We opened a new credit card to purchase windows for our house. When we bought our house, there were 3 windows that had the gas seal broken and were dirty looking (not cloudy like I’d think would happen). Three sashes were really bad. One is on the side of the house in our bedroom, so we never see it. The other is the window over the garage, so front and center. We just keep the black curtain drawn so hopefully you can’t notice it, but it’s definitely noticeable if you look for it. Over the past 3 years, more windows have started to go. Some are getting to the point of being that bad, and some just have a holographic look to it that you can catch at certain angles. We also have a couple of windows that are freezing if you get near them. In my daughter’s room, I line the bottom of the curtains with stuffed animals to keep some of the cold out and let the animals absorb the cold.

Well, it was time to open a credit card then.

All of these companies are happy to open a line of credit for you. You can make payments on your windows (or really anything) for 5, 7, 10 years. Well, if you have good credit and don’t open credit cards often, you can look into giving yourself an interest free loan for 12-18 months.

We look for a credit card that offers at least 12 months of 0% interest and a reward of some sort. Usually the reward is related to an amount of cash back if you spend a certain amount in a certain period (e.g., $300 cash back if you spend $5,000 in the first 3 months).

We’ve done this several times. We opened a credit card to pay for IVF to have our first child (~$30k). We opened a credit card for the new carpet we put in our current house (~$10k). Now we opened a new one for windows ($11k). We pay about $500 (at least the minimum monthly payment owed) per month and always by the due date. If you are late on a payment, you forfeit the free interest and may even owe the interest that would have been owed on previous payments. Then as the end date of the 0% interest gets closer, we make a plan on where money will be transferred from savings to pay it before that date.

That’s one of the keys. We’re not taking this because we don’t have the money to pay it right now. We’re opening a credit card to allow our money to earn interest in a savings account of some sort for all that time. So instead of spending that money and losing that income, we delay the payment as long as possible to keep our money working for us. If you need something and don’t have the money to pay it right now, but you think you’ll be able to make payments on it as you earn income, then make that the variable. Don’t open a credit card if you haven’t ever and don’t plan to have that amount of money within the term. We also don’t open a new credit card while we’re paying on the previously opened credit card. In this instance, we paid off the balance of the carpet this past October. While it would have been nice to delay opening a new card a bit longer, the windows are really in rough shape, so we only had 2.5 months without a large credit balance to think about.

Many of our activities over this last month were already paid for or minimal cost. We went to Colorado, and we’ve been doing back to school type activities. Mr. ODA was in Colorado longer than the rest of us (I flew home on my own with 3 kids!), and he went on a work trip for a week, so my goal has been activities outside of the house as much as possible in this final stretch before school starts. We’ve had quite a few activities on rental properties too.

RENTAL PROPERTIES

Historically, if the 1st through 5th of the month falls on a Friday, that’s the day that I receive rent. Meaning, if the 3rd is a Friday, then I get rent that day. This month, the 2nd was on Friday. I received very little rent. Going into the 5th, I was still waiting on 60% of rent payments; I was already told by 3 tenants (making up 23% of that amount I’m waiting on), that rent will be late this month. Luckily, 2 of those 3 tenants had paid partial rent already. That left 4 houses going into the 5th that hadn’t paid and I hadn’t heard from. That’s more than normal and was a bit worrisome. By the time of this post, I’m missing nearly $2,000 worth of rent, which is over 10%.

We’ve had several small actions that needed attention from our handyman, so I paid out on that. We had an AC go out before a hot weekend, so we had our technician go out and fix that (I haven’t seen that bill, but it’s expected to be around $1,000). Mr. ODA went out to a local house to properly fix their kitchen cabinets that were apparently never installed correctly (before we owned the house) to install them into the studs.

I was called for a garbage disposal that wasn’t working, and I attempted the fix on my own. I was nervous going into it, but I successfully fixed it in about two minutes. That felt good. I also went out to check on a roof replacement at a local house, and Mr. ODA replaced their deck. This tenant doesn’t communicate well whatsoever with us. She said “the deck is in bad shape.” That was it. Didn’t send a picture, didn’t give any details. I went out to check on it, and the deck stairs were hardly sturdy and none of the pickets were installed anymore around the decking part (it’s more of a landing than a deck when you think of size). It’s infuriating that people could not communicate such a dire issue. Most of my tenants do a great job, but this is why annual inspections are necessary.

PERSONAL ACTIVITIES

It has been a crazy month! I have thrived with the busy scheduled and a sense of accomplishment.

I was elected to our Homeowner’s Association board of directors this past month. I’ve spent a significant amount of my time going through that information and trying to get things organized and back on a schedule. I had my first meeting on the Landlord/Tenant Advisory Committee. And I joined on with a start-up school to be their financial consultant.

We signed our oldest kid up for Fall Ball and our second for gymnastics. She did acro last year, but I said all year that she would thrive better in actual gymnastics where they do more activities than dance. Our oldest started kindergarten, which is really exciting. That also required a lot of attention between back-to-school activities and paperwork to be filled out. I ran a 5k with zero training (I had run 1.4 miles the week leading up to the race), but my friend and I beat last year’s time by 5 minutes!

We worked on our own deck. A tree fell on it last July. We had to get our insurance company to understand our issue and fully cover the repairs that were necessary (it took them forever to get an engineer involved instead of all different adjusters). We finally got started in March on the replacement. After weeks and weeks and weeks of our contractor working on it, he finally ghosted us because he couldn’t get the waterproofing to be waterproof. So this past weekend, we tore up our deck boards and repairs the waterproofing issue. It’s supposed to rain this weekend, so hopefully we’ll see that our fix worked finally. Once we prove to ourselves that no water is getting down there, we can have the electricity finished. We also built a little wall to hide the storage being kept under the stairs under the deck, which was cool.

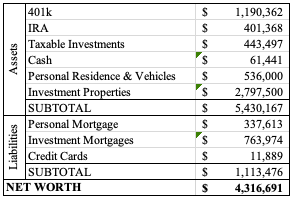

NET WORTH

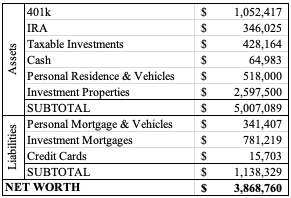

Obviously, our investment accounts diminished slightly since last month, as the stock market has been a constant discussion point recently. Last August, my updated said: Our overall net worth went down slightly from last month because of market fluctuation. So this seems to be a typical cycle! Last year it was offset by a large insurance check we received, while this year our cash balance is much lower from last month to this month.

I have about $9k to still pay out on a roof replacement (insurance is covering most of it), about $1k to pay to a plumber, and a couple of other odd jobs that are waiting on invoicing. Our net worth isn’t 100% accurate this month because I don’t have access to a few accounts (well, I have the log in and password, but it requires either text or email verification to get logged in, and Mr. ODA holds those and isn’t available – annoying!). I also have a $1500+ insurance payment to make, but I’m purposely holding off until this credit card statement cycle ends so that I can feel like one month isn’t a crazy high balance.

To update our net worth, I have spreadsheets set up that I overwrite from last year. Last year’s August update had our net worth at $3.78 million. So even though this month is over $27k less than last month, we’re still up over $500k from a year ago without any drastic changes in investment portfolio.

Back when I spent my days working in front of a computer, it was easy for me to analyze our spending. These days, with 3 kids in tow, I’m lucky to record our finances timely. There’s no time for analyzing. But over the past two years, I haven’t been happy with our spending total for the year, so it was time to look into it a bit more. It’s hard to know what has changed since I don’t have month over month, or year over year, trends to compare this data to, but it’s a start.

There are some caveats.

I don’t include any spending that isn’t on a credit card here. That means some of our rental property bills aren’t captured (they’re paid via Venmo or check), but I decided that’s ok because I can see that in a different way (a separate spreadsheet). Those expenses are reactive and a necessity to running the business, so it’s not like I can change a spending trend there. I’m more curious about our actual expenses and where our money is going for personal decisions. There will be some rental expenses captured here though.

I’m doing this analysis for the first half of the year. If this was for a month at a time (which is a goal), then I’d be able to dive deeper into spending at each place. For instance, at Walmart, those expenses aren’t always ‘grocery.’ However, I don’t have the time to go through all the purchases and siphon out non-food purchases. I did go through most of the Amazon purchases and categorize them.

If a purchase was made at Lowe’s or Home Depot, it’s classified as home improvement. It may have been rental property work, but generally it’s related to something we’re doing at our house.

If a purchase was made while on vacation (such as amusement park, tolls, hotels, dog sitting) , it’s categorized as ‘vacation.’ If we were on vacation and purchased food, it wasn’t labeled as vacation. All fast food or restaurant purchases for the first half of the year are categorized as ‘restaurant.’

If we did an activity from home, it’s labeled as ‘entertainment.’ If we did something related to sports (this includes swim lessons, ticket purchases for performances, etc.), then it’s labeled as ‘sports.’ The entertainment versus sports delineation is because something like a single tournament could be considered entertainment, but I kept all sports items as ‘sports.’

None of this includes whether we were reimbursed by someone else for a purchase. For example, we purchased tickets for 15 of us to go to an amusement park on vacation, but we only paid for 4 tickets of that personally. Mr. ODA is a personal shopper for restaurants, so much of our restaurant shopping around town is actually later reimbursed in that process (but not captured here because it’s not a credit card line item).

In the process of going line-by-line on my expenses, I discovered that I never received a refund for something. I placed an order on Etsy for a personalized gift for my niece’s birthday. A few days later, I went to check the status of the order, and I discovered that the shop I ordered from was no longer selling on Etsy. I was frustrated that I received no email that told me my order wouldn’t be fulfilled. I contacted Etsy customer service. At the time, I misunderstood Etsy’s billing process. I assumed it was charged when the item shipped. As I was just going through charges, I realized that the amount was charged on the date of purchase (e.g., not when shipped), and I had never received a response from Etsy. After another frustrating round of attempting to contact customer service this morning, I finally received a resolution. Now my ‘to do list’ has to keep track of this refund appearing. It’s $10.01, so it’s not the end of the world. However, it would be nice if Etsy shuts down a seller (their words), that they manage the outstanding orders without me having to take my time to get it corrected. Plus, if I let every “it’s just $10” go, it could add up quickly.

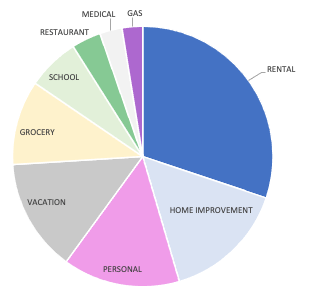

FIRST HALF OF THE YEAR SPENDING

By far, our largest slice of the pie up there is for rental expenses. Honestly, I’m happy to see that so much of our credit card expenses are taken up by rental expenses we had. I pay our insurance premiums (where they aren’t escrowed) via credit card, and I can pay our county taxes for one house with a credit card, which I do for the cash back rewards. There was flooring replaced at one house, which was a significant amount of that slice.

The ‘home improvement’ category includes new patio furniture we purchased, but were reimbursed by insurance (a tree fell on our deck). It also includes the electrician work and dirt fill purchases that we needed for the deck rebuild. Our house has a few more fairly large projects we want to complete, so I expect that to continue being a larger chunk.

I know that our “grocery” expense isn’t completely groceries. I’d like to focus on this category of spending more in the second half of the year. I want to quantify what’s purchased at Walmart that is actually grocery versus personal shopping type purchases. I think that our grocery purchases are higher than they should be, but I can’t put my finger on exactly why. Historically, I’ve blamed it on ‘bulk’ shopping; Mr. ODA will go to Kroger for the “buy 5” type sales. I’m not sure that’s it though.

We don’t eat at restaurants very often. We usually eat at fast food places while we travel or are away from home at an inopportune time. When we’re at home, we’re usually eating at a “personal shopper” experience where our food cost is mostly reimbursed (although that’s not captured in the chart).

Our health insurance deductible is $3,200 per year, so we expect slightly more than that each year in the medical expense category (and based on how deductibles work, that expense is front loaded in the year). I actually pre-paid a bill at a child’s urgent care visit. I paid them $50, but that visit, along with two more visits since then, came to a total of $12. I’m waiting for their reimbursement of that difference.

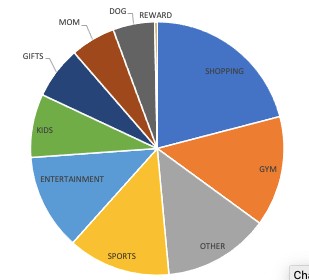

PERSONAL SPENDING

I’m going to dig deeper into the ‘personal’ category. I labeled a bunch of things as ‘personal’ as a means of not having too many small slivers of the overall spending pie. This includes all gifts, needs for kids (new shoes), clothing for kids, gym membership, sports, etc. It includes a ‘shopping’ category. I spent some time going through my Amazon orders and categorizing them, but the ‘shopping’ category was too daunting and difficult to parse out further. About a third of the ‘shopping’ category is Amazon orders through Mr. ODA’s account that I didn’t pull up to categorize. The rest is random purchases that were probably related to gifts or kids clothing.

For entertainment, this is small things like going to the movies (which we go for $2 per ticket), bowling, and aquarium. The largest chunk of this pie part here is actually 4 season pass lift tickets for our family’s future winter season. I put the ‘mom’ category to see what I’ve purchased for myself that wasn’t a necessity (e.g., a travel cosmetic bag, baseball shirts to wear to my son’s games), as well as my one hair cut and one pedicure that I’ve gotten this year so far. The ‘other’ category is boring stuff – utilities, car maintenance, professional fees, etc.

Had I gone through my Walmart orders in detail, I would have been able to identify some more purchases that could be removed from ‘shopping’ and put into other categories. For instance, the ‘dog’ category is actually higher because I order his glucosamine and tooth cleaning treats from Walmart most of the time, and that’s a monthly expense. His annual vet appointment is in the Fall, so this will be a larger slice of the pie for the end of the year.

SUMMARY

Our annual credit card payment total for the last three years have been about the same. While it’s a ‘win,’ that it isn’t increasing, it’s still at a number that I don’t like. Mr. ODA has been working towards a ‘retirement’ date. We’ve pushed it back just because his job hasn’t significantly impeded our lifestyle, but the day will eventually come. If it’s next year, I’d feel better if our credit card payments weren’t as high.

I went into this expecting my grocery category to be higher than I’d prefer. I didn’t identify much of what is causing that, so I’ll try to focus heavily on watching that expense each time it hits the credit card, rather than trying to remember what each purchase entailed six months later.

I was surprised to see the gas category such a small sliver of the pie. We’ve done a lot of trips (although, I suppose a majority were in July, which isn’t captured in this data). It appears living in a smaller city and doing things mostly on this side of town means we’re not having to fill up our tanks too often.

Overall, I didn’t notice any egregious spending. We don’t spend for the sake of spending. This year we traveled more than we had the previous two years, but mostly our spending is the same. Now that we’re two years into our house, there are less projects that we’re putting money towards. I’m encouraged that now that I’m looking at this, I’ll be able to identify areas to scale back.

We have several rental properties in Richmond, VA. However, we moved away from the area in September 2020, leaving the properties under a property manager’s oversight. My goal was to make it back to the houses annually to do walk throughs of properties. It’s surprising how many people don’t tell landlords about issues timely. Since most of our properties keep long term tenants in them, we don’t get eyes on the condition of the house regularly like we would if we were turning over the house between tenants.

Generally, I check to make sure their HVAC filters are changed out, that they don’t have any piles of garbage or old food (or the gigantic pile of laundry that was blocking one tenant’s second form of egress), that the yard is maintained, and simple things like that. I also take this as an opportunity to fix or improve things that I know need attention, but weren’t necessarily worth the up-charges of hiring the action out to a contractor.

We did a walk through of the Richmond houses in July 2022. At that time, nearly all our properties had long term tenants in them. A few small items came out of those walk throughs (e.g., change out filter, re-caulk the tub). While we hoped to get there last summer, it just wasn’t in the cards with our 3rd baby.

Based on the rest of our summer schedule (and soon to be constriction of school schedules), we were only able to get there for 2 full days. None of the work that I wanted to get done is a high priority; it’s mostly work that would improve the aesthetic of the house or help the longevity of an investment (like a new porch).

PROPERTY 7

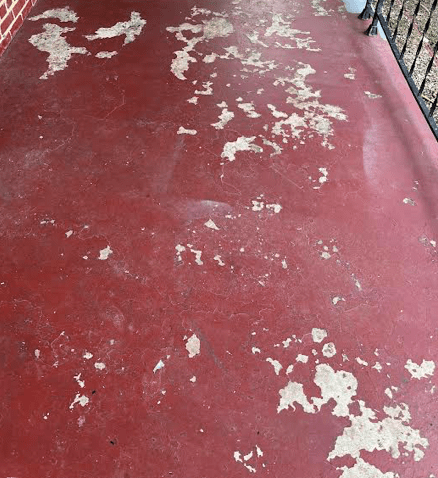

This house recently turned over. The house was flipped when we purchased it 7 years ago, and we knew that everything that was done before we owned it would just be a bandaid. We had a couple of long term tenants in the house, and we even had quick turnovers because people needed a place to live, so we didn’t have time to do major renovations. It was time. We put a lot of effort into fixing up the place (e.g., all new paint, new flooring and fixing of subflooring). The front porch and front door were red, and it just made the house look dingy. I wanted to make it look better. See: not a priority, but something worth looking into eventually.

I arrived on the evening of the 4th to pressure wash the porch so it would dry by morning when I would paint it. I did not account for how bad the condition of the paint was. It appears someone just painted over peeling paint years ago. There were several layers of gray, purple, and red colored paint. The latest paint job had several places where that was the only layer of paint on the concrete. Very odd, but that meant that I had to scrape as much flaking paint away as I could. I spent over 10 hours on this. Not exactly what I had in mind. I scraped and scraped and scraped. I then put two coats on. I’m nervous how long it will hold up though. I did this during an extreme heat advisory so it likely didn’t cure correctly by drying in mere minutes.

I also did 3 coats of black over the red door. I don’t think it’s going to hold up against her animals, but at least it looks better from the street.

This house still needs the back deck pressure washed and painted. However, this is something I’ll do either with tenant turnover or if we sell it. It’s really worn down and places are missing paint because we removed the covered portion of it. The porch railing had also been painted at some point and is peeling, but I hadn’t budgeted time for that. I did a few touch up areas with black paint to cover where previous owners had painted it red.

PROPERTY 3

The tenant here reached out to me a couple of months ago to tell me that a salesman broke their doorbell. Fascinating. They claimed “well, it’s old.” My thought was “well, it’s meant to be outside, and the house next door was built the same time without any doorbell breakage now.” But instead of sending someone out to fix that, I put it on our to do list. It took Mr. ODA about 2 minutes worth of work, and the new doorbell cost $10.

While there, we cleaned out the gutters. That’s been a known issue throughout the life of this house because there are a lot of trees around the perimeter. We also cleaned the mildew growing on the house.

PROPERTY 2

This house is a mirror image of Property 3, but the trees in the backyard are much closer to the house. The back of this house had significant mold growth on the siding. We got all the siding cleaned up there too. Mr. ODA got on the roof to clean out the gutters. While up there, he also cut some trees off the roof.

The first picture is a ‘during’ picture because I didn’t get a ‘before.’ The part at the top that is dark is actually better than what was there, and it was over the entire back of the house. We soft washed with a mold and mildew cleaner and got it looking almost brand new.

PROPERTY 9

During the last turnover period of this house, we had the front porch jacked up (it was sinking), had the front stairs redone (they were sinking too), and had the back decking replaced. I had intended to stain the new wood for this house, but it being well over 90 degrees precluded that action. Instead, Mr. ODA got the siding on this house all cleaned up, and he cut/pulled several large weeds that were growing.

DRIVE BYS

We did drive by the other Richmond properties that we have. I didn’t have the time (or energy) to schedule walk throughs of everything. Once you do a walkthrough, you inevitably end up with a list of things to do to the house. I already had a lengthy list of things to do, so I didn’t want to manage that right now. Just by driving by, I did add to my to do list that one house needs its gutter replaced (how does a gutter, with no trees around, twist away from the house), and that their back deck really needs to be replaced (just the deck boards and railing; the substructure is fine).

I’ll need to make it back there to walk through the properties. If nothing else, it gets the tenants to clean things up once a year. One of our property managers offered a filter check quarterly, which was really used as a way to get into a house and make sure things were being kept clean and orderly. While a filter should be changed that often, I think that’s too much time being in someone’s place they call home. However, once per year is worth it to keep things moving in the right direction and to make sure there aren’t any maintenance issues that hadn’t been reported.

I had this post mostly written by Wednesday, but we traveled earlier this week, and I haven’t kept track of the day very well. This is the first I’ve been able to update our net worth and get this done. Ironic, considering how I started this post when I expected it to be on time. And now..

This past month has been exhausting on me. I knew March was going to be busy. We had a bunch of sports schedules to manage, lots of kids birthday parties, hosting my dad for a long weekend that coincided with 3 family birthdays and the first anniversary of my mom’s passing, an assortment of Easter activities, a trip, and random other events. On top of managing these day-to-day things for our family, our deck replacement started, and we had to work on a massive turnover of a rental property. I’m in a perpetual state of tired these last few weeks.

DECK REPLACEMENT

On July 2nd of last year, a storm blew threw that destroyed our neighborhood. Honestly, we’re surprised by how little actual structure damage there was for our neighborhood because it looked like a war zone with the amount of trees down. A couple of houses had a tree fall on their roof, but only cause minimal damage that resulted in shingle replacement. We appeared to bear the brunt of the worst, which was a tree falling on our deck, crushing our furniture, moving all the supports, and cracking the concrete blow it. Another tree missed falling on one of our cars by centimeters, but that limb ended up cracking our driveway apron. We struggled communicating the extent of the damage with our insurance company, and they eventually realized what was needed and paid out on it five months after the incident. Our construction started on March 18th.

It hasn’t been an easy process. It’s emotionally draining on me because there were communication issues with our contractor that he wasn’t taking responsibility for. Then there were minor issues, but issues nonetheless. For instance, they installed waterproofing so the patio would be a dry area, but they cut through one of the barriers. Instead of realizing that was going to be an issue and fixing it themselves, I had to point it out. Then we went out there while it was raining to check it, only to see that there are 3 spots where water is just pouring through the seams. That just takes a lot out of me to have that conversation. They cracked off the top of our sewer cleanout, which not only made a mess in the yard, also caused a backup into our basement tub and toilet once it was glued back on because of a pressurizing issue (we think).

Then there are those hidden things that take energy, such as managing how to move money out of savings (while not exceeding the maximum of six transfers) and keeping track of all the bills, while ensuring the checking account has the right amount of money to cover the bills paid.

RENTAL PROPERTIES

Everyone paid rent on time! I had two technically pay on the 6th, but I sat waiting to see if it showed up before reaching out that morning. One of our tenants bought a house and vacated as of March 31st. They actually had left the house a little early, which was really helpful to us because the house needed a lot of work. The house had been flipped before we bought it. We knew everything was going to eventually need attention, but we hung on as long as possible. The neighborhood is really nice, so it was time to bring the state of the house up to a better standard. It had been “good enough” all these years, but there were definitely some items that should be replaced. This ended up being a huge overhaul, costing us over $10k. I’ll go into all the details in a future post.

NET WORTH

We’ve made a few substantial payments on the deck. We had been investing the money from the insurance company, while we waited for them to finish their estimates and then while waiting for the contractor to begin. Our taxable investment accounts have decreased a bit from that, and they’ll continue to decrease as this project finishes up in the next 2-3 weeks. The market is lower than it was a month ago, but our house values are starting their upward Spring trend, offsetting some of that loss. Overall, our net worth increased over the last month, but only by about $4,500 instead of the drastic increases we had been seeing month-to-month.

I’ve been working on the ‘year in review’ posts for 3 months. I really want to be consistent on tracking our spending and making sure I’m being intentional in our spending. Our main credit card had the nerve to tell me that it was exporting 461 line items for me to categorize and manipulate in Excel. We have 8 credit cards. So that wasn’t a fun realization.

Additionally, if I track it more than once every two years, I may be able to better categorize our spending. For example, a Walgreens purchase may be pictures that I printed, or it could be a prescription. My Amazon purchase may be clothes for the kids they needed, a gift for someone, something in the home improvement category, etc. The entertainment category can include exercise that we’ve paid for (e.g., 5K, ultimate frisbee, kids’ activities) or a trip we went on.

There’s also no direct way that I’m tracking where a credit card expense has been offset by someone paying us back. For instance, I put $980 on my credit card for a trip, but someone paid me $480 for it via Venmo. That offset is in my year’s total transactions, but not in a manner where I can capture it for this year-long-view of expenses. Additionally, we go out to eat at restaurants, but Mr. ODA gets paid for some of those as a secret shopper.

EXPENSES

This doesn’t identify the actual money spent in each category, but it shows how categories align with each other. To simplify this graph (and to allow all bars to even be seen), I combined several smaller categories into an overarching category. For example, the entertainment category includes anything from doing a brewery tour to traveling to another state. Home Improvement includes $10,000 worth of new carpeting, so it’s an outlier. This also doesn’t include expenses that were paid for out of our checking account(s); although nearly all of our expenses are paid via credit card to gain the rewards.

MEDICAL: We spent the first half of the year managing doctor appointments. They were mostly for the baby, and then halfway through the year, I started having serious vertigo issues. The baby was born a little early, had jaundice, diagnosed with reflux and put on medication, and then had trouble gaining weight. My 3rd baby then needed to have formula supplemented, after I nursed two kids and had extra milk to donate to NICU babies. That was an unexpected psychological and financial change. Once he started to become healthier, I hit a wall. After a week of wondering why I kept feeling lightheaded and dizzy, I woke up one morning not able to walk a straight line, and if I even attempted to, I’d throw up. I was diagnosed with an ear infection, which seemed to make sense, but the antibiotics didn’t stop the vertigo episodes. After several specialists, I was given the same thing that I always am: “your symptoms don’t fit neatly into any one category, and I don’t know what’s wrong with you.” Luckily, most of my symptoms have died down at this point. And thankfully, outside of random viruses and a bout of pink eye through 3/5 of us, the others were healthy.

SPORTS: We joined the Y and were really strong for the first 3 months. Once my mom died, I didn’t have it in me to go exercise, and then I got sick for most of the summer with that vertigo issue. Mr. ODA played softball, vintage baseball, and ultimate frisbee; I was able to play some ultimate frisbee and run a 5K. The kids did swim lessons at the Y (and was quite a terrible experience). Our oldest attempted soccer for the second time, and then cried through all practices and games. Our middle thrived in ‘acro’ for the second half of the year. I plan to finish our this semester with her in acro, but I think she’s going to love gymnastics after that.

TRAVEL: We traveled to NY for my mom’s funeral. I took 3 flights in a few days with the baby, all with points (which American Airlines was super easy to work with for last minute flights and using points). We went to the middle of nowhere Tennessee with Mr. ODA’s family, to NY two more times, a short family camping trip, to Indy for some kid-related fun, and a trip to Cincinnati to see Christmas lights and take the kids skiing for the first time. I bought myself new skis (I had been snowboarding for the last 13 years), which led to buying the kids ski equipment (although, it’s noteworthy that we bought them second hand and their skis and boots totaled $100 for two kids). That then led to buying mid-week season passes at our local ski resort. On top of our family trips, Mr. ODA took two work trips, a golf trip, and a mountain biking trip.

GAS: Typically, our gas usage can correlate to our travel because we usually drive somewhere instead of fly with 3 little kids and all the gear they come with. In June and November, we drove to NY, so those have bigger spikes in the graph below (June also included a trip about 4 hours away). In the beginning of the year, we were more interested in staying home because we had a new little baby, but we ventured out more towards the end of the summer.

RESTAURANTS: I was pleasantly surprised to see the amount spent each month in this category. I didn’t feel like we ate at restaurants all that much in the last year, but I was concerned with whether the numbers who support that. There’s an outlier in March because we spent a lot at one restaurant during the week of my mom’s funeral. On Long Island, food is a big deal; while every one else was paying for meals, I felt it was our turn. We don’t need to actually mention how much that meal was. May’s spike was simply the volume of times we went out to eat, and the majority of them being related to Mr. ODA’s secret shopper gig.

HOME: In July, we had a storm come through that wrecked our neighborhood. No one reported the damage to the National Weather Service, which makes me sad because I wanted to know if it was a tornado! We had several trees fall. One took out our deck, another took out our fence, and another cracked our driveway, but missed Mr. ODA’s car by centimeters. We fought insurance for 5 months, and now we’re in the queue to have it replaced some time late Spring.

CAR: We bought a car. That’s $6,000 worth of the “Home Bills” category. Since most of our bills actually can’t be paid by credit card, it’s surprising to have such a high category for that on the graph, but that’s why. They allowed us to do two $3,000 transactions on a credit card so we could get the points, and then we paid the balance by personal check.

GROCERIES: I’d like to watch this spending more in the future. A purchase at Walmart may include non-grocery items (e.g., shoes), but that is being lumped in with the groceries because I can’t possibly siphon out individual transaction expenses for an entire year in one sitting. So here’s a graph of our “grocery” spending per month, but noting such a caveat.

SUMMARY

While I know we’ve had some larger one-time expenses, I’m still not happy to see the amount spent in each category. I feel we’re diligent in our food spending, but I think we can reduce that amount.

I removed rental information, any rewards received, the $6,000 car purchase, and the $10,000 worth of carpet purchase to try to show that our spending is consistent month-to-month. Again, the baby kept us home in January and February, but we’re generally consistent in spending. I hope that I can review our expenses more often going forward so that I can more accurately categorize our spending.

We’re just going to cut to the chase – $4 million net worth! I mentioned that this was a goal for this year. Unlike other years worth of large jumps because of purchasing houses, this was less in our control (granted, our market allocation decisions are what’s driving it…. and by “our,” I absolutely mean only Mr. ODA’s because I don’t do anything in that realm).

RENTALS

Well, we’ve had a quiet month. What’s going to be funny is, I’m going to list the things that we did. Quiet doesn’t mean silent or without effort, but we’ve had a rough go of it over the last year, so this was a welcomed break.

We had termites at a property. We pay $98 annually for their termite warranty program, since we found extensive termite damage and live termites when we bought the house. We’ve had to treat the house several times, so this $98 is a steal. However, I’m wondering why we keep needing to treat the house.

We paid $125 for a plumber to go out to a clogged sink. When we received the invoice, it was for 2 plumbers to go. Between the phone call that they were on their way and the tenant saying they were great, only 35 minutes had elapsed. The company charged us almost $300. Mr. ODA called to ask why they choose to send two plumbers to do a one-man job, while also charging us for it. The owner said it was for liability purposes, which Mr. ODA fought back on. They agreed to a reduced rate, but we were only charged $125, which was less than agreed upon.

We had our third tenant move in, after we unexpectedly had to turnover three houses in the middle of winter. We also were given notice by another tenant that she’s vacating by the end of March. We handled increases for two houses (one handled by a property manager to increase $50/month, and one handled by me to increase by $25/month).

We had one tenant pay on the morning of the 6th with no communication, so I did have our property manager let them know that’s not going to be ok. We also had a usual suspect pay late, with the late fee. However, their communication was frustrating. They said they’d pay on the 6th. At the end of the 6th, they said the money hadn’t cleared like they expected. No communication on the 7th. I asked for an updated on the morning of the 8th, and they said it would be that day. At 11 pm, I hadn’t received anything and reached out. I was then told that money was going into the ATM right then so that she could pay. Sometimes I wish I could do a deep dive into tenant finances so that I could help them out.

PERSONAL

Mr. ODA has a trip in July where a group of guys will hike in the Rockies. Our family is going out before that trip is scheduled to do our own exploring. We booked 4 round trip plane tickets, and Mr. ODA handled the lodging booking for the guys’ portion. That’s almost $3,000 worth of purchases, so our credit cards are higher than usual.

Speaking of the plane tickets. We purchased gift cards from Costco for Southwest. The gift cards are essentially $450 for $500 worth of purchasing power at Southwest. We bought two, therefore saving $100 on the tickets. For an extra few clicks on the computer, and the 15 minutes waiting time before the e-gift cards were delivered to my email, that’s $100 that can be used somewhere else.

We bought a new vanity for our bathroom. That was about $700 for the vanity, faucet, toilet flusher, and mirror. I sold the old vanity (in rough shape) for $30. And because I’m proud that I did most of it on my own, here’s a picture. I needed Mr. ODA’s help with the supply lines because I lost patience with how tightly they were screwed on and my lack of progress. I cut the baseboards down to size, except I somehow measured wrong on one quarter round cut (I was cutting while it was on the wall). Mr. ODA cut and installed the replacement piece for me.

We finished up the ski season. The kids did great. I was really proud of them for sticking with it. We used our season pass well (i.e., exceeding the cost had we bought individual tickets for each visit). I took two of the three kids to the aquarium, and we took the baby for a procedure at a local children’s hospital. We’ve started tee ball for our oldest. Our March is very full and busy, so we’re getting into the swing of things and keeping track of the schedule.

NET WORTH

Well, we far exceeded that $4 million goal. The market went up big, with our biggest changes being in our retirement account, IRAs, and cash. Our cash increase is offset by the lower amount in our Treasury account. Some of the short term bonds were transferred back into our savings account, and we’ve kept that money in savings since our deck replacement is slated to begin.

As an intro for newbies: I write a monthly finance post. These posts started out as a way to manage our dollars spent per category. It evolved to show insight into my monthly money management and thought process. It’s also meant as a way to remind people that they should be looking at their money regularly.

Every month, I’m looking back at my spending, looking at trends on the higher level (e.g., why is my credit card higher than I expected), and sharing the rental property expenses and activities that I’ve accomplished.

I typically post on Thursdays. Unfortunately, life got in the way. I had 98% of this written, but I hadn’t updated our accounts until 10 pm, so this is now posting off-schedule, on Friday morning. Sorry about that!

RENTALS

I suppose with 13 houses, it’s inevitable that I’ll have to keep track of one.. or a few.. to collect their rent. One tenant is set up to pay twice per month (they pay a premium for this). They paid both parts of December late, and the first part of January late. They pay a late fee with that. I had two other tenants pay late by a few days, but they communicated this up front, and I didn’t collect late fees.

I’ve been sharing that I have a tenant who has been behind on rent since October 1 and has communicated very poorly. By the end of December, she was caught up with rent due, but no late fees. We’re now 11 days into January without any payment. My frustration with her was that she didn’t communicate at all for the first two months, and didn’t keep her word on anything that she said she was going to do, but didn’t tell us that something would change. I always say that I’m willing to help and work with you, but you have to talk to me. If I have to beg you to tell me what the plan is, I can’t help.

I paid a carpet cleaner $250 and paid a painter $2000 for a house that we’re turning over. The carpet was new before the last tenant, but they were there for over 3 years, so it had to be done. They didn’t damage the walls, but my property manager said that all the walls looked like different colors, and I didn’t trust “touching up” 4 year old paint. The paint looks amazing, so I’m happy I went for the whole house.

I paid just over $1000 as a deposit on 3 new windows for a house, which are scheduled to be replaced on Monday (a couple of weeks for new windows far exceeded my expectations!). We had replaced the majority of windows when we bought the house. However, at the time, the kitchen and bathroom windows were considered an irregular size, and we were told they were going to be $2000 just themselves, when we were paying $2000 for all the other windows. I don’t know what pricing scheme changed in 5 years, but now all sizes are the same price, and the 3 of them are $2000 now.

We had a tenant ask to be released from his lease, which we concurred to. We had terms associated with that, which I’ll share in a separate post. We were able to get a couple into that house with no loss of rent, which has been appreciated.

We’re under contract with our handyman to do work on a house, so that’s over $5,000 of cost that is waiting to rear its head out there.

PERSONAL

This was a month of spending in activities. I signed up for a 5k in August with “early bird” pricing, our daughter’s acro class had semester tuition due, and the kids’ monthly school tuition was paid as usual. Mr. ODA bought a new battery for his car and installed that. On somewhat of a whim, we replaced our back door, which was over $1100 added to Mr. ODA’s credit card.

Just before Christmas, we took a trip. It was just to Cincinnati, which we regularly do as a day-trip. However, we wanted to accomplish a few things this time around. We went to Top Golf for 90 minutes and lunch, let the baby nap at the AirBnB, went to Zoo Lights, spent the night, and then went skiing the next morning (the kids’ first time!). We already purchased season passes (and equipment) for skiing for 4 of us, and had already purchased the zoo annual membership. Without the cost of those two things, our trip cost $330 for Top Golf, lodging, parking (we stayed in the city), a ski lesson for our 5 year old, and food. Our lodging for 1 night was nearly $200 and was significantly more than we’d typically spend on lodging. However, we’re still in a phase of life where the baby needs the be in a space by himself so he sleeps for a nap and through the night. That means we look for a place with at least 2 bedrooms and 2 bathrooms, or 3 bedrooms and 1 bathroom (bonus points for master-sized closets or an extra bathroom with no windows for me to black out). We then made 2 day trips since then, and the kids are doing awesome on skis.

NET WORTH

Our cash has decreased, but that was offset to taxable investments because of our Treasury Direct accounts. Even with our extra spending, our credit card balances are comparable to last month’s. The increase in net worth from last month is mostly due to increases in our investment accounts.

This year’s goal is to hit $4 million net worth. Mr. ODA said that to our financial advisor via Instagram, and he didn’t share that publicly because it wasn’t relatable. The point in sharing here is that, well it’s January and people set goals, and to note that even if this goal specifically isn’t attainable to you in the short term, know that we also once had an account balance well below where we’re currently at. Consistent investing in the market (maxing out the 401k, maxing out the Roth IRAs, and establishing regular investing and watching the market) is a large contributing factor to where we are 10 years later. If I take the investment properties out of the equation, we’re still over $2 million net worth. That doesn’t happen overnight, and it’s something you can start working towards today.

We purchased a house in June 2022. Most of the house had been updated or was in good shape, but the master bathroom was the original from 1992. This isn’t a bad thing, but bathroom designs have changed a lot since that time. Aesthetically, the bathroom would have been fine. Functionally, I didn’t want to shower in a 2.5′ by 2.5′ shower stall, and the higher standard of vanity height is something I’ve gotten used to. The day we closed, we started gutting the bathroom.

BATHROOM EXPERIENCE

Our first ever renovation project was a bathroom that we gutted, redesigned, and rebuilt in our first home we owned, back in 2013. The house was a foreclosure, and it had been flipped by the bank. The place looked good, but it didn’t last. The bathroom shower tiles were cracking as soon as we moved in. We took walls down and rebuilt them because of mold, we moved the door to allow for a better vanity set up, and we moved the toilet so that you weren’t walking around the vanity to get to it. We had been quoted $25k for a contractor to do it. We spent $4k on materials.

Our last home was a new-build and had an unfinished basement with a bathroom rough-in. We had my dad’s help setting the plumbing, and then we finished it out ourselves. After we did the first bathroom, we said we wouldn’t do vertical tiling again. We really just learned not to use 12×12 tiles on the wall.

The bathroom cost us about $6k to complete. While everyone was being quoted $75k-120k for a finished basement with bathroom, we did almost all the work ourselves (dad’s help on bathroom and setting studs, hired a drywall finisher, and we didn’t lay our own flooring) for about $20k.

We also did a quick bathroom refresh in our current home. The basement bathroom here was forgotten. It hadn’t been cleaned or updated (most of the house had switches and outlets changed to white from yellow, but not this room). For less than $1,000, we laid a new floor, updated the trim, replaced the vanity and toilet, painted, updated the accessories and mirror, and replaced the switches and outlet. We didn’t touch the tub or the faucets in there.

BACKGROUND

The bathroom was an L-shape. There was a 114″ vanity with a full length wall mirror over that. It also had 2 5-light wall mounted light fixtures over each sink (excessive!). Then the shower was your typical plastic molded shower stall with a frosted glass door. It was 2.5′ x 2.5′. Around the L was the toilet (awkward positioning, really), and beyond that was the soaking tub with built-in molded steps. Oh, and there was a ceiling fan over the vanity.

THE PLAN

We needed to take everything out so we could see our options. We gutted the bathroom pretty quickly, but we dragged our feet on the rebuild. It worked out in my favor though; I’ll come back to that.

The L-shape encompasses the master bedroom’s closet. It’s a walk-in closet, but it’s not spectacular. We tried to make a plan where we knocked down the closet walls and reconfigured the whole space, but the window placement hindered us, along with some of the desired sizes of fixtures. Once we gave up on incorporating the closet space, it was clear we just wanted to make the shower more functional.

As we started laying blue tape to map out the size of the shower, we realized we were hindered by the closet walls. If we made it too big, we lost the ability to walk around the L-shape comfortably. The whole point here was that we wanted a bigger shower. We settled on as wide as we could make it, while still being able to fit around the corner (generally looking at 3′ wide, which is standard hallway width).

At the beginning, I mentioned that I wanted to washer and dryer moved from the garage entry. Mr. ODA said we’d do it “later.” But the walls were opened now… so why not now? He came around. We hired an electrician to move the dryer electric from the room off the garage, directly above it to our bedroom, and then up into the attic to move over and come down into the bathroom. That meant the width of the shower was now maxed at how wide our washer/dryer was to get through the hole.

We bought a waterproofing system to build the shower any size we wanted (versus a shower pan), and we ended up about 3.5′ x 5′. We dropped the vanity section to 7′, and dropped our lighting to 2 2-light fixtures. 🙂

We eventually will add glass to the shower area (there’s a curtain there for now). The master bathroom is the most infrequently cleaned area of my house (and I clean a lot!), so maintaining a glass shower enclosure that’s used daily is just not high on my priority list. Mr. ODA had built a shower bench for our last house’s shower, and by some miracle, it fit perfectly in this newly built shower. We also reused the floor tile option because we wanted a statement in here, but we were too scared to commit to a pattern and it not look right; we knew what this pattern looked like, so we kept it.

The plumbing for the washer and dryer was a concern. We were able to use the old tub’s drain to be the washer drain. We were also able to use the supply lines. However, since the supply lines were on an interior wall, and we were nervous about moving them to an exterior wall (so it would be behind the washing machine), we kept them there. The width of the room didn’t allow for clearance for the supply lines to be hidden down further, so the lines fall across the top of the washer. While not aesthetically great, everything else about this is so much more functional and makes me happy.

MUD ROOM

The washer and dryer moving to where the tub was in the master bathroom meant we could create a mud room. This was a really big deal to me. We park in the garage. Our garage door is basically always open and this is how people come and go. I wanted a functional space that wasn’t cramped by a washer and dryer that you were walking around.

Additionally, the previous owner had changed the closet function to be 2 shelves. There was no hanging room for coats, and there was no storage for mops or vacuums on the first floor. We moved the middle-of-the-closet shelf to be a higher shelf, added the dowel so we could hang coats, and cut the bottom shelf in half to still allow for some storage options, but also allow for vacuum storage.

We’ve since added shelving over mini fridge, and there are bins for shoes in the cubbies. In our last house, we had a bar area in the basement where this fridge was. We had originally planned for it to be in the basement in our current house also, but we don’t spend as much time as we thought down there. It was a perfect fit to include it in the mud room and build the bench to incorporate it.

By moving the washer and dryer from this room (for our own labor and about $400 worth of an electrician), we made our house significantly more functional. As I grow older (and move an absurd amount of times), I’ve learned how much more important it is for my house to function.

SUMMARY

A quick facelift to a bathroom is a pretty easy project. Moving plumbing, electric, and walls creates a few more levels of difficulty. However, it’s not impossible. We’ve learned over the years that if we act as our own general contractor (hiring out piecemeal), we can save a lot of money. In this post-covid-world, contractor costs are high. If we hired out this entire bathroom, I don’t doubt that we could have been looking at $45-50k with all the things that were to be moved. Instead, it cost us about $5,000 worth of materials and our time.

Our time was definitely at a premium. We dragged our feet on decision making, while focusing on other areas of the house. The kids’ bathroom is directly outside our bedroom, so it wasn’t a hassle for us nor was there an immediate need for us to be back in our own bathroom. We got the floor tile down as fast as we could before we officially moved in, since our washer and dryer would need to be placed. That lit the fire for our toilet and vanity to be installed too. But the shower was a different story. We got it framed out, but didn’t start laying tile and grouting until after our 3rd was born. I thought I would feel better doing that work once I wasn’t pregnant anymore, but I didn’t factor in the baby needing to be help all day long, so that created quite a challenge. But we did it.

We gutted the bathroom in mid-June, and we had it completed done (well, except for the shower glass that I just don’t even want) by Christmas. While we took our time doing it, the best parts are how much more functional and comfortable the house is, and how it cost us about 10% of what it would have been if we hired it out.

Life is different these days. Our 3rd child was born on Thanksgiving, and we’ve been finishing up some projects around the house. We’ve had a few things happen with rentals, and, basically, I’m just tapped out to keep up with blogging. Mr. ODA asked me what our net worth is at these days, and so I’m updating our spreadsheet.

“JANUARY”

It’s January, so that means I have to create my two main Excel workbooks for the year: the paycheck to paycheck monitoring of our expected income and expenses, and the management of each rental property. The paycheck to paycheck spreadsheet is where I have a line item for each house’s rental income each month, each house’s mortgage payment (where applicable), and then all our bills owed (credit cards, utilities, investments). I break this down by paycheck because that’s the easiest way for me to make sure I have enough income to offset the bills owed during that two-week period. That worksheet in that workbook feeds my net worth calculations, where I also update loan balances. There is actually several tabs in this workbook, but those are the main two. I finally got that all set up today. I haven’t even started creating the investment property workbook.

January also means I have to go through last year’s investment property workbook to verify all the expenses listed are supported by receipts, that all receipts I have are recorded, and that my income is accurate. Then I read off the data to Mr. ODA, who enters it into an online tax portal to file our taxes. I haven’t started that daunting task either.

RENTALS

We had one of our properties flooded by a burst pipe. That’s a mess and is hardly making progress because the tenant’s renters insurance can’t get the tenant property out of the house. We had an electrical issue with a hot water heater in another property. That got fixed, but now I am in a position where I have to fight Home Depot about their shoddy installation a year ago and have them reimburse the cost of rewiring. I finally moved forward with the judgement against a tenant for destruction of property, and our attorney established that collections account.

Surprisingly, we didn’t have any issues with rent payments in December or January. Usually I hear from one or two houses that they need a couple of weeks to pay all of rent. While not everyone was on time, they communicated well and were only a few days late. One tenant reached out and asked if they could pay rent on the 6th (since that’s Friday, and pay day); I told them not to worry about the late fee and that would be fine. Little gestures like that can make a big difference for your tenant’s life.

I sent a letter to our property manager for the KY houses that we’re releasing them at the end of this month, so that’s a new development that is taking my time as well. You’d think my property management company would have a way to communicate this change with the tenants, but alas, that would be too logical. Wish me luck while I add 3 more houses under my own purview. While we moved to KY two years ago, it was easier to maintain status quo with having a property manager. Unfortunately, it has taken too much of my effort to manage the property manager and to fight for our money.

PERSONAL

We finished our master bathroom in the home we bought over the summer (and the room we gutted immediately… only took 6 months to get us to the finish line… and by finish line, there’s still paint touch ups to be had). We bought all the supplies to gut and renovate the basement bathroom in this house. Mr. ODA built a bench for our kitchen table so that we have more seating easier. We made the plans to get the mudroom bench and shelves in, and hopefully those supplies will be bought this weekend.

Truthfully, while I updated most of my net worth spreadsheet in December, I never posted it because I don’t even know where all our money is. When we sold our personal residence at the beginning of November, we were handed a large check. In the past, that check type mostly went towards a downpayment on a new house, but that wasn’t the case this time. Mr. ODA immediately started investing that money in short term treasury accounts that I can’t even begin to explain. Between that account, another savings type account, and our regular investment account, I can update what I see online, but I don’t know what I may be missing. I’m hoping Mr. ODA will chime in soon to describe the type of investment decisions he’s made.

NET WORTH

Several property value assessments declined over the last couple of months. So while our investments are on the upswing from November’s update, those updates to property values have caused a decrease to our net worth.