We last purchased a rental property in 2022, after most of our purchasing was done in the the 2019 era. We were busy with 3 kids, and I recently felt like I was coming out of the fog. Mr. ODA and I went to a wealth building seminar in the Spring; my intention was to have that seminar reinvigorate our desire to build our portfolio. It worked well for Mr. ODA, but once options started to show up, I started to panic.

We first went to an open house. It was a bit further away that I’d prefer to maintain a house, and there were a few red flags. For one, it frustrates me that landlords can fill out a seller disclosure claiming they know nothing about the house. I can tell you if I had any roof issues or major system issues in any of my houses, even though I haven’t physically lived there. Mr. ODA wanted to pursue it, but I couldn’t bring myself to get on board.

We were then sitting with his parents one night, telling the story of this open house, and his mom said that she saw a townhouse posted on Facebook that she thought we’d be interested in. It was owned by the son of an old friend of her’s. We asked our real estate agent if she’d show it to us, but she was out of town. So then his mom texted her friend to see if they were there and we could go look. They weren’t there, but they gave us the contractor box code (which is surprising in itself that there wasn’t a sentribox on the door). We went over and the house looked to be in good order, so we put an offer in. We like to surprise our agent with these types of things where all she needs to do is get the contract ratified.

UNDER CONTRACT

The house had been listed for some time when we came across it. It was was listed at $182,500. We offered $182,000 with $2,000 worth of seller subsidy on September 2, 2025. They agreed that day. We ended up needing to redo the contract because the wife wasn’t on the deed of the house, but she had signed the contract, but that wasn’t a big deal.

We had the inspection scheduled for September 10th. There was hardly any issues in the report, and we picked a few of the bigger things to ask for them to fix. They agreed to our list. They gave our agent a receipt showing they had paid someone to fix the items on our list. We did our final walk through the afternoon before closing and were disappointed to find that two of the bigger items (leaks) were not addressed properly and the house was dirty (including things left in the fridge and freezer). Our agent reported that to their agent, and they addressed everything that evening. We swung by the next morning before closing to see it all cleaned up and the leaks addressed.

The appraisal was ordered by our lender and came back at $188,000. That was a pleasant surprise to see we had immediate equity in it.

COMMERCIAL LOAN

We chose to go a commercial loan route. Interest rates aren’t falling as quickly as we expected to see. We have a commercial loan on one of our other properties in town, and I was still surprised to see how easy this process is. The loan qualifications are mostly based on the cash flow of the property. I filled out an application, submitted a ledger of our other property cash flows, and sent in 3 years worth of tax returns.

We were quoted at 6.74% interest. The loan terms are a bit different. Our last commercial loan was amortized over 25 years, but there’s a balloon at 5 years. This time around, it’s amortized over 25 years, but the balloon is at 15 years. A commercial loan also means that the taxes and insurance are not escrowed, and I’m responsible for paying them on my own.

The loan is an Adjustable Rate Mortgage (ARM) too. There was no different to us in the 3 year or 5 year ARM, so for the first time, we picked a 3 year ARM. In the past, it was related to securing our low rate. This time around, we’re expecting rates to drop in the near future, so we locked in our rate for only 3 years. It only changes on 3 year increments (some of the others will change every year after the initial lock period). It also has a clause that indicates the rate has a floor of 4%. I also don’t see a maximum adjustment that can happen (we have other ARMs that state an adjustment can’t be more than 2% at the change date).

We were expected to put 25% down. That would be $45,500 based on the $182,000 purchase price, and would leave 136,500 worth of a loan. They ran some numbers and determined that we could only qualify for a loan of $132,000 based on a rent of $1,400. They only us the cash flow to determine the eligible amount and not the rest of our portfolio. Let’s break that down to the fact that a loan of $136,500 equates to a monthly loan payment of 942.23, and a loan of $132,000 equates to a monthly payment of 911.17. So at a rent rate of $1,400, we could cover the monthly payment of $911.17, but we could not cover a monthly payment $31.06 higher. We pushed back for a second, but in the end it didn’t matter and we accepted the loan of $132,000.

PROS

When I look at this place, it feels like a place someone will rent. It’s clean, feels like home, and has a good layout. It has a closet available for a washer and dryer, which is a plus. Both bedrooms are upstairs and each has its own bathroom, and there’s a powder room on the main floor. It’s more secluded than other units in the complex, giving the occupant more grass area to hang out in the front and back.

CONS

We do have some concerns. The townhouse is at the back of the neighborhood. The entire rest of the community has parking right outside their front door. This group of 4 townhomes is separated from the parking lot, so you have to walk a bit further. The trade off there is that it’s secluded, you have a front “yard” (instead of pavement), and you’re more secluded from your neighbors.

I didn’t want another townhouse in our portfolio. With a townhouse, your value is strongly dictated by what your neighbors have done (or not done) to the property. As much as we don’t plan to resell these properties in a short time frame, I do have the thought that I want to be able to sell it when the time comes.

Also with a townhouse, you’re also at the whim of a community manager that is likely not putting utmost effort in. We asked about the HOA at closing and the previous owner said the cost used to be $35 per month. When it was that cheap, they weren’t paying their bills, so the lawn wasn’t mowed and the trash wasn’t removed. They increased the price to $95 two or three years ago, and that has made a difference in the community’s upkeep.

The HOA is due monthly, which is an inconvenience and a surprising process on their part. I plan to pay it monthly until I have confidence in their ability to process my payment and apply it to my account timely. After some time, I may pay in advance. I just went to process the first payment and planned to pay 3 months worth, but then realized that will create a harder tracking mechanism on me right now.

CLOSING

We had our closing on October 16th. It was super quick and easy. I listed the house for rent that evening.

SUMMARY

At this point, we have the house listed for rent at $1375. We had determined the range for rent during our purchase evaluation. Unfortunately, I hadn’t looked at the current market by the time we went to list, and there’s quite a bit out there. I’ve shown it to 2 people and have another showing today. One of the people from the weekend said they were seeing other places on Wednesday, so I’ll hold out on any changes to the rent price until this weekend.

We bought a Tesla. In the process, they’re offering a 0% APR promotion. They let you see how your credit rating affects your monthly payment (through different APRs). The final column in the table below shows the increase each level adds from the previous level.

This is based on a 60 month term. So, ignoring the promotional option available, between the ‘>720’ and ‘680-720’ would cost you $39 per month. That’s a total of $2,340 over the loan term. By using the promotional rate, that’s $88 per month “saved,” which is $5,280. Don’t let it be lost that working on your credit history and credit worthiness is something that pays off into the future.

When we look into a large sum of money leaving our account, we consider the “net present value” of the dollars. The net present value is the difference between the present value of cash inflows and the present value of cash outflows over a period of time. Investopedia uses the following over-simplified example. “An investor could receive $100 today or a year from now. Most investors would not be willing to postpone receiving $100 today. However, what if an investor could choose to receive $100 today or $105 in one year? The 5% rate of return might be worthwhile if comparable investments of equal risk offered less over the same period.”

The 0% interest loan through Tesla is for about $40,000. Mr. ODA calculated that our net present value of money, based on our approximately 4% savings interest rate, is $36,017. Taking nearly $40k out of our savings account wouldn’t be a financial problem, but it’s not the smartest financial move in our portfolio. Instead, we’re going to pay about $580 per month, while the “balance” of that $40k earns interest. At 4% interest, the balance of $40k earns nearly $1,000 in a year. That balance will continue to dwindle, therefore lowering the interest earned each year, but it’s still a significant sum of money. In the first few years, the interest earned is essentially paying a couple of months worth of the car payment.

By being conscious of our financial standing in the world, we’ve set ourselves up for earning these promotions. Had our credit worthiness been below a score of 720, it would have cost us over $5k more over those 5 years of the loan. While I understand that purchasing a Tesla may be considered a luxury, this concept and awareness can be applied across all financial decisions, which is why I wanted to highlight it here.

I have a tenant who, in the same day, told me that she couldn’t pay rent on time and asked whether she could buy the house. She said she paid $60,000 to me and that could have gone towards owning a house. While I understand the lump sum of what you paid being a pain point, owning a house isn’t that simple. I thought I’d break down a comparison of what she would have done to own this house versus her renting it over the last several years.

RENT HISTORY

Based on the proximity to Main St and the comps in the area, we went into the purchase expecting about $1,000 per month in rent. At the 1% Rule (where you set monthly rent at 1% of your purchase price), we should have been at $1,020. Knowing that it was October/November by the time we would get it rented (there aren’t as many people looking for a new rental in the Fall, after school has started and holiday activities are ramping up) we chose to list it at $975 and keep it below that 4 digit threshold. It sat for 3.5 weeks with hardly any activity, and we dropped it to $875. We found a tenant in under 2 weeks then, but we weren’t thrilled amount our cash flow on it.

The tenant’s lease started on November 1, 2019. Her rent was $875. My property manager incorrectly established a one-year term lease instead of an 18-month lease like she was supposed to, so we had to do a 6-month extension after the first year. Then in March 2021, we tried to increase the rent to $900, and she complained that due to the pandemic, she couldn’t afford that. We let it go and she renewed a year lease at $875.

Come February 2022, we were significantly under market value for rent and she hadn’t been a friendly tenant, so we were content pushing a raise to $950. If she didn’t want to pay that, she was free to leave and we would take the vacancy hit to fix it up and get it re-rented. She complained about the increase, and our property manager told her to take a few days to look around to see if she could find somewhere to rent that was at a price she would feel more comfortable with. She came back and said she couldn’t find anything and accepted the increase to $950.

Not including a few late fees she has owed over the last nearly-five-years, she’s paid us $52,850. While in total that appears to be a significant number, that number does not mean that you’d have $52k in equity in a home had you paid towards a mortgage.

OUR PURCHASE INFORMATION

We paid $102,000 for the house in 2019. We asked for several options for the loan structure. We asked about putting 20% versus 25% down, and whether the rate for a 15 year, 20 year, or 30 year loan would have the best rate. Going through those details is something I’ve done in the past, so for this purpose I’ll just note that we chose to put 25% down because then we didn’t need to “buy down” the rate. The rate for each loan length was 4.55%. With no incentive to do a shorter loan term (and therefore increase our monthly payment), we chose the 30 year term. I do want to note that our interest rate is higher than the average for 2019 (3.9%) because it was an investment property and not a loan for a primary residence.

Based on the 25% down and the closing costs, we had to come to the table with $26,589.12.

Our mortgage was $538.46, which includes escrow. We paid off this loan fairly soon after we closed on it, so we don’t have a monthly mortgage payment. However, I do need to plan for our current mortgage and insurance payments each year, which is currently over $2,000.

FACTORS TO CONSIDER

To keep this more consistent in the message, note that the loan discussed will be based on the purchase price of $102,000.

First, you need to have favorable credit to qualify for the mortgage. In an example, the lowest credit score I could plug in was 620. However, in much of what I’ve read, anything below 680 is questionable on qualification. Our requirement to rent a property is to have a credit score of 600. Perhaps there are lenders that will process a mortgage if your credit score is below 620, but you’re going to pay a premium via the interest rate.

With a credit score of 780, say you’ll have a rate of 6%. But then with a score of 680, you’re looking at 6.5%. At 6%, your principal and interest payment (doesn’t include the escrow required) would be $599.19. At 6.5%, it goes to $631.69. That’s only $32.50 per month extra; over 30 years, that’s an extra $11,700 paid to the bank. I have some tenants where an extra $32 per month is a big deal.

Without at least 20% down on a loan, you’ll likely have to pay private mortgage insurance (PMI). This amount could add a monthly premium to your mortgage payment anywhere from 0.2% to 6%. I did a quick calculator with the example of $102,000 purchase price, $3,060 down (typically the lowest available without any special loan structures is 3%), and a credit score of 620 (lowest it allowed). The PMI was calculated as $187 each month.

I mentioned that our final closing costs were over $26k. If I remove our down payment, that leaves $1,089 in closing costs. I will note though, that our contract had $2,000 in seller subsidy (a credit). Without that purchase agreement structure, that means your closing costs are actually $3,089. This means that you need to come to the table with $6,149. Buying a house is not like buying a car where you can roll all the costs into the loan, and I feel like people don’t realize this.

Your debt to income ratio also plays a factor in whether you can qualify and what your interest rate would be. So even with a decent credit score, you need to show a low debt-to-income ratio, meaning you can’t have your credit cards maxed out. The lender wants to see that you don’t have high monthly costs that would prevent you from paying your mortgage.

That brings me to the flexibility of paying rent. She paid $475 worth of August rent (due August 1st, with a grace period to August 5th before a late fee is owed) on August 20th. If you pay your mortgage late, there’s a late fee and it gets reported to the credit bureaus. Your late payment of rent doesn’t get reported to anyone. She also has the extra advantage that I’m willing to work with her on late payments. An apartment complex type owner is going to immediately file for eviction on the 6th without full rent payment, regardless of your story.

SUMMARY

While a mortgage payment of $538.46 looks favorable against a rent payment of $950, it’s not that simple. I was able to qualify for the mortgage, qualify for a favorable interest rate, and put significant money down.

If I add a premium to the rate we were able to get, assuming my tenant’s credit score is similar to what it was when she rented our house, and then add the PMI that would be applied by not having 20% down, then the mortgage payment (including escrow) would have been $903.02. PMI stays on the mortgage until you reach 78% loan to value ratio (unless you pay for an appraisal and can prove 80% earlier than that). That threshold in this example is $79,560. That principal balance would be achieved in over 11 years, which means you’ve paid $25,058 for essentially nothing.

Then on top of paying these premiums for the mortgage, she would need to pay for the maintenance of the property herself, which is included in my rent factors. I’ve paid over $3,000 for repairs and maintenance on the house over the last 5 years (which is fairly low). However, that includes a deck replacement that we did ourselves and probably would have cost $4,000 instead of the $400 we paid in materials.

So the next time you think that you could be paying half of your rent with a loan, know that you’re not looking at the whole story. There are many factors that go into a mortgage, especially the initial ability to qualify for such loan.

The day that’s in the contract as the closing date.

I truly can’t believe how many people have asked some form of this question in my life recently. While I’ve had multiple in person conversations on this topic, this post really stemmed from a Facebook post. “Is it an expectation for people to be moved out of their home the day of closing when buying a home? We sold our house, and are moving into a new home that we’re supposed to close the same day. Is there not a grace period?” What would that grace period be? How would the timing be determined?

On one side, I see the “closing date” section of a Kentucky contract simply states, “The closing of this transaction shall occur on the ___ day of ________________, 20__.” That’s quite useless actually (as I consistently find in KY law and legal documents). There’s a lot to be inferred by that statement, versus it being explicitly and clearly stated. On the contrary (as this has gone many times over), Virginia wins out.

In the paragraph before this image, it states where closing shall occur and by what date. This excerpt clearly indicates the purpose of “closing,” leaving little room for interpretation.

However, if we take a step back from the legal jargon and contractual obligations, whether explicit or inferred, we can see the logic. If you’re the buyer, once you sign the paperwork to purchase the house, wouldn’t you expect the keys to be handed over to you right then so you can start moving in and living in this house you just paid for? Wouldn’t you want the sellers out of the house because they’re no longer financially responsible for the house, and you don’t want any liabilities of their damage (intentional or accidental) to fall on your hands? You’ve done a final walk through and signed off that the house was in the condition you expected it to be in at that point in time.

Now this isn’t to say that there aren’t other terms and conditions that can be agreed to between both parties. “Lease back” or “rent back” clauses are commonly used. Sometimes it’s beneficial for a buyer to process the transaction (e.g., a rate lock expiration), but they allow the seller to remain in the home for an agreed-upon period of time (e.g., to bridge a gap before their new house is ready/available). But all of these terms are to be agreed to, in writing, before the closing date.

When we just sold our last house, we allowed the buyers to store things in the garage. We entered into a contract separate from the house purchase contract, called a “Preclosing Occupancy Agreement.” I haven’t needed one of these in Virginia, so I don’t know their standard form, but KY’s form does well here. The document outlines the date the buyer can take occupancy and whether there’s a charge for it. There were other items that outlined incidentals, such as utilities. In our case, the buyers were simply asking for garage space to put some of their belongings (because they had a same-day-closing for their sale and purchase), so we didn’t require them to put any utilities in their name before the sale.

BRIDGE LOAN

I can understand the complaint. Financially, you likely need to sell your current home to afford a new home. The “cash” from your sale is what you’ll use as your downpayment, as most people don’t have 20% of $400k sitting in a savings account (nor should you!). That makes the option to buy the house, take a day or two or seven to empty out your old house, and then sell your house not feasible.

There’s such a thing called a bridge loan. It’s a short-term loan used to purchase assets until long-term financing can be secured. There are more fees and high interest rates associated with this. However, it could be worth it to save the hassle of Private Mortgage Insurance (PMI). PMI is required in many cases where you cannot provide 20% as a downpayment for a house purchase. It protects the lender in case you don’t make your mortgage payments. PMI is removed when your principal balance falls below 80% of the original value of your home, whether that’s through regular mortgage payments or you make additional principal only payments. You can request PMI be removed earlier than that if you provide proof that your home value has caused your principal balance to now be less than 80% of the value, which is typically proven through an appraisal at your cost. If you put 0% down on a $400,000 purchase, it would take almost 12 years of payments before your loan reached 80% of the original home value. That’s 12 years that you’re paying PMI on top of your mortgage payment, and those are funds that are doing nothing productive to your net worth. A bridge loan may be worth it if you already have a sale date on your current house and only need to cover a few days or weeks.

SUMMARY

Logistically, it would be great if you could buy your new home, move all your things, and then sell your current home. Financially, this isn’t normally feasible. A lot of the time, you’re needing the equity you have tied up in your current home to purchase your next home.

Our first purchase was made up of two 401k loans (that we maxed as residential loans, which are penalty free), a gift from parents because we were short just a few thousand dollars, and cash on hand. We needed about $80k. Our second transaction, we chose a new build house. We sold our house, went into a rental for 3 months, and then used the sale money to purchase. Our third transaction was also a new build. We hopped AirBnBs until that got old with a 6 month old and 2 year old, and then crashed in Mr. ODA’s parents’ basement. We had 7 weeks between selling our house and purchasing the new one, so the cash from the sale went into our account, and we let it sit there until we needed it to close. Then this current purchase was actually done before we sold our third house, but we had executed a Home Equity Line of Credit prior to the sale. We used the HELOC to put the down payment on the current house, and then the sale of our third house paid off the mortgage and HELOC before distributing the cash balance to us. In all of these transactions, we had the ability to float the funds. That allowed us the ability to house our belongings in “long term” storage (not a day or two) for those two times we had a gap between the sale and purchase. The HELOC allowed us to slowly move our belongings to the new house this last time, and then we did a final moving day of all our big items just before closing (our current house needed work when we bought it, so we didn’t move right away).

But in all cases, unless there’s a separate document indicating so, the closing date of a transaction is the date that you give or take possession of the property. If you were buying, you wouldn’t want to take the risk of the previous owners messing with something in a property you now own. If you were selling, the buyers would have the same expectation.

Surprisingly, I didn’t cover all our houses in posts last year. I was going to say, “let’s finish this up,” but we’ve since purchased #14! This is a long post. I tried to separate the stories, but since they were part of the same purchase, it was too convoluted to decide which story went with which house.

We spent the summer of 2019 living in Lexington, KY. Mr. ODA took a temporary job for 3 months, and we spent our summer looking for more rental properties to try another market. The housing costs in central Kentucky were less than central Virginia, but the rental rates were also lower.

We drove around with our Realtor for quite some time. We were hoping to find a multi-door complex. However, 4-8 door units have just not been well taken care of. We take care of our houses, and I didn’t want to inherit all the deferred maintenance of a poor landlord. Many of the places had long-term tenants, so there wouldn’t be a vacancy to ease getting work done either. Additionally, there were several that we saw where the tenant was home, smoking and telling us all that was wrong with the property. It was abysmal.

So after searching through many other options, we settled on two houses at the same time.

FIRST OFFER

Mr. ODA actually made an offer on a house in Winchester that I hadn’t seen. It was a large house that had been converted into 2 units. Mr. ODA and our Realtor went after work one day, and it wasn’t worth me packing up the baby and driving a half hour to meet them for one house. However, I did get to see some of it because I took on the home inspection appointment. Since I had never walked through the house, it was easy for me to objectively see the information on the inspection and convince Mr. ODA to walk away. There was just too many big-ticket items (e.g., not enough head room for stairs, water damage not properly cleaned up in multiple rooms, several code violations) and deferred maintenance that it wasn’t worth us putting the money into it. The tenants were sitting on the porch smoking during the inspection, and I didn’t love the idea of inherited tenants that were allowed to smoke in the house.

SECOND OFFER

I can’t tell the history of these purchases without this gem of a story. Mr. ODA found a house that was in a decent shape in Winchester.

Aside: We focused on Winchester because while the rent income was low, the housing cost was also low. Whereas in Lexington, the rent was low, but the housing prices were higher.

We made an offer on the house. In the offer, it lists the seller’s name. It was a State Senator! When we sent over the offer, the seller’s agent agreed to our details, but asked for a pre-approval letter before he’d sign. The amount of weight the people in Kentucky put on a pre-approval letter is absurd, in my opinion. We went through the effort to get the letter and send it over. About that same time, the seller’s agent said someone else came in with a better offer, so we could either submit our highest and best offer, or lose the deal. The sketchiness of the action floored us.

The house had been on the market for a month. We had a verbal agreement (that had even been put in writing, but not yet signed). What are the odds that someone came in at the same time as us with an offer over asking for a house on the market a month? We called his bluff, and we were wrong.

THIRD AND FORTH OFFERS – UNDER CONTRACT

In August 2019, we went under contract on two houses in Winchester, KY.

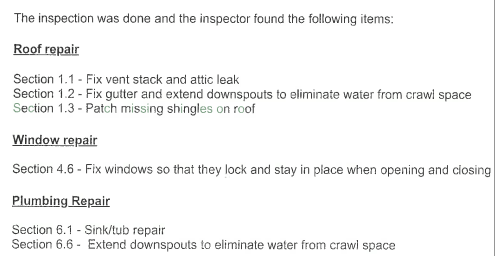

Property12 had been owner occupied and flipped to sell. The owner had lived there long enough that she wouldn’t Docusign the contract, and we had to wait for her to initial, sign, and date all the pages by hand. The house had been listed for 36 days when we made the offer. It was listed at $115,000, and we went under contract at $112,000 with $2,000 in seller subsidy (closing costs) on 8/7. It’s a 3 bed, 2 bath ranch at 1120 sf.

We received the home inspection on 8/14. We asked for the items below to be addressed, or to take $1000 off the purchase price. They agreed to fix the issues.

Property13 had been listed for nearly 3 months before we made an offer. It had been most recently listed at $105,500. Our offer was for $102,000 with $2,000 seller subsidy. We also included the following requirement in the contract: Seller agrees to remediate the water and mold in the crawl space, fix the down spout next to the crawl space door so that it channels the water away from the home, replace the missing gutter on the front of the house, and repair the rotted facia and sheathing on the front of the house.

Additionally, we had a home inspection on the house and identified the following items for them to repair.

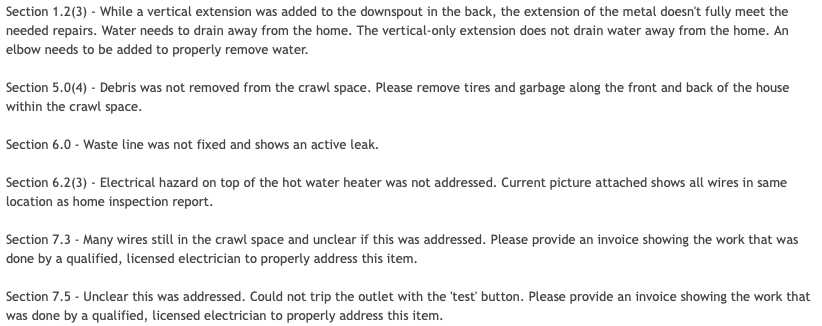

Getting the sellers to identify that these items were done before closing was not an easy task. We checked the day that closing was originally schedule for and noted that several things were not complete.

Then, at 7:30 pm the night before closing (which had already been delayed a week), we received one receipt identifying a couple of things were done. Eventually we received documentation that it was taken care of.

LOAN DETAILS

The options we typically ask for when considering the direction of our loan are as follows.

We chose the 25% down – 30 yr fixed option for both properties. Our goal is to not pay points, so that led us to the 25% down options. Since there was no incentive to take a shorter term (thereby increasing your monthly mortgage payments and decreasing your cash flow), we chose the 30 year option.

These loans were originated in September 2019. We processed multiple cash-out-refinances on some of our properties in December 2021; we used it to pay off about $66k on Property12 and about $74k on Property13.

LOAN PROCESSING & DELAYED CLOSING

We had a lender that we loved in Virginia. She couldn’t cover loans in Kentucky, but the company itself had a branch that could do it. She referred us to someone in Kentucky. It was the worst experience I’ve had in closings. Our closings are always annoyingly stressful in that last week, but this was bad throughout the month and then bad enough that our closing was delayed a week – completely due to the loan officer’s inability to manage the loan.

We had multiple issues over the course of the week we initiated our relationship just accessing the disclosures. They kept telling us to sign things we didn’t receive, or they’d tell us our access code and then when I say it doesn’t work, act like they never told us different information and give new information.

On August 16, I had to tell the loan officer that one of the addresses was wrong. THE ADDRESS. On August 26, we received conditional approval of our loan from underwriting. On August 27, we received our appraisal with no issues noted. But at that point, our August 30 closing was delayed a week already.

That’s where the problem was – our appraisal was ordered late, had to be rushed, and still didn’t make it in time for them to develop the Closing Disclosure (CD) and get us to a closing on August 30. The loan officer never once acknowledged that he ordered the appraisals late, causing this delay. It took asking for timelines from his supervisor, and piecing together emails we had on hand, to show that it was his fault.

On August 29, I finally made contact with the loan officer’s supervisor and was rerouted to someone else to get the job done. I had to repeat all of our issues and the errors that were found on the CDs.

On September 3, I was given disclosures that were still wrong. The new loan officer claimed that what she put in the system was correct, so she wasn’t sure what was wrong, causing me to once again outline all the errors.

On September 4, I was asked for more documentation that wasn’t caught during underwriting. I was furious.

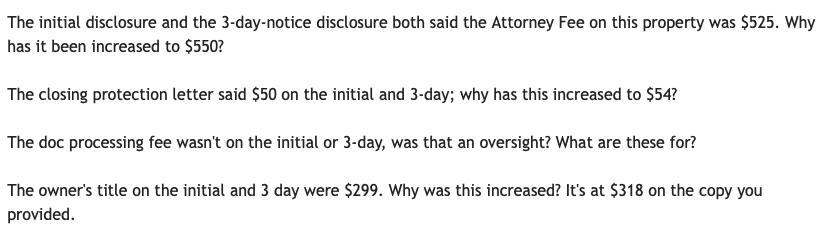

On September 5, I gave up talking to our lender about issues on the CD and spoke directly to the Title Attorney’s office, who was much more knowledgable and responsive. Here’s an example of what I’m questioning when I look over a CD. Some of these seem small (e.g., $4 difference, $25 difference), but you can see how these add up, both on a single transaction and when we’re processing several homes in one year. Not to mention – why pay more for something than you were quoted or you’re supposed to?

Another surprise that came our way was a “Seller Agent Fee” for $149 per transaction. At no point in time was an additional fee disclosed to us by our Realtor. A typical transaction has 6% commission paid by the seller, which is traditionally split 3% and 3% for the buyer and seller representation. Being that these were Rentals #12 and 13, in addition to 2 personal residences we had purchased, imagine the surprise when we, as buyers, were being charged for representation. We questioned why this wasn’t disclosed to us up front as a Re/Max requirement, and it was taken off our CD.

CLOSING DAY

I had planned to leave town the Friday after the original closing date because that was the last date that we had our apartment. I didn’t want to move me and the baby into my in-laws house and continue the poor sleep we had been dealing with by not being at home. So even though closing was delayed, I left. Mr. ODA had to be my power of attorney. He had to sign his name, write a blurb, and then sign my name on ALL those papers that are part of a closing….. times two. Eek. I didn’t know that at the time (but baby went back to sleeping perfectly once we were home, so it was worth my sanity 🙂 ).

At 11:30 am on closing day, the lender claimed that the power of attorney documents (from the lawyer…) were not complete enough to be counted as filed on their end. I appreciated the snip from the attorney when questioned.

I always wondered why tv shows always showed both at the closing table with a ceremonious passing of the key. We’ve had our share of weird closings (in a closet, in a parking lot, at our dining room table), but we never sat at the table with the seller in Virginia. We were so confused about how specific the closing attorney was being about the closing time options, and then we found out that the seller and buyer are at the table together in Kentucky. The seller for Property12 was so rude to Mr. ODA through the transaction! She kept grilling him on whether he addressed the utilities. The seller shouldn’t be allowed to talk to the buyer! We’ve since been able to process 3 transactions in Kentucky and avoid the seller at the table, but I’d like to advocate that Kentucky move away from this buyer/seller meeting process!

RENTAL HISTORIES

Property12 was listed at $895 on 10/2. Based on my birds-eye-view of the area, I thought $1000 was going to be easy to rent it at. Based on the 1% Rule that we had followed in Virginia, we should have a goal of $1,100 per month. However, we were trying for a Fall lease, which is more difficult than a Spring lease, so I thought listing at $995 would get quick movement instead of letting it sit for too long. Our property manager disagreed. She also said we were limited our pool of candidates by not allowing smokers; but, the whole house is carpeted and I was not budging on that.

We found a tenant on October 16 and allowed her to move in right away, but not start paying rent until November 1 if she agreed to an 18 month lease (we really wanted to be on a Spring renewal going forward). That was an unfortunate blow to our expectations – nearly two whole months without rental income on a house we didn’t need to do any work to.

We increased rent to $950 as of 6/1/2022 after no previous increases.

Property13 was listed for rent at $995 with no movement. We dropped to $875 and offered free October rent for however long was remaining in the month. A lease was established on 10/18/2019. Our property manager was supposed to establish an 18 month lease and didn’t. Luckily, the tenant agreed to a 6 month extension.

Property13 renewal came in April 2022. She had balked about the state of our economy in 2021, and we backed off the proposed increase at that time. Well, all the jurisdictions finally jumped on the increased assessments, and we saw a drastic increase in our costs. We told her that the new offer for a year lease is $950, which is higher than we’d typically increase in one year ($75 instead of $50). But we told her that we were willing to let her walk if she didn’t agree to it since she originally negotiated a lower cost and argued an increase at the 18 month mark, which we let go. She tried to fight it, but our property manager told her to check the rental options in the area to see that she’s still getting a deal. She agreed to the increase.

MAINTENANCE HISTORIES

Property12 requires a new heat pump in June 2021. We paid $3900 for a whole new system, which is a funnily low number just a year later.

The tenant there complained of high water bills. I asked to see a history of the water bills to know how much was considered higher than their average usage. The property manager agreed that the toilet was running and causing higher bills, but also admitted that they attempted to fix the toilet twice over a 3 week period, with multiple days between receiving a maintenance request and taking action. While I agreed that we could compensate her for the issue, I couldn’t quite pinpoint why this was my financial burden and neither the tenant’s nor the property manager’s. I followed up with more information from the property manager with questions like: Why did it take the tenant from 9/20 until 10/11 to identify the issue still remained and that there was a waste of water? They indicated that they believe they made a good faith effort to address the issues as reported. I eventually settled on a $25 concession on one month’s rent.

Property13 had several issues with the hot water installation that were eventually resolved, which was frustrating after we tried to manage issues with the hot water heater through the home inspection process and received documentation as if it was complete. The tenant requested pest control in July 2020 claiming that a vacant house next door caused an increase in pests. I was frustrated because that’s not how it works. I approved treatment at that time, and then she came back with another request in October. Luckily, I haven’t heard about pests since then. In my Virginia leases, we’ll handle some pest control requests, but if there are roach issues once a tenant has been there for some time, we don’t typically pay for that type of treatment.

SUMMARY

All in all, these tenants have been pretty quiet. They ask for random maintenance things here and there, but they’re not usually big-ticket items (except that HVAC replacement!). Our property manager has been more difficult than the tenants.

Being that we were used to the 1% Rule when we purchased these houses, it’s unfortunate that even at 3 years in, we’re not renting it at 1% of our purchase prices. Our cash-on-cash isn’t completely accurate right now because I won’t see our taxes for this year for another month or two. Being that jurisdictions kept the tax amount steady through the pandemic, I’m expecting to see an increase in assessments for this year. I’ve also seen big increases in our home insurance policies, so that will probably eat into our cash flow as well. Our cash-on-cash analysis on Property12 is about 6.5%, and it’s about 7.5% on Property13. These numbers are only slightly lower than our expectation/desire, with our average being about 8%.

In the upcoming year, we’re going to look to get rid of our property manager, so these houses may begin needing more attention from us. It’s been hard to take on more when paying a property manager has been a sunk cost at this point. However, the frustration of managing their management (e.g., making sure charges are correct, not getting a full picture of what work is being done, and then paying them a significant amount of management money and leasing money only for them to claim that checking on the property requires additional fees) has led to us wanting to take it on since we’re in town now. The current lease terms are up in April and May, so if we’re going to take on management, it should be before the possibility of paying them half a month’s rent for leasing it (not to mention they’re notoriously 4-6 weeks out in every leasing attempt they’ve done for us, whereas I’ve never had an issue getting a property leased within a week).

While the housing market has cooled some since I started this post in the Spring, there are still some areas that are moving quickly and aggressively, and this information is still helpful regardless of you being in a multiple offer scenario. Over the course of 6 years and 18 properties purchased (and countless offers made), we’ve caught on to some helpful parts of contracts. Again, keep in mind that I’ve seen real estate contracts in New York, Virginia, and Kentucky; this is not all encompassing or what may work perfectly in your market. This also doesn’t include all parts of a contract since most of them are standard and/or can’t be anything but matter-of-fact (e.g., will the property be owner occupied; is the property subject to a homeowner’s association).

BASICS

Your contract is going to encompass the basics of the purchase each time. This would be the buyer and seller names, address of the property, offer price, and closing date.

Typically, the buyer’s agent draws up the contract with the information being offered. If the offer is accepted by the seller, the seller signs the contract. If there are negotiations, the buyer’s agent will adjust, have the buyer re-sign, and then submit to the seller for signature. When the buyer makes the offer (which is just filling out the contract and sending it to the seller), the buyer will typically include an expiration date of the offer. This isn’t always enacted, but it’s there as a protection so the buyer isn’t sitting idle for extended periods of time waiting for a seller to make a decision. For example, we had an expiration clause in a contract recently where our offer expired at 8 pm that night, but we knew they weren’t going to review offers until the end of the weekend; we had put it in there as a way to hopefully push the seller to make a decision with just our offer instead of waiting for more offers to roll in. We ended up getting the contract on the house, even though our expiration date had technically expired.

In Virginia, the closing date language says “on or before X date, or a reasonable time thereafter.” In Kentucky, it says “on or before X date,” and if you can’t close by that date, you and the buyer have to process an addendum to the contract with a new closing date. We had a contract, as the seller in Virginia, close 2 months after the date in the contract. We were furious about that. We could have walked away and kept the buyer’s earnest money deposit, but then we’d have to formally list (it was an off market deal) and manage that process along with the home inspection issues that may arise. We also had a contract in Kentucky where our lender messed up and delayed our closing, so we had to sign an addendum to the contract to allow us to close a week late.

EARNEST MONEY DEPOSIT (EMD)

Earnest money, or good faith deposit, is a sum of money you put down to demonstrate your seriousness about buying a home. In most cases, earnest money acts as a deposit on the property you’re looking to buy. You deliver the amount when signing the purchase agreement or the sales contract, and it’s applied to your balance owed at closing.

This is not a requirement, but it’s showing your “good faith” to purchase the property because there’s a penalty to you if you try to walk away from the purchase.

In most cases, you pay the EMD to your realtor’s office and they hold it until closing. In Kentucky, they’re on it right away, asking you to send the check as soon as the contract is signed. In Virginia, I didn’t always send the EMD. The amount is listed in the contract, so if I were to default on the contract as a buyer, I would still owe that amount even though I hadn’t paid it to my realtor’s office.

Typically, you’re looking to put 1% down. On a $90k purchase, we gave an EMD of $900. On a purchase of $438k, we gave an EMD of $5,000 (but there were other factors at play as to why we went higher than 1% on that, which I’ll cover later).

CONTINGENCIES

Some items we’ve seen in our contracts are options for the buyer to back out of the contract, or a contingency.

Financing

A sale can be subject to financing. If it’s not an all-cash offer, and there will be a loan secured to purchase the property, data can be entered to protect the buyer’s interests. Typically, it’s going to list the years of the loan to be secured (e.g., 30 year conventional), a downpayment amount, and a maximum interest rate. The interest rates hadn’t been fluctuating much, but this would play into things in the past few months. If you tried to purchase a home when the prevailing interest rate was about 4%, and then interest rates rose to 5.5%, it may affect your ability to qualify for the loan or put you outside a comfort zone for your monthly payment amount. For example, on a $250,000 loan at 4%, your monthly payment is about $1200 per month (principal and interest); if the rate raises to 5.5%, your monthly payment becomes $1420 per month.

This information does not lock you into that break down. If the contract says 80%, and you decide to put 25% down based on the rate sheet, the contract isn’t changed nor is it voided.

Appraisal

If the sale is subject to financing, then it has to be subject to the appraisal. This is a lender requirement to protect their interests. There are some caveats to this, but I will cover them later since they’re more advanced. An appraisal will cost the buyer in the realm of $450-600.

If you’re attempting to qualify based on rental property income, the lender may require you to pay for a rental appraisal as well. We’ve seen this cost at an additional $150, but we’ve typically been able to negotiate our way out of that by providing leases and income history.

Home Inspection

This is one that I almost always recommend including in your offer. This is your “out” in almost every situation. If you get a home inspection, and it finds anything, you can walk away from the contract and not lose your EMD. If a house is important enough to you (a personal residence that you want regardless of what you find on an inspection report), you may eliminate this contingency, but you’ll typically include it. You can even include that you’ll do a home inspection and decide to not do it.

If the house is being sold as-is, it doesn’t mean you can’t get a home inspection. You can still get the inspection to know whether you want to move forward with the purchase. Being sold as-is just tells the buyer that the seller is not willing to negotiate price or fixing items if the home inspection finds something.

The buyer is responsible for the cost of the home inspection. We’ve paid between $300 and $650 for it. The inspector will take about 2 hours to look through the house, including the roof and mechanical parts behind the scenes. Sometimes the inspector will say “this doesn’t look right, but you need to consult a professional in that trade,” which is usually what happens when it comes to roofing. We have done a home inspection, found too many issues to manage (e.g., stairs built out of code) and walked away from the contract. In that scenario, we don’t lose our EMD, but we did pay about $500 for “nothing” (unless you count all the savings of not throwing money into the house to make it safe and livable).

If you find items on the home inspection that you don’t or can’t fix yourself, and the house isn’t being sold as-is, you can request the seller address them. An addendum to the contract will be filed to identify what the seller agrees to fix, and professional receipts have to be supplied before closing to satisfy the requirement. A seller may say they don’t want to be bothered with coordinating the trades to fix the items and offer financial compensation (e.g., we project the cost of these fixes to be $1000, so we’ll take $1000 off the purchase price).

In the realm of “the contract can say almost anything you want,” here’s an example of an additional term that was in one of our contracts. On this particular house, we should have walked away. The closing process was a nightmare because the seller hadn’t paid the electric bill, so we should have known that them wanting a free pass on inspection items was a red flag.

Virginia has a clause to protect the seller’s ability to walk away from the contract in the event of drastic home inspection repair costs.

Wood Destroying Insects (WDI)

A WDI is basically your termite inspection (may include carpenter bees, ants, etc.). We learned with our very first home purchase that this inspection is pretty useless. You can teach yourself what outward signs to look for regarding termite damage. It’s a visual inspection of what the technician can see. But the damage caused by WDIs is behind the drywall. If there’s signs of WDIs outside the studs of the walls, you’ll see it, and that means you have a big problem. Pay the $35 for a professional to say there are signs of active termites.

Another way we found that the WDI is useless is that we had a major termite problem in our house. We were paying for treatment when we sold the house. The treatments weren’t working and the next step was pulling up all the flooring in the basement and treating under the foundation ($$$). The termite company wrote their report: There is an active infestation of termites that are actively being treated. Technically, true. Productively, not the whole picture.

‘ADVANCED’ CONTRACT OPTIONS

I don’t know that these are necessarily advanced, but they’re less common options when making an offer. Some of them come in handy at opportune times, so it’s helpful to know the options at your disposal.

Seller Subsidy

The seller subsidy is the seller’s contribution to closing costs. It reduces the seller’s bottom line based on the offer amount, and it reduces the amount of money the buyer needs to bring to the settlement table. If a contract offer is $102,000 purchase price with $2,000 seller subsidy, then the seller’s bottom line is $100,000.

There is a limit of how much seller subsidy can be in a contract, which is based on the lender’s requirements and is typically 2% of the purchase price. We have had to adjust the contract to account for this limit before we were aware of it; we kept the seller’s bottom line the same, but adjusted the numbers so that we could maximize the seller subsidy.

In Virginia contracts, there’s a boiler plate section identifying the possibility of seller subsidy. In Kentucky, it has to be written into the additional terms section.

Escalation Clause

If you’re in a multiple offer scenario, it may be helpful to offer with an escalation clause. This is an option that a prospective buyer may include to raise their offer on a home should the seller receive a higher competing offer. The buyer will include a cap for how high the offer may go. It’s essentially a way for the buyer to compete with other offers, but not necessarily pay top dollar for the house.

Most recently, our offer was $420,000 and we were told there were at least 4 other offers. We added an escalation clause to our offer. We decided to make it a strange number (e.g., increase by $1770 at a time), and we capped it around $450,000. We were basically saying that we were willing to pay up to $450,000 for the house, but we didn’t have to commit to that number by making our offer at $450,000. The highest offer outside of our offer was about $436k, so our escalation of $1770 over highest offer got us the house for about $438k.

AppraisalGap Clause

As mentioned, a home purchase with financing is going to be subject to an appraisal. With the housing market exploding purchase prices in the last couple of years, houses have been selling for well over list price. This is nice in theory, but that doesn’t mean that a bank is going to agree that your purchase price is “fair market value.” If your contract is for $500,000, but the home values in the area only support $420,000, the bank is not going to give you a loan based on $500,000. Either the seller has to agree to accept the lower purchase price, end the contract and start over with the listing, or the buyer has to agree to pay the difference in value in cash. A gap clause is preemptive attempt to address this difference between the contract price and the potentially lower appraisal price.

If the buyer believes that the area’s home prices will support a purchase price of about $450,000, but they want to make an offer of $500,000, the buyer may include a gap clause of $50,000. This means that the buyer is more attractive to the seller because the seller’s risk of the contract falling through after the appraisal comes back is minimized. This also means that a buyer would have to be able to show the lender that they have the cash to cover the gap clause needed (if needed), the down payment, and the closing costs.

We used a gap clause on our most recent purchase. The list price was $415,000. I was confident that an appraisal would cover up to $425k, but I didn’t see many comparable sales higher than that without venturing into different neighborhoods. We offered, with an escalation clause, up to about $450,000. Since we weren’t sure that the appraisal would go that high, we offered a gap clause of $25,000. Our final purchase price was $438k, and the lender waived an appraisal need, so our gap clause wasn’t enacted.

RANDOM CLAUSES

I mentioned that a contract can almost say whatever you want. Here are a couple of examples of protections we put in an offer that had to be satisfied within the term given or we could walk away from the deal with no penalty.

SELLER THOUGHT PROCESS

The seller’s comfort comes into play when you’re in a multiple offer scenario. A buyer can make an offer saying almost anything they want (within reason of a residential real estate transaction). You can manipulate your offer to show the seller how vested you are in the purchase. Sometimes a seller just cares about the bottom line numbers, but sometimes (like if you’re competing with a similar offer), a few tweaks to your offer may make you more desirable.

I mentioned that we went higher than 1% on our EMD for our personal residence purchase. We wanted to show that we were very interested in the property, so one way to do that is to show that we have a lot of “skin in the game.” If we default on this contract, we’re out $5,000 and getting nothing. Whereas, when we’re purchasing a rental property without emotion, if it doesn’t go through, it doesn’t go. Sticking to about 1% is showing that we’re “checking the box,” but not that we’ll do anything and everything to make sure this deal goes through. We would still be out some money and get nothing if we walked from a contract without enacting a contingency, so the higher EMD you include, the more serious you appear.

A seller may not understand the big picture of providing the subsidy, so that could be risky. If a seller sees that they’re contributing to $2,000 of your closing costs, they may balk at it. Hopefully, they have a realtor on their end that can explain “think of your offer as $100,000 instead of $102,000.”

Eliminating a home inspection may make a seller feel more comfortable too. They may know of some issues in the house and are waiting for the “shoe to drop” through the inspection process, so it could eliminate a stressor for them. I wouldn’t recommend eliminating a home inspection unless you’re confident there aren’t any fatal flaws in the house (e.g., quarter width cracks in the foundation, wet marks on the ceiling, warped/sunken flooring).

The housing market has slowed down, so some of the out-of-the-norm clauses may no longer be worth the buyer’s risk just to compete for a house, but these are some options out there. The general concepts still apply, like when to pay for extra inspections or to expect financing and an appraisal to go together. Know that everything is a negotiation and don’t feel stuck in a contract if red flags are flying.

When reaching out to a loan officer, there are a lot of options to choose from. I’m hoping to break down the decision-making here. I’ll share how we ended up with several different options, too.

Basically, it boils down to:

Put enough down to avoid paying Private Mortgage Insurance (PMI)

Don’t pay more than 20% unless there’s a decent incentive.

Don’t pick a loan term shorter than 30 years unless there’s a decent incentive.

Carefully evaluate any Adjustable Rate Mortgages (ARMs).

PMI

I broke down PMI in a previous post: PMI – Private Mortgage Insurance. We suggest doing whatever you can to meet the requirements to avoid paying this. The cost of PMI can be a couple hundred dollars per month, which is money that can be put towards the principal balance of your loan or other bills, rather than in the bank’s pockets. There are also hoops to jump through to remove PMI early, which may include paying for another appraisal on the house ($400-$700!).

LOAN TERMS

A conventional loan will likely require 20% to avoid paying PMI. There are some loan options out there that may allow a smaller down payment without a ‘penalty’ (e.g., PMI, higher interest rate), but 20% is the standard, and is usually required when purchasing an investment property.

There may be an option to put down more than 20% or you may think you can afford to pay a higher mortgage each month, so you’re interested in a shorter loan term. Unless there’s an incentive (e.g., lower interest rate, better closing costs), stick with the bare minimum to get the loan.

If there is an incentive, you’ll need analyze the math and your goals to determine if committing extra money to a higher down payment or a larger monthly payment is worth it. If you have extra cash each month, you can pay more towards your principal rather than pigeon holing yourself into a higher monthly payment. Plus, if you have more cash liquid, you may be able to purchase another rental property, which will increase your monthly cash flow.

While we evaluate the loan terms on every house purchase, I’ll share the details of the two most “unconventional” options we chose. Two things to note: 1) lenders add a ‘surcharge’ to the rate for it being an investment property, typically around 0.75%, which means the rates aren’t going to be the great, super-low, rates being advertised; and 2) the term “point” means a fee of 1% of the loan amount.

HOUSE #2

For House #2 (purchased in 2016), we were informed that if we put 20% down instead of 25%, the rate would increase 0.25% on average. If we assume a 30 year conventional loan, 20% down at 4.125% equates to about $69,700 paid in interest (assuming no additional principal payments); 25% down at 3.875% equates to about $60,800 paid in interest. By putting an additional $5,850 as part of our down payment, we saved about $9,000 in interest over the life of the loan.

Once we determined that we’ll put 25% down, we then had to figure out the appropriate loan length. On this particular offer, 30 year amortization wasn’t an option for us because we would have had to pay a point to get a competitive rate. We chose a 20 year amortization because the house already came with a well qualified tenant, we didn’t expect a lot of maintenance and repair costs due to the house’s age, and we didn’t have an immediate need for a higher monthly cash flow based on our place in life at the time.

While our long term goal was to have rental property cash flow replace our W2 income, this house was early in our purchasing. At the time, we were focused more on paying off House #1 (higher rate and a balloon payment after 5 years). Frankly, we didn’t truly understand the power of real estate investing at this time, and didn’t know how much it would accelerate the timeline for us to meet our goals. By decreasing our loan length, we increased our monthly payment, but also lowered the total interest paid over the loan’s life by over $22k. Since more of our monthly payment is going towards principal reduction than had it been a 30 year amortization, this loan isn’t on our priority list to pay off early.

HOUSE #3

For House #3, we evaluated the rate sheet for the loan term, interest rate, and down payment percentage again. This house was purchased a few months after House #2, so those rate decisions were fresh on our minds. We were quoted several options: 1) 20% down at 4.25% for 20 or 30 years, 2) 25% down at 3.75% for 20 or 30 years, or 3) 25% down at 3.25% with 0.5% points for 15 years.

As you can see, there’s no incentive to pick the 20-year term because it’s the same rate as a 30-year term. If we have additional cash, we can make a principal-only payments against the 30-year term rather than unnecessarily tying up our money.

At first, we thought paying points was an absolute ‘no.’ However, points aren’t a bad thing. Paying down your rate up front can save you an appreciable amount in interest. Plus, points are tax deductible.

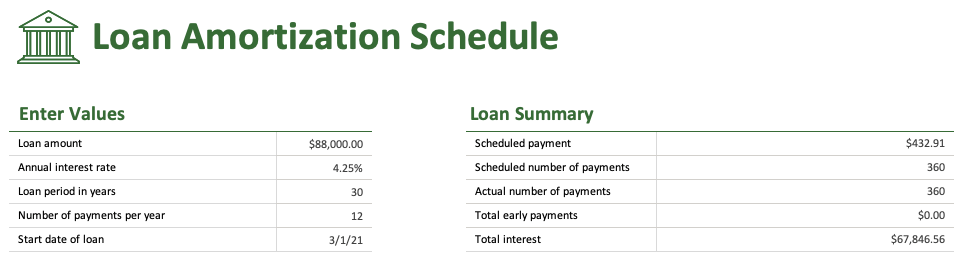

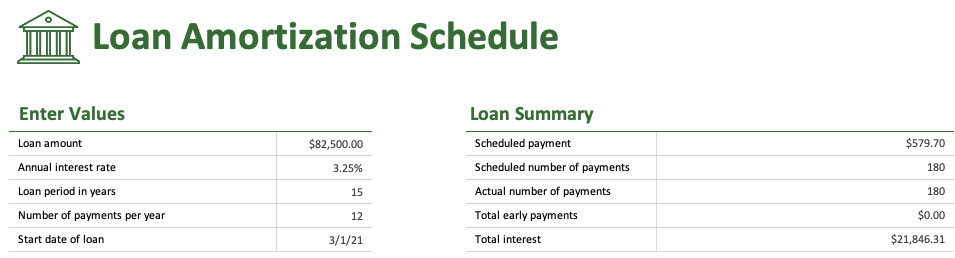

Now for the breakdown of each options. Let’s say the house purchase was $110,000 (because it wasn’t an exact number, and it’ll just be easier to use a ‘clean’ number like this). Microsoft Excel has an amortization template where you can plug in the loan terms and see the entire amortization schedule.

Option 1: 20% down payment equates to a loan amount of $88,000; the annual interest rate is 4.25%; the loan is for 30 years, with 12 payments per year. If we make no additional payments, this totals about $67,800 worth of interest paid over the life of the loan.

Option 2: 25% down payment equates to a loan amount of $82,500 at 3.75%. If we make no additional payments, this totals $55k worth of interest paid over the life of the loan. This requires an additional $5,500 brought to the closing table, but saves almost $13k in interest. It also decreases our monthly principal and interest payment (i.e., not including escrow) from Option 1 by $50.

Option 3: 25% down payment, 3.25% interest, and 15 years (instead of 30 years) equates to just under $22k paid in interest. To obtain the 3.25% rate, it required “half a point.” If a point is 1% of the loan amount, that would be 1% of $82,500. This rate only required 0.5%, so that meant paying $412.50 as part of closing costs along with the additional $5,500 of down payment required for 25%. However, the shorter loan length means that monthly payment is increased (between Option 2 and Option 3, the difference is $197.63).

For about $6k, we pay a higher monthly payment, but we also save a significant amount of interest over the life of the loan. The short loan term of 15 years means this one is also not on our radar to pay off while we focus on paying down other, higher interest and higher balanced, mortgages. In this case, the benefits of the big picture math outweighed the increase in monthly payment.

We are five years in on this mortgage and are already seeing significant reduction in the outstanding principal due to the amortization schedule becoming favorable more quickly. In 10 short years more, our house will be fully paid for, through rent collection, without a single dollar of extra principal payments from our other financials. What a great feeling.

ADJUSTABLE RATE MORTGAGES (ARMs)

An adjustable rate mortgage can be beneficial depending on the terms and how long you expect to own the house. For us, we expect to hold our investment properties for a long time, so it wasn’t worth the risk of an ARM. Many times lenders won’t even offer an ARM on an investment. However, when we purchased our DC suburb home, we knew we didn’t expect to be there for more than 5 years, so we chose a 5 year ARM.

After a positive experience with that decision, we also chose an ARM on our second primary residence. We chose a 5 year ARM, even though we expected to be there longer than 5 years. We figured we would either accept the new rate, if there was one, at the end of the 5th year, or we would refinance when necessary. As a result, Mr. ODA monitored rates and refinance options over the last year or so. Unexpectedly, we sold that house 3.5 months shy of the end of the initial ARM term so we didn’t have to do anything.

I break down all the details of an ARM and our decision making in a recent post.

SUMMARY

When I reach out to my lender to ask what the rates of the day are and begin the process of locking a rate on a new loan, I ask for options. These options are in the form of a “rate sheet.” When you ‘lock’ a rate, you’re actually locking the ‘rate sheet,’ not the individual decisions of loan length and percent down. For every house, we evaluate the rate savings that can come from doing something less “conventional” than a 30-year fixed at 20% down mortgage. Our decision is based on what’s best for our goals and our cash in-hand.

As shown above, in our early decisions, we favored shorter loan terms for rate savings. but since House #3’s purchase, we noticed how much more we cared about low monthly payments and low down payments to allow us to buy more properties along the way. Every investment property loan since House #3 has been the ‘standard’ 30-year fixed at 20% down. Because of this perspective shift, we were able to buy six properties in 2017, which gives us about $2,000 in monthly cash flow that we can then use to pay down mortgages.

Don’t pay it. Get creative for your down payment. Here’s a brief on how PMI works and how we avoided paying it.

What is PMI?

A lender typically requires PMI when the loan is greater than 80% of the loan-to-value (LTV) ratio because it’s higher risk for them. If a buyer has less of their own money as equity in the property, the bank views this as a higher probability the homeowner will default on their loan. With that, the PMI is required until the borrower reaches at least 80% for the LTV ratio and the loan is in good standing for at least 5 years. This typically means that a borrower needs 20% of the purchase price as a down payment. There are a few exceptions, but overall, if you don’t have a 20% down payment, you’ll be paying PMI.

PMI can be up to 2% of the loan balance. The lender uses your credit score/history, the down payment amount, and the loan term to evaluate your risk and set the PMI rate.

While there are requirements that the PMI must be removed when your loan hits 78% and 5 years in good standing, you can request the removal of PMI earlier if your house value has risen (e.g., market fluctuation, improvements you made). If you request the removal of PMI, you may be required to pay for the new appraisal, which is an added cost. You should weigh the cost of the appraisal against the remaining payments. In a broad example, if the appraisal costs $450, and your monthly PMI is $120, then as long as you have more than 3 months left before hitting the 78% LTV ratio, it’s worth paying the appraisal fee to have PMI removed. There is also a risk that the appraisal doesn’t come back with a high enough house value, so you should be confident in your home’s value before requesting said action.

How did we avoid paying PMI?

While we were more than qualified to purchase a home in the D.C. suburbs based on our debt-to-income ratio, we restricted ourselves to what we could afford as the down payment.

A bank qualifies you based on your debt-to-income ratio. If you have low recurring monthly bills, then you’re qualified for a larger loan. At the time, our only recurring monthly payment was on my vehicle, at about $350/month. The bank pre-qualified us for about $700,000. Sure, we could “afford” a monthly payment on a $700,000 mortgage, but then we couldn’t eat, sit on furniture, or do anything else. 😉 We’d also be paying PMI because we didn’t have 20%, or $140,000, to put down.

Also due to our low debt-to-income ratio, we couldn’t qualify for any programs that would allow anything less than a 20% down payment for a mortgage. We set our purchase limit at $350,000, which meant we would need $70,000 for the down payment, plus closing costs. Due to the limited inventory at that price in the DC suburbs and the knowledge that we were pre-qualified for double what we were searching for, our Realtor kept pushing us to raise our purchase price. However, we advocated for ourselves and kept our focus on what we could afford as our down payment so we wouldn’t pay PMI. After months of searching and seeing places that were literally missing floors and walls, we increased our search to $400,000, hoping that if we found something in the 350k-400k range, we could negotiate it to 350k.

Our move to the D.C. area was not in our original plans. Mr. ODA had been saving through high school and college, expecting to buy a house in a lower cost of living locality. When we moved to D.C., we knew that we would need to change our expectations and day-to-day actions. We rented an apartment in Fairfax, but we didn’t want to be putting over $1600 per month towards rent for long, and we’d prefer to be paying towards a mortgage and building equity in a home. Positives to owning a home: mortgage tax deduction, appreciation, and the equity building that you get back when you sell the home.

While we rented, we were conscious of our spending. We aimed to spend less than $10 per day on food between the two of us, and we limited how much we ate out. We did activities with Groupons or restaurant.com coupons.

We moved to DC in December, and over the summer, we put an offer on a flipped foreclosure. The listing was $384,900; our offer was $380,000 with $2,000 in closing costs. It was denied by the bank, as we were told we were the 2nd best offer of 3. The next day, we got a call that the bank countered our offer. Apparently, the first offer attempted to negotiate their offer further, and the bank moved on to us. They countered $380,000 with no closing costs; we accepted. We now had to scrounge up about $80k for closing.

We looked into a Thrift Savings Plan (Federal government’s 401k) loan. Many warned us against the idea, but our research showed it wasn’t as much of a concern as others let on. The details of this loan option are on another blog post. We decided to each take a residential loan from our accounts. I took a $15,000 loan and Mr. ODA took a $25,000 loan. We also borrowed $5,000 from Mr. ODA’s parents and paid it back within a couple of months. We avoided PMI.

An argument heard about not owning a home is that it costs a lot to maintain a home. While owning the home for 3.5 years, we gutted the main floor bathroom ($4,000), replaced the AC ($3,600), replaced the hot water heater ($1,100), resolved termite issues with treatment and wall replacements ($2,000), laid carpet in the basement living area, improved the yard through grass maintenance and purchased a shed, and painted a few rooms. We sold the home for over $60,000 more than we purchased it for (tax free since it was our primary residence the whole time), far more than the minimal expenses we put into it.

Key takeaways from our experience:

The efforts we put in to avoid paying PMI meant we had another $100-200 in our pockets per month. Instead of padding the bank’s ‘pockets,’ we paid ourselves back with interest into our retirement account.

We lived below our means, saved, and kept focus on the big picture.

We pushed ourselves to our financial limits to begin building equity in a home, rather than paying rent to a landlord (or in our case, an apartment company). The efforts put in that year have paid off time and time again, starting with selling the home 3.5 years later for a profit that led to some of our first rental purchases.