Well, Mr. ODA didn’t like that I shared I didn’t know where our money was last month. They’re all kinds of Treasury accounts, and I’n just logging the transactions and leaving him to it. 🙂 I don’t have a lot of bandwidth these days, but I’m learning to juggle 3 kids and our finances.

PERSONAL FINANCES

We bought a new van this month. We’ve been wanting a new one for a while now. We bought our 2017 Pacifica in September 2020. It was a great deal, and it was a necessity as we were about to spend 7 weeks “homeless” and AirBnB/couch hoping. The car had some defects. We decided we’d keep an eye out for a newer version. Suddenly, Mr. ODA found a good deal on a 2020 Pacifica that had more options than we were actually looking for. We drove to Ohio about 36 hours later. They made us a good deal for our trade-in, and we went home with a new van! We put some of the purchase on two credit cards and then the balance with a personal check.

We’re currently paying close attention to credit card deadlines and our savings account. Where I used to pay a credit card bill almost after the statement closed so that it wasn’t hanging out there and I wouldn’t accidentally miss a deadline, I’m now leaving money in our savings account as long as possible. Our savings account is now earning 4% on the balance, so we’re seeing a significant amount of interest each month. I’m juggling managing our bills as close to their due date as possible, while also projecting future bills necessary since there’s a limit of 6 transfers out of the savings account per month.

All that was to point out that our credit card balances are high right now because of the van purchase, but the credit card statement hasn’t closed yet. Instead of paying the credit card balances down right now, the money is sitting in savings earning interest for 4-6 weeks between the purchase, to the statement closing, to the statement’s due date. More directly, we put $3,000 on one credit card for the van purchase. That was on 2/7. That statement, once it closes, will not have a due date until 4/20. That means that the money put on the credit card can sit in savings earning interest for about 70 days.

We also had to pay the initial payment for the restoration services on the rental that had a burst pipe. So while the insurance company sent us a check to cover the cost of this work, it’s still $17k sitting on our credit card, not being paid until the last minute. I should also note that our cash balance is inflated by about $50k because it’s the money from the insurance company that we’re waiting to pay the contractor as milestones are completed.

Had I seemed nonchalant about the plan? Because I’m definitely not. 🙂 I need to stay on top of how many transfers happen per month out of the savings account (while Mr. ODA randomly pulls money for investments), and not miss any deadlines and cost us interest charges or late payment marks on our credit. It’s stressful! Since we’re not doing anything that requires our credit to be pulled right now, it’s fine. If we were having our credit checked, having multiple cards nearly maxed out would be a problem. But we know we have the cash available to pay off all the credit cards if we needed to.

RENTAL FINANCES

I finally got through to someone on the issue with the improperly installed water heater. He says he submitted all the paperwork to send us a check for $200 to cover the plumber we paid to fix their issue. I haven’t seen any paperwork, nor have I received the check, but I’ll keep it on my radar and follow up in a couple of weeks.

I made all the decisions on the restoration of our flooded house. We’re expecting to hear a timeline for work to start next week, and then it’ll take about 40 working days to get the work done.

I paid a warranty for termites on another house. We had an infestation when we purchased the house, but we didn’t pay the warranty information. Our tenants found swarmers, and when we called to ask about treatment, they said they’d let us backpay the warranty and invoke that. We have a good relationship with this company and appreciated that offer, so we’re staying on top of the warranty payments now. The payment is $98 per year.

We received a surprise in the mail – the tenant had turned off the electric in the flooded house back on January 12th. The power company is supposed to notify me. I received an email on February 6th notifying me of an action on the account. So this was in my name from 1/12 to 2/1 for me to be billed $255 without my knowledge. Not to mention, there’s a bill hanging out there from 2/2 until the present that I’ll also get billed for. Mr. ODA sent our property management excerpts from the lease indicating that the utilities must be in their name for the entirety of the lease, that they’re responsible for this bill, and that they must get it back in their name immediately. We’ll see how that plays out.

RENTAL WORK

I picked up the keys from our property manager for the 3 houses I took over managing. I also worked on a rental here in town this week, which took about an hour including travel time, and I have another to work on later this week, which will be about 2 hours worth of work.

I sent a prospective tenant the pre-application we have, which he passed, so I sent him the application to submit. If all goes well, we’ll have that house re-rented with no vacancy period.

We have 3 leases that end at the end of April. We put a requirement that tenants give us 60 days notice, or that we give 60 days notice of any changes. That means that these leases need acknowledgement by the end of this month. So I ran the analysis on those 3 houses. We decided to increase the rent on 2 of them by $50 per month, each, and we’ll keep another house the same since it was increased last year. One house actually had an increase last year, but that house is well below market value, so we’re offering them to continue the lease with an increase because if they were to move out, we could get even more from the house based on it’s size and demographics. The 2 houses we’re increasing have a property manager, so she’s responsible for notification and signing an addendum before the end of the month. But once again, I need to manage the property manager and ensure we have action on time.

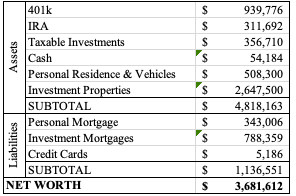

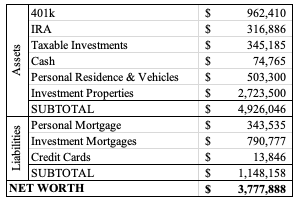

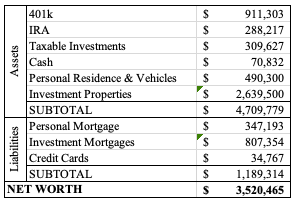

NET WORTH