on 8/18. Here’s the email I sent to our attorney releasing the $5,000 withheld, less the cost of my HVAC technician performing the repairs.

It cost me $125 for the HVAC technician’s trip. Our attorney told the seller’s attorney that he would release the $5000 less the $125. The seller’s attorney said he didn’t have any authority to allow that; so our attorney said he didn’t have any authority to release the $5000. Well, the seller’s attorney decided $4875 was better than nothing, and I got my $125 back.

All in all, everything fell into place, but there were many days and hours that felt like we were about to fall into a pit.

We purchased the house for $89,000, plus the $1,300 for contractor repairs, and the seller paid $2,000 of our closing costs (this minimizes the amount we have to bring to closing and allows us to leverage every last dollar we can for maximum efficiency). Our first lease was for $995/month, exceeding the 1% Rule. We closing in mid-August, and the first lease didn’t execute until October 1, which was one of our longer vacancies. That tenant renewed her lease once. Currently, the rent is $1,025/month. We sought $1,050 for a 12 month lease, and the prospective tenant negotiated an 18-month lease at $1,025. We accepted this because it was rented in October, and an 18-month lease brought as back to spring-time turnover. Even though taxes have risen since the purchase, we still maintain the substantial cash-on-cash return that is provided for in trying to obtain the 1% rule on investment real estate purchases.

After closing, I painted nearly the entire house (including the trim) over the course of a week; the house looked significantly better with just a fresh coat of paint. We also had to do a more thorough cleaning job than we’ve typically had to do on houses we purchase, including caulking the tub and cleaning the carpet.

We replaced the dishwasher with the first tenant, and then replaced the refrigerator after the second tenant kept complaining about the seal not working well. Most costly, the house has had several roof and siding issues. The kitchen was an addition with a flat roof, which typically causes problems. We replaced the gutters, fixed the flashing, repaired some siding, and then eventually replaced that part of the roof altogether. We also had to replace a cracked window, which was surprisingly under warranty. It took a lot of work to find the window manufacturer and a local distributor, but it surprisingly all worked out because it was a stress fracture and covered under a lifetime warranty.

Dave Ramsey has convinced (too many) people to pay off their mortgage and be “debt free.” Then you have Robert Kiyosaki telling people not to buy a house because its a liability, but never seems to address that you still have to pay for a roof over your head somehow. We subscribe to a different view – make your money work for you. There are certain types of debt that could truly benefit you, and a mortgage is one of those.

If we worried about paying down our mortgage, we wouldn’t have near the savings and investments we do, and wouldn’t be able to establish enough rental income to replace Mrs. ODA’s income, and being well on our way to replacing Mr. ODA’s.

We lived below our means, took some loans, and bought a house in one of the more expensive regions of the country – DC suburbs (oh, and while paying for a wedding). We knew we’d have no trouble qualifying for a mortgage and paying the monthly payment, but we didn’t want to pay Private Mortgage Insurance (PMI), which meant coming up with 20% to put down (i.e., about $80,000). In fact, we were pre-qualified for double the purchase price of a house than we were comfortable with because we were more focused on our down payment threshold than what we could support as a monthly payment (which is how a bank will pre-qualify you based on your other monthly debt payments).

Our first, expensive, little house that jumpstarted our investing before we even knew

Our primary goal to enhance our savings in the months leading up to the house purchase was to keep the cost of our daily food intake below $10 between the two of us. We were cautious with how we spent money on groceries, whether we ate out (meaning no buying lunch during the work day), and the types of activities we did. While most of our meals consisted of macaroni and cheese and pb&j, we did ‘splurge’ a little more once in a while (read splurge as meaning “2 for $20” at Applebee’s, not steak dinners). That year of actively watching what we spent paid off in ways we wouldn’t know down the road.

Three and a half years later, we sold our house for a $60,000 profit and purchased a home in the Richmond area for less than what that first house cost us when we bought it. That left a substantial balance in our savings account that needed to get to work.

We’re not interested in preparing for doomsday. In an emergency, there’s hardly anything that can’t be put on a credit card. If we can’t pay off the credit card, we have money in the stock market that can be liquidated within 24 hours to pay it. This perspective is particularly possible because we live a lifestyle that allows for a high savings rate while Mr. ODA is still W-2 employed, which means we’re even more unlikely to need stock liquidation to cover expenses. We weigh the risk of a possible emergency against not having our money make more money, which gives us the ability to live less conservatively.Since we’re not interested in maintaining 3x our monthly income in a savings account at 0.01% interest rate, the next option to discuss is paying down our primary residence mortgage.

Our mortgage rate was 2.875%, a very cheap lending rate [this was a 5-year Adjustable Rate Mortgage (ARM), a topic we can discuss in a future post on weighing mortgage options]. The question we had to ask was whether paying down the mortgage at a low interest rate was more beneficial than the income we could bring in with a rental property. If we paid more than 20% for our new primary residence’s down payment, was that going to provide us a greater cash flow to leave our careers before typical retirement age?

No, it wouldn’t allow us to leave our careers. So, we put the balance of money from the sale of our first home into the stock market and investment properties to make it generate income instead.

Our first investment property purchase was in February 2016. Since then, we’ve purchased twelve other investment properties, with the most recent two being in September 2019. Mrs. ODA’s income was replaced by our rental property cashflow by the time our son was born in August 2018; that’s within 2.5 years after we purchased our first investment property.

Of our 12 investment properties, two have mortgages paid off. First, there’s a maximum of 10 mortgages you can have when lending under Fannie Mae. There are ways around this in theory, but that’s another post. One of the mortgages we paid off because it had a balloon payment coming due. Another mortgage was paid off because it had a low balance and was one of the higher interest rates among our properties. Currently, we’re working to pay down two other mortgages due to their relatively high interest rates (5.1% and 4.95%), and each have a balance around $26,000 now. We’re choosing to pay down mortgages in this season instead of purchase new rental properties because we are not finding properties in decent condition that meet the 1% Rule. Plus, not having a mortgage on a property immediately increases your cash flow if you want to live off that monthly income rather than W-2 employment.

Had we chosen to pay down our primary residence mortgage instead of leverage our funds through mortgages, we’d still have a mortgage payment of over $1,500 per month and no other income strings. Instead, we still have a mortgage payment for our primary home, but we also have the cash flow that replaced Mrs. ODA’s six-figure income.