Well, tracking spending is just bugging me. We’re over where I want to be in monthly spending. I registered the kids for summer camps, so that was $580 more than usual spending. I also paid for a kid to take swim lessons ($85) and our gymnastics cost went up because she earned a spot in an advanced class that’s a half hour longer. If I take out the camp registration cost, then our spending is about $1700. My goal is $1350 per month. That’s not what we can actually afford (Mr. ODA’s number is higher), and I’m learning may not be realistic, but that’s my general goal each month. I’m halfway into March and can tell you that we’re going to be nowhere near that number this month, which is frustrating, but also reality.

RENTALS

We had two service calls this last month. One was a water heater being out and the other was unnecessary but cost us $100. This lady has actually been a problem in this realm. She claimed the mail key didn’t work for weeks and took forever to respond to messages. Mr. ODA finally went over there and it turned out she was trying the wrong box and not paying attention to what Mr. ODA was telling her. Then she said the microwave wasn’t working. The circuit was tripped, and Mr. ODA let her know that she can’t run an airfryer and microwave at the same time. Then she said the washing machine wasn’t working. We had an appliance guy go out and he said, “it’s working fine. There’s not supposed to be any more water than this in a high efficiency machine.” So much fun.

I’m expecting a tenant to move out at the end of this month. I still haven’t heard the final information on that, which isn’t surprising, but that’s on the horizon.

I increased the rent on two units over the last couple of weeks, which is in addition to a raise I put into effect on another one last month. I also have let three renew at the rate they were at the past year (or more) based on their cash flow numbers and the tenants in there.

PERSONAL

I’m still working part time. Although, these hours are 50% more than I had signed up for. I’m helping get another office organized and training a new hire. It’s been a lot. I feel productive, but I want more hours in my day. Mr. ODA started a part time job as well. We’re on the hunt for insurance help. We’re paying out of pocket for the whole policy that we were under for the last 5-6 years. While we’re not expecting a lot of coverage to be paid by the employer, there is a benefit to having the funds come out pretax.

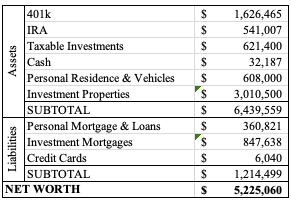

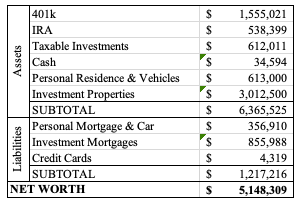

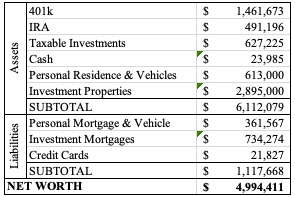

NET WORTH

Well, my update isn’t really that accurate. I’ve updated the numbers I could, but I’m already days behind on my schedule, so I couldn’t wait for Mr. ODA’s numbers anymore. We are still carrying half of the window order on credit cards (and that install should be next week… hopefully… it’s been pushed back once already). Our investments are down even more than last month, but I don’t know the extent at this time. Our net worth decreased from last month, with 10 accounts not updated, so I’d say it’s a substantial hit.