It’s getting to be that time of year when large payments need to be made. I’m projecting out our account to cover several tax payments in October and December. I’m also paying insurance amounts, such as $1500 for two houses that’s currently on the credit card. We also have about $5,000 sitting on that 0% interest credit card that will need to be paid off by October 1st (when the 0% incentive expires).

Our credit card balances are higher than average because of rental payments. In addition to the insurance payments, we had an invoice come in that I knew was going to be high. We paid for the water line from the street to the house on a rental to be replaced, which was $3,080.

June and July were rough sick months on us, so now I’m paying those medical bills almost daily it seems. We reached our deductible early this year, so these are just the coinsurance amounts; those $5-20 payments add up though.

Our insurance adjuster finally came out, three weeks after the incident. He literally said “I’m not a contractor, and I’m not from here so I don’t know the codes,” and then proceeded to do the estimate wrong. He was missing items, called things the wrong thing (like a Trex water proofing system that costs $1500 just for materials, he called it a “vapor barrier” and put $190). Now we’re waiting on a second adjuster to come out and meet the deck contractor to go through what actually needs to be done. All the while, our 3 year old keeps sadly saying “I don’t like our broken deck.”

I had to call a medical provider and get some money back. I told them I didn’t want to pay in advance because then I have to call them to get my money back. They said “we’re good about sending it back” and said “it’s simple, it’s just 5% of the total cost.” I said “the total cost isn’t what the insurance allowance is, so whatever I pay you will end up being less.” So now I had to take time out of my day, after giving them a month to do it on their own, to call with 3 kids in the background making noise, and get my $5 back. But then there was a surprise where another urgent care that we saw almost a year ago sent me back the $20 I paid them. That one had slipped through the cracks on me. I had noted that I overpaid them, but then I had a baby!

We had two rentals not be able to pay rent on time this month. One was able to pay on the 12th, which they did. Another paid what they could, and I’m still waiting on the rest. I actually told them to catch up as they could because I didn’t want them to not be able to get their 3 kids ready for school. I’m waiting on an invoice from our handyman for work he’s done on multiple houses, an invoice from an HVAC guy who did work weeks ago, and a roofer to start his job that’s been two months in the making.

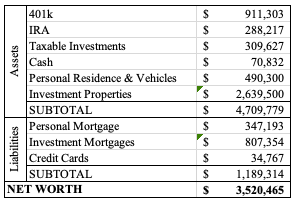

Our overall net worth went down slightly from last month because of market fluctuation. Our cash increased by over $30k, but that’s because we received a check from our insurance company to replace our deck after a tree fell on it last month. Some of that is going towards replacing furniture that has been bought already (so it’s on a credit card), and some of it is a reimbursement for the outlay I already made to remove the trees that fell on the deck and fence, but some of it is still to be paid out when the deck is replaced. In the meantime, we’re earning interest in our savings account on it at least.